1Q20 Baron Discovery Strategy Letter

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

OSB Representative Participant List by Industry

OSB Representative Participant List by Industry Aerospace • KAWASAKI • VOLVO • CATERPILLAR • ADVANCED COATING • KEDDEG COMPANY • XI'AN AIRCRAFT INDUSTRY • CHINA FAW GROUP TECHNOLOGIES GROUP • KOREAN AIRLINES • CHINA INTERNATIONAL Agriculture • AIRBUS MARINE CONTAINERS • L3 COMMUNICATIONS • AIRCELLE • AGRICOLA FORNACE • CHRYSLER • LOCKHEED MARTIN • ALLIANT TECHSYSTEMS • CARGILL • COMMERCIAL VEHICLE • M7 AEROSPACE GROUP • AVICHINA • E. RITTER & COMPANY • • MESSIER-BUGATTI- CONTINENTAL AIRLINES • BAE SYSTEMS • EXOPLAST DOWTY • CONTINENTAL • BE AEROSPACE • MITSUBISHI HEAVY • JOHN DEERE AUTOMOTIVE INDUSTRIES • • BELL HELICOPTER • MAUI PINEAPPLE CONTINENTAL • NASA COMPANY AUTOMOTIVE SYSTEMS • BOMBARDIER • • NGC INTEGRATED • USDA COOPER-STANDARD • CAE SYSTEMS AUTOMOTIVE Automotive • • CORNING • CESSNA AIRCRAFT NORTHROP GRUMMAN • AGCO • COMPANY • PRECISION CASTPARTS COSMA INDUSTRIAL DO • COBHAM CORP. • ALLIED SPECIALTY BRASIL • VEHICLES • CRP INDUSTRIES • COMAC RAYTHEON • AMSTED INDUSTRIES • • CUMMINS • DANAHER RAYTHEON E-SYSTEMS • ANHUI JIANGHUAI • • DAF TRUCKS • DASSAULT AVIATION RAYTHEON MISSLE AUTOMOBILE SYSTEMS COMPANY • • ARVINMERITOR DAIHATSU MOTOR • EATON • RAYTHEON NCS • • ASHOK LEYLAND DAIMLER • EMBRAER • RAYTHEON RMS • • ATC LOGISTICS & DALPHI METAL ESPANA • EUROPEAN AERONAUTIC • ROLLS-ROYCE DEFENCE AND SPACE ELECTRONICS • DANA HOLDING COMPANY • ROTORCRAFT • AUDI CORPORATION • FINMECCANICA ENTERPRISES • • AUTOZONE DANA INDÚSTRIAS • SAAB • FLIR SYSTEMS • • BAE SYSTEMS DELPHI • SMITH'S DETECTION • FUJI • • BECK/ARNLEY DENSO CORPORATION -

2021 Honored Companies Please Join Us As We Give Special Recognition and Honor S&P 500 and F1000 Companies with at Least 35% of Board Seats Held by Women

Cipriani 42nd St | November 10, 2021 | 7:30 AM-11:00 AM 2021 Honored Companies Please join us as we give special recognition and honor S&P 500 and F1000 companies with at least 35% of board seats held by women. 50% + AMN Healthcare General Motors Co. Sally Beauty Holdings, Inc. Autodesk, Inc. Hasbro, Inc. Schnitzer Steel Industries, Inc. Bed, Bath & Beyond, Inc. Hawaiian Electric Industries, Inc. Science Applications International Corporation (SAIC) Best Buy Companies Inc. Healthpeak Properties, Inc. Steelcase Inc. Big Lots Inc. Herman Miller, Inc. Summit Materials, Inc. Bright Horizons Family Solutions, Inc. HNI Corporation Tapestry, Inc. Caleres, Inc. J.Crew Group, Inc. Thrivent Financial Casey’s General Stores, Inc. L Brands, Inc. TIAA Celanese Corporation Micron Technology Inc Tiffany & Co. Chico’s Fas, Inc. Navient Corporation ULTA Beauty Inc. Citi Omnicom Group Inc. ViacomCBS Inc. Coty Inc. PC Connection, Inc. Welltower Inc. DaVita Pitney Bowes, Inc. Western Digital Corporation EQT Corporation The Procter & Gamble Co. Williams-Sonoma, Inc. Etsy, Inc. The Progressive Corporation 40% + Abercrombie & Fitch Co. Genworth Financial The ODP Corporation ABM Industries, Inc. Globe Life Inc. Penn Mutual Accenture The Goldman Sachs Group, Inc. Phillips 66 Company AES Corporation Groupon Inc. Principal Financial Group Inc. Afliated Managers Group (AMG) H & R Block, Inc. PROG Holdings, Inc. AGNC Investment Corp. The Hershey Companies Quest Diagnostics Inc. Alliant Energy Hewlett Packard Enterprise RR Donnelley & Sons Co. Amazon.com, Inc. Hill-Rom Holdings Inc. Reinsurance Group Of America, Inc. American Water Works, Inc. Hilton Worldwide Holdings, Inc. Reliance Steel and Aluminum Co. Amica Mutual Insurance Company HP Inc. -

1St Quarter Report

Quarterly Holdings Report for Fidelity® Variable Insurance Products: Mid Cap Portfolio March 31, 2021 VIPMID-QTLY-0521 1.799869.117 Schedule of Investments March 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 99.3% Shares Value Shares Value COMMUNICATION SERVICES – 3.5% Tapestry, Inc. 673,600 $ 27,759,056 Entertainment – 2.3% thredUP, Inc. (b) 26,600 620,578 Activision Blizzard, Inc. 1,187,600 $ 110,446,800 236,705,162 Cinemark Holdings, Inc. (a) 612,400 12,499,084 TOTAL CONSUMER DISCRETIONARY 1,215,512,530 Electronic Arts, Inc. 287,790 38,958,132 Live Nation Entertainment, Inc. (b) 245,500 20,781,575 182,685,591 CONSUMER STAPLES – 5.3% Interactive Media & Services – 0.5% Beverages – 0.6% Bumble, Inc. 39,400 2,457,772 C&C Group PLC (United Kingdom) (b) 7,982,445 30,922,922 IAC (b) 179,700 38,870,907 Monster Beverage Corp. (b) 183,000 16,669,470 41,328,679 47,592,392 Media – 0.7% Food & Staples Retailing – 2.6% Interpublic Group of Companies, Inc. 1,986,185 57,996,602 BJ’s Wholesale Club Holdings, Inc. (b) 1,891,100 84,834,746 Performance Food Group Co. (b) 1,118,796 64,453,838 TOTAL COMMUNICATION SERVICES 282,010,872 U.S. Foods Holding Corp. (b) 1,638,300 62,451,996 211,740,580 CONSUMER DISCRETIONARY – 15.0% Food Products – 1.1% Automobiles – 0.2% Nomad Foods Ltd. (b) 3,382,400 92,880,704 Harley‑Davidson, Inc. 474,400 19,023,440 Household Products – 1.0% Diversified Consumer Services – 0.6% Spectrum Brands Holdings, Inc. -

COVERAGE LIST GEO Group, Inc

UNITED STATES: REIT/REOC cont’d. UNITED STATES: REIT/REOC cont’d. UNITED STATES: NON-TRADED REITS cont’d. COVERAGE LIST GEO Group, Inc. GEO Sabra Health Care REIT, Inc. SBRA KBS Strategic Opportunity REIT, Inc. Getty Realty Corp. GTY Saul Centers, Inc. BFS Landmark Apartment Trust, Inc. Gladstone Commercial Corporation GOOD Select Income REIT SIR Lightstone Value Plus Real Estate Investment Trust II, Inc. Gladstone Land Corporation LAND Senior Housing Properties Trust SNH Lightstone Value Plus Real Estate Investment Trust III, Inc. WINTER 2015/2016 • DEVELOPED & EMERGING MARKETS Global Healthcare REIT, Inc. GBCS Seritage Growth Properties SRG Lightstone Value Plus Real Estate Investment Trust, Inc. Global Net Lease, Inc. GNL Silver Bay Realty Trust Corp. SBY Moody National REIT I, Inc. Government Properties Income Trust GOV Simon Property Group, Inc. SPG Moody National REIT II, Inc. EUROPE | AFRICA | ASIA-PACIFIC | MIDDLE EAST | SOUTH AMERICA | NORTH AMERICA Gramercy Property Trust Inc. GPT SL Green Realty Corp. SLG MVP REIT, Inc. Gyrodyne, LLC GYRO SoTHERLY Hotels Inc. SOHO NetREIT, Inc. HCP, Inc. HCP Sovran Self Storage, Inc. SSS NorthStar Healthcare Income, Inc. UNITED KINGDOM cont’d. Healthcare Realty Trust Incorporated HR Spirit Realty Capital, Inc. SRC O’Donnell Strategic Industrial REIT, Inc. EUROPE Healthcare Trust of America, Inc. HTA St. Joe Company JOE Phillips Edison Grocery Center REIT I, Inc. GREECE: Athens Stock Exchange (ATH) AFI Development Plc AFRB Hersha Hospitality Trust HT STAG Industrial, Inc. STAG Phillips Edison Grocery Center REIT II, Inc. AUSTRIA: Vienna Stock Exchange (WBO) Babis Vovos International Construction S.A. VOVOS Alpha Pyrenees Trust Limited ALPH Highwoods Properties, Inc. -

Thomas Mitchell Telephone : 484-709-7589 E-Mail : [email protected]

Contact Information Thomas Mitchell Telephone : 484-709-7589 e-mail : [email protected] Address 28 Nancy Circle, Reading, PA 19606 Profile Objective To secure a challenging position with a stable organization offering opportunity for growth, advancement, & utilization of my senior-level skills & knowledge. Availability 2 Weeks Key Skills Significant senior-level working experience with a vast array of concepts & technologies, including (not limited to): Active Directory 2K – 2K16 Windows 2K - 2K16 PowerShell Microsoft Azure Exchange 5.5 - 2K16 VMWare / Hyper-V SAN / Clustering / EMC Dell / IBM / HP Hardware O365 / Exchange Online Project Management DNS / WINS / DHCP Certificate Svcs / PKI OWA / ActiveSync Citrix XenApp 6.0 Microsoft WSUS SharePoint Services In addition to the above skill sets, I possess very strong oral and written communication skills and I require very little to no direct supervision to perform my job functions effectively. I am a solutions-oriented self-starter. Education 1991 to 1993 A.S. Degree – Computer Engineering Technology CHI Institute, Southampton, PA Certifications MCSE: Cloud Platform & Infrastructure (Azure), MCSA: Windows Server 2012, MCSA: Windows Server 2008, MCTS Numerous MCP Certifications, including Messaging VMWare VCP 5.1 (Recently Completed Classroom-Based 6.0 Certification Training) Recently Passed the “Managing Office 365 Identities and Requirements” Exam Preparing to Complete the O365 MCSA Work Experience CONFIDENTIAL, East Norriton, PA Employee Senior Systems Engineer 2017 to Present -

Public Competition Enforcement Review

Enforcement Review Enforcement the Public Competition Competition Public Public Competition Enforcement Review Eleventh Edition Editor Aidan Synnott Eleventh Edition lawreviews © 2019 Law Business Research Ltd Public Competition Enforcement Review Eleventh Edition Reproduced with permission from Law Business Research Ltd This article was first published in May 2019 For further information please contact [email protected] Editor Aidan Synnott lawreviews © 2019 Law Business Research Ltd PUBLISHER Tom Barnes SENIOR BUSINESS DEVELOPMENT MANAGER Nick Barette BUSINESS DEVELOPMENT MANAGER Joel Woods SENIOR ACCOUNT MANAGERS Pere Aspinall, Jack Bagnall ACCOUNT MANAGERS Olivia Budd, Katie Hodgetts, Reece Whelan PRODUCT MARKETING EXECUTIVE Rebecca Mogridge RESEARCH LEAD Kieran Hansen EDITORIAL COORDINATOR Tommy Lawson HEAD OF PRODUCTION Adam Myers PRODUCTION EDITOR Caroline Herbert SUBEDITOR Tessa Brummitt CHIEF EXECUTIVE OFFICER Paul Howarth Published in the United Kingdom by Law Business Research Ltd, London 87 Lancaster Road, London, W11 1QQ, UK © 2019 Law Business Research Ltd www.TheLawReviews.co.uk No photocopying: copyright licences do not apply. The information provided in this publication is general and may not apply in a specific situation, nor does it necessarily represent the views of authors’ firms or their clients. Legal advice should always be sought before taking any legal action based on the information provided. The publishers accept no responsibility for any acts or omissions contained herein. Although the information -

2014 Gaming Conference April 13-16, 2014 the Mirage Casino and Resort, Las Vegas, NV

2014 Gaming Conference April 13-16, 2014 The Mirage Casino and Resort, Las Vegas, NV Sunday April 13, 2014 3:00 – 6:00 PM WRK-1 Viva Elvis, Viva Las Vegas: Business Communication Lessons From the Entertainment Capital of the World Ralph Villanueva, CIA, CRMA IT Security and Compliance Analyst The LVH – Las Vegas Hotel and Casino Discuss issues that typically keep audit professionals from effectively communicating their reports and recommendations to various stakeholders. Learn to apply “Vegas-style” principles to make business communications as interesting and entertaining as the Entertainment Capital of the world. Participate in group exercises designed to practice enlivening and reinvigorating audit presentations. Critique a mock presentation of an audit report to reinforce lessons learned. Ralph Villanueva has more than 20 years’ professional experience in accounting, auditing, financial management, and fraud examination in the United States, Philippines, and other Asia-Pacific countries. In his current role, he oversees compliance with the company's internal controls, Nevada gaming regulations on IT, and COBIT. Villaneuva is an in-demand speaker and contributes articles for numerous trade publications. Learning Level: Intermediate Learning Field: Communication Monday April 14, 2014 9:00 – 10:00 AM GS 1 Global and Domestic Expansion of the Gaming Industry Geoff Freeman President and Chief Executive Officer American Gaming Association Hear how AGA plans to promote the value of gaming at state and local levels. Learn about the value of regulated gaming. Explore the future of gaming, globally and within the United States. 2014 Gaming Conference April 13-16, 2014 The Mirage Casino and Resort, Las Vegas, NV Geoff Freeman is the leading advocate for the commercial gaming industry, responsible for positioning the association to address regulatory, political, and educational challenges and opportunities. -

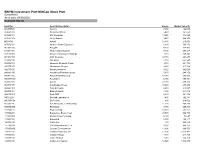

BNYM Investment Port:Midcap Stock Port (Unaudited) As of Date: 09/30/2020 Common Stocks

BNYM Investment Port:MidCap Stock Port (Unaudited) As of date: 09/30/2020 Common Stocks Identifier Security Description Shares Market Value ($) 002535300 Aaron's 7,450 422,043 00404A109 Acadia Healthcare 5,480 161,550 004498101 ACI Worldwide 13,250 346,223 00508Y102 Acuity Brands 9,470 969,255 BD845X2 Adient 12,480 216,278 00737L103 Adtalem Global Education 6,800 166,872 00766T100 AECOM 4,170 174,473 018581108 Alliance Data Systems 7,130 299,317 01973R101 Allison Transmission Holdings 7,110 249,845 00164V103 AMC Networks 10,710 264,644 023436108 Amedisys 2,760 652,547 025932104 American Financial Group 3,310 221,704 03073E105 AmerisourceBergen 2,220 215,162 042735100 Arrow Electronics 5,620 442,069 04280A100 Arrowhead Pharmaceuticals 5,670 244,150 045487105 Associated Banc-Corp 47,940 605,003 05329W102 Autonation 6,980 369,451 05368V106 Avient 23,030 609,374 053774105 Avis Budget Group 10,600 278,992 05464C101 Axon Enterprise 2,410 218,587 062540109 Bank of Hawaii 4,830 244,012 06417N103 Bank OZK 6,630 141,352 090572207 Bio-Rad Laboratories 1,480 762,881 09073M104 Bio-Techne 880 218,002 05550J101 BJs Wholesale Club Holdings 11,270 468,269 09227Q100 Blackbaud 3,750 209,363 103304101 Boyd Gaming 18,350 563,162 105368203 Brandywine Realty Trust 93,500 966,790 11120U105 Brixmor Property Group 6,300 73,647 117043109 Brunswick 8,150 480,117 12685J105 Cable One 300 565,629 127190304 CACI International, Cl. A 3,980 848,377 12769G100 Caesars Entertainment 11,890 666,553 133131102 Camden Property Trust 11,390 1,013,482 134429109 Campbell Soup 4,440 -

SCHEDULE 14A Proxy Statement Pursuant to Section 14(A) of the Securities Exchange Act of 1934

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 Filed by the Registrant x Filed by a Party other than the Registrant ¨ Check the appropriate box: ¨ Preliminary Proxy Statement ¨ Confidential, for use of the Commission only (as permitted by Rule 14a-6(e)(2)) x Definitive Proxy Statement ¨ Definitive Additional Materials ¨ Soliciting Material under Rule 14a-12 ManTech International Corporation (Name of Registrant as Specified In Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box) x No fee required. ¨ Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (Set forth the amount on which the filing fee is calculated and state how it was determined.): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ¨ Fee paid previously with preliminary materials. ¨ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: 12015 Lee Jackson Highway Fairfax, VA 22033-3300 April 1, 2010 Dear Stockholder: You are cordially invited to attend the 2010 Annual Meeting of Stockholders of ManTech International Corporation, which will be held at The Hyatt Fair Lakes, 12777 Fair Lakes Circle, Fairfax, VA 22033, on Wednesday, May 12, 2010, at 11 am (EDT). -

Top 10 Relative Contributors and Detractors Equity Funds Quarter End As of June 30, 2021

Top 10 Relative Contributors and Detractors Equity Funds Quarter End as of June 30, 2021 Holdings are subject to change. The information below is derived using the portfolio's holdings as of the beginning of each month included in the quarter ending on the date indicated, does not reflect intramonth trading activities, and may not be representative of the current or future investments of the portfolio. Portfolio and index weights below are average weights in each company over the period as represented by the portfolio's holdings or the index's constituents as of the beginning of each month included in the quarter. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy or sell the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. To obtain a list showing every holding as a percentage of the portfolio at the end of the most recent publicly available disclosure period, visit www.dimensional.com. Relative Contribution Difference reflects how the portfolio's holdings impacted return relative to the benchmark. Relative Contribution Difference compares the performance of a security in the portfolio to the benchmark’s total return, factoring in the difference in weight of that security in the benchmark. Returns are calculated using daily security returns and month end weights. In aggregate, portfolio return estimates are gross of advisory fees, may exclude certain derivatives and will differ from actual fund performance. -

The Current Condition and Future Viability of Casino Gaming in Pennsylvania

THE CURRENT CONDITION AND FUTURE VIABILITY OF CASINO GAMING IN PENNSYLVANIA MAY 2014 REPORT SUBMITTED TO: Philip Durgin Executive Director The Pennsylvania Legislative Budget and Finance Committee A Joint Committee of the Pennsylvania General Assembly Office Room 400, Finance Building Harrisburg, PA 17105 REPORT SUBMITTED BY: Econsult Solutions 1435 Walnut Street, Suite 300 Philadelphia, PA 19102 Econsult Solutions, Inc.| 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102 | 215-717-2777 | econsultsolutions.com The Current Condition and Future Viability of Casino Gaming in Pennsylvania | May 2014 1 TABLE OF CONTENTS Table of Contents............................................................................................................................ 1 Executive Summary ........................................................................................................................ 4 1.0 Introduction ......................................................................................................................... 11 2.0 Pennsylvania Gaming Industry Performance ................................................................. 14 2.1 Industry Supply ........................................................................................................... 15 2.1.1 Slot Machine Supply and Revenue ..................................................................... 17 2.1.2 Table Game Supply And Revenue ..................................................................... 19 2.1.3 Revenue Per Position ............................................................................................ -

Prepared Statement of the Federal Trade Commission

Prepared Statement of the Federal Trade Commission Before the Subcommittee on Regulatory Reform, Commercial and Antitrust Law of the Judiciary Committee United States House of Representatives “Oversight of the Antitrust Enforcement Agencies” Washington, D.C. December 12, 2018 Chairman Marino, Ranking Member Cicilline, and members of the Subcommittee, thank you for the opportunity to appear before you today. I am Joe Simons, Chairman of the Federal Trade Commission, and I am pleased to testify on behalf of the Commission and discuss some of our current competition enforcement activities and policy priorities.1 For over 100 years, the FTC has worked to ensure that American markets are open, vibrant, and unencumbered by unreasonable private or public restraints. With its dual missions to promote competition and protect consumers, the FTC applies antitrust and consumer protection law in a dynamic economy that is rapidly responding to new technology. The FTC is committed to understanding how technological developments and globalization can and should impact our law enforcement, research, and advocacy. As commerce and technology continue to evolve, companies may find newer ways to engage in unfair and deceptive practices that cause substantial consumer harm. Companies may also merge or engage in other conduct that harms, or threatens to harm, competition. Our agency tackles these challenges primarily through targeted law enforcement, although we also take full advantage of our unique set of policy tools. Our bipartisan administrative structure, extensive research capabilities, and committed staff enable the FTC to continue to meet its mandate of protecting consumers and competition in an ever-changing marketplace. 1 This written statement represents the views of the Federal Trade Commission.