Principal Exchange-Traded Funds Form N-CSR Filed 2020-08-27

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Architecture of Downtown Des Moines: Some Highlights from the Twentieth Century and Beyond

Paula Mohr is an architectural historian and directs the certified local government program in Iowa. She is a graduate of the Cooperstown Museum Studies program and the architectural history program at the University of Virginia. Paula is the local co-chair for FORUM 2018. Architecture of Downtown Des Moines: Some Highlights from the Twentieth Century and Beyond By Paula Mohr In its 170-some years, the evolution of Des Moines’ commercial core has paral- leled that of many American cities. Fort Des Moines, an early foothold in terms of Euro-American settlement, today survives only as an archaeological site. Early commercial buildings of wood frame on both the east and west sides of the Des Moines River were replaced with brick later in the nineteenth century. At the turn of the twentieth century another wave of development introduced tall buildings or skyscrapers. In the midst of all this change, we can see the impact of external forces, including architectural ideas from Chicago, the City Beautiful Movement and the contributions of nationally and internationally renowned architects. The “book” on Des Moines’ architecture is still being written. As a result of this constant renewal and rebuild- Youngerman Block (1876), also by Foster, features ing, only a handful of nineteenth century buildings a façade of “Abestine Stone,” a nineteenth-century survive in Des Moines’ downtown. In the Court artificial stone manufactured by the building’s Avenue entertainment area across the river from owner, Conrad Youngerman. The five-story Des the FORUM conference hotel are several notable Moines Saddlery Building (c. 1878), just around examples. -

Property and Casualty Guaranty Associations

Property and Casualty Guaranty Associations Jurisdiction Address Phone FaxNumber Alaska Alaska Insurance Guaranty Association 907-338-7484 907-338-6364 Northern Adjusters, Inc 1401 Rudakof Circle Anchorage, AK 99508 Alabama Alabama Insurance Guaranty Association 205-823-4042 205-979-3578 2020 Canyon Road, Suite 200 Birmingham, AL 35216 Arkansas Arkansas Dept of Ins. Liquidation Division 501-371-2776 501-371-2774 1023 West Capitol Avenue,Suite 2 Little Rock, AR 72201 Arizona Arizona Insurance Guaranty Funds 602-364-3863 602-364-3872 Non-Comp 1110 West Washington Street, Suite 270 Phoenix, AZ 85007 Arizona SCF of Arizona 520-292-4000 520-292-4049 Comp Wetmore Road, Suite 110 Tucson, AZ 85719 California California Insurance Guarantee Association 818-844-4300 323-782-1489 P.O. Box 29066 Glendale, CA 91209 Colorado Western Guaranty Fund Services 303-759-5066 303-759-5312 1720 South Bellaire Street, Suite 408 Denver, CO 80222 Connecticut Guaranty Fund Management Services 617-227-7020 Comp Fax 617-305-0126 One Bowdoin Square P&L Fax 617-305-0128 Boston, MA 02114-2916 Delaware Delaware Insurance Guaranty Association 302-456-3656 302-456-3680 220 Continental Drive, Suite 309 Newark, DE 19713 District of Columbia Guaranty Fund Management Services 617-227-7020 Comp Fax 617-305-0126 One Bowdoin Square P&L Fax 617-305-0128 Boston, MA 02114-2916 Property and Casualty Guaranty Associations Florida Florida Insurance Guaranty Association 904-398-1238 904-398-6871 Non-Comp 10151 Deerwood Park Boulevard, Building 100 Suite 400 Jacksonville, FL 32256 Florida Unisource Administrators 888-457-1400 941-342-6939 Comp Attn: LuAnne Foss-Versteeg 5951 Cattleridge Boulevard, Suite 200 Sarasota, FL 34232-6052 Georgia Georgia Insurers Insolvency Pool 770-621-9835 770-938-3296 2177 Flintstone Dr., Suite R Tucker, GA 30084 Hawaii Hawaii Insurance Guaranty Association 808-528-1222 808-532-1495 P.O. -

2O2o Annual Report

COMMUNITY & COMMITMENT 2O2O ANNUAL REPORT DEAR DOWNTOWN STAKEHOLDER It is with deep pride and steadfast commitment that we share with you the 2020 Annual Report for the Downtown Center Business Improvement District (DCBID). Looking back at the most difficult year in our District’s history, we can say with renewed confidence that our organization, and our community, is resilient, resourceful, and built to last. While Downtown Los Angeles (DTLA), like cities across the globe, faced unprecedented circumstances due to the impacts of COVID-19, the core services that the DCBID has provided to its property owners since its inception in 1998 helped keep the District safe, clean, and viable throughout the year, and helped position us for recovery and revitalization as the pandemic begins to recede. Deemed essential workers at the start of the shutdown, our Safe and Clean Teams maintained its commitment to the highest standards of hygiene, sanitation, and safety across the District, 24/7, through months of extremely challenging conditions. In 2020, they responded to over 24,563 calls for service, and removed over 69,766 bags of trash and over 18,108 instances of graffiti. Working with our Homeless Outreach teams, our Safe and Clean teams continued their tireless efforts without interruption, proving just how essential they truly are. Nurturing a sense of community in the District is a key element of our mission and was never more critical than during this crisis. In the distinct absence of office workers and visitors, the District’s residential community filled the void, showing its strength and commitment by supporting local businesses, helping clean-up efforts following demonstrations and celebrations, and just keeping the lights on during a very dark period. -

Securities Offerings

SECURITIES OFFERINGS STATE NOTICES Gamma Lending Opportunities LP 101 Park Ave., Suite 2602, New York, NY 10178 Published pursuant to provisions of General Business Law Partnership — GRE Lending Opportunities LLC [Art. 23-A, § 359-e(2)] Gelesis, Inc. DEALERS; BROKERS 501 Boylston St., Suite 6102, Boston, MA 02116 State or country in which incorporated — Delaware 3118 W Lake REIT, LLC IFM Fintech Opportunities LP 801 Grand Ave., Des Moines, IA 50309 c/o IFM Fintech Opportunities GP Limited, One London Wall, 6th Fl., London EC2Y 5EB United Kingdom Ailanthus Capital Partners (QP), LP Partnership — IFM Fintech Opportunities GP Limited 61 Broadway, Suite 2825, New York, NY 10006 Partnership — Ailanthus Capital, LLC M-Line Tower REIT, LLC Ajax Fund, L.P. 801 Grand Ave., Des Moines, IA 50309 80 Hamilton Ave., Suite 101, Trenton, NJ 08611 Partnership — Ajax Capital Management, LLC Macritchie Storage Fund I, LP c/o Macritchie Storage LLC, 435 4th Ave. SW, Suite 725, Calgary, American Independence Funds Trust Alberta T2P 3A8 1345 Avenue of the Americas, 2nd Fl., New York, NY 10105 Partnership — Macritchie Storage LLC State or country in which incorporated — Delaware Metro East Valley REIT, LLC BBR Absolute Return Long Duration, LP 801 Grand Ave., Des Moines, IA 50309 140 E. 45th St., 26th Fl., New York, NY 10017 Partnership — BBR General Partner, LLC Nevada Sunrise Gold Corporation Suite 1100-1111 Melville St., Vancouver, British Columbia, Canada Bodri Capital Management, LLC V6E 3V6 290 Lowell Ave., Palo Alto, CA 94301 State or country in which incorporated — California State or country in which incorporated — Canada Cello Fixed Income Domestic Fund, LP OncoCyte Corporation 12 E. -

Awards List New Design.Indd

Awards GRUMMAN/BUTKUS ASSOCIATES | www.grummanbutkus.com | Energy Efficiency Consultants and Sustainable Design Engineers 2019 ASHRAE – Society Technology Award First Place - 801 Grand, Des Moines, IA, Assessment, Modeling, and Improvements ASHRAE – Region VI Technology Award First Place - Zoetis, Kalamazoo, MI, Chiller Expansion Project First Place - University of Illinois at Urbana-Champaign, Frederick Seitz Materials Research Laboratory Renovation Building Commissioning Association – Building Award Northwestern University, Ryan Fieldhouse and Walter Athletics Center, Evanston, IL (New Construction) University of Chicago Medicine, Advanced Therapeutics cGMP Facility, Chicago, IL (Major Renovation) U.S. Dept. of Energy, Lawrence Berkeley National Laboratory, Smart Energy Analytics Campaign Recognition Universal Health Services (UHS) (New Installation of a Fault Detection and Diagnostics System, Healthcare Category) 2018 ASHRAE – Illinois Chapter Excellence in Engineering Award Zoetis, Kalamazoo, MI, Chiller Expansion Project University of Illinois at Urbana-Champaign, Frederick Seitz Materials Research Laboratory Renovation ASHRAE – Region VI Technology Award First Place - 801 Grand, Des Moines, IA, Assessment, Modeling, and Improvements Honorable Mention - Advocate Healthcare – Six Hospitals, IL, Boiler Plant Optimization ENR Midwest magazine, 2018 Best Projects, Project of the Year and Best Project - Sports, Northwestern University Ryan Fieldhouse and Walter Athletics Center, Evanston, IL (Commissioning) 2017 ASHRAE – Illinois Chapter -

Principal Global Investors, LLC Form ADV Part 2A

Principal Global Investors, LLC Form ADV Part 2A 801 Grand Ave Des Moines, IA 50309 Phone: 800-533-1390 www.principalglobal.com March 30, 2021 This brochure provides information about the qualifications and business practices of Principal Global Investors, LLC (“PGI”). If you have any questions about the contents of this brochure, please contact us at 800-533-1390. The information in this brochure has not been approved or verified by the United States Securities and Exchange Commission (“SEC”) or by any state securities authority. Additional information about PGI also is available on the SEC's website at www.adviserinfo.sec.gov. PGI is an SEC registered investment adviser. This registration does not imply any certain level of skill or training. 1 Item 2: Material Changes Summary The PGI Advisory Brochure (Part 2A of Form ADV) (the “Brochure”) dated March 30, 2021 is our annual updating amendment to the prior Brochure dated December 11, 2020. There have been no material changes since the last amendment dated December 11, 2020. 2 Item 3 – Table of Contents Item 1 – Cover Page............................................................................................................ 1 Item 2 – Material Changes.................................................................................................. 2 Item 3 – Table of Contents...................................................................................................3 Item 4—Advisory Business ................................................................................................4 -

801 Grand Ave Des Moines, Iowa 50309 (800) 533-1390

FORM ADV Part 2B Principal Global Investors, LLC 801 Grand Ave Des Moines, Iowa 50309 (800) 533-1390 www.PrincipalGlobal.com March 29, 2018 Supervised Persons Principal Global Fixed Income (David Blake) General Account (Scott Bennett) Securitized Products & Rates (Bryan Davis, Zach Gassmann, Erika Isley, Ryan McCann) High Yield (Mark Denkinger, Darrin Smith, Josh Rank) Municipal (James Welch, James Noble) U.S. Multi-Strategy (Timothy Warrick, William Armstrong, Christina Paris, John Friedl, Scott Peterson) Investment Grade (Timothy Warrick, Randy Woodbury, Craig Dawson, Brad Stoermer) Emerging Markets Debt (Darryl Trunnel, Nicholas Varcoe) Global Strategies (Heath Sollars, Bill Armstrong, Darryl Trunnel, Tim Warrick, Randy Woodbury, Binay Chandgothia, Raj Singh) Cash & Short Term Management (Allison Hitchings, Tracy Reeg, Tim Warrick, Christina Paris, Scott Peterson) Currency (Mark Farrington) This brochure supplement provides information about the “Supervised Persons” of Principal Global Fixed Income and Currency that supplements the Principal Global Investors, LLC brochure. Principal Global Fixed Income and Currency are specialized investment groups within Principal Global Investors, LLC. You should have received a copy of that brochure. Please contact us at (800) 533-1390 if you did not receive the brochure or if you have any questions about the contents of this supplement. David Blake Principal Global Investors, LLC 801 Grand Ave., Des Moines, Iowa 50309 (800) 533-1390 / www.PrincipalGlobal.com Fixed Income This brochure supplement provides information about David Blake, a “supervised person” of Principal Global Investors Fixed Income team and supplements the Principal Global Investors, LLC brochure. You should have received a copy of that brochure. Please contact us using the information above if you did not receive the brochure or if you have any questions about the contents of this supplement. -

AUTM 2018 Central Region Meeting Pre-Registration List As of July 02

AUTM 2018 Central Region Meeting Attendance List July 9 - July 11, 2018 Minneapolis, MN Pre-Registration List as of July 02, 2018 Megan Aanstoos Kevin Anderson Melissa Baines Ohio State University Technology Marketing Manager Licensing Associate 3531 Brewton Dr University of Minnesota University of Cincinnati Westerville, OH 43081-9638 OTC - McNamara Alumni Center 51 Goodman Dr., Ste. 240 United States 2000 Oak St SE Ste 280 Cincinnati, OH 45221-0829 Minneapolis, MN 55455 United States William Adolfsen United States (513) 558-5274 Patent Attorney (612) 624-8293 Andrus Intellectual Property Law LLP (612) 624-6554 Greg Baker 100 East Wisconsin Avenue Director, Innovation and Tech Suite 1100 Gabe Angieri Commercialization Milwaukee, WI 53202 Director Of Development Children's National Health System United States ARCH GRANTS 111 Michigan Ave NW (608) 244-7635 911 Washington Avenue Washington, DC 20010-2916 St. Louis, MO 63101 United States Robert Alderson United States Senior Partner (314) 397-3782 Peter Ball Jacobacci & Partners S.p.A. Sr Licensing Manager Corso Emilia, 8 Benjamin Armitage Mayo Clinic Torino, 10152 Shareholder 200 First St SW Italy Billion & Armitage Rochester, MN 55905 +39-011-2440311 7401 Metro Blvd United States +39-011-286300 Suite 425 (507) 293-7378 Minneapolis, MN 55439 Esther Allay United States Nikhil Bansal Senior Licensing Associate (952) 697-2632 Account Executive St Jude Children's Research Hospital (952) 697-2631 Wellspring 262 DannyThomas Place 350 North LaSalle St Memphis, TN 38105 William Aylor Ste 1200 United States Director Chicago, IL 60654 (901) 595-4700 South Dakota State University United States (901) 595-3148 Box 2201 Administration Building 200 Kevin Barquinero Lawrence E. -

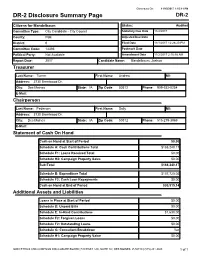

DR-2 Disclosure Summary Page DR-2

Generated On: 11/13/2017 1:15:11 PM DR-2 Disclosure Summary Page DR-2 Citizens for Mandelbaum Status: Audited Committee Type: City Candidate - City Council Statutory Due Date 11/2/2017 County: Polk Adjusted Due Date District: 0 Filed Date 11/1/2017 12:28:20 PM Committee Code: 14393 Postmark Date Political Party: Not Available Amendment Date 11/2/2017 2:16:18 AM Report Date: 2017 Candidate Name: Mandelbaum, Joshua Treasurer Last Name: Turner First Name: Andrew MI: Address: 3730 Brentwood Dr. City: Des Moines State: IA Zip Code: 50312 Phone: 909-532-0254 E-Mail: Chairperson Last Name: Pederson First Name: Sally MI: Address: 3730 Brentwood Dr. City: Des Moines State: IA Zip Code: 50312 Phone: 515-279-3969 E-Mail: Statement of Cash On Hand Cash on Hand at Start of Period $0.00 Schedule A: Cash Contributions Total $188,240.17 Schedule F1: Loans Received Total $0.00 Schedule H2: Campaign Property Sales $0.00 Sub-Total $188,240.17 Schedule B: Expenditure Total $157,725.03 Schedule F2: Cash Loan Repayments $0.00 Cash on Hand at End of Period $30,515.14 Additional Assets and Liabilities Loans in Place at Start of Period $0.00 Schedule D: Unpaid Bills $0.00 Schedule E: In-Kind Contributions $1,630.00 Schedule F2: Forgiven Loans $0.00 Schedule F2: Outstanding Loans $0.00 Schedule G: Consultant Breakdown Yes Schedule H1: Campaign Property Value $0.00 IOWA ETHICS AND CAMPAIGN DISCLOSURE BOARD | 510 EAST 12th, SUITE 1A | DES MOINES, IA 50319 | (515) 281-4028 1 of 1 Generated On: 11/13/2017 1:15:12 PM Schedule A: Contributions Sch-A Citizens for Mandelbaum -

United States District Court District of Minnesota

CASE 0:08-cv-03414-JRT-JSM Document 439 Filed 03/11/13 Page 1 of 5 UNITED STATES DISTRICT COURT DISTRICT OF MINNESOTA ROCKLAND BURKS and ADRIENNE Civil No. 08-3414 (JRT/JSM) LAWRENCE, individually, and as parents and natural guardians of E.B., Plaintiffs, ORDER v. ABBOTT LABORATORIES and MEAD JOHNSON & CO., Defendants. Stephen C. Rathke, Kate G. Westad, Nicholas A. Dolejsi, and Robert J. King, Jr., LOMMEN, ABDO, COLE, KING & STAGEBERG, PA, 80 South Eighth Street, Suite 2000, Minneapolis, MN 55402; Richard H. Taylor and W. Lloyd Copeland, TAYLOR MARTINO, 51 Saint Joseph Street, Mobile, AL 36601; Kara Hadican Samuels, SANGISETTY & SAMUELS, LLC, 610 Baronne Street, Third Floor, New Orleans, LA 70113, for plaintiffs. June K. Ghezzi, Melissa B. Hirst, Kelly M. Marino, and Paula S. Quist, JONES DAY, 77 West Wacker Drive, Suite 3500, Chicago, IL 60601; Robert Bennett, Sara H. Daggett, and William J. Tipping, GASKINS, BENNETT, BIRRELL, SCHUPP, LLP, 333 South Seventh Street, Suite 2900, Minneapolis, MN 55402, for defendant Abbott Laboratories. Margaret P. Daday, Anthony J. Anscombe, David J. Grycz, and Karen E. Woodward, SEDGWICK LLP, One North Wacker Drive, Suite 4200, Chicago, IL 60606; Frederick W. Morris, Brian W. Thomson, and Jonathon T. Naples, LEONARD STREET AND DEINARD, PA, 150 South Fifth Street, Suite 2300, Minneapolis, MN 55402; Mark L. Tripp, BRADSHAW FOWLER PROCTOR & FAIRGRAVE PC, 801 Grand Avenue, Suite 3700, Des Moines, IA 50309, for defendant Mead Johnson & Company. 26 CASE 0:08-cv-03414-JRT-JSM Document 439 Filed 03/11/13 Page 2 of 5 This is a failure to warn action brought by Rockland Burks and Adrienne Lawrence (“plaintiffs”), individually and on behalf of their minor child, E.B., against Abbott Laboratories and Mead Johnson & Company (collectively, “defendants”). -

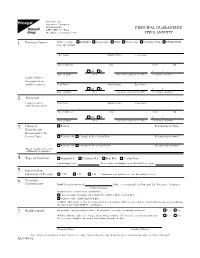

Principal Guaranteed Fixed Annuity

Principal Life Insurance Company 801 Grand Ave. PRINCIPAL GUARANTEED ATTN: IDPC-8th Floor Des Moines, IA 50392-1770 FIXED ANNUITY Primary Owner Owner is a/an: Individual Corporation Trust Partnership Custodian/POA UTMA/UGMA 1. PLEASE PRINT First Name Middle Initial Last Name Street Address City State Zip M F ( ) Date of Birth Sex Social Security or Tax ID # Telephone Number Joint Owner Not applicable for qualified contracts First Name Middle Initial Last Name M F ( ) Date of Birth Sex Social Security or Tax ID # Telephone Number 2. Annuitant Complete only if First Name Middle Initial Last Name different than owner Street Address City State Zip M F ( ) Date of Birth Sex Social Security or Tax ID # Telephone Number 3. Owners Primary Relationship to Owner Beneficiary Do not complete for Pension Trust Primary OR Contingent Beneficiary Name Relationship to Owner Primary OR Contingent Beneficiary Name Relationship to Owner Attach separate sheet for additional beneficiaries 4. Type of Contract Nonqualified Traditional IRA Roth IRA Pension Trust Contribution Year: Date of first contribution to any Roth IRA account: 5. Interest Rate Guaranteed Period 1 Yr* 3 Yr 5 Yr *minimum renewal interest rate for contract year 2 6. Premium Contribution Initial Premium Amount $ Make checks payable to Principal Life Insurance Company $5000 minimum Original source of premium contribution: Transfer from Traditional IRA, Roth IRA, SIMPLE IRA*, or SEP IRA. Rollover from eligible qualified plan. *SIMPLE IRA funds cannot be transferred to a Traditional IRA or converted to a Roth IRA for two years following the date of the initial SIMPLE contribution. 7. -

Proof of Service

·f'OCKLE 2311 Douglas Street . ~Legal Briefs E-Mail Address: Omaha, Nebraska 68102-1214 Est. 1923 [email protected] l-800-225-6964 Web Site ( 402) 342-2831 www.cocklelegalbriefs.com Fax: (402) 342-4850 No. 19-169 JANE DOE, Petitioner, V. IOWA, Respondent. AFFIDAVIT OF SERVICE I, Andrew Cockle, of lawful age, being duly sworn, upon my oath state that I did, on the 9th day of September, 2019, send out from Omaha, NE 3 package(s) containing * copies of the BRIEF OF AMICUS CURIAE PUBLIC DEFENDER ASSOCIATION OF IOWA IN SUPPORT OF PETITIONER JANE DOE in the above entitled case. All parties required to be served have been served by third-party commercial carrier for delivery within 3 calendar days. Packages were plainly addressed to the following: SEE ATTACHED To be filed for: LANCE W. LANGE CHARLES F. WEBBER Counsel of Record ERIN L. HOFFMAN . CHANELLE HAN FA.EGRE BAKER DANIELS LLP FAEGRE BAKER DANIELS LLP 2200 Wells Fargo Center 801 Grand Avenue, 33rd Floor 90 S. Seventh Street Des Moines, Iowa 50309 Minneapolis, Minnesota 55402 (515) 248-9000 (612) 766-7000 [email protected] [email protected] [email protected] [email protected] ALEXANDER E. PRELLER Counsel for Amicus Curiae FAEGRE BAKER DANIELS LLP Public Defender Association 300 N. Meridian Street, of Iowa Suite 2500 Indianapolis, Indiana 46204 (317) 23 7-0300 [email protected] Subscribed and sworn to before me this 9th day of September, 2019. I am duly authorized under the laws of the State of Nebraska to administer oaths.