9579 Zenith Larger Text/Sun28

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SBF Overview

SECTION 02 Global Implementation of Mizu To Ikiru SBF Overview We are developing our five regional businesses by focusing on the needs of customers in each country and market. Number of employees Business overview Main products (as of December 31, 2018) Main company name (start year) Suntory Foods Limited (1972) We are strengthening the position of long-selling brands like Suntory Beverage Solution Limited (2016) Suntory Holdings Suntory Tennensui and BOSS, while offering a wide portfolio Suntory Beverage Service Limited (2013) that includes tea, juice drinks, and carbonated beverages. We JAPAN 9,682 Japan Beverage Holdings Inc. (2015) also develop integrated beverage services such as vending Suntory Foods Okinawa Limited (1997) machines, cup vending machines, and water dispensers. Suntory Products Limited (2009) Our business in Europe focuses on brands that have been Suntory Beverage & Food (SBF)* locally loved for many years. Alongside core brands like Orangina Schweppes Holding B.V. (2009) Orangina in France, and Lucozade and Ribena in the UK, EUROPE 3,798 Lucozade Ribena Suntory Limited (2014) we are also developing Schweppes carbonated beverages and a wide range of other products. Our business in Asia consists of soft drinks and health supplements. We have established joint venture companies Suntory Beverage & Food Asia Pte. Ltd. (2011) that manage the soft drink businesses in Vietnam, Thailand, BRAND’S SUNTORY INTERNATIONAL Co., Ltd. (2011) ASIA and Indonesia in a way that fits the specific needs of each 6,963 PT SUNTORY GARUDA BEVERAGE (2011) market. The health supplement business focuses on the Suntory PepsiCo Vietnam Beverage Co., Ltd. (2013) manufacture and sale of the nutritional drink, BRAND’S Suntory PepsiCo Beverage (Thailand) Co., Ltd. -

Comparison of Sports Drink Products 2017

Nutritional Comparison of Sports Drink Products; 2017 All values are per 100mL. All information obtained from nutritional panels on product and from company websites. Energy (kj) CHO (g) Sugar (g) Sodium Potassium (mg/mmol) (mg/mmol) Sports Drink Powerade Ion4 Isotonic Sports Drink Blackcurrant 104 5.8 5.8 28.0 (1.2mmol) 33 (0.9mmol) Powerade Ion4 Isotonic Sports Drink Berry Ice 104 5.8 5.8 28.0 (1.2mmol) 33 (0.9mmol) Powerade Ion4 Isotonic Sports Drink Mountain Blast 105 5.8 5.8 28.0 (1.2mmol) 33 (0.9mmol) Powerade Ion4 Isotonic Sports Drink Lemon Lime 103 5.8 5.8 28.0 (1.2mmol) 33 (0.9mmol) Powerade Ion4 Isotonic Sports Drink Gold Rush 103 5.8 5.8 28.0 (1.2mmol) 33 (0.9mmol) Powerade Ion4 Isotonic Sports Drink Silver Charge 107 5.8 5.8 28.0 (1.2mmol) 33 (0.9mmol) Powerade Ion4 Isotonic Sports Drink Pineapple Storm (+ coconut water) 97 5.5 5.5 38.0 (1.7mmol) 46 (1.2mmol) Powerade Zero Sports Drink Berry Ice 6.1 0.1 0.0 51.0 (2.2mmol) - Powerade Zero Sports Drink Mountain Blast 6.8 0.1 0.0 51.0 (2.2mmol) - Powerade Zero Sports Drink Lemon Lime 6.8 0.1 0.0 56.0 (2.2mmol) - Maximus Sports Drink Red Isotonic Sports Drink 133 7.5 6.0 31.0 - Maximus Sports Drink Big O Isotonic Sports Drink 133 7.5 6.0 31.0 - Maximus Sports Drink Green Isotonic Sports Drink 133 7.5 6.0 31.0 - Maximus Sports Drink Big Squash Isotonic Sports Drink 133 7.5 6.0 31.0 - Gatorade Sports Drink Orange Ice 103 6.0 6.0 51.0 (2.3mmol) 22.5 (0.6mmol) Gatorade Sports Drink Tropical 103 6.0 6.0 51.0 (2.3mmol) 22.5 (0.6mmol) Gatorade Sports Drink Berry Chill 103 6.0 6.0 51.0 -

Osmolality, Ph, and Titratable Acidity of Sports Drinks on the Swiss Market

Original article Swiss Sports & Exercise Medicine, 66 (4), 56–63, 2018 Osmolality, pH, and titratable acidity of sports drinks on the Swiss market Mettler S1,2,*, Weibel E1 1 Department of Health, Bern University of applied sciences, Switzerland, [email protected]; 2 Department of Health Sciences and Technology, ETH Zurich, Switzerland, [email protected] * corresponding author Abstract Zusammenfassung The regular consumption of acidic drinks can erode dental Der Konsum von säurehaltigen Getränken kann zu erosiven enamel and promote caries. As many sports drinks on the Schäden am Zahnschmelz beitragen. Weil viele kommer- market feature critically low pH values, it is possible that zielle Sportgetränke einen für den Zahnschmelz kritischen athletes with regular sports drink consumption harm their pH-Wert aufweisen, kann sich ein regelmässiger Konsum oral health. As neither pH nor osmolality values must be la- entsprechend auf die Zahngesundheit auswirken. Da weder beled on products, it is difficult for athletes to make informed der pH noch die Osmolalität deklariert werden müssen, ist es choices. schwierig, diese Parameter bei der Produktauswahl zu be- We screened the Swiss market for sports drinks and gels rücksichtigen. for domestic and international brands and products and ana- Wir haben Sportgetränke und Gels von nationalen und lyzed products for their pH, titratable acidity, and osmolality. internationalen Markenherstellern auf dem Schweizer Markt For all analyzed parameters, the results varied widely. We auf pH, titrierbare Säure und Osmolalität analysiert. identified several products with a neutral pH and or low ti- Für alle analysierten Parameter wurde eine starke Streu- tratable acidity. On the other hand, there are still many prod- ung festgestellt. -

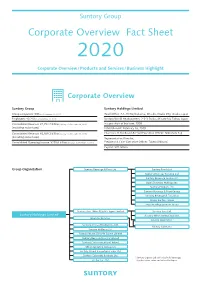

Corporate Overview Fact Sheet 2020

Suntory Group Corporate Overview Fact Sheet 2020 Corporate Overview/ Products and Services / Business Highlight Corporate Overview Suntory Group Suntory Holdings Limited Group companies: 300 (as of December 31, 2019) Head Office: 2-1-40 Dojimahama, Kita-ku, Osaka City, Osaka, Japan Employees: 40,210 (as of December 31, 2019) Suntory World Headquarters: 2-3-3 Daiba, Minato-ku, Tokyo, Japan Consolidated Revenue: ¥2,294.7 billion (January 1 to December 31, 2019) Inauguration of business: 1899 (excluding excise taxes) Establishment: February 16, 2009 Consolidated Revenue: ¥2,569.2 billion (January 1 to December 31, 2019) Chairman of the Board & Chief Executive Officer: Nobutada Saji (including excise taxes) Representative Director, Consolidated Operating Income: ¥259.6 billion (January 1 to December 31, 2019) President & Chief Executive Officer: Takeshi Niinami Capital: ¥70 billion Group Organization Suntory Beverage & Food Ltd. Suntory Foods Ltd. Suntory Beverage Solution Ltd. Suntory Beverage Service Ltd. Japan Beverage Holdings Inc. Suntory Products Ltd. Suntory Beverage & Food Europe Suntory Beverage & Food Asia Frucor Suntory Group Pepsi Bottling Ventures Group Suntory Beer, Wine & Spirits Japan Limited Suntory Beer Ltd. Suntory Holdings Limited Suntory Wine International Ltd. Beam Suntory Inc. Suntory Liquors Ltd.* Suntory (China) Holding Co., Ltd. Suntory Spirits Ltd. Suntory Wellness Ltd. Suntory MONOZUKURI Expert Limited Suntory Business Systems Limited Suntory Communications Limited Other operating companies Suntory Global Innovation Center Ltd. Suntory Corporate Business Ltd. * Suntory Liquors Ltd. sells alcoholic beverage Sunlive Co., Ltd. (spirits, beers, wine and others) in Japan. Suntory Group Corporate Overview Fact Sheet Products and Services Non-alcoholic Beverage and Food Business/Alcoholic Beverage Business Non-alcoholic Beverage and Food Business We deliver a wide range of products including mineral water, coffee, tea, carbonated drinks, sports drinks and health foods. -

Energy Drinks and Children

House of Commons Science and Technology Committee Energy drinks and children Thirteenth Report of Session 2017–19 Report, together with formal minutes relating to the report Ordered by the House of Commons to be printed 27 November 2018 HC 821 Published on 4 December 2018 by authority of the House of Commons Science and Technology Committee The Science and Technology Committee is appointed by the House of Commons to examine the expenditure, administration and policy of the Government Office for Science and associated public bodies. Current membership Norman Lamb MP (Liberal Democrat, North Norfolk) (Chair) Vicky Ford MP (Conservative, Chelmsford) Bill Grant MP (Conservative, Ayr, Carrick and Cumnock) Darren Jones MP (Labour, Bristol North West) Liz Kendall MP (Labour, Leicester West) Stephen Metcalfe MP (Conservative, South Basildon and East Thurrock) Carol Monaghan MP (Scottish National Party, Glasgow North West) Damien Moore MP (Conservative, Southport) Neil O’Brien MP (Conservative, Harborough) Graham Stringer MP (Labour, Blackley and Broughton) Martin Whitfield MP (Labour, East Lothian) Powers The Committee is one of the departmental select committees, the powers of which are set out in House of Commons Standing Orders, principally in SO No 152. These are available on the internet via www.parliament.uk. Publication Committee reports are published on the Committee’s website at www.parliament.uk/science and in print by Order of the House. Evidence relating to this report is published on the relevant inquiry page of the Committee’s website. Committee staff The current staff of the Committee are: Danielle Nash (Clerk), Zoë Grünewald (Second Clerk), Dr Harry Beeson (Committee Specialist), Dr Elizabeth Rough (Committee Specialist), Martin Smith (Committee Specialist), Sonia Draper (Senior Committee Assistant), Julie Storey (Committee Assistant), and Joe Williams (Media Officer). -

Knowledge of and Attitudes to Sports Drinks of Adolescents Living in South Wales, UK RM FAIRCHILD

Knowledge of and attitudes to sports drinks of adolescents living in South Wales, UK R M FAIRCHILD BSc (Hons), PhD1 D BROUGHTON BDS (Hons) 2 M Z MORGAN BSc (Hons), PGCE, MPH, MPhil, FFPH2 1Cardiff Metropolitan University, Department of Healthcare and Food, Cardiff CF5 2YB 2Applied Clinical Research and Public Health, College of Biomedical and Life Sciences, Cardiff University, School of Dentistry, Heath Park, Cardiff CF14 4XY Key words: oral health, children, sports drinks Word count including abstract 2,399 Abstract – 270 Corresponding author: Ruth M Fairchild (Dr) Cardiff School of Health Sciences Department of Healthcare and Food Cardiff Metropolitan University, Department of Healthcare and Food, Western Avenue Cardiff CF5 2YB ABSTRACT Background: The UK sports drinks market has a turnover in excess of £200M. Adolescents consume 15.6% of total energy as free sugars, much higher than the recommended 5%. Sugar sweetened beverages, including sports drinks, account for 30% of total free sugar intake for those aged 11-18 years. Objective: To investigate children’s knowledge and attitudes surrounding sports drinks. Method: 183 self-complete questionnaires were distributed to four schools in South Wales. Children aged 12 - 14 were recruited to take part. Questions focussed on knowledge of who sports drinks are aimed at; the role of sports drinks in physical activity and the possible detrimental effects to oral health. Recognition of brand logo and sports ambassadors and the relationship of knowledge to respondent’s consumption of sports drinks were assessed. Results: There was an 87% (160) response rate. 89.4% (143) claimed to drink sports drinks. 45.9% thought that sports drinks were aimed at everyone; approximately a third (50) viewed teenagers as the target group. -

Cornwall South West Drinks Brochure 2016 Contents

LWC LWC Cornwall Depot South West Depot (Jolly’s Drinks) King Charles Business Park Wilson Way Old Newton Road Pool Industrial Estate Heathfield Redruth | Cornwall Newton Abbot | Devon TR15 3JD TQ12 6UT 0845 345 1076 0844 811 7399 [email protected] [email protected] ER SE SUMM ASON CORNWALL SOUTH WEST DRINKS BROCHURE 2016 CONTENTS Local Brands ���������������������������������������2-18 National Brands ������������������������������ 19-42 LWC ARE THE LARGEST INDEPENDENT WHOLESALER IN THE UK We currently carry over 6000 product lines But are you competitively priced? including: 127 different draught products of The last three years has seen us grow our sales beers, lagers and ciders from £110 million to £180 million this year� 1,212 different spirit lines We have only done this because we offer the best 740 soft drink lines balance of service, product range and price anywhere 1,035 different wines in the UK today� We are totally committed to 131 cider lines helping our customers grow their sales and 97 RTD’s margins through competitive pricing and a wide Over 1,000 different cask ales and varied product range� Are LWC backed and supported by Sounds good how do I get in touch? all national suppliers? Simple, for Cornwall call Naomi Mankee on LWC are partner wholesaler status with Coors, 0845 345 1076 or email cornwall@lwc-drinks�co�uk InBev and Heineken UK� We also work in for South West call Lucy Tucker on conjunction with ALL regional brewers in the UK� 0844 811 7399 or email southwest@lwc-drinks�co�uk This means that -

ANNUAL REPORT 2015 Corporate Philosophy

ANNUAL Otsuka Holdings Co., Ltd. ANNUAL REPORT 2015 REPORT 2015 For the year ended December 31, 2015 Corporate Philosophy These words embody our commitment to: Creating Contributing to the Improving human innovative lives of people health products worldwide In keeping with this corporate philosophy and the Otsuka mottos of Jissho (Proof through Execution) and Sozosei (Creativity), the Otsuka Group strives to utilize its unique assets and skills to develop differentiated scientific solutions which contribute to the lives of people worldwide in the form of innovative and creative products ranging from pharmaceuticals to consumer products. We are striving to cultivate a culture and a dynamic corporate climate reflecting our vision as a healthcare company. Consistent with this approach, we are dedicated to achieving global sustainability, to our relationships with local communities and to the protection of the natural environment. Monuments embodying the Otsuka Group Philosophy Giant Tomato Trees / Bent Giant Cedar / Floating Stone These three monuments embody the Otsuka Group philosophy, reminding all who visit the birthplace of the Otsuka Group in Tokushima of the importance of being creative and open-minded to new ideas. Message from Corporate the President Philosophy Progress report on the Second Medium-Term Explanation of the Otsuka Group’s Management Plan and description of strategic corporate philosophy moves to achieve sustainable medium- and long-term growth moving forward. Business P.00 P.10 Contents Model Overview of the Otsuka -

“Obesity - from Clinical Practice to Research” Donal O’Shea October 12Th 2013 IPNA, Athlone

“Obesity - from clinical practice to research” Donal O’Shea October 12th 2013 IPNA, Athlone. Outline of talk • A bit of background • Why we are where we are • A healthy lifestyle • Some of our research Obesity: like no previous epidemic • Diabetes • Cancer • Dementia • Cardiovascular Disease • Asthma • Arthritis Causes 4000 – 6000 Deaths per year in Ireland (Pop 5 million) Suicide deaths 486 (2011), Road deaths 161 (2012) Percentage increase in BMI categories since 1986 Sturm and Hattori, Int J Obes 2012 Body Mass Index 40 & 50 BMI 40 BMI 52 Body Mass Index 40 & 50 BMI 40 BMI 52 Guess 32 Guess 41 General facts • Average woman (5 ft 4) normal weight up to 10 stone (65 kilos) needs 1700-1800 kcal per day up tp 50yo then 1500kcal per day • Average man (5ft 10) normal weight up to12 stone (78 kilos) needs 1900-2000 kcal per day up to 50yo then 1700 kcal General Facts • From age of 4 to 14 child should be half age in stone General Facts • From age of 4 to 14 child should be half age in stone (depends on height) 4 year old – 2 stone 8 year old – 4 stone 14 year old – 7 stone And then they fill out….. Childhood Obesity in Ireland (and Europe) • 25% 3 year olds overweight/obese • 25% 9 years olds overweight/obese • low self image, concept and self esteem Growing up in Ireland 2009 Median BMI for each 5-year rise in age of onset of overweight O’Connell et al JPHN 2011 Young Scientist 2012 Age v Weight 75 70 65 60 55 50 45 40 Weight(kg) 35 30 25 20 15 4 4.5 5 5.5 6 6.5 7 7.5 8 8.5 9 9.5 10 10.5 11 11.5 12 12.5 13 13.5 14 Age • Study cohort - 6328 -

Expectativa Do Consumidor De Bebida Funcional Não Alcoólica E Percepção De Alimentos Funcionais

UNIVERSIDADE ESTADUAL PAULISTA “JÚLIO DE MESQUITA FILHO” – UNESP FACULDADE DE CIÊNCIAS FARMACÊUTICAS PROGRAMA DE PÓS-GRADUAÇÃO EM CIÊNCIA DOS ALIMENTOS ALESSANDRA CARVALHO FERRAREZI MENEGARIO Expectativa do consumidor de bebida funcional não alcoólica e percepção de alimentos funcionais Orientadora: Profa. Dra. Magali Monteiro da Silva Coorientadora: Profa. Dra. Camila Pinelli ARARAQUARA - SP 2014 ALESSANDRA CARVALHO FERRAREZI MENEGARIO Expectativa do consumidor de bebida funcional não alcoólica e percepção de alimentos funcionais Tese apresentada ao Programa de Pós-graduação em Ciência dos Alimentos da Faculdade de Ciências Farmacêuticas da Universidade Estadual Paulista “Júlio de Mesquita Filho”, como parte dos requisitos para obtenção do título de Doutora em Ciência dos Alimentos Orientadora: Profa. Dra. Magali Monteiro da Silva Coorientadora: Profa. Dra. Camila Pinelli ARARAQUARA - SP 2014 Ficha Catalográfica Elaborada Pelo Serviço Técnico de Biblioteca e Documentação Faculdade de Ciências Farmacêuticas UNESP – Campus de Araraquara Menegario, Alessandra Carvalho Ferrarezi M541e Expectativa do consumidor de bebida funcional não alcoólica e percepção de alimentos funcionais / Alessandra Carvalho Ferrarezi Menegario. – Araraquara, 2014 113 f. Tese (Doutorado) – Universidade Estadual Paulista. “Júlio de Mesquita Filho”. Faculdade de Ciências Farmacêuticas. Programa de Pós Graduação em Alimentos e Nutrição Orientador: Magali Monteiro da Silva Coorientador: Camila Pinelli . 1. Expectativa do consumidor. 2. Discurso do sujeito coletivo. -

The Optimal Sports Drink

TheÜbersichtsartikel optimal sports drink 25 Susan M. Shirreffs School of Sport & Exercise Sciences, University of Loughborough, Loughborough, United Kingdom The optimal sports drink Summary Zusammenfassung There is a large amount of evidence showing that exercise-induced Eine grosse Anzahl an stichhaltigen Hinweisen zeigt klar auf, dass dehydration has a negative impact on exercise performance and der belastungsbedingte Flüssigkeitsverlust eine Verschlechterung restoration of fluid balance must be achieved after exercise. It is der Leistungsfähigkeit verursacht und dass die Flüssigkeitsbilanz equally well known that muscle glycogen must be restored after nach einer Belastung wiederhergestellt werden muss. Ebenfalls exercise if subsequent performance is not to be negatively affec- bekannt ist, dass die Muskelglycogenspeicher nach einer Belas- ted. Sports drinks are ideally placed to fill both these roles. tung wieder aufgefüllt werden müssen, sofern keine Einbusse bei Clear evidence is available that drinking during exercise improves der nächsten Belastung in Kauf genommen werden soll. Sport- performance, provided that the exercise is of a sufficient duration getränke können beiden Aspekten gerecht werden. for the drink to be emptied from the stomach and be absorbed in Trinken während einer physischen Aktivität verbessert ganz ein- the intestine. Generally, drinking plain water is better than drink- deutig die Leistungsfähigkeit, sofern die Aktivität von genügend ing nothing, but drinking a properly formulated carbohydrate langer Dauer ist, damit das Getränk aus dem Magen entleert und electrolyte sports drink will allow for an even better exercise per- im Darm absorbiert werden kann. Generell gesehen ist das Trinken formance. von reinem Wasser besser als nichts trinken, aber die Verwendung Of importance for rehydration purposes after exercise is consump- eines sinnvoll zusammengesetzten Kohlenhydrat-Elektrolyt-Ge- tion of both an adequate volume (greater than the sweat volume tränkes wird die Leistungsfähigkeit stärker verbessern. -

Long Term Sponsored By

SILVER Long term Sponsored by Lucozade Ogilvy & Mather Lucozade Sport: Longitudinal Case Study COMPANY PROFILE Ogilvy Ireland, part of Ogilvy worldwide is owned by WPP, the world’s second largest marketing communications organisation. The Ogilvy worldwide network includes 497 offices in 125 countries with 14,000+ employees working in over 50 languages providing Advertising, Promotions, Direct Marketing, Public Relations and Digital marketing services. Ogilvy & Mather Dublin, is one of Ireland’s largest advertising agencies handling a diverse portfolio of local Irish clients ranging from finance through major consumer brands to social marketing. INTRODUCTION AND BacKGROUND Launched in Ireland long before ‘Brand Beckham’ and the cult of the sports celebrity, Lucozade Sport recognized the potential in the growing trend for serious amateur participation in sport in Ireland as well as the influence that professional sport was having on amateur players and coaches. “Ten years ago you’d see lads on the team bus on the way up to Croker having a fag. You’d just never see that now” Dessie Dolan, Westmeath senior footballer (FBI Research, summer 2008). Sport is about results. So is this case Lucozade Sport pioneered a drinks category now worth more than €52 million. Before its launch sports drinks were virtually unknown, so our 157 SILVER challenge was to tap in to the hydration and nutrition needs of athletes who were just beginning to understand more about the demands placed on their bodies by sports. Importantly we also needed to establish Lucozade Sport as an Irish brand strong enough to withstand the threat of international brands like Powerade or Gatorade.