Bluestar Israel Equity Review and Outlook

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Biolinerx Ltd. (Exact Name of Registrant As Specified in Its Charter) (Translation of Registrant’S Name Into English)

As filed with the U.S. Securities and Exchange Commission on March 12, 2020 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F (Mark One) ☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2019 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report For the transition period from __________ to __________ Commission file number _______________ BioLineRx Ltd. (Exact name of Registrant as specified in its charter) (Translation of Registrant’s name into English) Israel (Jurisdiction of incorporation or organization) 2 HaMa’ayan Street Modi’in 7177871, Israel (Address of principal executive offices) Philip A. Serlin +972 (8) 642-9100 +972 (8) 642-9101 (facsimile) [email protected] 2 HaMa’ayan Street Modi’in 7177871, Israel (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered American Depositary Shares, each representing 15 Nasdaq Capital Market ordinary shares, par value NIS 0.10 per share Ordinary shares, par value NIS 0.10 per share Nasdaq Capital Market* *Not for trading; only in connection with the registration of American Depositary Shares. -

Alphabetical Listing by Company Name

FOREIGN COMPANIES REGISTERED AND REPORTING WITH THE U.S. SECURITIES AND EXCHANGE COMMISSION December 31, 2015 Alphabetical Listing by Company Name COMPANY COUNTRY MARKET 21 Vianet Group Inc. Cayman Islands Global Market 37 Capital Inc. Canada OTC 500.com Ltd. Cayman Islands NYSE 51Job, Inc. Cayman Islands Global Market 58.com Inc. Cayman Islands NYSE ABB Ltd. Switzerland NYSE Abbey National Treasury Services plc United Kingdom NYSE - Debt Abengoa S.A. Spain Global Market Abengoa Yield Ltd. United Kingdom Global Market Acasti Pharma Inc. Canada Capital Market Acorn International, Inc. Cayman Islands NYSE Actions Semiconductor Co. Ltd. Cayman Islands Global Market Adaptimmune Ltd. United Kingdom Global Market Adecoagro S.A. Luxembourg NYSE Adira Energy Ltd. Canada OTC Advanced Accelerator Applications SA France Global Market Advanced Semiconductor Engineering, Inc. Taiwan NYSE Advantage Oil & Gas Ltd. Canada NYSE Advantest Corp. Japan NYSE Aegean Marine Petroleum Network Inc. Marshall Islands NYSE AEGON N.V. Netherlands NYSE AerCap Holdings N.V. Netherlands NYSE Aeterna Zentaris Inc. Canada Capital Market Affimed N.V. Netherlands Global Market Agave Silver Corp. Canada OTC Agnico Eagle Mines Ltd. Canada NYSE Agria Corp. Cayman Islands NYSE Agrium Inc. Canada NYSE AirMedia Group Inc. Cayman Islands Global Market Aixtron SE Germany Global Market Alamos Gold Inc. Canada NYSE Alcatel-Lucent France NYSE Alcobra Ltd. Israel Global Market Alexandra Capital Corp. Canada OTC Alexco Resource Corp. Canada NYSE MKT Algae Dynamics Corp. Canada OTC Algonquin Power & Utilities Corp. Canada OTC Alianza Minerals Ltd. Canada OTC Alibaba Group Holding Ltd. Cayman Islands NYSE Allot Communications Ltd. Israel Global Market Almaden Minerals Ltd. -

Bluestar Israel Global Technology Index Index Methodology Guide 1.8

Dec. 1 2020 BlueStar Israel Global Technology Index Index Methodology Guide 1.8 Issue Date: Dec 1. 2020 Produced by: BlueStar Global Investors, LLC d/b/a BlueStar Indexes 1350 Avenue of the Americas, Fourth Floor, New York, NY 1009 www.bluestarindexes.com 1 BlueStar Israel Global Technology Index Dec. 1 2020 The information contained in this document is current as of the publication date and is subject to change without notice. BlueStar Indexes will not accept responsibility for damages, direct or indirect, caused by any error or omission in this document. The BlueStar Indexes logo is a service mark of BlueStar Global Investors LLC. The BlueStar Israel Global Technology Index® is a trademark of BlueStar Global Investors LLC. ©220 BlueStar Global Investors LLC. All Rights Reserved. 2 BlueStar Israel Global Technology Index Dec. 1 2020 Contents Chapter 1: Introduction and Index Description........................................................................................... 4 Chapter 2: Index Construction ..................................................................................................................... 5 2.1 Base Date and Value .......................................................................................................................... 5 2.2 Component Eligibility Requirements ................................................................................................. 5 2.3 Initial Component Selection.............................................................................................................. -

Biolinerx Ltd. (Exact Name of Registrant As Specified in Its Charter) (Translation of Registrant’S Name Into English)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F (Mark One) o REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ⌧ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2012 OR o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR o SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report For the transition period from __________ to __________ Commission file number _______________ BioLineRx Ltd. (Exact name of Registrant as specified in its charter) (Translation of Registrant’s name into English) Israel (Jurisdiction of incorporation or organization) P.O. Box 45158 19 Hartum Street Jerusalem 91450, Israel (Address of principal executive offices) Philip Serlin +972 (2) 548-9100 +972 (2) 548-9101 (facsimile) [email protected] P.O. Box 45158 19 Hartum Street Jerusalem 9777518, Israel (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered American Depositary Shares, each representing 10 ordinary shares, par value NIS 0.01 per share Nasdaq Capital Market Ordinary shares, par value NIS 0.01 per share Nasdaq Capital Market* *Not for trading; only in connection with the registration of American Depositary Shares. Securities registered or to be registered pursuant to Section 12(g) of the Act. -

Signature Redacted

VC Funding Elements in US-Israel Case and Application to China-Korea By Anna Lee B.S. Business Administration, Finance and Corporate Management California State University, East Bay, 2012 SUBMITTED TO THE MIT SLOAN SCHOOL OF MANAGEMENT IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE IN MANAGEMENT STUDIES AT THE MASSACHUSETTS INSTITUTE OF TECHNOLOGY JUNE 2017 @2017 Anna Lee. All rights reserved. The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part in any medium now known or hereafter created. Signature redacted Signature of Author: V MIT Sloan S chool of Management May 12, 2017 Signature redacted Certified by: Jake Cohen Seniot Associate Dean for Undergraduate and Master's Programs Thesis Supervisor Signature redacted Accepted by: MASSA H IsENSTITUTE Rodrigo Verdi OFTEHNLGY Associate Professor of Accounting JUN 2 0 2017 Program Director, M.S. in Management Studies Program LIBRARIES ARCHIVES 77 Massachusetts Avenue Cambridge, MA 02139 MITLibraries http://Iibraries.mit.edu/ask DISCLAIMER NOTICE Due to the condition of the original material, there are unavoidable flaws in this reproduction. We have made every effort possible to provide you with the best copy available. Thank you. The images contained in this document are of the best quality available. Th c ppo n K> 2 VC Funding Elements in US-Israel Case and Application to China-Korea By Anna Lee Submitted to MIT Sloan School of Management on May 12, 2017 in Partial Fulfillment of the requirements for the Degree of Master of Science in Management Studies. -

Bluestar Israel Global Index Index Methodology Guide 1.6

December 4, 2019 BlueStar Israel Global Index Index Methodology Guide 1.6 Issue Date: December 4, 2019 Produced by: BlueStar Global Investors, LLC d/b/a BlueStar Indexes 1350 Avenue of the Americas, Fourth Floor, New York, NY 1009 www.bluestarindexes.com 1 BlueStar Israel Global Index December 4, 2019 The information contained in this document is current as of the publication date and is subject to change without notice. BlueStar Indexes will not accept responsibility for damages, direct or indirect, caused by any error or omission in this document. The BlueStar Indexes logo is a service mark of BlueStar Global Investors LLC. The BlueStar Israel Global Index® is a trademark of BlueStar Global Investors LLC. ©2018 BlueStar Global Investors LLC. All Rights Reserved. 2 BlueStar Israel Global Index December 4, 2019 Contents Chapter 1: Introduction and Index Description........................................................................................... 4 Chapter 2: Index Construction ..................................................................................................................... 5 2.1 Base Date and Value .......................................................................................................................... 5 2.2 Component Eligibility Requirements ................................................................................................. 5 2.3 Initial Component Selection............................................................................................................... 6 2.4 Dividend -

List of Section 13F Securities, Second Quarter, 2021

List of Section 13F Securities Second Quarter FY 2021 Copyright (c) 2021 American Bankers Association. CUSIP Numbers and descriptions are used with permission by Standard & Poors CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. All rights reserved. No redistribution without permission from Standard & Poors CUSIP Service Bureau. Standard & Poors CUSIP Service Bureau does not guarantee the accuracy or completeness of the CUSIP Numbers and standard descriptions included herein and neither the American Bankers Association nor Standard & Poor's CUSIP Service Bureau shall be responsible for any errors, omissions or damages arising out of the use of such information. U.S. Securities and Exchange Commission OFFICIAL LIST OF SECTION 13(f) SECURITIES USER INFORMATION SHEET General This list of “Section 13(f) securities” as defined by Rule 13f-1(c) [17 CFR 240.13f-1(c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [15 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 [17 CFR 240.13f-1] under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of June 15, 2021, and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending June 30, 2021. Institutional investment managers should report holdings-- number of shares and fair market value--as of the last day of the calendar quarter as required by [ Section 13(f)(1) and Rule 13f-1] thereunder. -

1-800 Flowers.Com, Inc

FLWS 1-800 Flowers.Com, Inc. - Class A Common Stock FCOB 1St Colonial Bancorp Inc FNRC 1St Nrg Corp TDCH 30Dc Inc TSIOF 361 Degrees Intl Ltd TDEY 3D Eye Solutions Inc DPSM 3D Pioneer Systems Inc DDD 3D Systems Corporation Common Stock TDCP 3Dicon Corp DDDX 3Dx Industries Inc MMM 3M Company Common Stock PSPW 3Power Energy Group Inc CATV 4Cable Tv Intl Inc FOUR 4Licensing Corp BARZ 5Barz International Inc RNWR 808 Renewable Energy Corp EIHDF 888 Holdings Plc Ord EGHT 8X8 Inc - Common Stock DRWN A Clean Slate Inc SHLM A. Schulman, Inc. - Common Stock AOS A.O. Smith Corporation Common Stock AMKBY A.P Moller-Mrs Uns/Adr AEMMY A2A Spa Unsp/Adr AACAY Aac Techs Hldgs Unsp/Adr ELUXY Ab Electrolux B S/Adr RJA Ab Svensk Ekportkredit (Swedish Export Credit Corporation) Elements Linked To The Rogers International Commodity Index - Agriculture Total Return Structured Product ABCFF Abacus Mining & Expl Corp ABKI Abakan Inc ATTBF Abattis Bioceuticals Ord ABB Abb Ltd Common Stock ABLZF Abb Ltd Zuerich ABT Abbott Laboratories Common Stock ABBV Abbvie Inc. Common Stock ABBY Abby Inc ABCZY Abcam Plc Adr AGOAF Abengoa Sa Abg/Ac B ABGOF Abengoa Sa Ord ABGB Abengoa, S.A. - American Depositary Shares ANF Abercrombie & Fitch Company Common Stock ABBAF Aberdeen Asian Income Fun ABDNY Aberdeen Asset Mgmt Adr IAF Aberdeen Australia Equity Fund Inc Common Stock GCH Aberdeen Greater China Fund, Inc. Common Stock IF Aberdeen Indonesia Fund, Inc. (Common Stock ABMD Abiomed, Inc. - Common Stock ABOT Abot Mining Co Ida Cap ABHD Abtech Holdings Inc ACCA Acacia Diversified Hldgs ACTG Acacia Research Corporation - Common Stock AKR Acadia Realty Trust Common Stock AXDX Accelerate Diagnostics, Inc. -

Save the Date

Save The Date 29TH ANNUAL MARCH 12-15 THE RITZ CARLTON ORANGE COUNTY, CA 29th Annual ROTH Conference scheduled for March 12-15, 2017 at The Ritz Carlton, Laguna Niguel in Orange County, CA. Following the success of previous year's events, the ROTH Conference, with close to 500 participating companies and over 4,000 attendees, will feature presentations from public and private companies in a variety of sectors including: Healthcare Consumer Technology, Internet & Media Oil & Gas / Mining & Minerals Cleantech, Industrial Growth & Solar Business Services Throughout the three and a half day event, we will host: Ÿ 10 concurrent tracks of company presentations Ÿ Thousands of 1-on-1 / small group meetings Ÿ Several thematic panel discussions Ÿ A private company track Ÿ Three nights of signature evening entertainment Ÿ ROTH's Signature Social Sunday featuring the ROTH Ride, Spin, Golf & Tennis events This gathering of institutional investors, private equity investors, VCs, company executives and service providers has become a must-attend event for anyone working in the small and mid-cap space. This event is for institutional clients of ROTH, and by invitation only. Attendees must be registered for the conference to book a hotel room. RSVP: Contact a ROTH Sales Representative at 800.678.9147 or email [email protected] 888 San Clemente Drive | Newport Beach CA 92660 800 678-9147 | www.roth.com | Member SIPC / FINRA CLICK HERE to view a live list of Participating Companies Presenting Companies 29TH ANNUAL MARCH 12-15 THE RITZ CARLTON ORANGE COUNTY, CA 22nd Century Group Inc (XXII) BioSig Technologies Inc Darling Ingredients Inc. -

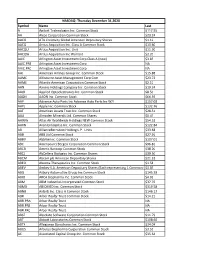

NASDAQ Index

NASDAQ- Thursday December 31,2020 Symbol Name Last A Agilent Technologies Inc. Common Stock $117.55 AA Alcoa Corporation Common Stock $23.24 AACG ATA Creativity Global American Depositary Shares $1.19 AACQ Artius Acquisition Inc. Class A Common Stock $10.60 AACQU Artius Acquisition Inc. Unit $11.30 AACQW Artius Acquisition Inc Warrant $2.20 AAIC Arlington Asset Investment Corp Class A (new) $3.85 AAIC.PRB Arlington Asset Investment Corp NA AAIC.PRC Arlington Asset Investment Corp NA AAL American Airlines Group Inc. Common Stock $15.88 AAMC Altisource Asset Management Corp Com $23.72 AAME Atlantic American Corporation Common Stock $2.10 AAN Aarons Holdings Company Inc. Common Stock $19.34 AAOI Applied Optoelectronics Inc. Common Stock $8.50 AAON AAON Inc. Common Stock $66.59 AAP Advance Auto Parts Inc Advance Auto Parts Inc W/I $157.02 AAPL Apple Inc. Common Stock $132.76 AAT American Assets Trust Inc. Common Stock $28.51 AAU Almaden Minerals Ltd. Common Shares $0.47 AAWW Atlas Air Worldwide Holdings NEW Common Stock $54.52 AAXN Axon Enterprise Inc. Common Stock $122.84 AB AllianceBernstein Holding L.P. Units $33.68 ABB ABB Ltd Common Stock $27.91 ABBV AbbVie Inc. Common Stock $107.01 ABC AmerisourceBergen Corporation Common Stock $96.81 ABCB Ameris Bancorp Common Stock $38.20 ABCL AbCellera Biologics Inc. Common Shares $39.50 ABCM Abcam plc American Depositary Shares $21.32 ABEO Abeona Therapeutics Inc. Common Stock $1.58 ABEV Ambev S.A. American Depositary Shares (Each representing 1 Common Share)$3.03 ABG Asbury Automotive Group Inc Common Stock $145.39 ABIO ARCA biopharma Inc. -

ARK ISRAEL INNOVATIVE TECHNOLOGY ETF (IZRL) HOLDINGS As of 07/30/2021

ARK ISRAEL INNOVATIVE TECHNOLOGY ETF (IZRL) HOLDINGS As of 07/30/2021 Company Ticker CUSIP Shares Market Value($) Weight(%) 1 FIVERR INTERNATIONAL LTD FVRR M4R82T106 17,875 4,589,227.50 1.62 2 KORNIT DIGITAL LTD KRNT M6372Q113 32,491 4,326,501.56 1.52 3 GILAT SATELLITE NETWORKS LTD GILT M51474118 407,160 4,250,750.40 1.50 4 INMODE LTD INMD M5425M103 36,594 4,246,001.82 1.50 5 NICE LTD - SPON ADR NICE 653656108 14,736 4,152,457.44 1.46 6 SILICOM LTD SILC M84116108 91,836 4,132,620.00 1.46 7 TEVA PHARMACEUTICAL-SP ADR TEVA 881624209 428,057 4,147,872.33 1.46 8 PURPLE BIOTECH LTD-ADR PPBT 74638P109 737,182 4,120,847.38 1.45 9 RADA ELECTRONIC INDS LTD RADA M81863124 313,235 4,125,304.95 1.45 10 MATRIX IT LTD MTRX 6747754 148,310 4,082,477.34 1.44 11 CERAGON NETWORKS LTD CRNT M22013102 1,090,119 4,087,946.25 1.44 12 CAMTEK LTD CAMT M20791105 109,748 4,102,380.24 1.44 13 SOLAREDGE TECHNOLOGIES INC SEDG 83417M104 15,549 4,060,310.37 1.43 14 PERION NETWORK LTD PERI M78673114 208,534 4,020,535.52 1.42 15 UROGEN PHARMA LTD URGN UQ M96088105 258,704 4,007,324.96 1.41 16 MALAM - TEAM LTD MLTM 6875923 120,173 3,991,533.29 1.41 17 COGNYTE SOFTWARE LTD CGNT M25133105 152,667 3,999,875.40 1.41 18 BET SHEMESH ENGINES HOLDINGS BSEN 6103936 197,115 3,998,331.45 1.41 19 E & M COMPUTING EMCO 6302216 640,592 3,992,195.47 1.41 20 CYBERARK SOFTWARE LTD/ISRAEL CYBR M2682V108 27,759 3,983,416.50 1.40 21 BATM ADVANCED COMMUNICATIONS BATM B85PTW0 3,246,850 3,971,660.48 1.40 22 WIX.COM LTD WIX M98068105 13,109 3,974,648.80 1.40 23 PLASSON INDUSTRIES LTD PLSN 6094728 -

IKARIA® to In-License Biolinerx's BL-1040

FOR IMMEDIATE RELEASE CONTACT: Samina Bari Dganit Bar Ikaria BioLineRx 908.238.6372 972-2-5489100 [email protected] [email protected] IKARIA® to In-License BioLineRx’s BL-1040 Clinton, NJ and Jerusalem, Israel, July 6, 2009 – Ikaria Holdings, Inc. and BioLineRx Ltd. (TASE: BLRX) today announced that Ikaria has entered into an agreement to obtain a worldwide exclusive license to BioLineRx’s BL-1040, a potential breakthrough treatment for preventing pathological cardiac remodeling following acute myocardial infarction (AMI). BL-1040, currently in a phase I/II clinical trial, is administered via the coronary artery during standard catheterization and flows into the damaged heart muscle, where it forms a protective “scaffold” that enhances the mechanical strength of the heart muscle during recovery and repair. BL-1040 is the first program to graduate from the BIJ (BioLine Innovations Jerusalem) incubator subsidized by the Israeli Office of the Chief Scientist. Under the terms of the agreement, BioLineRx will receive upfront and milestone payments. BioLineRx will also receive royalties on annual net sales. Ikaria will be responsible for completing clinical development and commercialization efforts. The deal is contingent upon receipt of the approval of the Israeli Office of the Chief Scientist. “The acquisition of the rights to BL-1040 reinforces our commitment to deliver novel treatments to critically ill patients around the world,” commented Daniel Tassé, President and CEO of Ikaria. “Millions of patients suffer from MI each year, and BL-1040 represents the potential of an exciting solution to the problem of ventricular remodeling following AMI, for which the unmet need remains very high.” “This agreement is consistent with our business model of developing early-stage programs through human Proof of Concept trials and ultimately partnering with a global therapeutics company that has the expertise and resources to complete development and commercialization " said Morris C.