Oddo Bhf German Conference

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Presentation of Oddo Bhf Group

PRESENTATION OF ODDO01 BHF GROUP FINANCING CONFERENCE UKRAINE Berlin, June 2019 1 The leading independent Franco-German financial group Entrepreneurial Independent Unique Stable Driven A family-owned Freedom of spirit and A unique Franco- Determination to work Employees motivated by company in which action acknowledged German group on a long-term basis an ideal of excellence employees have a by our clients model, a quality of with employees, and by a constantly stake in the share relationship that the partners and clients, renewed commitment capital and thus similar client cannot find ensuring trust and interests to clients anywhere else integrity OUR 3 KEY POINTS CLIENTS’ ASSETS €100 PEOPLE billion NET BANKING INCOME BBB The interests of our employees, who are partners in €591 Fitch the share capital, are aligned with those of our million Ratings clients. LONG-TERM EQUITY The Group builds relationships of trust with its 2,300 clients, partners and employees. EMPLOYEES €844 million 1,000 RESEARCH SOLVENCY IN FRANCE & TUNISIA RATIO 1,300 The Group invests 20% of its revenue IN GERMANY +15% in financial analysis and information systems. 4 More than 150 years of history – your partner for the next 150 years Our mission is to help people and business to grow ODDO BHF is a unique Franco German financial group with a long history rooted in these two key European markets for more than 150 years. It builds its success on its proximity to corporates and entrepreneurs. It is in particular close to family-owned mid-sized companies which are the backbone of European economy. -

DEF Mar 2018.Xlsx

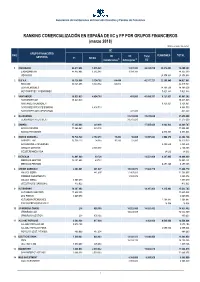

Asociación de Instituciones de Inversión Colectiva y Fondos de Pensiones _____________________________________________________________________________________________________________________ RANKING COMERCIALIZACIÓN EN ESPAÑA DE IIC y FP POR GRUPOS FINANCIEROS (marzo 2018) (Datos en miles de euros) IIC GRUPO FINANCIERO RKG IIC IIC Total PENSIONES TOTAL GESTORA FI SICAV Inmobiliarias(1) Extranjeras(2) IIC 1 CAIXABANK 44.877.886 1.516.041 1.931.383 48.325.310 25.974.993 74.300.303 CAIXABANK AM 44.877.886 1.516.041 1.931.383 48.325.310 VIDACAIXA 25.974.993 25.974.993 2 B.B.V.A. 39.128.555 3.124.752 64.414 42.317.721 22.209.840 64.527.561 BBVA AM 39.128.555 3.124.752 64.414 42.317.721 BBVA PENSIONES 14.788.508 14.788.508 GESTION PREV. Y PENSIONES 7.421.333 7.421.333 3 SANTANDER 38.623.523 4.804.719 431.089 43.859.331 9.721.921 53.581.252 SANTANDER AM 38.623.523 38.623.523 SANTANDER PENSIONES 9.721.921 9.721.921 SANTANDER PRIVATE BANKING 4.804.719 4.804.719 SANTANDER AM LUXEMBURGO 431.089 431.089 4BLACKROCK 31.215.600 31.215.600 31.215.600 BLACKROCK INVESTMENT 31.215.600 31.215.600 5 BANKIA 17.265.864 239.990 17.505.854 6.983.933 24.489.787 BANKIA FONDOS 17.265.864 239.990 17.505.854 BANKIA PENSIONES 6.983.933 6.983.933 6 BANCO SABADELL 16.738.129 2.152.473 15.206 52.085 18.957.893 3.508.274 22.466.168 SABADELL AM 16.738.129 14.080 15.206 52.085 16.819.500 BANSABADELL PENSIONES 3.453.638 3.453.638 URQUIJO GESTIÓN 2.138.393 2.138.393 MEDITERRANEO VIDA 54.636 54.636 7 IBERCAJA 12.481.680 69.724 12.551.404 6.297.465 18.848.869 IBERCAJA GESTION 12.481.680 69.724 12.551.404 IBERCAJA PENSION 6.297.465 6.297.465 8 CREDIT AGRICOLE 2.403.001 441.697 15.020.072 17.864.770 17.864.770 AMUNDI IBERIA 441.697 11.467.000 11.908.697 PIONEER INVESTMENTS 3.553.072 3.553.072 AMUNDI IBERIA 1.987.079 1.987.079 CREDIT AGRIC.BANKOA G. -

Name Adresse PLZ Ort Land 1741 Fund Management AG 10, Bangar

Folgende Investmentfondsgesellschaften können wir Ihnen anbieten: Name Adresse PLZ Ort Land 1741 Fund Management AG 10, Bangarten 9490 Vanduz Liechtenstein 3 Banken-Generali Investment-Gesellschaft mbH Untere Donaulände 28 4020 Linz Österreich Aachener Grundvermögen Kapitalverwaltungsgesellschaft Wörthstraße 32 50668 Köln Deutschland mbH Abalone Asset Management Ltd 179, Marina Street 9042 Pieta Malta Aberdeen Asset Management Deutschland AG Bockenheimer Landstraße 25 60325 Frankfurt am Main Deutschland Aberdeen Fund Managers Limited 1 Bread Street London EC4M 9BE Großbritannien Aberdeen Global 49, Avenue J.F. Kennedy 1855 Luxemburg Luxemburg Aberdeen Standard Investments Luxembourg S.A. 35a, avenue John F. Kennedy 1855 Luxemburg Luxemburg ABN AMRO Investment Solutions 3, avenue Hoche 75008 Paris Frankreich Guild House, Guild Street, International Absolute Insight Funds p.l.c. Dublin 1 Irland Financial Services Centre ACATIS Investment Kapitalverwaltungsgesellschaft mbH Taunusanlage 18 60325 Frankfurt am Main Deutschland Accuro Fund Solutions AG Hintergass 19 9490 Vaduz Liechtenstein ACOLIN Fund Management S.A. 4, rue Dicks 1417 Luxemburg Luxemburg Aegon Asset Management Europe ICAV 25/28 North Wall Quay Dublin 1 Irland AFFM S.A. 3, Boulevard Royal 2449 Luxemburg Luxemburg Ahead Wealth Solutions AG Austrasse 37 9490 Vaduz Liechtenstein Alceda Fund Management S.A. 5, Heienhaff 1736 Senningerberg Luxemburg Algebris UCITS Funds plc Earlsfort Terrace, Arthur Cox Building Dublin 2 Irland ALGER SICAV 2-8, avenue Charles de Gaulle 1653 Luxemburg Luxemburg AllianceBernstein (Luxembourg) S.à r.l. 2-4, rue Eugene Ruppert 2453 Luxemburg Luxemburg Allianz Global Investors GmbH Bockenheimer Landstraße 42-44 60323 Frankfurt am Main Deutschland Allianz Global Investors Ireland Ltd. 15/16 Fitzwilliam Place Dublin 2 Irland 2633 Luxemburg- Allianz Global Investors Luxembourg S.A. -

01Presentation Of

PRESENTATION01 OF ODDO BHF GROUP 2019 2 A UNIQUE FRANCO-GERMAN FINANCIAL GROUP 3 Meet Philippe Oddo, our General Partner Make finance work for you Our Franco-German expertise means that we can provide our clients with in-depth knowledge of the companies, economy and investors of the region. PHILIPPE ODDO General Partner 4 The leading independent Franco-German financial group Entrepreneurial Independent Unique Stable Driven A family-owned Freedom of spirit and A unique Franco- Determination to work Employees motivated by company in which action acknowledged German group on a long-term basis an ideal of excellence employees have a by our clients model, a quality of with employees, and by a constantly stake in the share relationship that the partners and clients, renewed commitment capital and thus similar client cannot find ensuring trust and interests to clients anywhere else integrity OUR 3 KEY POINTS CLIENTS’ ASSETS €100 PEOPLE billion NET BANKING INCOME BBB The interests of our employees, who are partners in €591 Fitch the share capital, are aligned with those of our million Ratings clients. LONG-TERM EQUITY The Group builds relationships of trust with its 2,300 €844 clients, partners and employees. EMPLOYEES million 1,000 RESEARCH IN FRANCE & TUNISIA SOLVENCY RATIO 1,300 The Group invests 20% of its revenue IN GERMANY +15% in financial analysis and information systems. 5 More than 150 years of history – your partner for the next 150 years Our mission is to help people and business to grow ODDO BHF is a unique Franco German financial group with a long history rooted in these two key European markets for more than 150 years. -

ODDO BHF Private Equity Announces the 1St Closing of ODDO BHF Secondaries Fund with Total Capital Commitments on the Strategy in Excess of € 160 Million

PRESS RELEASE ODDO BHF Private Equity announces the 1st closing of ODDO BHF Secondaries Fund with total capital commitments on the strategy in excess of € 160 million November 13th 2018, Düsseldorf, Frankfurt am Main, Paris. ODDO BHF Private Equity is pleased to announce that it has successfully completed the first closing of ODDO BHF Secondaries Fund, whose fundraising started in July 2018, with total commitments above €160 million, including a dedicated mandate for an institutional investor. Commitments come mostly from French and German institutional clients. As an anchor investor, the ODDO BHF Group has made a significant investment in the Fund. Nicolas Chaput, President of ODDO BHF Private Equity stated, “We are proud to receive such a strong support both from our historical partners as well as new investors that consider the secondary Private Equity market as a strong investment opportunity given the current market conditions. This first closing, happening less than 4 months after the launch of the strategy is also a great recognition of the quality and long standing track record of the PE team, led by Gilles Michat, Jérôme Marie and Ferdinand Dalhuisen.” ODDO BHF Secondaries Fund invests in the lower end of the secondary European and North American markets, specifically focusing on medium seized transactions ranging from € 5 million to € 50 million. The Fund specializes in investing in mature and primarily cash generative assets with dominant positions and strong commitment of management teams. For Gilles Michat, Managing Director of ODDO BHF Private Equity: “The differentiating nichy approach of the Fund is based both on our ability to negotiate attractive conditions at entry and acquire assets presenting a strong value creation potential. -

AUFLISTUNG ZU DEN VON UNS ANGEBOTENEN EMITTENTEN/VERSICHERUNGS- GESELLSCHAFTEN UND ANBIETERN Investmentfonds

STAND 01.01.2018_Anlage AUFLISTUNG ZU DEN VON UNS ANGEBOTENEN EMITTENTEN/VERSICHERUNGS- GESELLSCHAFTEN UND ANBIETERN Investmentfonds Aachener Grundvermögen Aberdeen Global Aberdeen Global Services S.A. Kapitalverwaltungsgesellschaft mbH Abrias Absolute Insight Funds p.l.c. ACOLIN Fund Management S.A. AFFM S.A. Ahead Wealth Solutions AG Alceda Fund Management S.A. ALGER SICAV AllianceBernstein (Luxembourg) S.A. Allianz Global Investors Europe GmbH Allianz Global Investors GmbH Allianz Global Investors Ireland Ltd. Allianz Global Investors Luxembourg S.A. Allianz Invest Kapitalanlagegesellschaft mbH Alma Capital Investment Management ALTE LEIPZIGER Trust Investment-Gesellschaft mbH Ampega Investment GmbH Amundi Amundi Deutschland GmbH Amundi Investment Solutions Amundi Luxembourg S.A. ANIMA Funds plc Aspect UCITS Funds plc Assenagon Asset Management S.A. Atlantis Investment Management (Ireland) Limited AVANA Investmentaktiengesellschaft mit Aviva Funds Services S.A. Aviva Investors Luxembourg Teilgesellschaftsvermögen AXA Funds Management S.A. AXA Investment Managers Deutschland GmbH AXA Investment Managers Paris AXA Investment Managers UK Limited AXA Rosenberg Equity Alpha Trust AXXION S.A. Balfidor Fondsleitung AG Baloise Fund Invest (Lux) Bank Austria Real Invest Immobilien-Kapitalanlage GmbH Bankhaus Schelhammer & Schattera Banque et Caisse dEpargne de lEtat, Luxembourg Bantleon Invest S.A. Kapitalanlageges. mbH Barclays Investment Funds (Luxembourg) SICAV Baring Fund Managers Limited Baring International Fund Managers (Ireland) Limited BAWAG P.S.K. INVEST GmbH BayernInvest Kapitalanlagegesellschaft mbH BayernInvest Kapitalverwaltungsgesellschaft mbH BayernInvest Luxembourg S.A. Berenberg Lux Invest S.A. bfw fondsleitung ag BI SICAV (BankInvest) BlackRock Asset Management Deutschland AG BlackRock Asset Management Ireland Limited BlackRock Fund Management Company (Ireland) BlackRock Investment Management (Dublin) BlackRock (Luxembourg) S.A. Limited Limited BlackRock (Singapore) Limited BLI - Banque de Luxembourg Investments S.A. -

Communication on Progress UN Global Compact

Communication on Progress UN Global Compact 2018 - 2019 Background ODDO BHF is an independent and European financial operator at the heart of the real economy for 170 years. ODDO BHF, established in 1849, is a family owned company with a true entrepreneurial mindset in which the interests of shareholder employees are aligned with those of clients (25% of the capital is owned by employees). The independency of the Group allows for a real freedom of spirit and action recognised by our clients. The stability of the Group is reflected in the relationship built on long-term trust and integrity with our clients, partners and employees. Since 1849 ODDO BHF works actively to contribute to economic, social and environmental progress with a focus on helping our clients achieve their ambition in a sustainable society. The company integrates the environment, social aspects and cor- porate governance matters in all its activities. The Group intends to make its commitments in terms of sustainable development and corporate social responsibility (CSR) a long-term commitment, and wishes to involve further its employees in this process. In France and Germany, the Group employees have launched in 2019 a "Sustainable Development Committee" whose purpose is to support all initiatives that help reduce the company's ecological footprint and change individual and collective behaviour. 31 internal ambassadors, representing different Group businesses, have volunteered to support our initiatives and help us move forward on this issue. Statement of continued support by the Managing Partner Our entrepreneurial DNA and the ambitious long-term targets we have set ourselves aim to offer the highest quality service. -

Press Release Ranking List Bund Issues Auction Group

ADDRESS Olof-Palme-Straße 35 Press Release 60439 Frankfurt/Main TEL +49 69 25616-1607 Number 13 on 10 December 2020 FAX +49 69 25616-1476 Page 1 of 3 [email protected] www.deutsche-finanzagentur.de Ranking list of the Bund Issues Auction Group In 2020, Federal securities (Federal bonds, Federal notes, Federal Treasury notes, Treasury discount paper, inflation-linked Federal securities and for the first time Green Bonds) were issued in 106 auctions via the Bund Issues Auction Group. The attached list shows the ranking of the 36 group members of the Bund Issues Auction Group in 2020. The ranking is based on the allotted amounts in 2020, weighted by the respective duration and interest rate risk of the auctioned securities. The relevant weights were announced in December 2014 and will be adjusted in 2021 (page 3). The ranking is published twice a year, at the end of June and December. REPRODUCTION PERMITTED ONLY IF SOURCE IS STATED. MEMBERS OF THE EXECUTIVE BOARD Dr. Tammo Diemer and Dr. Jutta A. Dönges REGISTERED OFFICE Frankfurt/M. SOLE SHAREHOLDER Federal Republic of Germany, represented by the Federal Ministry of Finance REGISTER COURT Local Court Frankfurt/M. HRB 51411 DEUTSCHE BUNDESBANK IBAN DE03 5040 0000 0050 4089 90 BIC MARKDEFF The General Terms and Conditions of the company apply. Number 13 on 10 December 2020 Page 2 of 3 Bund Issues Auction Group Ranking 2020 * Rank Bund Issues Auction Group Member 1 HSBC France S.A. 2 Commerzbank AG 3 BNP Paribas S.A. 4 Bank of America (BofA) Securities Europe S.A. -

Job Post: Head of ESG Research – ODDO BHF Corporates & Markets

Job Post: Head of ESG research – ODDO BHF Corporates & Markets – Paris Role type: Permanent Branch: Brokerage Activities on the Equity and Bond Markets Education level: Master’s degree/MA/MS/MSC Job: Merchant bank Level of experience: Senior Country: France City: Paris Start date: As soon as possible About ODDO BHF ODDO BHF is an independent Franco-German financial services group, with a history stretching back over 150 years. It was created from the alliance of a French family-owned business built up by five generations of stockbrokers and a German bank specialising in Mittelstand companies. With 2,300 employees (1,300 in Germany and 1,000 in France), and more than 100 billion euros in assets under management, ODDO BHF operates in three main businesses, based on significant investment in market expertise: private banking, asset management and corporate and investment banking. The Group has a specific ownership structure as 60% of its capital is held by the Oddo family and 30 % by employees. This “partnership” ethos guarantees the long-term involvement of its teams. At 31 December 2016, ODDO BHF generated net banking income of 577 million euros, net profit after tax of 136 million euros and at 31 December 2016, the Group had over 814 million euros of shareholders' equity. www.oddo-bhf.com Mission Undertake analysis of extra financial factors in sectors and companies under coverage within the Research Department to support ESG integration in the overall research product. Drive product and research innovation to strengthen ODDO BHF Corporates & Markets’ expertise in sell-side Equity ESG research. -

Improving Consistency on a Global Scale

A Bloomberg Professional Services Offering Investment Management Journey case study Improving consistency Asset Manager on a global scale. ODDO BHF Asset Management & Bloomberg Buy-Side Solutions Case study Improving consistency on a global scale Location ODDO BHF Asset Management Headquarters in Paris, France and Düsseldorf, Germany ODDO BHF Asset Management (OBAM), the first Industry independent Franco-German financial group, is following Investment banking, asset management two paths: expansion and front-to-middle consolidation. and private wealth After several key acquisitions, the firm increased its total Customer profile AUM from approximately €17 billion to €61 billion in four • Asset management years. Rapid growth has spurred the firm to bring trusted • Serves wholesale clients, companies Bloomberg buy-side solutions from one office to many others. and institutional investors • €61 billion AUM • 10 offices worldwide in Europe, How buy-side firms achieve total transformation the Middle East and Asia To sustain a competitive advantage and help ensure long-term success, buy-side leaders need to develop a well-defined Target Operating Model (TOM). The TOM Target operating model ambitions clarifies the firm’s key operational goals and the changes that are necessary to achieve them. • Consolidate front and middle office activities across offices Bloomberg has helped asset management firms around the world meet a wide • Reduce total cost of ownership variety of operational objectives. Based on our experience, we have identified with a single operating model four paths that firms can take on their road to transformation: • Manage regulatory concerns 1. Specialization for multiple jurisdictions The asset manager specializes in a particular strategy, seeking to be nimble • Support cross-border as a primary TOM focus but needing to upgrade technology systems to support investment strategies rapid growth. -

ODDO BHF Green Bond PROSPECTUS and TERMS of INVESTMENT 10/2019

ODDO BHF Green Bond PROSPECTUS AND TERMS OF INVESTMENT 10/2019 Investment management company: ODDO BHF Asset Management GmbH Investment manager: ODDO BHF Asset Management GmbH In the event of disputes, consumers may call upon the Investment Fund units are bought and sold on the basis of the Prospectus, the Key Funds Ombudsman operated by the German Investment Funds Association Investor Information and the General Terms of Investment in conjunction (BVI Bundesverband Investment und Asset Management e.V.) as the com- with the Specific Terms of Investment, each as amended from time to time. petent consumer arbitration body. ODDO BHF Asset Management GmbH The General Terms of Investment and Specific Terms of Investment are participates in arbitration proceedings before this body. included in this document after the Prospectus. The Prospectus is to be provided on request and free of charge to Contact details for the Investment Funds Ombudsman are as follows: potential purchasers of Fund units and to all investors in the Fund. It will be supplied together with the most recent published annual report and any Büro der Ombudsstelle des BVI subsequent half-yearly report. Potential purchasers of Fund units are also Bundesverband Investment und Asset Management e. V. to be provided with the Key Investor Information free of charge in good Unter den Linden 42 time prior to entering into any agreement. 10117 Berlin No information may be provided and no declarations made that Phone: + 49 (0) 30 6 44 90 46 - 0 deviate from the Prospectus. Any unit purchase based on information or Fax: + 49 (0) 30 6 44 90 46 - 29 declarations that are not contained in the Prospectus or the Key Investor Email: [email protected] Information is exclusively at the buyer’s own risk. -

Libro De Entidades (1 MB )

REGISTROS DE ENTIDADES 2021 SITUACION A 23 DE SEPTIEMBRE DE 2021 BANCO DE ESPAÑA INDICE Página CREDITO OFICIAL ORDENADO ALFABETICAMENTE ...................................................................................................... 7 ORDENADO POR CODIGO B.E. ......................................................................................................... 9 BANCOS ORDENADO ALFABETICAMENTE .................................................................................................... 13 ORDENADO POR CODIGO B.E. ....................................................................................................... 15 CAJAS DE AHORROS ORDENADO ALFABETICAMENTE .................................................................................................... 25 ORDENADO POR CODIGO B.E. ....................................................................................................... 27 COOPERATIVAS DE CREDITO ORDENADO ALFABETICAMENTE .................................................................................................... 31 ORDENADO POR CODIGO B.E. ....................................................................................................... 33 ESTABLECIMIENTOS FINANCIEROS DE CREDITO ORDENADO ALFABETICAMENTE .................................................................................................... 45 ORDENADO POR CODIGO B.E. ....................................................................................................... 47 ESTABLECIMIENTOS FINANCIEROS DE CREDITO ENTIDADES DE PAGO