Legal Developments: Third Quarter, 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

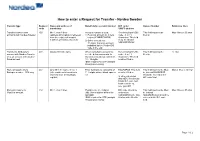

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Uncovering Opportunities in 2017 Deloitte Deleveraging Europe 2016 – 2017

Uncovering opportunities in 2017 Deloitte Deleveraging Europe 2016 – 2017 Financial Advisory Uncovering opportunities in 2017 | Deloitte Deleveraging Europe 2016 – 2017 Contents Introduction Introduction 01 The European loan portfolio market has regained much of the momentum it established over the last number of years. Uncertainty over the terms of Brexit and the US Presidential transition temporarily delayed deal Market overview 02 making in mid-2016, but the fundamental balance sheet and regulatory drivers of loan sale transactions proved stronger. Six months ago we forecast a second half resurgence in loan portfolio sales; that is what has Viewpoint: Risks and opportunities in 2017 06 happened, with more to come in 2017. United Kingdom and Ireland 07 By the numbers the leading European loan sale markets in reach something approaching a point of The record rate of loan disposals achieved in 2017. Portugal, which has yet to deliver a equilibrium. In the meantime we estimate Viewpoint: Banks still need to face reality 12 2015 has been repeated again in 2016, with significant deal flow, is likely to achieve more that there remains €2 trillion in unresolved Germany and the Netherlands just over €103 billion of completed deals for than the €1.8 billion of completed deals in non-core assets in Europe, suggesting that 13 the full year. Yet the Brexit-induced mid-year 2016, if pricing becomes more realistic. the loan sale market has the potential to Spain and Portugal 17 pause in dealmaking had an impact on the expand in 2017. final deal numbers. The number of ongoing Different markets, changing assets Italy 23 deals at the end of 2016 is considerable, with These markets will take the lead from Ireland Headline facts and figures 56 deals representing €70 billion by value. -

Nordea Group Annual Report 2018

Annual Report 2018 CEO Letter Casper von Koskull, President and Group CEO, and Torsten Hagen Jrgensen, Group COO and Deputy CEO. Page 4 4 Best and most accessible advisory, with an 21 easy daily banking experience, delivered at scale. Page 13 Wholesale Banking No.1 relationship Asset & Wealth bank in the Nordics Management with operational Personal Banking 13 excellence. Page 21 Commercial & Business Banking Our vision is to become the lead- ing Asset & Wealth Manager in the 25 Nordic market by 2020. Page 25 Best-in-class advisory and digital experience, 17 ef ciency and scale with future capabilities in a disruptive market. Page 17 Annual Report 2018 Contents 4 CEO letter 6 Leading platform 10 Nordea investment case – strategic priorities 12 Business Areas 35 Our people Board of Directors’ report 37 The Nordea share and ratings 40 Financial Review 2018 46 Business area results 49 Risk, liquidity and capital management 67 Corporate Governance Statement 2018 76 Non-Financial Statement 78 Conflict of interest policy 79 Remuneration 83 Proposed distribution of earnings Financial statements 84 Financial Statements, Nordea Group 96 Notes to Group fi nancial statements 184 Financial statements Parent company 193 Notes to Parent company fi nancial statements 255 Signing of the Annual Report 256 Auditor’s report Capital adequacy 262 Capital adequacy for the Nordea Group 274 Capital adequacy for the Nordea Parent company Organisation 286 Board of Directors 288 Group Executive Management 290 Main legal structure & Group organisation 292 Annual General Meeting & Financial calendar This Annual Report contains forward-looking statements macro economic development, (ii) change in the competitive that reflect management’s current views with respect to climate, (iii) change in the regulatory environment and other certain future events and potential fi nancial performance. -

Caglesmmvig Abanca Corporacion Bancaria, S.A. Casdesbbxxx Arquia Bank, S.A. Bmares2mxxx Banca March, S.A. Bapues22xxx Banca Pueyo, S.A

Classified as Internal / Clasificado como Interno# ENTIDADES PARTICIPANTES Y CÓDIGOS BIC OPERATIVOS EN EL SISTEMA ARCO PARTICIPANT ENTITIES AND OPERATIONAL BIC CODES IN ARCO SYSTEM CÓDIGO BIC ENTIDAD CAGLESMMVIG ABANCA CORPORACION BANCARIA, S.A. CASDESBBXXX ARQUIA BANK, S.A. BMARES2MXXX BANCA MARCH, S.A. BAPUES22XXX BANCA PUEYO, S.A. BBVAESMMXXX BANCO BILBAO VIZCAYA ARGENTARIA, S.A. BBVAESMMBAG BANCO BILBAO VIZCAYA ARGENTARIA, S.A. (entidad agente) CCOCESMMRVN BANCO CAMINOS, S.A. CCOCESMMXXX BANCO CAMINOS, S.A. BCOEESMMRVN BANCO COOPERATIVO ESPAÑOL, S.A. BCOEESMMXXX BANCO COOPERATIVO ESPAÑOL, S.A. ALCLESMMXXX BANCO DE ALCALA, S.A. BCCAESMMXXX BANCO DE CREDITO SOCIAL COOPERATIVO ESPBESMMXXX BANCO DE ESPAÑA ESPBESM1CDI BANCO DE ESPAÑA - CUENTAS DIRECTA ESPBESM1AMF BANCO DE ESPAÑA - FROB FFA ESPBESM1OFI BANCO DE ESPAÑA, OPERACIONES FINANCIACION INTRADIA ESPBESMMAFD BANCO DE ESPAÑA. AGENTE FINANCIERO DEUDA (entidad agente) ESPBESMMRMS BANCO DE ESPAÑA. RMS ESPBESMMCCB BANCO DE ESPAÑA CORRESPONSALÍA DE VALORES BSABESBBXXX BANCO DE SABADELL, S.A BSABESBBBME BANCO DE SABADELL, S.A (entidad agente) BSABESBBEAG BANCO DE SABADELL, S.A (entidad agente) BFIAPTPLXXX BANCO FINATIA, S.A. (entidad agente) INVLESMMXXX BANCO INVERSIS, S.A. INVLESMMOPS BANCO INVERSIS, S.A. (entidad agente) BFIVESBBRFP BANCO MEDIOLANUM, S A BFIVESBBXXX BANCO MEDIOLANUM, S.A. BSCHESMMXXX BANCO SANTANDER, S.A. BSCHESMMAGE BANCO SANTANDER, S.A. (entidad agente) BSCHESMMBME BANCO SANTANDER, S.A. (entidad agente) CAHMESMMXXX BANKIA, S.A. BKBKESMMBAC BANKINTER, S.A. BKBKESMMXXX BANKINTER, S.A. BKOAES22XXX BANKOA S.A. BARCGB22XXX BARCLAYS BANK PLC. ESPBESMMPLV BE. PROGRAMA DE LENDING PSPP. VALORES CMBOESMMBK2 BEKA FINANCE (entidad agente) MEFFESBBCRF BME CLEARING S.A.U. MEFFESBBCRV BME CLEARING, S.A. - CAMARA DE RENTA VARIABLE MEFFESBBMRV BME CLEARING, S.A.U. -

ABANCA CORPORACIÓN BANCARIA, S.A. €375,000,000 Perpetual Non-Cumulative Additional Tier 1 Preferred Securities

ABANCA CORPORACIÓN BANCARIA, S.A. (incorporated as a limited liability company (sociedad anónima) under the laws of the Kingdom of Spain) €375,000,000 Perpetual Non-Cumulative Additional Tier 1 Preferred Securities The issue price of the €375,000,000 Perpetual Non-Cumulative Additional Tier 1 Preferred Securities of €200,000 of Original Principal Amount each (as defined in the terms and conditions of the Preferred Securities (the "Conditions")) (the "Preferred Securities") of ABANCA Corporación Bancaria, S.A. (the "Issuer" or "Bank" or "ABANCA") is 100% of their principal amount. The Preferred Securities have been issued on 20 January 2021 (the "Issue Date"). The Bank and its consolidated subsidiaries are referred to herein as the "ABANCA Group". The Preferred Securities will accrue non-cumulative cash distributions ("Distributions") on their Outstanding Principal Amount (as defined in the Conditions), as follows: (i) in respect of the period from (and including) the Issue Date to (but excluding) 20 July 2026 (the "First Reset Date"), at the rate of 6% per annum, and (ii) in respect of each period from (and including) the First Reset Date and every fifth anniversary thereof (each a "Reset Date") to (but excluding) the next succeeding Reset Date (each such period, a "Reset Period"), at the rate per annum, calculated on an annual basis and then converted to a quarterly rate in accordance with market convention, equal to the aggregate of 6.57% per annum (the "Initial Margin") and the 5- year Mid-Swap Rate (as defined in the Conditions) for the relevant Reset Period. Subject as provided in the Conditions, such Distributions will be payable quarterly in arrear on 20 January, 20 April, 20 July and 20 October in each year (each a "Distribution Payment Date"). -

Fitch Ratings ING Groep N.V. Ratings Report 2020-10-15

Banks Universal Commercial Banks Netherlands ING Groep N.V. Ratings Foreign Currency Long-Term IDR A+ Short-Term IDR F1 Derivative Counterparty Rating A+(dcr) Viability Rating a+ Key Rating Drivers Support Rating 5 Support Rating Floor NF Robust Company Profile, Solid Capitalisation: ING Groep N.V.’s ratings are supported by its leading franchise in retail and commercial banking in the Benelux region and adequate Sovereign Risk diversification in selected countries. The bank's resilient and diversified business model Long-Term Local- and Foreign- AAA emphasises lending operations with moderate exposure to volatile businesses, and it has a Currency IDRs sound record of earnings generation. The ratings also reflect the group's sound capital ratios Country Ceiling AAA and balanced funding profile. Outlooks Pandemic Stress: ING has enough rating headroom to absorb the deterioration in financial Long-Term Foreign-Currency Negative performance due to the economic fallout from the coronavirus crisis. The Negative Outlook IDR reflects the downside risks to Fitch’s baseline scenario, as pressure on the ratings would Sovereign Long-Term Local- and Negative increase substantially if the downturn is deeper or more prolonged than we currently expect. Foreign-Currency IDRs Asset Quality: The Stage 3 loan ratio remained sound at 2% at end-June 2020 despite the economic disruption generated by the lockdowns in the countries where ING operates. Fitch Applicable Criteria expects higher inflows of impaired loans from 4Q20 as the various support measures mature, driven by SMEs and mid-corporate borrowers and more vulnerable sectors such as oil and gas, Bank Rating Criteria (February 2020) shipping and transportation. -

ABANCA and Crédit Agricole Assurances Announce They Have

ABANCA and Crédit Agricole Assurances announce they have signed a partnership for the creation of a property and casualty insurance company aimed at the Spanish and Portuguese market • The new joint venture will be based in Galicia and will combine ABANCA's knowledge of the customer base with Crédit Agricole Assurances’ technical and product expertise. • This agreement will see Europe’s leading bancassurer team up with the Galician financial institution as part of a long-term arrangement. • The new company will take a disruptive approach to develop technological solutions tailored to the needs of its customers and to expand its activity. 08/07/2019. ABANCA and Crédit Agricole Assurances are today announcing the signature of a 30-year partnership agreement to carry out property and casualty insurance activities in Spain and Portugal. Under this agreement, Europe’s leading bancassurer will team up with the financial institution to create a 50/50 joint venture offering innovative products that draw on stand-out technological solutions and customer experience. The alliance will combine ABANCA's customer knowledge with Crédit Agricole Assurances’ acquired scale on the European insurance market. The press conference was attended by Crédit Agricole Assurances’ Chief Executive Officer and Head of International Insurance, Frédéric Thomas and Guillaume Oreckin, and ABANCA's Chairman and Chief Executive Officer, Juan Carlos Escotet Rodríguez and Francisco Botas Ratera “To achieve our growth objectives, we need to work with a powerful industry player -

Responsible Banking 22 September 2019

Official Signing and Global Launch of the Principles for Responsible Banking 22 September 2019 Date/Time: 22 September, 14.00-15.30 Location: Trusteeship Council Attendance: About 300-400 high-level representatives from: banks becoming the Founding Signatories of the Principles for Responsible Banking, financial sector institutions, civil society, high-level UN representatives, VIPs, policy makers and international media. Background on the Event and the Principles for Responsible Banking: Official Signing and Global Launch of the Principles for Responsible Banking More than 40 bank CEOs from all five continents have personally committed to come to New York on 22nd and September 2019, to join United Nations Secretary-General António Guterres and United Nations Environment Programme (UNEP) Executive Director Inger Andersen to launch the UN Principles for Responsible Banking. The Principles will open the door to leverage the power of the US$ 134.1 trillion banking industry, which is responsible for more than two-thirds of all financing globally, and 90% of financing in developing countries – making their engagement critical to achievement of the Sustainable Development Goals (SDGs). Already endorsed by 130 banks from over 45 countries representing more than US$47 trillion in assets and with that over one third of the global banking industry, the Principles are the most significant mechanism ever created jointly between the UN and the global banking industry. Background The Principles for Responsible Banking set the criteria for responsible and sustainable banking. The 130 banks that have already committed to the Principles, and the many others that are set to follow, demonstrate the highest-level commitment from the banking industry. -

Nordea Fund of Funds, SICAV Société D’Investissement À Capital Variable R.C.S

Nordea Fund of Funds, SICAV Société d’Investissement à Capital Variable R.C.S. Luxembourg B 66 248 562, rue de Neudorf, L-2220 Luxembourg NOTICE TO SHAREHOLDERS On 25th January 2018 NORDEA and UBS announced an agreement on the acquisition of part of Nordea’s Luxembourg-based private banking business by UBS (hereinafter the “Transaction”). The Transaction foresees the acquisition of part of Nordea Bank S.A.’s business and its integration onto UBS’s advisory platform. Subject to the completion of the Transaction, the shareholders (the “Shareholders“) of Nordea Fund of Funds (the “Company”) are hereby informed of the following changes: 1. Change of the Investment Managers and appointment of an Investment Sub Manager: 1.1. Nordea Investment Management AB : New Investment Manager : Current Investment Manager Investment Manager with effect as of the 15th of October 2018 Nordea Bank S.A. Nordea Investment Management AB, including 562, rue de Neudorf its branches L-2220 Luxembourg Mäster Samuelsgatan 21 Stockholm, M540 10571 Sweden 1.2. UBS Europe SE, Luxembourg Branch : Investment Sub Manager : Nordea Investment Management AB has further appointed UBS Europe SE, Luxembourg Branch, 33 A Avenue J.F. Kennedy L-1855 Luxembourg as investment sub-manager with effect as of the 15th of October 2018. 2. Redemption of shares free of charges Shareholders who do not agree to the changes as described above may redeem their Shares free of any charges, with the exception of any local transaction fees that might be charged by local intermediaries on their own behalf and which are independent from the Company and the Management Company. -

Aareal Bank AG SSM > 900Bps ABANCA Corporación Bancaria S.A. SSM 300 to 599 Bps Alpha Services and Holdings S.A. SSM 600 To

High-level individual results by range adverse scenario, FL Maximum CET1 ratio Institution Sample (FL) depletion by ranges Aareal Bank AG SSM > 900bps ABANCA Corporación Bancaria S.A. SSM 300 to 599 bps Alpha Services and Holdings S.A. SSM 600 to 899 bps Argenta Bank- en Verzekeringsgroep NV SSM 300 to 599 bps AXA Bank Belgium SA ; AXA Bank Belgium NV SSM 600 to 899 bps Banca Carige S.p.A. - Cassa di Risparmio di Genova e Imperia SSM > 900bps Banca Popolare di Sondrio, Società Cooperativa per Azioni SSM 600 to 899 bps Banco de Crédito Social Cooperativo, S.A. SSM 300 to 599 bps Bank of America Europe Designated Activity Company SSM > 900bps Bank of Cyprus Holdings Public Limited Company SSM 600 to 899 bps Bank of Valletta plc SSM > 900bps Banque Degroof Petercam SA SSM 600 to 899 bps Banque et Caisse d’Epargne de l’Etat, Luxembourg SSM 300 to 599 bps Banque Internationale à Luxembourg S.A. SSM 600 to 899 bps BAWAG Group AG SSM < 300bps Biser Topco S.à.r.l. SSM 300 to 599 bps Bpifrance SSM > 900bps C.R.H. - Caisse de Refinancement de l’Habitat SSM < 300bps Citibank Holdings Ireland Limited SSM < 300bps Credito Emiliano Holding S.p.A. SSM < 300bps de Volksbank N.V. SSM > 900bps DekaBank Deutsche Girozentrale SSM 300 to 599 bps Deutsche Apotheker- und Ärztebank eG SSM 300 to 599 bps Deutsche Pfandbriefbank AG SSM 300 to 599 bps Erwerbsgesellschaft der S-Finanzgruppe mbH & Co. KG SSM 300 to 599 bps Eurobank Ergasias Services and Holdings S.A. -

Lloyds Banking Group PLC

Lloyds Banking Group PLC Primary Credit Analyst: Nigel Greenwood, London (44) 20-7176-1066; [email protected] Secondary Contact: Richard Barnes, London (44) 20-7176-7227; [email protected] Table Of Contents Major Rating Factors Outlook Rationale Related Criteria Related Research WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 5, 2020 1 THIS WAS PREPARED EXCLUSIVELY FOR USER CIARAN TRELLIS. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Lloyds Banking Group PLC Major Rating Factors Issuer Credit Rating BBB+/Negative/A-2 Strengths: Weaknesses: • Market-leading franchise in U.K. retail banking, and • Geographically concentrated in the U.K., which is strong positions in U.K. corporate banking and now in recession owing to the impact of COVID-19. insurance. • Our risk-adjusted capital (RAC) ratio is lower than • Cost-efficient operating model that supports strong the average for U.K. peers, which partly reflects the pre-provision profitability, business stability, and deduction of Lloyds' material investment in its competitiveness. insurance business. • Supportive funding and liquidity profiles anchored by strong deposit franchise. WWW.STANDARDANDPOORS.COM/RATINGSDIRECT JUNE 5, 2020 2 THIS WAS PREPARED EXCLUSIVELY FOR USER CIARAN TRELLIS. NOT FOR REDISTRIBUTION UNLESS OTHERWISE PERMITTED. Lloyds Banking Group PLC Outlook The negative outlook on Lloyds Banking Group reflects potential earnings pressures arising from the economic and market impact of the COVID-19 pandemic. Downside scenario If we saw clear signs that the U.K. systemwide domestic loan loss rate was going to exceed 100 basis points in 2020, and not be offset by the prospect of a quick economic recovery, we would likely lower the anchor, our starting point for rating U.K. -

Fondos De Inversión ANEXO A1.1 Sep-15

Fondos de inversión ANEXO A1.1 sep-15 Fondo Compartimento Clase Código ISIN Sociedad Gestora Entidad Depositaria Grupo Financiero 1 KESSLER CASADEVALL, FI - - ES0156304000 GVC GAESCO GESTIÓN, SGIIC, S.A. SANTANDER SECURITIES SERVICES, S.A. GVC GAESCO 30-70 INVERSION, FI - - ES0184833038 INVERCAIXA GESTION, S.A., SGIIC CECABANK, S.A. LA CAIXA A&G TESORERIA, FI - - ES0156873004 A&G FONDOS, SGIIC, SA SANTANDER SECURITIES SERVICES, S.A. EFG BANK ABACO GLOBAL VALUE OPPORTUNITIES FI - A ES0140074008 ABACO CAPITAL, SGIIC, S.A. UBS BANK, S.A. ABACO CAPITAL - B ES0140074016 ABACO CAPITAL, SGIIC, S.A. UBS BANK, S.A. ABACO CAPITAL ABACO RENTA FIJA MIXTA GLOBAL, FI - - ES0140072002 ABACO CAPITAL, SGIIC, S.A. UBS BANK, S.A. ABACO CAPITAL ABANCA FONDEPOSITO, FI - - ES0115019004 AHORRO CORPORACION GESTION, S.G.I.I.C., S.A. ABANCA CORPORACION BANCARIA, S.A. ABANCA ABANCA GARANTIA 3, FI - - ES0157082035 AHORRO CORPORACION GESTION, S.G.I.I.C., S.A. ABANCA CORPORACION BANCARIA, S.A. ABANCA ABANCA GARANTIA 4, FI - - ES0113250031 AHORRO CORPORACION GESTION, S.G.I.I.C., S.A. ABANCA CORPORACION BANCARIA, S.A. ABANCA ABANCA GARANTIA 5, FI - - ES0115081038 AHORRO CORPORACION GESTION, S.G.I.I.C., S.A. ABANCA CORPORACION BANCARIA, S.A. ABANCA ABANCA GARANTIA 6, FI - - ES0117182032 AHORRO CORPORACION GESTION, S.G.I.I.C., S.A. ABANCA CORPORACION BANCARIA, S.A. ABANCA ABANCA GARANTIZADO PREMIUM I, FI - - ES0105577037 AHORRO CORPORACION GESTION, S.G.I.I.C., S.A. ABANCA CORPORACION BANCARIA, S.A. ABANCA ABANCA GESTION, FI ABANCA GESTION /- ES0133400046 AHORRO CORPORACION GESTION, S.G.I.I.C., S.A.