Annual Report and Accounts 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Transport with So Many Ways to Get to and Around London, Doing Business Here Has Never Been Easier

Transport With so many ways to get to and around London, doing business here has never been easier First Capital Connect runs up to four trains an hour to Blackfriars/London Bridge. Fares from £8.90 single; journey time 35 mins. firstcapitalconnect.co.uk To London by coach There is an hourly coach service to Victoria Coach Station run by National Express Airport. Fares from £7.30 single; journey time 1 hour 20 mins. nationalexpress.com London Heathrow Airport T: +44 (0)844 335 1801 baa.com To London by Tube The Piccadilly line connects all five terminals with central London. Fares from £4 single (from £2.20 with an Oyster card); journey time about an hour. tfl.gov.uk/tube To London by rail The Heathrow Express runs four non- Greater London & airport locations stop trains an hour to and from London Paddington station. Fares from £16.50 single; journey time 15-20 mins. Transport for London (TfL) Travelcards are not valid This section details the various types Getting here on this service. of transport available in London, providing heathrowexpress.com information on how to get to the city On arrival from the airports, and how to get around Heathrow Connect runs between once in town. There are also listings for London City Airport Heathrow and Paddington via five stations transport companies, whether travelling T: +44 (0)20 7646 0088 in west London. Fares from £7.40 single. by road, rail, river, or even by bike or on londoncityairport.com Trains run every 30 mins; journey time foot. See the Transport & Sightseeing around 25 mins. -

Airport Transfers

IRELAND & SCOTLAND 2009/10 www.BrendanVacations.com 15th-century Ross Castle overlooks the Lower Lake in Killarney 2 | www.BrendanVacations.com Welcome Dear Traveler, Taking a vacation to Ireland and Britain is exciting! Wouldn’t it be great if you knew someone who has personally been there to guide you though the experience? For over 40 years, Brendan has been helping travelers plan, book and enjoy their special vacation. Whether it’s on your own, with a guide and a group of like-minded travelers, or a combination of the two, we will help you make it the vacation of your dreams. It starts with your reservation. One of our experts will personally handle all the details, make sure you have the information you need, share ‘insider’ destination secrets and answer your questions. When it comes to Ireland and Britain, my father and I know this part of the world intimately (some would say, better than anybody). My father grew up in Dublin, and I have visited many times, plus we’ve both been to England, Scotland, Northern Ireland and Wales on numerous occasions. We have explored it all, from the famous ‘must see’ sights to little out-of-the-way local favorites. When we design our tours, we do so with the same care and thought that we use for our own personal vacations. Britain and, especially, Ireland hold a very special place in our hearts, and we look forward to sharing them with you. “Taking You Personally” is more than our slogan. It’s the way we want to be treated….so it is the way we want to treat you and every Brendan traveler. -

View Annual Report

National Express Group PLC Group National Express National Express Group PLC Annual Report and Accounts 2007 Annual Report and Accounts 2007 Making travel simpler... National Express Group PLC 7 Triton Square London NW1 3HG Tel: +44 (0) 8450 130130 Fax: +44 (0) 20 7506 4320 e-mail: [email protected] www.nationalexpressgroup.com 117 National Express Group PLC Annual Report & Accounts 2007 Glossary AGM Annual General Meeting Combined Code The Combined Code on Corporate Governance published by the Financial Reporting Council ...by CPI Consumer Price Index CR Corporate Responsibility The Company National Express Group PLC DfT Department for Transport working DNA The name for our leadership development strategy EBT Employee Benefit Trust EBITDA Normalised operating profit before depreciation and other non-cash items excluding discontinued operations as one EPS Earnings Per Share – The profit for the year attributable to shareholders, divided by the weighted average number of shares in issue, excluding those held by the Employee Benefit Trust and shares held in treasury which are treated as cancelled. EU European Union The Group The Company and its subsidiaries IFRIC International Financial Reporting Interpretations Committee IFRS International Financial Reporting Standards KPI Key Performance Indicator LTIP Long Term Incentive Plan NXEA National Express East Anglia NXEC National Express East Coast Normalised diluted earnings Earnings per share and excluding the profit or loss on sale of businesses, exceptional profit or loss on the -

Mining User Reviews of COVID Contact-Tracing Apps:An Exploratory

Mining user reviews of COVID contact-tracing apps: An exploratory analysis of nine European apps Vahid Garousi David Cutting Michael Felderer Queen’s University Belfast, UK Queen’s University Belfast, UK University of Innsbruck, Austria Bahar Software Engineering Consulting [email protected] Blekinge Institute of Technology, Sweden Corporation, UK [email protected] [email protected] Abstract: Context: More than 50 countries have developed COVID contact-tracing apps to limit the spread of coronavirus. However, many experts and scientists cast doubt on the effectiveness of those apps. For each app, a large number of reviews have been entered by end-users in app stores. Objective: Our goal is to gain insights into the user reviews of those apps, and to find out the main problems that users have reported. Our focus is to assess the "software in society" aspects of the apps, based on user reviews. Method: We selected nine European national apps for our analysis and used a commercial app-review analytics tool to extract and mine the user reviews. For all the apps combined, our dataset includes 39,425 user reviews. Results: Results show that users are generally dissatisfied with the nine apps under study, except the Scottish ("Protect Scotland") app. Some of the major issues that users have complained about are high battery drainage and doubts on whether apps are really working. Conclusion: Our results show that more work is needed by the stakeholders behind the apps (e.g., app developers, decision-makers, public health experts) to improve the public adoption, software quality and public perception of these apps. -

Bus & Motorcoach News

November 15, 2007 WHAT’S GOING ON IN THE BUS INDUSTRY Federal officials want industry to plan for pandemic WASHINGTON — Federal possibility of a prolonged and dev- significant risk to the United States If a severe pandemic were to hit of the economy is potentially sig- homeland security officials, plan- astating pandemic event may find and the world. the U.S., given today’s highly mo- nificant, officials contend. ning for a possible catastrophic themselves without the staff, equip- “Only its timing, severity and bile population, outbreaks could “Any disruption to these key pandemic that could slow the na- ment or supplies necessary to con- exact strain remain uncertain. Inter- occur almost simultaneously through- highway transportation services tion’s economy to a crawl, includ- tinue serving their customers or to national, federal, state, local and out the country, according to the and infrastructure may cause sig- ing the entire transportation sector, provide emergency assistance, fed- tribal government agencies are dili- U.S. Department of Homeland nificant local, regional and even have put together a series of guide- eral officials warn. gently planning for the public Security. national challenges potentially put- lines for the motorcoach and truck- President Bush has urged pri- health response to this potential Whether transporting passen- ting delivery of critical food, fuel ing industries. vate-sector companies to act, not- pandemic,” says Bush, urging pri- gers by bus, taxi or transit vehicles, and medical supplies, as well as Passenger transportation com- ing that “public health experts warn vate companies to also plan for or transporting goods by truck, the emergency response equipment, panies that fail to prepare for the that pandemic influenza poses a such a disaster. -

2003-Fall.Pdf

BOWDOINBOWDOINFall 2003 Volume 75, Number 1 JourneyJourney CzarsCzarsofof thethe Join CBB alumni on their tour of discovery from Moscow to St. Petersburg contents fall2003 Journey of the Czars 16 Text and photographs by Alicia MacLeay In our second joint article about one of our CBB programs, Colby magazine writer Alicia MacLeay describes an alumni trip to Russia with Bowdoin, Bates, and Colby grads. Led by Director of the Bowdoin Chorus Anthony Antolini ’63 and Sheila McCarthy, associate professor of Russian literature and language at Colby, the group travels through the canals, rivers and lakes of Russia and witnesses a country in transition. The Nose Knows 24 By Douglas MacInnis Photographs by Seth Affoumado Michael Broffman ’75 is sure that dogs can ascertain the presence of cancer cells more finely with their noses than is possible using the most sophisticated cancer-detection equipment available today. A nationally-known expert in Chinese medicine, Broffman has just finished a clinical trial of the dogs’ ability, and the evidence seems compelling. Family Ties 30 By David Treadwell ’64 Photographs by Tom McPherson In some families, Bowdoin Beata is more than a fond phrase, it’s the family crest. David Treadwell takes us back through the roots of some formidable family trees. Departments Mailbox 2 Bookshelf 4 College & Maine 5 Weddings 36 Class News 39 Obituaries 79 Interview 88 BOWDOINeditor’s note staff Volume 75, Number 1 Fall, 2003 MAGAZINE STAFF ditors think a fair amount about what it is that makes a story inter- Editor esting. (Or, at least, they do that once, and then afterward they just Alison M. -

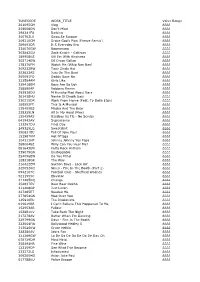

TUNECODE WORK TITLE Value Range 261095CM

TUNECODE WORK_TITLE Value Range 261095CM Vlog ££££ 259008DN Don't Mind ££££ 298241FU Barking ££££ 300703LV Swag Se Swagat ££££ 309210CM Drake God's Plan (Freeze Remix) ££££ 289693DR It S Everyday Bro ££££ 234070GW Boomerang ££££ 302842GU Zack Knight - Galtiyan ££££ 189958KS Kill Em With Kindness ££££ 302714EW Dil Diyan Gallan ££££ 178176FM Watch Me (Whip Nae Nae) ££££ 309232BW Tiger Zinda Hai ££££ 253823AS Juju On The Beat ££££ 265091FQ Daddy Says No ££££ 232584AM Girls Like ££££ 329418BM Boys Are So Ugh ££££ 258890AP Robbery Remix ££££ 292938DU M Huncho Mad About Bars ££££ 261438HU Nashe Si Chadh Gayi ££££ 230215DR Work From Home (Feat. Ty Dolla $Ign) ££££ 188552FT This Is A Musical ££££ 135455BS Masha And The Bear ££££ 238329LN All In My Head (Flex) ££££ 155459AS Bassboy Vs Tlc - No Scrubs ££££ 041942AV Supernanny ££££ 133267DU Final Day ££££ 249325LQ Sweatshirt ££££ 290631EU Fall Of Jake Paul ££££ 153987KM Hot N*Gga ££££ 304111HP Johnny Johnny Yes Papa ££££ 2680048Z Willy Can You Hear Me? ££££ 081643EN Party Rock Anthem ££££ 239079GN Unstoppable ££££ 254096EW Do You Mind ££££ 128318GR The Way ££££ 216422EM Section Boyz - Lock Arf ££££ 325052KQ Nines - Fire In The Booth (Part 2) ££££ 0942107C Football Club - Sheffield Wednes ££££ 5211555C Elevator ££££ 311205DQ Change ££££ 254637EV Baar Baar Dekho ££££ 311408GP Just Listen ££££ 227485ET Needed Me ££££ 277854GN Mad Over You ££££ 125910EU The Illusionists ££££ 019619BR I Can't Believe This Happened To Me ££££ 152953AR Fallout ££££ 153881KV Take Back The Night ££££ 217278AV Better When -

Press Release

Press release Thursday 26 February 2009 National Express Group PLC Full Year Results for the year ended 31 December 2008 National Express Group PLC, a leading international public transport group, operates bus, coach and rail services in the UK, bus and coach operations in Spain and school bus services in North America. Headlines In 2008 we delivered strong revenue and profit growth, despite an increasingly challenging economic environment as the year progressed. Total Group revenue grew 5.9% to almost £2.8 billion. We increased normalised* profit before tax by 9.7% to £194.1 million. 2009 will present significant challenges; however, we have robust plans to manage these. Financial Results • Continuing revenue up 5.9% to £2,767.0 million (2007: £2,612.3m) • Normalised operating margin improved to 9.2% (2007: 8.1%), excluding discontinued operations • Normalised profit before tax up 9.7% to £194.1 million (2007: £177.0m) • Normalised diluted earnings per share up 11.6% to 93.6 pence (2007: 83.9p) • Profit for the year £119.7 million (2007: £105.6m) • Operating cash flow** £152.3 million (2007: £200.9m) • Total dividend per share for the year 22.72 pence (2007: 37.96p) Operational Performance • Strong performance in delivery of Rail franchises in 2008, including meeting all first year commitments for East Coast • Robust growth in UK bus and coach, with enhanced efficiencies and cost savings from integration • Excellent customer retention in North America bus, supported by $38 million new contracts; steady progress in Business Transformation -

Dorchester Reporter “The News and Values Around the Neighborhood”

Dorchester Reporter “The News and Values Around the Neighborhood” Volume 29 Issue 31 Thursday, August 2, 2012 50¢ Patrick will sign ‘balanced’ bill on sentencing reform By GintautaS DuMciuS Sometimes known as the “three nEwS EDitor strikes” bill, the legislation eliminates A day after Beacon Hill lawmakers parole for some habitual violent rejected Gov. Deval Patrick’s attempt felons, eases some sentences for drug to add judicial discretion to the crime offenders, and reduces the so-called bill, Patrick said he will sign the “school zone” deployed by prosecutors controversial legislation, which its to enhance sentences to 300 feet from supporters say will crack down on 1,000 feet. the state’s most violent criminals. Patrick said preliminary estimates Opponents contend the bill dispropor- peg at almost 600 the number of non- tionately affects minorities. violent drug offenders who would be “I asked for a balanced bill and, after eligible for supervised parole as soon many twists and turns, the Legislature as the law goes into effect. has given me one,” Patrick said in The House and Senate on Monday a statement on Tuesday afternoon. rejected an amendment Patrick offered “Because of the balance between strict that he said would improve the bill by sentences for the worst offenders and providing judges with the discretion more common sense approaches for to grant parole to habitual offenders. those who pose little threat to public The House – whose speaker, Robert safety, I have said that this is a good bill. I will sign this bill.” (Continued on page 17) Summer recipe for tots: Tennis, dash of nutrition By ElizaBEth Murray SpEcial to thE rEportEr About a dozen fourth graders filed anxiously into the room used as both The right thing to do: A Crystal Transport bus turns to enter the UMass Boston a gym and cafeteria last Wednesday campus while another driver heads south down Morrissey Boulevard. -

Report on Public Transport Provision in Rural and Depopulated Areas in the United Kingdom

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics White, Peter Working Paper Report on public transport provision in rural and depopulated areas in the United Kingdom International Transport Forum Discussion Paper, No. 2015-07 Provided in Cooperation with: International Transport Forum (ITF), OECD Suggested Citation: White, Peter (2015) : Report on public transport provision in rural and depopulated areas in the United Kingdom, International Transport Forum Discussion Paper, No. 2015-07, Organisation for Economic Co-operation and Development (OECD), International Transport Forum, Paris This Version is available at: http://hdl.handle.net/10419/109194 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available -

By Parcel Firm

18.11.2016 NOT READY FOR CONTACTLESS? Your younger customers may start shopping elsewhere RN INTERVIEW Page 22 » Tobacco watch ‘Some customers still don’t believe 10-packs are going’ Page 24 » NEWS ● CONVENIENCE ● PROFIT www.betterretailing.com ● £2.30 GALA DINNER 2016 “The Gala Dinner helps us learn new ideas from other retailers and meet suppliers with fantastic insight on what our shoppers want.” JULIAN & JACKIE TAYLOR-GREEN TAYLOR-GREEN SPAR, LINDFORD IAA 2016 AMBASSADORS We challenge you not to be inspired! Be there: 1 December, East Wintergarden, London [email protected] #IAA16 Julian & Jackie - RN full page SIGNED OFF Folder.indd 1 15/11/2016 11:54 18.11.2016 NOT READY FOR CONTACTLESS? Your younger customers may start shopping elsewhere RN INTERVIEW Page 22 » Tobacco watch ‘Some customers still don’t believe 10-packs are going’ Page 24 » NEWS ● CONVENIENCE ● PROFIT www.betterretailing.com ● £2.30 Specialise to make e-cigs INNOVATION Delivery top earner robots to New franchise and gantry solutions will earn hit UK retailers more per square metre than any other next year Just Eat first to trial category, says NFRN Commercial. Page 5 » technology, able to deliver in just 15 minutes. Page 4 » SYMBOLS Simplified Nisa terms to support members ‘We’ll make Nisa easier to do business with,’ retailers told following conference. Page 6 » HND retailer AHEAD OF THE CURVE creates magazine “We’ve had a deli and coffee offer since 2000. But 16 years on, it’s subscription ofer to listening to our customers that’s helped grow our sales year on year.” stop customers going direct to publishers. -

Mid Anglia Rail Passengers Association Newsletter

MARPA Newsletter Mid Anglia Rail Passengers Association (MARPA) Published by MARPA Edited by Peter Rutt Tel: 01359 242464 e-mail: [email protected] Autumn / Winter 2008 Newsletter Welcome to the autumn 2008 MARPA newsletter. It has been a long summer off school for my son after taking his GCSEs. He is a keen birdwatcher so to get him out of the house I looked at the Traveline East Anglia website to try to plan a journey to a bird reserve using public transport. As the Suffolk coast is nearest we looked at the Minsmere/Dunwich area but this was a 4 hour journey involving 2 or 3 buses from Ipswich and the nearest he could get was Westleton or Leiston. I know you can book a Coastlink bus, but this involves a degree of pre-planning (two days notice) that teenagers can’t always do. Frustrated at getting on public transport to the wilder parts of the Suffolk coast we looked at North Norfolk. Cley Marshes can be reached by train from Stowmarket to Norwich, Norwich to Sheringham, then the frequent Coasthopper bus to the door of the reserve visitor centre. This takes under two and a half hours and costs a 16 year old with a Suffolk County Council ‘Explore’ card an incredibly good £8.50 for the return trip. Visiting nature reserves from our area can be done, for example RSPB Lakenheath is in easy walking distance of the station, and RSPB Titchwell is on the Coasthopper bus route from Sheringham or Kings Lynn. I travelled up to London last week, the train was clean, on time, staff courteous, at seat trolley service both ways – in fact pretty much a faultless journey.