Management Discussion and Analysis — Business Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BMJ in the News Is a Weekly Digest of Journal Stories, Plus Any Other News About the Company That Has Appeared in the National A

BMJ in the News is a weekly digest of journal stories, plus any other news about the company that has appeared in the national and a selection of English-speaking international media. A total of 21 journals were picked up in the media last week (1-7 April) - our highlights include: ● A study in The BMJ finding that routine HPV vaccination has led to a dramatic reduction in cervical disease among young women in Scotland was covered extensively, including BBC Radio 4 Today, The Guardian and Cosmopolitan. ● Research in Tobacco control suggesting that vaping has not re-normalised tobacco smoking among teens was picked up by The Independent, The Irish Times and The South China Morning Post ● A paper in the Archives of Disease in Childhood on misleading health claims on kids’ snacks packaging was picked up by The Times, BBC News and The Daily Telegraph. PRESS RELEASES BMJ | The BMJ Thorax | Tobacco Control Archives of Disease in Childhood | Vet Record EXTERNAL PRESS RELEASES The BMJ OTHER COVERAGE The BMJ | Annals of the Rheumatic Diseases BMJ Case Reports | BMJ Global Health BMJ Nutrition, Prevention & Health | BMJ Open BMJ Open Quality | BMJ Open Sport & Exercise Medicine British Journal of Sports Medicine | Heart Journal of Epidemiology & Community Health | Journal of Investigative Medicine Journal of Medical Ethics | Journal of Medical Genetics Journal of Neurology Neurosurgery & Psychiatry Journal of the Royal Army Medical Corps | Occupational & Environmental Medicine B MJ New Editor-in-Chief for BMJ Open Sport & Exercise Medicine journal InPublishing 02/04/2019 (PR) Health Education England chooses BMJ Best Practice InPublishing 03/04/19 (PR) Antiseptics and Disinfectants Market Size Worth $27.99 Billion by 2026: Grand View Research, Inc. -

Reuters Institute Digital News Report 2020

Reuters Institute Digital News Report 2020 Reuters Institute Digital News Report 2020 Nic Newman with Richard Fletcher, Anne Schulz, Simge Andı, and Rasmus Kleis Nielsen Supported by Surveyed by © Reuters Institute for the Study of Journalism Reuters Institute for the Study of Journalism / Digital News Report 2020 4 Contents Foreword by Rasmus Kleis Nielsen 5 3.15 Netherlands 76 Methodology 6 3.16 Norway 77 Authorship and Research Acknowledgements 7 3.17 Poland 78 3.18 Portugal 79 SECTION 1 3.19 Romania 80 Executive Summary and Key Findings by Nic Newman 9 3.20 Slovakia 81 3.21 Spain 82 SECTION 2 3.22 Sweden 83 Further Analysis and International Comparison 33 3.23 Switzerland 84 2.1 How and Why People are Paying for Online News 34 3.24 Turkey 85 2.2 The Resurgence and Importance of Email Newsletters 38 AMERICAS 2.3 How Do People Want the Media to Cover Politics? 42 3.25 United States 88 2.4 Global Turmoil in the Neighbourhood: 3.26 Argentina 89 Problems Mount for Regional and Local News 47 3.27 Brazil 90 2.5 How People Access News about Climate Change 52 3.28 Canada 91 3.29 Chile 92 SECTION 3 3.30 Mexico 93 Country and Market Data 59 ASIA PACIFIC EUROPE 3.31 Australia 96 3.01 United Kingdom 62 3.32 Hong Kong 97 3.02 Austria 63 3.33 Japan 98 3.03 Belgium 64 3.34 Malaysia 99 3.04 Bulgaria 65 3.35 Philippines 100 3.05 Croatia 66 3.36 Singapore 101 3.06 Czech Republic 67 3.37 South Korea 102 3.07 Denmark 68 3.38 Taiwan 103 3.08 Finland 69 AFRICA 3.09 France 70 3.39 Kenya 106 3.10 Germany 71 3.40 South Africa 107 3.11 Greece 72 3.12 Hungary 73 SECTION 4 3.13 Ireland 74 References and Selected Publications 109 3.14 Italy 75 4 / 5 Foreword Professor Rasmus Kleis Nielsen Director, Reuters Institute for the Study of Journalism (RISJ) The coronavirus crisis is having a profound impact not just on Our main survey this year covered respondents in 40 markets, our health and our communities, but also on the news media. -

Contact Information for Non-USC Activities

6/16/17 CURRICULUM VITAE JOEL W. HAY, PhD PERSONAL INFORMATION Business/Mail Address Professor of Pharmaceutical Economics and Policy & Professor of Health Policy and Economics University of Southern California Schaeffer Center for Health Policy and Economics University Park Campus, Verna & Peter Dauterive Hall (VPD 214-L) 635 Downey Way Los Angeles, CA 90089-3333 USA Business Telephone Office: (818) 338-5433 Assistant: (213) 821-7940 Fax: (213) 740-3460 (ATTN: Joel Hay) E-Mail [email protected] USC Websites : http://healthpolicy.usc.edu/ListItem.aspx?ID=4 http://pharmacyschool.usc.edu/faculty/profile/?id=374 Graduate Program Website : http://pharmacyschool.usc.edu/programs/pep/ Schaeffer Center Street Address 635 Downey Way Los Angeles, CA 90089-3333 USA (Deliveries, e.g. Fedex, UPS) Main Phone/Front Desk: (213) 821-7940 J Hay Office: (213) 821-8160 Fax: (213) 740-3460 (ATTN: Samantha) http://healthpolicy.usc.edu Contact Information for Non-USC Activities Joel W. Hay, PhD 22101 Dardenne St. Calabasas, CA 91302 818-338-5433 [email protected] Joel W. Hay, Ph.D. -- C.V. -2- 6/16/17 EDUCATION 1974 B.A. (Summa cum laude), Economics, Amherst College 1975 M.A., Economics, Yale University 1976 M.Phil., Economics, Yale University 1980 Ph.D., Economics, Yale University PROFESSIONAL EXPERIENCE March 2009 – Present Full Professor (with tenure), Pharmaceutical Economics and Policy; School of Pharmacy Professor (by courtesy), Department of Economics; University of Southern California, Los Angeles, California. September 2009-Present Full Professor, Health Economics and Policy Leonard D. Schaeffer Center for Health Policy and Economics University of Southern California, Los Angeles, California 1992 – 2009 Associate Professor (with tenure), Pharmaceutical Economics and Policy; School of Pharmacy. -

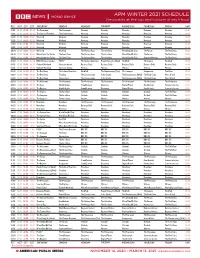

APM WINTER 2021 SCHEDULE Newscasts at the Top and Bottom of Each Hour

APM WINTER 2021 SCHEDULE Newscasts at the top and bottom of each hour PST MST CST EST SATURDAY SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY GMT 21:00 22:00 23:00 00:00 The Newsroom The Newsroom Newsday Newsday Newsday Newsday Newsday 05:00 21:30 22:30 23:30 00:30 The Cultural Frontline The Conversation Newsday Newsday Newsday Newsday Newsday 05:30 22:00 23:00 00:00 01:00 Weekend Weekend Newsday Newsday Newsday Newsday Newsday 06:00 22:30 23:30 00:30 01:30 Weekend Weekend Newsday Newsday Newsday Newsday Newsday 06:30 23:00 00:00 01:00 02:00 Weekend Weekend Newsday Newsday Newsday Newsday Newsday 07:00 23:30 00:30 01:30 02:30 Weekend Weekend Newsday Newsday Newsday Newsday Newsday 07:30 00:00 01:00 02:00 03:00 Weekend Weekend The History Hour The Arts Hour W’end Doc/Bk Club The Forum The Real Story 08:00 00:30 01:30 02:30 03:30 When Katty Met Carlos The Food Chain The History Hour The Arts Hour W’end Doc/Bk Club The Forum The Real Story 08:30 00:50 01:50 02:50 03:50 When Katty Met Carlos The Food Chain The History Hour The Arts Hour W’end Doc/Bk Club Sporting Witness The Real Story 08:50 01:00 02:00 03:00 04:00 BBC OS Conversations FOOC* The Climate Question People Fixing the World HardTalk The Inquiry HardTalk 09:00 01:30 02:30 03:30 04:30 Outlook Weekend Science in Action Business Daily Business Daily Business Daily Business Daily Business Daily 09:30 01:50 02:50 03:50 04:50 Outlook Weekend Science in Action Witness Witness Witness Witness Witness 09:50 02:00 03:00 04:00 05:00 The Real Story The Cultural Frontline HardTalk The Documentary -

South Asia Your Guide to the BBC World Service Schedule from Saturday 8 May 2021

South Asia Your guide to the BBC World Service schedule From Saturday 8 May 2021 https://wspartners.bbc.com/ GMT+8 GMT Saturday Sunday Monday Tuesday Wednesday Thursday Friday GMT 00:00 16:00 BBC OS News Bulletin News Bulletin BBC OS BBC OS BBC OS BBC OS 16:00 00:06 16:06 Sportsworld Sportsworld 16:06 00:30 16:30 News Update News Update News Update News Update News Update 16:30 00:32 16:32 BBC OS BBC OS BBC OS BBC OS BBC OS 16:32 01:00 17:00 News Bulletin The Newsroom News Bulletin News Bulletin News Bulletin News Bulletin News Bulletin 17:00 01:06 17:06 The Fifth Floor Sportsworld Outlook Outlook Outlook Outlook 17:06 01:30 17:30 News Update News Update News Update News Update News Update News Update 17:30 01:32 17:32 The Fifth Floor Trending Outlook Outlook Outlook Outlook 17:32 01:50 17:50 Witness Sporting Witness Witness Witness Witness Witness 17:50 02:00 18:00 The Newsroom News Bulletin The Newsroom The Newsroom The Newsroom The Newsroom The Newsroom 18:00 02:06 18:06 The History Hour* 18:06 02:30 18:30 News Update News Update News Update News Update News Update News Update News Update 18:30 02:32 18:32 Sport Today The History Hour* The Cultural Frontline Sport Today Sport Today Sport Today Sport Today 18:32 03:00 19:00 News Bulletin News Bulletin News Bulletin News Bulletin News Bulletin News Bulletin News Bulletin 19:00 03:06 19:06 Tech Tent The Arts Hour Business Weekly The Climate Question The Documentary (Tue) The Compass Assignment 19:06 03:30 19:30 News Update News Update News Update News Update News Update News Update News -

The Middle East and Countries of The

THE MIDDLE EAST and countries of the FSU A GUIDE to LISTENING IN ENGLISH GMT +2 TO GMT +4⁄ NOVEMBER 2010 – marcH 2011 including Egypt, Eastern Mediterranean (GMT +2), Sudan, Gulf States, Iraq (GMT +3), Iran (GMT +3∕), UAE (GMT +4) and South Afghanistan (GMT +4∕) Where you see this sign v you will hear a short News Update at 30 minutes past the hour GMT SaturdaY SundaY MondaY TuesdaY WednesdaY ThursdaY FridaY GMT 0:00 News News World Briefing v World Briefing v World Briefing v World Briefing v World Briefing v 0:00 0:06 Global Business v Heart & Soul (P) 0:06 0:32 The Interview One Planet (P) 0:32 0:41 Sports Roundup Sports Roundup Sports Roundup Sports Roundup Sports Roundup 0:41 0:50 Witness Witness Witness Witness Witness 0:50 1:00 News World Briefing News News News News News 1:00 1:06 Friday Documentary v The Forum v Monday Documentary v Global Business v Wednesday Documentary v Assignment v 1:06 1:20 Sports Roundup v 1:20 1:32 Science in Action FOOC Health Check Digital Planet Discovery One Planet 1:32 2:00 News News World Briefing News News News News 2:00 2:06 Outlook v Assignment v Outlook v Outlook v Outlook v Outlook v 2:06 2:20 World Business News v 2:20 2:32 The Strand World of Music Letter From..... The Strand The Strand The Strand The Strand 2:32 2:41 Over to You 2:41 3:00 The World Today v The World Today v The World Today v The World Today v The World Today v The World Today v The World Today v 3:00 3:32 Politics UK Something Understood Digital Planet Americana HARDtalk/Bottom Line Heart & Soul Crossing Continents/FOOC 3:32 -

THE MIDDLE EAST and Countries of The

THE MIDDLE EAST and countries of the FSU A GUIDE TO LISTENING IN ENGLISH GMT +3 TO GMT +4½ MARCH – OCTOBER 2021 including Eastern Mediterranean, Gulf States, North and South Sudan, Iraq (GMT +3), UAE (GMT +4), Iran and South Afghanistan (GMT +4½) Where you see this sign v you will hear a short News Update at 30 minutes past the hour GMT SATURDAY SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY GMT 0:00 News News News News News News News 0:00 0:06 Business Matters v The Science Hour World Business Report v Business Matters v Business Matters v Business Matters v Business Matters v 0:06 0:32 Discovery (rpt) 0:32 1:00 The Newsroom v The Newsroom v The Newsroom v The Newsroom v The Newsroom v The Newsroom v The Newsroom v 1:00 1:32 The Conversation When Katty Met Carlos The Climate Question The Documentary (Tue) The Compass Assignment World Football 1:32 2:00 News News News News News News News 2:00 2:06 The Fifth Floor v Weekend Weekend Feature v Outlook v Outlook v Outlook v Outlook v 2:06 2:32 Documentary v (B) The Story 2:32 2:50 Witness Over To You Witness Witness Witness Witness 2:50 3:00 News News The Newsroom v The Newsroom v The Newsroom v The Newsroom v The Newsroom v 3:00 3:06 The Real Story (rpt) v FOOC v 3:06 3:32 The Cultural Frontline The Conversation In The Studio The Documentary (Wed) The Food Chain Heart & Soul 3:32 4:00 The Newsroom v The Newsroom v Newsday v Newsday v Newsday v Newsday v Newsday v 4:00 4:32 Trending The Documentary (Tue) 4:32 4:50 Ros Atkins On… (rpt) 4:50 5:00 Weekend v Weekend v Newsday v Newsday v Newsday -

Louisiana Press Association Cox, Not Dukes Himself As Dukes to Add Items to the Agenda

May 2016 THE Serving Louisiana Newspapers since 1880 LOUISIANA PRESS LPA’s Convention is June 17-18 LPA’s Annual Convention will take place June 17-18 at L’Auberge Lake Charles. The Room rate is $199 per night. For Calendar individual reservations:, please call 866- 580-7444 and use Group Code: SLPA16.. Speakers this year include Tim Smith talking about “Bundling Print with May 2016 Digital” and Lisa Tackett Griffin giving a 12: Webinar: Three-Call Sales “Newspaper Technology Update” and also System: Proven process for talking about “InDesign: Favorite Features.” closing sales quickly There will also be a “Hot Topics” Panel 19: Webinar: Creating focus on Discussion featuring Billy Gunn of The enterprise news: Best practices for Advocate, discussing the police shooting digging deeper in Marksville; Christiaan Mader of The Lafayette theatre shooting. Independent (Lafayette) discussing the As always, the Silent Auction will be June 2016 Lafayette City Marshall given jail time open and the convention will close with 3: Webinar: How to market and community service for not honoring a the annual Awards Luncheon. and sell in brutally compeitive public records request and Calie Taylor of See page 9A for the complete environments The Advertiser (Lafayette) discussing the convention schedule. 9: Webinar: Interactive storytelling tools; Enhance your readers’ experience Legislative Wrap-Up 16-18: LPA Annual Convention: On a TV morning show recently, House committee and is awaiting Lake Charles a political commentator said of the action on the House floor. There is a presidential races for party nominees, systematic national effort to do away For more information on the fat lady hasn’t sung yet, but she’s with this publication in every state. -

4 December 2020 Page 1 of 17 SATURDAY 28 NOVEMBER 2020 Already Set up and Ready for Business

World Service Listings for 28 November – 4 December 2020 Page 1 of 17 SATURDAY 28 NOVEMBER 2020 already set up and ready for business. BBC Thai's Chaiyot SAT 06:06 Weekend (w172x7d5fr78h9f) Yongcharoenchai set out to crack the mystery of the self-styled Iranian nuclear scientist killed SAT 00:00 BBC News (w172x5p5kcw9djy) "CIA" food hawkers. The latest five minute news bulletin from BBC World Service. Iran has urged the United Nations to condemn the assassination ‘They messed with the wrong generation’ of its top nuclear scientist, Mohsen Fakhrizadeh, and it's Peru has been in the headlines for having three presidents in a pointed the finger at Israel. We explore how the incoming SAT 00:06 The Real Story (w3cszcnx) week. It’s a story of corruption allegations, impeachment and Biden administration's relationship with its traditional ally will Covid vaccines: An opportunity for science? mass protests, with young people saying their generation has shape regional tensions. had enough of the broken system which their parents put up The rapid development of coronavirus vaccines has heightened with. Ana Maria Roura has been making sense of events for Also on the programme: The number of confirmed coronavirus the hope for a world free of Covid-19. Governments have BBC Mundo. cases in the United States has passed thirteen million, with the ordered millions of doses, health care systems are prioritising pandemic still surging from coast to coast; And a new recipients, and businesses are drawing up post-pandemic plans. Lahore's toxic smog documentary explores Frank Zappa the man, his music, and But despite these positive signs, many people still feel a sense It's the time of year when many Pakistani rice farmers set fire politics. -

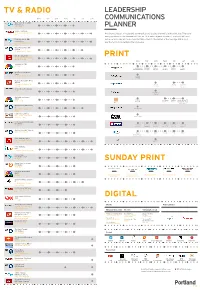

Print Digital Tv & Radio Sunday Print

TV & RADIO LEADERSHIP MON TUE WED THUR FRI SAT SUN COMMUNICATIONS Wake Up to Money, BBC Radio 5 Live 5:15 - 6 am PLANNER Sunrise, Sky News 6 - 9 am; Sat & Sun: 6 - 10 One important part of leadership communications is using the media in the right way. There are am many opportunities to communicate live on TV or radio, in print or online. Each has a different 5 Live Breakfast, BBC audience and some will be more suited than others to the leader or the message. But a good Radio 5 Live 6 - 10 am; Sat & Sun 6 - 9 way to start is to understand the landscape. am Today Programme, BBC Radio 4 6 - 9 am; Sat: 7 - 9 am BBC Breakfast, BBC 1 PRINT 6 - 9:15 am ; Sat: 6 - 10 am, Sun: 6 - 7:40 am MON TUE WED THUR FRI SAT SUN Squawkbox, CNBC 6 - 9 am Monday Manifesto; Business Business Business Business Business Business Big Shot Big Shot Big Shot Big Shot Big Shot Big Shot Nick Ferrari Show, LBC Radio 7 - 10 am; Sat: 5 - 7 am Monday Interview Business Daily, BBC World Service 7:32 am; 14.06 pm & Fri Society Friday Saturday 7.32 am Interview Interview Interview (varies) On the Move, Bloomberg 9 am The Business Interview Worldwide Exchange, CNBC Monday 9 am - 11 pm Recruitment Business Lunch with the FT; Interview Interview Speak Person in the News; My Weekend Woman’s Hour, BBC Radio 4 Mon - Fri: 10 - 11 am; Sat: Monday View 4-5pm Daily Politics, BBC 2 Mon - Fri: 12 - 1 pm; Wed: Growth Capital 11:30 am - 1 pm In The Loop with Betty Liu, Bloomberg 1 - 3pm 60 Second 60 Second 60 Second 60 Second 60 Second 60 Second Interview Interview Interview Interview Interview -

Siriusxm Celebrates Black History Month with Special Programming Across Talk and Comedy Channels

NEWS RELEASE SiriusXM Celebrates Black History Month with Special Programming Across Talk and Comedy Channels 2/1/2021 From business to culture to medicine and beyond, Black history and achievements will be honored by SiriusXM throughout February NEW YORK, Feb. 1, 2021 /PRNewswire/ -- SiriusXM announced today that it will celebrate Black History Month by oering listeners a wide variety of programming across SiriusXM's talk and comedy channels. Beginning today, the specials will highlight the lasting contributions of Black Americans in history, culture, business, and our society. SiriusXM's Urban View (channel 126) is the home for dynamic discourse from prominent Black voices, dedicated to around-the-clock coverage of the Black experience. Urban View takes on even more signicance each February, and this year the channel is amplifying Black voices at a vital moment in the country's history. Some of the specials which can be heard on the channel include: Joe Madison, leader in the cause for social justice, human and civil rights activist, and member of the NAACP's national board of directors, uses his SiriusXM program as a platform for inspiring change and demanding action. In honor of Black History Month, "The Black Eagle" will host a virtual event with the Ford Men of Courage National Leadership Forum in partnership with Morehouse College. The panel will include Morehouse President Dr. David A. Thomas; author Shaka Senghor, and others who will share stories of inspiration, sacrice, and success. The special will air mid-February on "The Joe Madison Show." Pulitzer Prize-winning journalist, professor, publisher and SiriusXM host Karen Hunter will feature an original content series, "Black History Changemakers," weekdays in February showcasing Black heroes and hidden gures in history, science, law, banking, politics, sports, TV, lm, music, and more. -

BBC Schedule DRM Winter 2013

BBC Schedule DRM Winter 2013 IST GMT Saturday Sunday Monday Tuesday Wednesday Thursday Friday GMT 19:30 14:00 BBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI Transmission 14:00 19:36 14:06 BBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI TransmissionBBC HINDI Transmission 14:06 19:59 14:29 BBC News Update BBC News Update BBC News Update BBC News Update BBC News Update BBC News Update BBC News Update 14:29 20:02 14:32 Science in Action The Science Hour Newshour Newshour Newshour Newshour Newshour 14:32 20:20 14:50 Trending The Science Hour Newshour Newshour Newshour Newshour Newshour 20:30 15:00 BBC News The Newsroom BBC News BBC News BBC News BBC News BBC News 15:00 20:36 15:06 Sportsworld The Newsroom Business Daily Business Daily Business Daily Business Daily Business Daily 15:06 20:59 15:29 Sportsworld BBC News Update BBC News Update BBC News Update BBC News Update BBC News Update BBC News Update 15:29 21:02 15:32 Sportsworld Boston Calling Heart and Soul The Documentary Global Business Assignment World Football 15:32 21:30 16:00 BBC News BBC News The Newsroom The Newsroom The Newsroom The Newsroom The Newsroom 16:00 21:36 16:06 Sportsworld FOOC The Newsroom The Newsroom The Newsroom The Newsroom The Newsroom 16:06 21:59 16:29 Sportsworld BBC News Update BBC News Update BBC News Update BBC News Update BBC News Update BBC News Update 16:29 22:02 16:32 Sportsworld Heart and