UNO Template

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Seven Principles of WOM and Buzz Marketing Panos Mourdoukoutas L George J

The Seven Principles of WOM and Buzz Marketing Panos Mourdoukoutas l George J. Siomkos The Seven Principles of WOM and Buzz Marketing Crossing the Tipping Point Prof. Panos Mourdoukoutas Prof. George J. Siomkos Long Island University Athens University of Economics & Business Dept. Economics Patission 76 C.W. Post Campus 103 34 Athens 720 Northern Blvd. Greece Brookville NY 11548 [email protected] USA [email protected] ISBN 978-3-642-02108-4 e-ISBN 978-3-642-02109-1 DOI: 10.1007/978-3-642-02109-1 Springer Heidelberg Dordrecht London New York Library of Congress Control Number: 2009928097 # Springer-Verlag Berlin Heidelberg 2009 This work is subject to copyright. All rights are reserved, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, reproduction on microfilm or in any other way, and storage in data banks. Duplication of this publication or parts thereof is permitted only under the provisions of the German Copyright Law of September 9, 1965, in its current version, and permission for use must always be obtained from Springer. Violations are liable to prosecution under the German Copyright Law. The use of general descriptive names, registered names, trademarks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. Cover design: WMXDesign GmbH, Heidelberg, Germany Printed on acid-free paper Springer is part of Springer Science+Business Media (www.springer.com) To Georgios and Dimitris Preface In his best-selling book, The Tipping Point, Malcolm Gladwell has popularized the concept of social epidemics, the social changes brought about by sudden changes in human behavior caused by products or ideas that disseminate and spread like infectious diseases and shape history. -

Estrategias, Passwords, Códigos Y Consejos De La

TRUCOS A-Z PlayStation 3 TrucosESTRATEGIAS, PASSWORDS, CÓDIGOS Y CONSEJOSPS3 DE LA A A LA Z No te muevas de la esquina don- 05 CHINA Los colores que debes recordar ARMORED CORE 4 de empieza el pasillo. Regresa • M1: en la edificación gemela a son los siguientes, toma nota: • Puntos FRS fáciles: al ascensor y deja que Hicks te la que esconde el primer panel, Blanco: aldeano cotidiano del )A Si quieres conseguir puntos FRS cuente la localización de las ca- pero al otro lado del canal, en que podrás obtener información. completa el modo normal y si- bezas químicas. un rincón. Amarillo: objetivo de asesinato. ALONE mulador. • M3: nada más encontrar a • M2: en la casa que hay a la iz- Rojo: soldado. IN THE DARK Selecciona el modo difícil y com- Hicks, gira a la izquierda y ve quierda del cobertizo de pla- Azul: aliado. CONSEJOS pleta una misión con un rango in- hasta el fondo del pasillo, para cas metálicas azules, en el se- • Utiliza la visión especial: ferior a S. dar con la maleta metálica pe- gundo piso. El agente Edward Carnby puede Vuelve a jugar la misma misión gada a la pared de la derecha. • M3: tras el contenedor de co- utilizar su percepción con R3 pa- en dificultad normal y logra el IRAQ lor verde que hay al fondo del ra destacar elementos que pue- rango S. Conseguirás un punto • M1: justo antes de abandonar todo, justo donde el helicóptero den ser importantes. FRS rápidamente. Vuelve a jugar el primero de los bunker donde deja caer a los soldados del ejér- Si ves que andas un poco perdi- todas las misiones que no tengas entras (y antes de volar el heli- cito chino. -

2K Unveils Stellar Video Game Line

2K Unveils Stellar Video Game Line-up for 2006 Electronic Entertainment Expo; Line-up Includes Highly- Anticipated Titles such as The Da Vinci Code(TM), Prey, Sid Meier's Civilization IV: Warlords and NBA 2K7 May 10, 2006 8:31 AM ET NEW YORK--(BUSINESS WIRE)--May 10, 2006--2K and 2K Sports, publishing labels of Take-Two Interactive Software, Inc. (NASDAQ: TTWO), today announced a strong line-up for Electronic Entertainment Expo 2006 (E3) taking place at the Los Angeles Convention Center from May 10-12, 2006. From 2K, the line-up includes titles based on blockbuster entertainment brands such as The Da Vinci Code(TM) and Family Guy and popular comic book franchises The Darkness and Ghost Rider, as well as original next generation games such as Prey and BioShock. 2K is also featuring highly-anticipated titles from Firaxis Games, including Sid Meier's Civilization IV: Warlords and Sid Meier's Railroads! as well as the Firaxis and Firefly Studios collaboration title CivCity: Rome. Other eagerly awaited titles include Stronghold Legends(TM) along with Dungeon Siege II(R): Broken World(TM) and Dungeon Siege: Throne of Agony(TM), based on the acclaimed Dungeon Siege(R) franchise. In addition, the 2K Sports line-up features the next installments from top-rated franchises such as NHL 2K7, NBA 2K7 and College Hoops 2K7. 2K Line-up Includes: BioShock BioShock is an innovative role-playing shooter from Irrational Games who was named IGN's 2005 Developer of the Year. BioShock immerses players into a war-torn underwater utopia, where mankind has abandoned their humanity in their quest for perfection. -

UPC Platform Publisher Title Price Available 730865001347

UPC Platform Publisher Title Price Available 730865001347 PlayStation 3 Atlus 3D Dot Game Heroes PS3 $16.00 52 722674110402 PlayStation 3 Namco Bandai Ace Combat: Assault Horizon PS3 $21.00 2 Other 853490002678 PlayStation 3 Air Conflicts: Secret Wars PS3 $14.00 37 Publishers 014633098587 PlayStation 3 Electronic Arts Alice: Madness Returns PS3 $16.50 60 Aliens Colonial Marines 010086690682 PlayStation 3 Sega $47.50 100+ (Portuguese) PS3 Aliens Colonial Marines (Spanish) 010086690675 PlayStation 3 Sega $47.50 100+ PS3 Aliens Colonial Marines Collector's 010086690637 PlayStation 3 Sega $76.00 9 Edition PS3 010086690170 PlayStation 3 Sega Aliens Colonial Marines PS3 $50.00 92 010086690194 PlayStation 3 Sega Alpha Protocol PS3 $14.00 14 047875843479 PlayStation 3 Activision Amazing Spider-Man PS3 $39.00 100+ 010086690545 PlayStation 3 Sega Anarchy Reigns PS3 $24.00 100+ 722674110525 PlayStation 3 Namco Bandai Armored Core V PS3 $23.00 100+ 014633157147 PlayStation 3 Electronic Arts Army of Two: The 40th Day PS3 $16.00 61 008888345343 PlayStation 3 Ubisoft Assassin's Creed II PS3 $15.00 100+ Assassin's Creed III Limited Edition 008888397717 PlayStation 3 Ubisoft $116.00 4 PS3 008888347231 PlayStation 3 Ubisoft Assassin's Creed III PS3 $47.50 100+ 008888343394 PlayStation 3 Ubisoft Assassin's Creed PS3 $14.00 100+ 008888346258 PlayStation 3 Ubisoft Assassin's Creed: Brotherhood PS3 $16.00 100+ 008888356844 PlayStation 3 Ubisoft Assassin's Creed: Revelations PS3 $22.50 100+ 013388340446 PlayStation 3 Capcom Asura's Wrath PS3 $16.00 55 008888345435 -

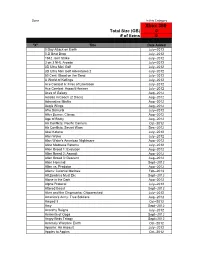

Xbox 360 Total Size (GB) 0 # of Items 0

Done In this Category Xbox 360 Total Size (GB) 0 # of items 0 "X" Title Date Added 0 Day Attack on Earth July--2012 0-D Beat Drop July--2012 1942 Joint Strike July--2012 3 on 3 NHL Arcade July--2012 3D Ultra Mini Golf July--2012 3D Ultra Mini Golf Adventures 2 July--2012 50 Cent: Blood on the Sand July--2012 A World of Keflings July--2012 Ace Combat 6: Fires of Liberation July--2012 Ace Combat: Assault Horizon July--2012 Aces of Galaxy Aug--2012 Adidas miCoach (2 Discs) Aug--2012 Adrenaline Misfits Aug--2012 Aegis Wings Aug--2012 Afro Samurai July--2012 After Burner: Climax Aug--2012 Age of Booty Aug--2012 Air Conflicts: Pacific Carriers Oct--2012 Air Conflicts: Secret Wars Dec--2012 Akai Katana July--2012 Alan Wake July--2012 Alan Wake's American Nightmare Aug--2012 Alice Madness Returns July--2012 Alien Breed 1: Evolution Aug--2012 Alien Breed 2: Assault Aug--2012 Alien Breed 3: Descent Aug--2012 Alien Hominid Sept--2012 Alien vs. Predator Aug--2012 Aliens: Colonial Marines Feb--2013 All Zombies Must Die Sept--2012 Alone in the Dark Aug--2012 Alpha Protocol July--2012 Altered Beast Sept--2012 Alvin and the Chipmunks: Chipwrecked July--2012 America's Army: True Soldiers Aug--2012 Amped 3 Oct--2012 Amy Sept--2012 Anarchy Reigns July--2012 Ancients of Ooga Sept--2012 Angry Birds Trilogy Sept--2012 Anomaly Warzone Earth Oct--2012 Apache: Air Assault July--2012 Apples to Apples Oct--2012 Aqua Oct--2012 Arcana Heart 3 July--2012 Arcania Gothica July--2012 Are You Smarter that a 5th Grader July--2012 Arkadian Warriors Oct--2012 Arkanoid Live -

Redline GT Compatible Games

Redline GT Compatible Games PlayStation®2 PlayStation®2 (con't) 18 Wheeler: American Pro Trucker ™ NASCAR® 07 Auto Modellista NASCAR® 08 Burnout 2: Point of Impact™ NASCAR® 09 Burnout 3 Takedown™ NASCAR® 2005: Chase for the Cup™ Burnout™ NASCAR® Heat™ 2: Road To The Championship Burnout™ Dominator NASCAR® Heat™ 2002 Burnout™ Revenge NASCAR® Thunder™ 2002 Colin McRae™ 2005 NASCAR® Thunder™ 2003 Colin McRae™ 3 NASCAR® Thunder™ 2004 Colin McRae™ Rally 4 Need For Speed™ Underground Corvette® Need For Speed™: Hot Pursuit 2 Driven Need for Speed™: Most Wanted Enthusia Professional Racing Need for Speed™: Underground 2 Evolution GT™ NHRA™ Championship Drag Racing™ F1™ 2001 Pro Race Driver F1™ 2002 R: Racing Evolution F1™ Career Challenge Rally Championship Ferrari® F355 Challenge™ Rally Fusion: Race of Champions Flatout™ Richard Burns Rally™ Ford Mustang: The Legend Lives RoadKill Formula One 2001™ Shox™ Formula One 2002™ Smuggler's Run 2: Hostile Territory Formula One 2003™ Starsky & Hutch™ Formula One 2004™ Street Racing Syndicate™ Gran Turismo™ 3 A-spec Test Drive® Gran Turismo™ 4 Test Drive® Eve of Destruction Gran Turismo™ Concept: 2001 Tokyo Test Drive® Off-Road: Wide Open™ Gran Turismo™ Concept: 2002 Tokyo-Geneva The Simpsons™ Hit & Run Grand Prix Challenge The Simpsons™ Road Rage Hot Wheels ™ Velocity X TOCA Race Driver™ 2 Initial D: Special Stage TOCA Race Driver™ 3 Juiced™ Total Immersion Racing™ Knight Rider™ Twisted Metal Black Online Lotus Challenge™ V-Rally™ 3 Midnight Club™ 3: DUB Edition World of Outlaws: Sprint Cars 2002 Midnight -

![[Japan] SALA GIOCHI ARCADE 1000 Miglia](https://docslib.b-cdn.net/cover/3367/japan-sala-giochi-arcade-1000-miglia-393367.webp)

[Japan] SALA GIOCHI ARCADE 1000 Miglia

SCHEDA NEW PLATINUM PI4 EDITION La seguente lista elenca la maggior parte dei titoli emulati dalla scheda NEW PLATINUM Pi4 (20.000). - I giochi per computer (Amiga, Commodore, Pc, etc) richiedono una tastiera per computer e talvolta un mouse USB da collegare alla console (in quanto tali sistemi funzionavano con mouse e tastiera). - I giochi che richiedono spinner (es. Arkanoid), volanti (giochi di corse), pistole (es. Duck Hunt) potrebbero non essere controllabili con joystick, ma richiedono periferiche ad hoc, al momento non configurabili. - I giochi che richiedono controller analogici (Playstation, Nintendo 64, etc etc) potrebbero non essere controllabili con plance a levetta singola, ma richiedono, appunto, un joypad con analogici (venduto separatamente). - Questo elenco è relativo alla scheda NEW PLATINUM EDITION basata su Raspberry Pi4. - Gli emulatori di sistemi 3D (Playstation, Nintendo64, Dreamcast) e PC (Amiga, Commodore) sono presenti SOLO nella NEW PLATINUM Pi4 e non sulle versioni Pi3 Plus e Gold. - Gli emulatori Atomiswave, Sega Naomi (Virtua Tennis, Virtua Striker, etc.) sono presenti SOLO nelle schede Pi4. - La versione PLUS Pi3B+ emula solo 550 titoli ARCADE, generati casualmente al momento dell'acquisto e non modificabile. Ultimo aggiornamento 2 Settembre 2020 NOME GIOCO EMULATORE 005 SALA GIOCHI ARCADE 1 On 1 Government [Japan] SALA GIOCHI ARCADE 1000 Miglia: Great 1000 Miles Rally SALA GIOCHI ARCADE 10-Yard Fight SALA GIOCHI ARCADE 18 Holes Pro Golf SALA GIOCHI ARCADE 1941: Counter Attack SALA GIOCHI ARCADE 1942 SALA GIOCHI ARCADE 1943 Kai: Midway Kaisen SALA GIOCHI ARCADE 1943: The Battle of Midway [Europe] SALA GIOCHI ARCADE 1944 : The Loop Master [USA] SALA GIOCHI ARCADE 1945k III SALA GIOCHI ARCADE 19XX : The War Against Destiny [USA] SALA GIOCHI ARCADE 2 On 2 Open Ice Challenge SALA GIOCHI ARCADE 4-D Warriors SALA GIOCHI ARCADE 64th. -

Ea Reports Record Fiscal Year Results

EA REPORTS SECOND QUARTER FISCAL 2007 RESULTS Q2 Net Revenue a Record $784 Million Driven by EA SPORTS Titles Need for Speed Carbon Debuts on 10 Platforms REDWOOD CITY, CA – November 2, 2006 – Electronic Arts (NASDAQ: ERTS) today announced preliminary financial results for its fiscal second quarter ended September 30, 2006. Fiscal Second Quarter Results Net revenue for the second quarter was $784 million, up 16 percent as compared with $675 million for the prior year. Sales were driven primarily by Madden NFL 07, NCAA® Football 07, FIFA 07, NBA Live 07 and catalog titles. Gross profit for the quarter was $445 million, up 14 percent year-over-year. Net income for the quarter was $22 million as compared with $51 million for the prior year. The Company adopted Statement of Financial Accounting Standards (SFAS) No. 123R “Share-Based Payment” at the beginning of its fiscal year resulting in pre-tax stock-based compensation charges of $33 million in the second quarter. Diluted earnings per share were $0.07 as compared with $0.16 for the prior year. Non-GAAP net income was $65 million as compared with $46 million a year ago – an increase of 41 percent year-over-year. Non-GAAP diluted earnings per share were $0.21 as compared with $0.15 for the prior year. (Please see Non-GAAP Financial Measures and reconciliation information included in this release.) Trailing twelve month operating cash flow was $571 million as compared with $592 million a year ago. The Company ended the quarter with cash, cash equivalents and marketable securities of $2.4 billion. -

Cyber Athletes: Identification, Competition, and Affect Implications

CYBER ATHLETES: IDENTIFICATION, COMPETITION, AND AFFECT IMPLICATIONS DISSERTATION Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of The Ohio State University By Robert Peter Griffiths, M.A. ***** The Ohio State University 2007 Dissertation Committee: Approved by Professor Matthew S. Eastin, Advisor Professor Osei Appiah ____________________________________ Professor Artemio Ramirez Advisor Graduate Program in Communication ABSTRACT Previous research has shown video games afford learning experiences, thus what occurs within the gaming realm is applicable to the real-world and vice-versa. Therefore, this study extends the video game effects literature by exposing the complexity of competitive gaming situations. In that spirit, this study incorporated a college football game to enact identification processes and direct competition to determine how player membership, opponent membership, and competition outcomes impact media effects variables such as enjoyment, presence, and state hostility. Two-hundred ninety four subjects participated in the 3 (opponent membership—main rival, conference opponent, other opponent) x 2 (player membership—identifier, non-identifier) x 2 (competitive outcome—win, loss) design. Overall, competition outcome significantly predicts levels of enjoyment and state hostility. Moreover, who the gamer plays as and against also influences these responses. Beating an emotionally relevant opponent solicited greater enjoyment than an irrelevant team. Further, losing while playing as an emotionally relevant team produced greater state hostility levels than losing as an emotionally irrelevant team. Similarly, losing to an emotionally relevant opponent generated higher state hostility levels than losing to an emotionally irrelevant team. ii DEDICATION Dedicated to my wife, Rachel, and my family and friends Καλεπα Τα Καλα iii ACKNOWLEDGMENTS This, the culmination of arduous graduate work, would not be possible without the help from so many family members, friends, and mentors. -

Titles Sep 29, 2021

All titles Sep 29, 2021 Name Description Rating Price Aggressive Inline Skating tricks with massive outdoor levels 77% Used £6.00 Freaky Flyers rare toony flyer 69% Used £10.00 Alias Its got gadgets! and girls! and thats about all 58% Used £10.00 Used £5.00 Full Spectrum Warrior Based on US army training. Best multi 80% America's Army: Rise of a Soldier 75% Used £7.50 No-Bk £4.00 Amped 2 80% No-Bk £4.00 Fuzion Frenzy 65% Used £6.00 Amped: Freestyle Snowboarding 79% Used £6.00 Galleon 71% Used £12.50 Armed and Dangerous 78% Used £8.50 Goblin Commander: Unleash the Horde Command & Conquor type game.. 73% Used £15.00 Bard's Tale The Excellent RPG. Coin & Cleavage is your goal. 73% Used £12.50 GoldenEye: Rogue Agent Intense 3D shooter - 100 weapon combos 62% Used £5.00 Batman Begins A 'dark' Batman game based on the movie 70% Used £10.00 Grabbed by the Ghoulies Jokey and spooky adventure 69% Used £12.50 Beyond Good & Evil Cartoony stealthy action game 88% Used £15.00 Gravity Games Bike: Street Vert Dirt 22% Used £6.00 Black Very nice FPS. 76% Used £12.50 Great Escape The Get out POW camp. Rush around adventure 57% Used £6.00 Blade II Falls short of the goretastic action of the movie 66% Used £12.50 Group S Challenge Street racer 53% Used £5.00 Blinx 2: Masters of Time & Space 72% Used £12.50 Gun Metal Control a 10m high robot fighter 69% Used £7.50 Blinx: The Time Sweeper 67% Used £10.00 Half-Life 2 87% Used £12.50 BloodRayne Dire vampire adventure yarn 74% Used £10.00 Used £7.50 Halo 2 The story continues in this classic 88% Brian Lara International Cricket 2005 Superb cricket game! 77% Used £7.50 No-Bk £5.00 Brothers in Arms: Road to Hill 30 Team Strategy based on D-Day 85% Used £5.00 Halo 2 Multiplayer Map Pack Requires Halo 2 - Play split-screen 85% Used £6.00 Brute Force Squad based shooter 77% Used £5.00 Halo: Combat Evolved THE pioneering Xbox game. -

Sport-Scan Daily Brief

SPORT-SCAN DAILY BRIEF NHL 8/14/2019 Anaheim Ducks 1107648 Ducks by position: Previewing Anaheim’s 2019-20 centers Arizona Coyotes 1107649 Arizona Coyotes' radio move to Fox Sports 910, iHeartMedia more than a dial change Boston Bruins 1107650 Bruins Summer Series: Jake DeBrusk looking to improve after a quiet postseason 1107651 2019 NHL farm system rankings: No. 29 Boston Bruins Calgary Flames 1107652 The Brett Kulak miscalculation: Flames’ value bet turns out to be bust Carolina Hurricanes 1107653 Carolina Hurricanes hire Rod Brind’Amour’s former teammate as its goaltending coach Chicago Blackhawks 1107654 Blackhawks add Swedish defenseman Philip Holm on a 1-year deal 1107655 Blackhawks sign Philip Holm, adding another name to defensive competition 1107656 Blackhawks sign one-year contract with Philip Holm Colorado Avalanche 1107657 Win? Or develop? The Avalanche’s AHL plan for the Colorado Eagles is to do both Detroit Red Wings 1107658 Red Wings' defense will take different shape as season progresses 1107659 Will Red Wings’ injury-plagued Trevor Daley draw trade interest? 1107660 Kid Rock paired with Nicklaus, Zetterberg added for Ally Challenge near Flint Montreal Canadiens 1107661 The Brett Kulak miscalculation: Flames’ value bet turns out to be bust New Jersey Devils 1107662 WATCH: Devils’ Connor Carrick gives inside look at offseason training 1107663 NJ Devils' Michael McLeod ready to make an impact in NHL Philadelphia Flyers 1107664 What Flyers prospect Jay O'Brien 'can't wait to prove' has him charging ahead Pittsburgh Penguins 1107665 First Call: Bill Guerin close to leaving Penguins?; Alex Rodriguez’s SUV robbed 1107666 Penguins Predictions: Can Dominik Simon ramp up his production? 1107667 These seven questions await when Penguins camp begins in a month 1107668 NHL Contraction Draft: Penguins load up on defense and get tougher in our 12-team league 1107669 2019 NHL farm system rankings: No. -

Animal Crossing

Alice in Wonderland Harry Potter & the Deathly Hallows Adventures of Tintin Part 2 Destroy All Humans: Big Willy Alien Syndrome Harry Potter & the Order of the Unleashed Alvin & the Chipmunks Phoenix Dirt 2 Amazing Spider-Man Harvest Moon: Tree of Tranquility Disney Epic Mickey AMF Bowling Pinbusters Hasbro Family Game Night Disney’s Planes And Then There Were None Hasbro Family Game Night 2 Dodgeball: Pirates vs. Ninjas Angry Birds Star Wars Hasbro Family Game Night 3 Dog Island Animal Crossing: City Folk Heatseeker Donkey Kong Country Returns Ant Bully High School Musical Donkey Kong: Jungle beat Avatar :The Last Airbender Incredible Hulk Dragon Ball Z Budokai Tenkaichi 2 Avatar :The Last Airbender: The Indiana Jones and the Staff of Kings Dragon Quest Swords burning earth Iron Man Dreamworks Super Star Kartz Backyard Baseball 2009 Jenga Driver : San Francisco Backyard Football Jeopardy Elebits Bakugan Battle Brawlers: Defenders of Just Dance Emergency Mayhem the Core Just Dance Summer Party Endless Ocean Barnyard Just Dance 2 Endless Ocean Blue World Battalion Wars 2 Just Dance 3 Epic Mickey 2:Power of Two Battleship Just Dance 4 Excitebots: Trick Racing Beatles Rockband Just Dance 2014 Family Feud 2010 Edition Ben 10 Omniverse Just Dance 2015 Family Game Night 4 Big Brain Academy Just Dance 2017 Fantastic Four: Rise of the Silver Surfer Bigs King of Fighters collection: Orochi FIFA Soccer 09 All-Play Bionicle Heroes Saga FIFA Soccer 12 Black Eyed Peas Experience Kirby’s Epic Yarn FIFA Soccer 13 Blazing Angels Kirby’s Return to Dream