NASACT News, January 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Pursuit of Financial Return and Societal Benefit: an Examination Of

The Pursuit of Financial Return and Societal Benefit JUNE 2017 AN EXAMINATION OF PENSION FUND ECONOMICALLY TARGETED INVESTMENTS PREPARED BY INSIGHT AT PACIFIC COMMUNITY VENTURES Authors THIS RESEARCH WAS CONDUCTED BY INSIGHT AT PACIFIC Lauren F. Dixon COMMUNITY VENTURES AS PART OF THE ACCELERATING Tom Woelfel IMPACT INVESTING INITIATIVE (AI3) The authors would like to thank John Griffith from Enterprise Community Reader comments and Partners for his leadership on the AI3, as well as Katie Grace Deane, Erin ideas are welcome. Please Shackelford, and David Wood from the Initiative for Responsible Investment, direct correspondence to: [email protected] who served as research advisors for this project. We would also like to thank Kendra Berenson for her research and contributions to this project—this report would not have been possible without her efforts. We are also indebted to the many pension fund managers, researchers, ETI experts, and investors who have shared their knowledge and ideas with us in interviews and subsequent conversations. This report is a direct result of their insights, feedback, and thoughtful direction. Finally, we are deeply grateful for the continued insight and support from the Ford Foundation and Omidyar Network, who have funded this project. PRODUCED BY THE ACCELERATING IMPACT INVESTING INITIATIVE (AI3) The AI3 is a partnership between Enterprise Community Partners and InSight at Pacific Community Ventures, with research support from the Initiative for Responsible Investment. Enterprise works with partners nationwide The Initiative for Responsible Investment PCV InSight is the impact investing to build opportunity, creating and at the Hauser Institute for Civil Society research and consulting practice at advocating for affordable homes at Harvard University is an applied Pacific Community Ventures. -

NASACT News, August 2013

keeping stateNASACT fiscal officials informed news Volume 33, Number 8 August 2013 NASACT Convenes in August for 98th Annual Conference By Glenda Johnson, Communications Manager ASACT President Martin J. Benison, comptroller of conferences_training/nasact/conferences/AnnualConferences/2013 NMassachusetts, recently welcomed members, corporate AnnualConference/materials.cfm. A complete list of the sessions partners and guests to Boston for NASACT’s ninety-eighth and speakers can be found on page 3. annual conference. The conference, which boasted the largest At lunch on Monday, President Benison announced the 2013 attendance in years (with over 460 registered attendees and Presidents Awards, which are given each year at the discretion guests), was held August 10-14 at the Seaport Hotel and World of the president to recognize service to the association and the Trade Center. Attendees were also welcomed during opening overall fi nancial management and accountability community. ceremonies by Massachusetts co-hosts Suzanne Bump, auditor of This year’s recipients were: the commonwealth; Steven Grossman, state treasurer; Massachusetts • Elaine M. Howle, state auditor of California, who was Governor Patrick Deval; and Boston Mayor Michael Menino (the recognized for her leadership as president of the National latter two through video messages). State Auditors Association in 2012-13 and also her efforts The conference began with a number of meetings and to revise NSAA’s Peer Review Manual, the policies and networking opportunities. On Saturday, August 10, some procedures governing NSAA’s Peer Review Program through attendees participated in the annual golf scramble, which which state audit organizations can receive an external was held at the Red Tail Golf Club. -

2020 Nasact Annual Conference

PROGRAM NASACT 2020 ANNUAL CONFERENCE August 24-28 | Virtual Training CONTINUING PROFESSIONAL EDUCATION Learning Objectives: Delivery Method: Group internet-based. All sessions include At the conclusion of the event, participants will be able to: Q&A opportunities. • Recount changes to the roles and responsibilities of state Attendance Requirements: In order to obtain CPE credit for auditors, state comptrollers and state treasurers as these this event, participants must submit attendance verification roles have evolved during the past year. codes provided during each session. • Identify and discuss new standards and rules from the government standards setting bodies and regulatory The National Association of State agencies. Auditors, Comptrollers and Treasurers is • Apply practical information learned through case studies registered with the National Association from peer offices and organizations. of State Boards of Accountancy (NASBA) • Discuss state government financial management as it as a sponsor of continuing professional relates to the broader, national fiscal outlook. education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance Level of Knowledge: Overview. of individual courses for CPE credit. Complaints regarding Education Prerequisite: No prerequisites required. registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: https://www. Advance Preparation: No advance preparation required. nasbaregistry.org/. CPE: 29.5 credits have been recommended for the conference. PRESIDENT’S MESSAGE Dear NASACT Members and Partners, It is my honor to welcome you to the 104th NASACT Annual Conference. I had hoped to welcome you to Vermont for this event, but the Covid-19 pandemic prevented that from happening. -

NASACT News, November 2014

KEEPING STATE FISCAL OFFICIALS INFORMED VOLUME 34, NUMBER 11 | NOVEMBER 2014 NASACT WEATHERS 2014 ELECTION SEASON With 48 member seats in question, the November worked on legislation that eventually became 2014 elections carried the potential for signifi cant Act 1088, which regulates the state’s treasury change within NASACT’s member ranks. management practices and procedures to ensure Elections results aff ecting member offi ces are prudent investment and management of public funds outlined below by state. Questions about this article entrusted to the state treasurer. Milligan will replace may be directed to Neal Hutchko, policy analyst, at Charles Robinson, who was named temporarily [email protected] or (202) 624-5451. in May 2013 to replace former treasurer Martha Shoff ner and was not eligible for re-election. ALABAMA CALIFORNIA Treasurer: Young Boozer, III (R), running unopposed, retained his seat. Th is will be his second Comptroller: Betty Yee (D) won her race to become term as state treasurer. the new state controller. She previously served as the chief deputy director for budget with the California ARIZONA Department of Finance. She earned her bachelor Treasurer: Jeff DeWit (R), who ran unopposed, is of arts degree in sociology from the University of Arizona’s new state treasurer. DeWit is an investment California, Berkeley, and her master’s degree in public professional and soft ware company owner with a administration from Golden Gate University, San degree from the University of Southern California Francisco. She replaces John Chiang, who was term in business administration and a minor in fi nance. limited. He will replace Doug Ducey, who ran a successful Treasurer: John Chiang (D) won the state treasurer campaign for governor. -

2020 Nasact Annual Conference

PROGRAM NASACT 2020 ANNUAL CONFERENCE August 24-28 | Virtual Training CONTINUING PROFESSIONAL EDUCATION Learning Objectives: Delivery Method: Group internet-based. All sessions include At the conclusion of the event, participants will be able to: Q&A opportunities. • Recount changes to the roles and responsibilities of state Attendance Requirements: In order to obtain CPE credit for auditors, state comptrollers and state treasurers as these this event, participants must submit attendance verification roles have evolved during the past year. codes provided during each session. • Identify and discuss new standards and rules from the government standards setting bodies and regulatory The National Association of State agencies. Auditors, Comptrollers and Treasurers is • Apply practical information learned through case studies registered with the National Association from peer offices and organizations. of State Boards of Accountancy (NASBA) • Discuss state government financial management as it as a sponsor of continuing professional relates to the broader, national fiscal outlook. education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance Level of Knowledge: Overview. of individual courses for CPE credit. Complaints regarding Education Prerequisite: No prerequisites required. registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: https://www. Advance Preparation: No advance preparation required. nasbaregistry.org/. CPE: 29.5 credits have been recommended for the conference. PRESIDENT’S MESSAGE Dear NASACT Members and Partners, It is my honor to welcome you to the 105th NASACT Annual Conference. I had hoped to welcome you to Vermont for this event, but the Covid-19 pandemic prevented that from happening. -

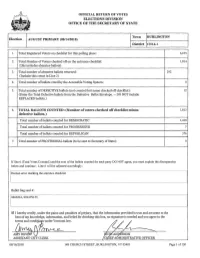

State Primary Official Return of Votes

OFFICIAL RETURN OF VOTES ELECTIONS DIVISION OFFICE OF THE SECRETARY OF STATE Town BURLINGTON Election AUGUST PRIMARY (08/14/2018) District CHI-6-1 1. Total Registered Voters on checklist for this polling place: 6,675 2. Total Number of Voters checked off on the entrance checklist: 1,814 (this includes absentee ballots) 3. Total number of absentee ballots returned: 292 (Include this count in Llne 2) 4. Total number of ballots voted by the Accessible Voting System: 0 5. Total number of DEFECTIVE ballots (not counted but name checked off checklist): 12 (Enter the Total Defective ballots from the Defective Ballot Envelope. -- DO NOT include REPLACED ballots.) 6. TOTAL BALLOTS COUNTED: (Number of voters checked off checklist minus 1,813 defective ballots.) Total number of ballots counted for DEMOCRATIC 1,430 Total number of ballots counted for PROGRESSIVE 7 Total number of ballots counted for REPUBLICAN 376 7. Total number of PROVISIONAL ballots (to be sent to Secretary of State): 0 If line 6 (Total Votes Counted.) and the sum of the ballots counted for each party DO NOT agree, you must explain the discrepancies below and continue - Line 6 will be adjusted accordingly: 'Human error marking the entrance checklist Ballot bag seal#: i02665 001279155 0 I hereby certify, under the pains and penalties of perjury, that the information provided is true and accurate to the best of my knowledge, information, and belief.By checking this box, no signature is needed and you agree to the ~n~r::_tlaw ~ AMY BOvEIY \.1 !c~~RSON ----- ASSISTANT CITI CLERK EF MINISTRATIVE OFFICER ' 08/16/2018 149 CHURCH STREET, BURLINGTON, VT 05401 Page I of 130 Town BURLINGTON Election AUGUST PRIMARY District CHI-6-1 NameonBaJJ.ot , Pflr.l:Y TownofResidence Vote Cast JAMES EHLERS DEMOCRATIC WINOOSKI 332 CHRISTINE HALLQUIST DEMOCRATIC HYDE PARK 564 BRENDA SIEGEL DEMOCRATIC NEWFANE 224 ETHAN SONNEBORN DEMOCRATIC BRISTOL 87 TOTAL WRITE IN COUNTS DEMOCRATIC 69 ALAN CHARRON (Write-in) DEMOCRATIC B. -

Annual Report 2017 Letter from the Director

Annual Report 2017 Letter from the Director “Vermont Fights Back” was on doors throughout the state. and corporate greed are being essentially our motto for 2017. They visited every community rolled back in Washington, I’m The year began with the largest and recruited members in every grateful for the opportunity to public rally in recent Vermont legislative district. press for state-based progress history (the Women’s March) right here. No, this work isn’t the on the steps of the State House, Our canvassers had tens of complete answer to the mess in one day after the presidential thousands of conversations, DC, but it can provide a model inauguration. and in each one they talked for the future that also benefits about how our shared values Vermonters right away. Ten months later, VPIRG co- were under attack by the Trump hosted the Crossroads Conference administration and Congress. We didn’t go looking for this fight, in Burlington – a gathering More importantly, they made clear but thanks for helping us be part of hundreds of Vermonters that VPIRG was fighting back. of it. committed to charting a path to progress on issues as diverse as One canvasser told me that she Paul Burns clean water, family leave, climate couldn’t imagine doing anything change and racial justice. more important during the summer of 2017. And I think that was a In between, we ran the largest common feeling among her peers. summer canvass campaign in VPIRG’s history. We had more I know that as protections against than 100 canvassers knocking climate change, toxic pollution Contact Phone 802-223-5221 Vermont Public Interest Fax 802-223-6855 Research Group Email [email protected] 141 Main Street, Suite 6 Montpelier VT 05602 Web www.vpirg.org Twitter @vpirg Facebook facebook.com/vpirg 2 ANNUAL REPORT 2017 In 2017, “Vermont Fights Back” became VPIRG’s animating theme. -

2018 Q3 Signalman's Journal

Volume 99 3RD QUARTER 2018 WIRELESS DISCOUNTS Welcome Home CREDIT CARDS Whether you are in the market to purchase a home or refinance an existing mortgage, Union Plus offers two mortgage providers FLOWERS designed to help union families. Every mortgage provides hardship & GIFTS assistance in case of disability, layoff, lockout, or strike. Find out more about this and other great Union Plus programs by CAR visiting unionplus.org. RENTAL Learn more at unionplus.org/mortgage Official Publication of the BROTHERHOOD OF RAILROAD SIGNALMEN WWW.BRS.ORG VOLUME 99 • 3RD Quarter 2018 DIRECTORY Canadian Pacific — Soo Line Railroad Company NATIONAL HEADQUARTERS: BRS Members Ratify Agreement 917 Shenandoah Shores Road Front Royal, VA 22630-6418 BRS Midwest Vice President Joe Mattingly and BRS CP/SOO Line General (540) 622-6522 Fax: (540) 622-6532 [email protected] Committee Chairman Keith Huebner negotiated the final terms of the new contract Floyd E. Mason, President that was signed on May 31, 2018, in Minneapolis, Minnesota .............................. 6 (ext. 525) • [email protected] Jerry Boles, Secretary-Treasurer (ext. 527) • [email protected] BRS Members Unite for Historic Signal Project Kelly Haley, Vice President Headquarters (ext. 524) • [email protected] Brotherhood of Railroad Signalmen (BRS) members unite to completely rebuild John Bragg, Vice President NRAB Canadian National Railway’s (CN) historic Homewood Interlocking Plant .......... 7 (ext. 524) • [email protected] Brandon Elvey, Director of Research (ext. 596) • [email protected] 52nd Regular BRS Convention Cory Claypool, Grand Lodge Representative (ext. 595) • [email protected] in Boston, Massachusetts Mike Efaw, Grand Lodge Representative (ext. 571) • [email protected] A summary of the minutes from the 52nd Regular Brotherhood of Railroad Signalmen Convention, WASHINGTON OFFICE: 815 16th Street NW, 4th Floor held the week of August 6, 2018, in Boston, Washington, D.C. -

NASACT News, November 2012

keeping stateNASACT fiscal officials informed news Volume 32, Number 11 November 2012 NASACT Responds to SEC Report on Municipal Securities Market Members Remain Opposed to Federal Intervention or SEC Authority Over State Fiscal Affairs his summer the U.S. Securities and Exchange Commission recommendations that it be given specifi c authority to establish Tissued a long-anticipated report looking at disclosure and the form and content of fi nancial statements and to designate a pricing practices in the municipal securities market. The report private sector body as the GAAP standard setter for municipal makes a series of legislative and regulatory recommendations issuer fi nancing: such actions represent a direct infringement to address concerns voiced by market participants during fi eld of states’ rights. Federal authority over the Governmental hearings, in comment letters, and in meetings and conference Accounting Standards Board would be a violation of federalism calls with the SEC. and NASACT would adamantly oppose any attempt by the The report contains legislative recommendations that are federal government or Congress to override or interfere with particulary concerning to NASACT’s members, as they would GASB’s independent standard setting. NASACT’s comments to give the SEC authority over municipal issuer disclosure, the SEC point out: including designating a state or local government’s accounting standards setter and controlling the form and content of an “Governments have an important responsibility to be issuer’s fi nancial statements. NASACT members do believe accountable to the taxpayers for the use of their resources. that voluntary initiatives can and do make improvements in Public accountability is a signifi cantly different objective the disclosure provided to municipal bond investors. -

2020 VT State Primary Election

OFFICIAL RETURN OF VOTES ELECTIONS DIVISION OFFICE OF THE SECRETARY OF STATE Town COLCHESTER Election PRIMARY ELECTION (08/11/2020) District CHI-9-1 1. Total Registered Voters on checklist for this polling place: 5,003 2. Total Number of Voters checked off on the entrance checklist: 1,744 (this includes absentee ballots) 3. Total number of absentee ballots returned: 1,296 (Include this count in Line 2) 4. Total number of ballots voted by the Accessible Voting System: 0 5. Total number of DEFECTIVE ballots (not counted but name checked off checklist): 96 (Enter the Total Defective ballots from the Defective Ballot Envelope. -- DO NOT include REPLACED ballots.) 6. TOTAL BALLOTS COUNTED: (Number of voters checked off checklist minus 1,649 defective ballots.) Total number of ballots counted for DEMOCRATIC 1,060 Total number of ballots counted for PROGRESSIVE 9 Total number of ballots counted for REPUBLICAN 580 7. Total number of PROVISIONAL ballots (to be sent to Secretary of State): 0 If line 6 (Total Votes Counted.) and the sum of the ballots counted for each party DO NOT agree, you must explain the discrepancies below and continue - Line 6 will be adjusted accordingly: CHECKLIST ERROR Ballot bag seal #: 0089106 0089104 þ I hereby certify, under the pains and penalties of perjury, that the information provided is true and accurate to the best of my knowledge, information, and belief.By checking this box, no signature is needed and you agree to the terms and conditions under Vermont law. JULIE A GRAETER WANDA FS MORIN TOWN CLERK & TREASURER -

Report to the Governor, the Vermont Legislature, and the Clean Water Board Where’S the Money Flowing? Cost- Effectiveness of Lake Champlain Clean Water Efforts

Vermont State Auditor Douglas R. Hoffer Report to the Governor, the Vermont Legislature, and the Clean Water Board Where’s the Money Flowing? Cost- Effectiveness of Lake Champlain Clean Water Efforts 7/15Date/2019 • Office• Office of ofthe the Vermont Vermont State State Auditor Auditor • Non • Non-Audit-Audit Report Report 15- 0819 -03 This is a non-audit report. A non-audit report is a tool used to inform citizens and management of issues that may need attention. It is not an audit and is not conducted under generally accepted government auditing standards. A non-audit report does not contain recommendations. Instead, the report includes information and possible risk-mitigation strategies relevant to an entity that is the object of the inquiry. Mission Statement The mission of the Vermont State Auditor’s Office is to hold government accountable. This means ensuring taxpayer funds are used effectively and efficiently, and that we foster the prevention of waste, fraud, and abuse. Principal Investigator Geoffrey A. Battista Non-Audit Inquiry This is a non-audit report. A non-audit report is a tool used to inform citizens and management of issues that may need attention. It is not an audit and is not conducted under generally accepted government auditing standards. A non-audit report has a substantially smaller scope of work than an audit. Therefore, its conclusions are more limited, and it does not contain recommendations. Instead, the report includes information and possible risk-mitigation strategies relevant to the entity that is the object of the inquiry. Table of Contents Executive Summary ........................................................................................................................ -

Making Economic Development Policy: Anecdotes Or Peer-Reviewed Literature

Vermont State Auditor Douglas R. Hoffer REPORT TO THE GOVERNOR AND THE GENERAL ASSEMBLY MAKING ECONOMIC DEVELOPMENT POLICY: ANECDOTES OR PEER-REVIEWED LITERATURE 9 JULY 2018 • OFFICE OF THE VERMONT STATE AUDITOR • NON-AUDIT REPORT 18-04 1/20/2015 • OFFICE OF THE VERMONT STATE AUDITOR • NON-AUDIT REPORT 15-01 1 Mission Statement The mission of the Vermont State Auditor’s Office is to hold government accountable. This means ensuring taxpayer funds are spent effectively and efficiently, and that we foster the prevention of waste, fraud, and abuse. Principal Investigator Christoph M. Demers Non-Audit Inquiry This is a non-audit report. A non-audit report is a tool used to inform citizens and management of issues that may need attention. It is not an audit and is not conducted under generally accepted government auditing standards. A non-audit report has a substantially smaller scope of work than an audit. Therefore, its conclusions are more limited, and it does not contain recommendations. Instead, the report includes information and possible risk-mitigation strategies relevant to the entity that is the object of the inquiry. 2 DOUGLAS R. HOFFER STATE AUDITOR STATE OF VERMONT OFFICE OF THE STATE AUDITOR Dear Colleagues Part of the State Auditor’s mission is to conduct performance audits and provide management and legislators with information useful for strategic planning and policymaking. There are some policy areas, however, that present challenges. For example, there is little reliable performance data about some of the State’s largest economic development programs, which makes it difficult to conduct performance audits.1 Here are some examples of programs with performance auditing challenges.