Sb 3022 Relating to Ferries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Environmental Assessment: Issues Surrounding the Exclusion of Projects Significantly Affecting Hawai`I's Fragile Environme

The Environmental Assessment: Issues Surrounding the Exclusion of Projects Significantly Affecting Hawai`i’s Fragile Environment Jordon J. Kimura * I. INTRODUCTION ................................................................................. 169 II. THE HEPA........................................................................................ 171 A. Purposes of the HEPA............................................................... 171 B. The Environmental Review Process under the HEPA .............. 172 1. Preliminary Matters Regarding the Environmental Review Process ................................................................. 172 2. The Environmental Assessment ........................................ 174 3. The Environmental Impact Statement............................... 175 4. Appeals.............................................................................. 175 C. Hawai`i Supreme Court Decisions Interpreting the HEPA ...... 176 1. The court interprets “use of state or county lands” broadly to increase review of actions ............................................. 176 2. The court emphasizes consideration of the secondary impacts of a proposed action under the HEPA.................. 177 D. Legislative Action Temporarily Amending the HEPA............... 178 III. ENVIRONMENTAL IMPACTS OF ACTIONS FALLING OUTSIDE THE SCOPE OF THE HEPA AND USING STATE OR COUNTY LANDS ............ 179 A. The Hawai`i Superferry............................................................ 180 1. The HSF traverses marine environments and may -

Of 1 House Record

Page 1 of 1 House Record From: Todd Payes [[email protected]] Sent: Wednesday, October 24,2007 12: 16 PM To: House Record Subject: re ATTN: House Committee on Transportation and House Committee on Finance DATE: Thursday, October 25,2007 TIME: 9:00 a.m. Auditorium, State Capitol HB 1 RELATING TO TRANSPORTATION Requires the Department of Transportation to perform an environmental impact statement (EIS) for certain improvements made to commercial harbors. Permits operation of large capacity ferry vessel company prior to completion of EIS upon meeting certain minimum conditions. Establishes a temporary Hawaii Inter-island Ferry Oversight Task Force. Dear Chairs Souki and Oshiro: My name is Robert Todd Payes and I strongly support Hawaii Superferry. Reasoning for my support is to help grow our local economy and making inter island more affordable to transfer people, auto, produce and goods to and from islands. I also think the superferry will be a safe guard for the state before and after WHEN we have a major natural disaster like a hurricane and or tidal wave. Thank You, Todd Payes R.T. Payes Corp. 810 Ekoa Place Honolulu, Hi. 96821 Cell: (808) 554-3230 Fax: (808) 373-7139 Email: rtpavesQhawaiiantel.net Page 1 of 1 House Record From: Mark Allen [[email protected]] Sent: Wednesday, October 24,2007 11 :53 AM To: House Record Subject: HB 1 RELATING TO TRANSPORTATION A'TTN: House Committee on Transportation and House Committee on Finance DATE: Thursday, October 25, 2007 TIME: 9:00 a.m. Auditorium, State Capitol HB 1 RELATING TO TRANSPORTATION Requires the Department of Transportation to perform an environmental impact statement (EIS) for certain improvements made to commercial harbors. -

Supplemental Environmental Impact Statement, a Regulatory Impact Review and an Initial Regulatory Flexibility Analysis

Amendment 14 to the Fishery Management Plan for Bottomfish and Seamount Groundfish Fisheries of the Western Pacific Region Including A Final Supplemental Environmental Impact Statement, A Regulatory Impact Review and An Initial Regulatory Flexibility Analysis MEASURES TO END BOTTOMFISH OVERFISHING IN THE HAWAIIAN ARCHIPELAGO Western Pacific Regional Fishery Management Council 1164 Bishop Street, Suite 1400 Honolulu, Hawaii 96813 December 19, 2007 ii Amendment 14 to the Fishery Management Plan For The Bottomfish and Seamount Groundfish Fisheries Of The Western Pacific Region Including A Final Supplemental Environmental Impact Statement A Regulatory Impact Review and An Initial Regulatory Flexibility Analysis MEASURES TO END BOTTOMFISH OVERFISHING IN THE HAWAIIAN ARCHIPELAGO December 19, 2007 Responsible Agency: Responsible Council: NMFS Pacific Islands Region Western Pacific Regional Fishery 1601 Kapiolani Blvd., Suite 1110 Management Council Honolulu, HI 96814-4700 1164 Bishop St., Suite 1400 Honolulu, HI 96813 Contact: Contact: William L. Robinson Kitty M. Simonds Regional Administrator Executive Director Telephone: (808) 944-2200 (808) 522-8220 Fax: (808) 973-2941 (808) 522-8226 Abstract: Based on fishery information and 2003 data analyzed by the National Marine Fisheries Service’s (NMFS) Pacific Islands Fisheries Science Center, NMFS determined that overfishing of the bottomfish species complex was occurring within the Hawaiian Archipelago with the primary problem being excess fishing mortality in the main Hawaiian Islands (MHI). The NMFS Regional Administrator for the Pacific Islands Regional Office notified the Western Pacific Regional Fishery Management Council (Council) of this overfishing determination on May 27, 2005. In response, the Council prepared Amendment 14 to the Bottomfish Fishery Management Plan (FMP), which recommended closure of federal waters around Penguin and Middle Banks to fishing for bottomfish in order to end the overfishing. -

Annual Labor Market Overview

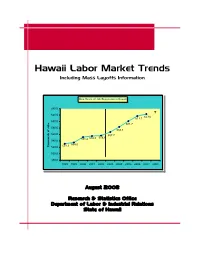

Hawaii Labor Market Trends Including Mass Layoffs Information Nine Years of Job Expansion in Hawaii 640.0 ? 620.0 623.6 617.1 600.0 601.7 580.0 583.4 560.0 567.7 556.8 551.4 555.0 540.0 535.0 Thousands of Jobs 520.0 531.3 500.0 480.0 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 August 2008 Research & Statistics Office Department of Labor & Industrial Relations State of Hawaii Research and Statistics Office Labor Market Research 830 Punchbowl St., Room 304 Honolulu, Hawaii 96813 Phone: 808.586.9025 Fax: 808.586.9022 Email: [email protected] Website: www.hiwi.org Research and Statistics Office Table of Contents Page Introduction ...................................................................................................................................... 1 Executive Summary......................................................................................................................... 1 Recent Significant Developments Spotlighting Mass Layoffs.......................................................... 2 Looking Ahead… Short- and Long-Term Job Outlook ................................................................................................. 4 Looking Back… Labor Market Highlights................................................................................................................... 7 Hawaii’s Job Expansion Continues for Ninth Year .......................................................................... 8 Industry Highlights ........................................................................................................................ -

Environmental Impact Assessment Committee Newsletter

them to begin seeking the best legal representation STANDING ON BOARD THE SUPERFERRY: available. By prevailing against the U.S. Navy, the SIERRA CLUB V. HAWAII DEPARTMENT NRDC and its fellow plaintiffs have not only inspired OF TRANSPORTATION other environmental groups around the country, but they have also issued a stern warning to the entire Lisa A. Bail regulated community that no organization is immune Goodsill Anderson Quinn & Stifel LLP from liability in this new era of heightened environmental awareness. Introduction In Sierra Club v. State of Hawaii Department of Transportation, 167 P.3d 292 (Haw. 2007), the AMERICAN BAR ASSOCIATION Hawaii Supreme Court ruled not only that Sierra Club SECTION OF ENVIRONMENT, ENERGY, and other plaintiffs had standing to pursue their claims AND RESOURCES under the Hawaii Environmental Policy Act, Chapter 343 of the Hawaii Revised Statutes (Hawaii EIS Law), Calendar of Section Events but also invalidated an exemption determination made by the State of Hawaii Department of Transportation Key Environmental Issues in U.S. EPA (DOT) for improvements necessary to accommodate Region 2 Hawaii Superferry at Kahului Harbor. The decision, June 3, 2008 which received international media coverage, is notable New York, New York for significantly expanding the category of persons who (Cosponsored with EPA Region 2, New have standing to pursue claims under the Hawaii EIS York State Bar Association, New Jersey Law. State Bar Association, New York City Bar, and Fordham Law School) Procedural History Global Warming II: How the Law Can The Hawaii Superferry project generally involves a Best Address Climate Change new inter-island ferry service between the islands of (36th National Spring Conference on Oahu, Maui, Kauai, and the Big Island. -

Resolution No

Resolution No. 05-46 REQUESTING PREPARATION OF AN ENVIRONMENTAL IMPACT STATEMENT FOR THE PROPOSED STATEWIDE HAWAII SUPERFERRY PROJECT WHEREAS, the Hawaii Superferry, in association with Austal USA, is proposing to provide non-stop, roundtrip ferry services daily between the islands of Hawaii, Kauai, Maui, and Oahu, commencing in 2007; and WHEREAS, this service will provide Hawaii with the world's newest and largest passenger vehicle catamaran, connecting the islands with a new "H4 highway", and could transform the State and Maui, positively and/or negatively; and WHEREAS, this interisland transportation system plans to expand its service by 2008 with the capability of transporting 1,732 people and 564 vehicles daily to Kahului Harbor on Maui; and WHEREAS, Hawaii Superferry intends to provide an efficient, environmentally friendly, state-of-the-art ferry service for passengers and vehicles between the islands at approximately half the price of flying; and WHEREAS, this system could expand our State's transportation infrastructure and economy by possibly lowering the cost of travel and shipment of goods and agricultural products; and WHEREAS, although this service promises many benefits to Maui's residents, it could also create or exacerbate existing problems for Maui's rural environment; and WHEREAS, Chapter 343 of Hawaii Revised Statutes (HRS), Environmental Impact Statements, requires the preparation of an Environmental Assessment and/or Environmental Impact Statement for any proposed action that utilizes State lands or State funds; -

The Hawaii Superferry SSHHAARRIINNGG

I N F O R M AT I O N The Hawaii Superferry SSHHAARRIINNGG Information sharing leads to operational success. by CAPT VINCE ATKINS former Commander, U.S. Coast Guard Sector Honolulu ENS MEGHAN HOUGH U.S. Coast Guard Sector Honolulu The complexities of maritime operations are often com- pounded by factors such as the variability of the sea itself, differing and sometimes overlapping legal authorities, and the presence of a wide range of concerned agencies with varying competencies and capabilities. Information sharing reduces operational complexity and sets the stage for success. A recent operation in Hawaii underscores how information sharing, taken in the broadest sense, can increase interagency effec- tiveness and public understanding. Hawaii Superferry (HSF) came to Hawaii to start a high-speed ferry service between the Hawaiian islands An Alakai protester in Nawiliwili Harbor, of Oahu, Maui, and Kauai. The Superferry vessel, the Kauai, demonstrates directly in front of Alakai, is a 350-foot high-speed catamaran designed to the Alakai. Honolulu Star-Bulletin pho- tograph by Mr. Tom Finnegan. carry 866 passengers and 282 vehicles. A Hostile Operating Environment Unfortunately, strong opposition from segments of the Alakai’s initial operations were greeted by an estimated local population shadowed the start of Alakai’s service. 300 protestors in Kauai. People gathered outside the Citizens and environmental groups opposed to this ferry’s shoreside facility, taunted would-be passengers, new service voiced several concerns, citing Alakai’s lack blocked vehicles, and, in some instances, caused minor of an environmental impact study, the possibility of in- property damage. Protesters on shore threw coconuts creased traffic congestion, and the potential for intro- and other debris at Coast Guard responders and several ducing invasive species and harming marine life. -

View Annual Report

2008 SUMMARYSUMMARY REPORT REPORT TO TO SHAREHOLDERS SHAREHOLDERS BUILDINGBUILDING AA BRIGHTER TOMORROW HawaiianHawaiian El ElEEctricctric industriEs, i inc.nc. (H(HEEii),), through through its its subsidiaries, subsidiaries, HHawaiianawaiian E Elelecctritricc ComComppanany,y, INc. and American S SAAvvingsings B Banank,k, F.S.B., F.S.B., providesprovides essential essential electric electric and and financialfinancial services ensuring a brighter futurefuture forfor thethe communitiescommunities it it serves. serves. HEI Hawaiian Electric Company American Savings Bank INcOME FROM Basic Earnings pER Share — RETURN ON AvERAGE DIvIDENDS pER Continuing Operations (1) Continuing Operations (1, 2) cOMMON EQUITy — cOMMON SHARE (2) (1) (millions of dollars) (dollars) Continuing Operations (dollars) (percent) 150 2.00 15 1.5 1.24 120 1.2 1.50 90 10 90 1.07 0.9 1.00 6.8 60 0.6 5 0.50 30 0.3 0 0 0 0 99 02 05 08 99 02 05 08 99 02 05 08 99 02 05 08 (1) 2008 consolidated and bank net income included a $36 million after-tax charge ($0.42 per share) resulting from American’s balance sheet restructuring. The balance sheet restructuring reduced the size of the bank’s balance sheet by approximately $1 billion, while enabling the bank to maintain its earnings power on a lower capital base and dividend excess capital to HEI. Return on average common equity — continuing operations, adjusted to exclude the $36 million after-tax balance sheet restructuring charge, was 9.3 percent. ( 2) Adjusted for a 2-for-1 stock split in June 2004 LETTER TO SHAREHOLDERS FINANCIAL -

A Summary of Ship Strikes and the Operation of a High Speed Ferry in Hawai‘I

Do not cite without author‟s permission SC/63/E4 A summary of ship strikes and the operation of a high speed ferry in Hawai‘i 1 1 2 2 LYMAN , EDWARD; DAVID K. MATTILA , DAVID SCHOFIELD AND JEFF WALTERS 1 NOAA, Hawaiian Islands Humpback Whale National Marine Sanctuary (HIHWNMS), 726 S. Kihei Road, Kihei, HI 96753 USA 2 NOAA, National Marine Fisheries Service (NMFS), Pacific Islands Regional Office, 1601 Kapiolani Boulevard, Suite 1110, Honolulu, HI 96814 USA ABSTRACT The population of North Pacific humpback whales, Megaptera novaeangliae, that mate and calve in the coastal waters surrounding the Hawaiian Islands each winter, has grown at approximately 6% annually since the cessation of whaling. In 2006 it was estimated that approximately 10,000 humpbacks use this near-shore habitat. This growing population has coincided with a growing concern about whale-vessel collisions, which have been increasing over the past decade. Given humpback whale preference for shallow water (<183 m) and the use of the same habitat by a majority of the vessel traffic, a high risk of contact exists between whales and vessels, The majority (~92%) of vessels known to be involved in whale-vessel collisions have been less than or equal to 19.8 m in length. In addition, more than half (61%) of vessels were traveling 13 kts. or less. Therefore, the introduction of a large (105m), high-speed (35 kt) ferry running between the main Hawaiian Islands, and potentially transiting the shallow waters with the highest known densities of whales, became the focal point of these growing concerns. -

Waikīkī Wiki Wiki Wire

Volume VIII, No. 33 Waikīkī Improvement Association Aug 16, 2007 — Aug 23, 2007 Waikīkī Wiki Wiki Wire New Ainahau Monument Dedicated To the sound of Scottish pipes, the dedication of a plaque and monument marking the site of Princess Kaiulani’s famed Ainahau home took place this Thursday evening, August 16, 2007, at a “Garden Gathering and Ho‘okupu”. The plague and monument stands in a small park that is part of the Ainahau Vista Waikīkī Project. Ainahau Vista Waikīkī is a senior affordable rental project by the Hawai‘i Housing Development Corporation (HHDC), a private non-profit organization. HHDC dedicated the park and provided the space for the monument. Randy Moore, chair of HHDC, and Gary Furuta, the project manager, have supported commemorating the Princess since learning of the site’s history. Mitsunaga construction and their architect, Kazu Yato, donated the design and the building of the monument at no cost to the project. The plaque resulted from the devotion of Kristin Zambucka, the author of a biography of the Princess, and the generosity of her associates, Princess Regina Kawananakoa, Condesa Azria, Nora Meijide Gentry, Bruce McEwan and Ramona Harris. Ms. Zambucka designed the plaque and her associates contributed funds for its making. The monument and plaque, clearly visible from Ala Wai Boulevard, represent a major new addition to the landscape of Waikīkī, honoring its history and culture. Inside this issue: Beachwalk bypass project nearing completion 2 HTA board announces committee assignments 6 Outrigger honors Duke by supporting OceanFest 3 Hawai‘i Convention Center announces new hires 6 Aloha Airlines wins UH Warriors charters 4 HTH Corp. -

Procedural Standing and the Hawaii Superferry Decision: How a Surfer, a Paddler, and an Orchid Farmer Aligned Hawaii’S Standing Doctrine with Federal Principles

Procedural Standing and the Hawaii Superferry Decision: How a Surfer, a Paddler, and an Orchid Farmer Aligned Hawaii’s Standing Doctrine with Federal Principles Stewart A. Yerton* INTRODUCTION ........................................................................................ 331 I. BACKGROUND ................................................................................... 333 A. Federal Standing Doctrine ....................................................... 334 1. Injury in fact: Article III standing .................................... 334 2. The zone of interests test: Standing’s prudential requirement ........................................................................ 335 3. Standing in federal environmental cases ........................... 337 a. Footnote 7: Justice Scalia articulates procedural standing in dicta ................................................................................... 338 b. Supreme Court disfavors Scalia’s critique of citizen suits .. 342 c. Federal courts use footnote 7 standing ................................. 343 B. Hawaii Standing Doctrine ........................................................ 345 1. Professor Davis’s “needs of justice” standing principle .... 346 2. Hawaii’s environmental standing limits ............................ 347 C. The Superferry Case ................................................................. 352 II. ANALYSIS ......................................................................................... 354 A. Sierra Club’s Bold Litigation Strategy .................................... -

From: Scott Kirk <[email protected]> Date: August 28, 2007 6

From: Scott Kirk <[email protected]> Date: August 28, 2007 6:36:49 PM HST To: Lori Abe <[email protected]> Subject: Hawaii Superferry Q&A from Aug 28 Press Conference Hawaii Superferry, Inc. Q&A NOTES FROM AUGUST 28 PRESS CONFERENCE 1. When do you think you will start voyages to and from Kauai? Our top priority is to operate a safe and reliable ferry system for Hawaii’s residents. We would, of course, like to resume service to and from Kauai as soon as possible. However, we do not have a specific timeframe. The Coast Guard has advised us that they are continuing to assess the situation. 2. Do you think that you jumped the gun, so to say, in starting service early? No. We began service because we were ready to go. 3. What kind of assurance do you need to begin service again? We will resume service once we receive assurances of safe passage from the Coast Guard and the DOT. 4. The Kauai Police Department had 110 officers. Is that not enough to handle the potential threat of the protestors? The Coast Guard notified us this afternoon that they could not assure a safe passage for the Alakai into Nawiliwili Harbor. 5. What assurances were you given by the Coast Guard and DOT prior to last night’s voyage that prompted your decision to continue servicing Kauai? We believed that the Coast Guard was adequately prepared for the Alakai to enter the port. 6. What did the Coast Guard tell you – what did they say exactly? The Coast Guard said that they could not recommend that our ship enter Nawiliwili harbor and are continuing to assess the situation.