Happy LIBOR Day September 4, 2020 | Issue No

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LACCD Vote Center Information for September 14 Recall Election

September 3, 2 021 FOR IMMEDIATE RELEASE News Media Contact: William H. Boyer, Director of Communications | [email protected], (213) 317-6691 COUNTY VOTE CENTERS AVAILABLE AT LACCD COLLEGES LOS ANGELES—Five of the Los Angeles Community College District (LACCD) colleges will serve as official Vote Center locations operated by the Los Angeles County Registrar- Record/County Clerk Office for eligible voters to cast ballots for the California Gubernatorial Recall Election September 14, 2021. All registered and eligible voters can cast ballots at the centers or drop off their completed ballots. Los Angeles Pierce College, Los Angeles Trade-Technical College (LATTC) and West Los Angeles College (WLAC) will each serve as 11-day Vote Centers for the County of Los Angeles beginning Saturday, September 4 through Election Day, September 14, 2021. Los Angeles City College and Los Angeles Harbor College will serve as four-day Vote Centers that will be open to the public September 11-14. Vote Centers will be open to the public from 10 a.m. to 7 p.m., including on Labor Day, Monday, September 6, and then from 7 a.m. to 8 p.m. on Election Day, Tuesday, September 14. In addition to the in-person Vote Centers, LATTC, WLAC and Los Angeles Valley College will also have the 24-hour Vote by Mail Drop-off Boxes to help support voters. All LACCD students, faculty, staff and public who are registered and eligible to vote can use any of the County’s Vote Centers in addition to the ones at the LACCD colleges. -

Peoria Unified School District 6-Day Rotation Schedule

Peoria Unified School District 2020 – 2021 School Year Six-Day Rotation Schedule August 2020 January 2021 Day 1: August 17, 19 AM, 26 PM and 27 Day 1: January 6 PM, 11 and 22 Day 2: August 18 and 28 Day 2: January 12, 13 AM, 20 PM and 25 Day 3: August 23 and 31 Day 3: January 4, 14, 26 and 27 AM Day 4: August 21 Day 4: January 5, 15 and 28 Day 5: August 24 Day 5: January 7, 19 and 29 Day 6: August 25 Day 6: January 8 and 21 September 2020 February 2021 Day 1: September 8, 18 and 29 Day 1: February 2, 12 and 25 Day 2: September 2 AM, 9 PM, and 21 Day 2: February 4, 16 and 26 Day 3: September 11, 16 AM and 23 PM Day 3: February 3 PM, 5 and 18 Day 4: September 1, 14, 24 and 30 AM Day 4: February 8, 10 AM, 17 PM and 19 Day 5: September 3, 15 and 25 Day 5: February 9, 22 and 24 AM Day 6: September 4, 17 and 28 Day 6: February 1, 11 and 23 October 2020 March 2021 Day 1: October 9 and 22 Day 1: March 8, 25 and 31 AM Day 2: October 1, 13 and 23 Day 2: March 9 and 26 Day 3: October 2, 15 and 26 Day 3: March 1, 11 and 29 Day 4: October 5, 7 PM, 16 and 27 Day 4: March 2, 12 and 30 Day 5: October 6, 14 AM, 21 PM and 29 Day 5: March 3 PM, 4 and 22 Day 6: October 8, 20, 28 AM and 30 Day 6: March 5, 10 AM, 23 and 24 PM November 2020 April 2021 Day 1: November 2, 12 and 20 Day 1: April 5, 7 PM, 15 and 27 Day 2: November 3, 13 and 30 Day 2: April 6, 14 AM, 16, 21 PM and 29 Day 3: November 5 and 16 Day 3: April 8, 19, 28 AM and 30 Day 4: November 6 and 17 Day 4: April 9 and 20 Day 5: November 9 and 18 Day 5: April 1, 12 and 22 Day 6: November 4 PM, 10 and 19 Day 6: April 2, 13 and 26 December 2020 May 2021 Day 1: December 7, 15 and 16 AM Day 1: May 7 and 18 Day 2: December 8 and 17 Day 2: May 10 and 19 Day 3: December 1 and 9 Day 3: May 5 PM, 11 and 20 Day 4: December 2 and 10 Day 4: May 3, 12 AM, 13 Day 5: December 3 and 11 Day 5: May 4 and 14 Day 6: December 4 and 14 Day 6: May 6 and 17 EARLY RELEASE or MODIFIED WEDNESDAY • Elementary schools starting at 8 a.m. -

2021 7 Day Working Days Calendar

2021 7 Day Working Days Calendar The Working Day Calendar is used to compute the estimated completion date of a contract. To use the calendar, find the start date of the contract, add the working days to the number of the calendar date (a number from 1 to 1000), and subtract 1, find that calculated number in the calendar and that will be the completion date of the contract Date Number of the Calendar Date Friday, January 1, 2021 133 Saturday, January 2, 2021 134 Sunday, January 3, 2021 135 Monday, January 4, 2021 136 Tuesday, January 5, 2021 137 Wednesday, January 6, 2021 138 Thursday, January 7, 2021 139 Friday, January 8, 2021 140 Saturday, January 9, 2021 141 Sunday, January 10, 2021 142 Monday, January 11, 2021 143 Tuesday, January 12, 2021 144 Wednesday, January 13, 2021 145 Thursday, January 14, 2021 146 Friday, January 15, 2021 147 Saturday, January 16, 2021 148 Sunday, January 17, 2021 149 Monday, January 18, 2021 150 Tuesday, January 19, 2021 151 Wednesday, January 20, 2021 152 Thursday, January 21, 2021 153 Friday, January 22, 2021 154 Saturday, January 23, 2021 155 Sunday, January 24, 2021 156 Monday, January 25, 2021 157 Tuesday, January 26, 2021 158 Wednesday, January 27, 2021 159 Thursday, January 28, 2021 160 Friday, January 29, 2021 161 Saturday, January 30, 2021 162 Sunday, January 31, 2021 163 Monday, February 1, 2021 164 Tuesday, February 2, 2021 165 Wednesday, February 3, 2021 166 Thursday, February 4, 2021 167 Date Number of the Calendar Date Friday, February 5, 2021 168 Saturday, February 6, 2021 169 Sunday, February -

Payroll Calendar 2021

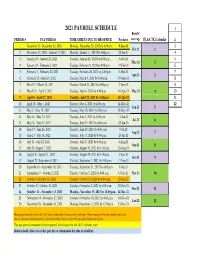

2021 PAYROLL SCHEDULE 1 Benefit PERIOD # PAY PERIOD TIME SHEETS DUE TO HR OFFICE Paydates coverage FLSA 7K Calendar 2 1 December 13- December 26, 2020 Monday, December 28, 2020 by 4:00 p.m. 8-Jan-21 3 Feb-21 1 2 December 27, 2020 - Janurary 9, 2021 Monday, January 11, 2021 by 4:00 p.m. 22-Jan-21 4 3 January 10 - January 23, 2021 Tuesday, January 26, 2021 by 4:00 p.m. 5-Feb-21 5 Mar-21 2 4 January 24 - February 6, 2021 Tuesday, February 9, 2021 by 4:00 p.m. 19-Feb-21 6 5 February 7 - February 20, 2021 Tuesday, February 26, 2021 by 4:00 p.m. 5-Mar-21 7 Apr-21 3 6 February 21 - March 6, 2021 Tuesday, March 9, 2021 by 4:00 p.m. 19-Mar-21 8 7 March 7 - March 20, 2021 Tuesday, March 23, 2021 by 4:00 p.m. 2-Apr-21 9 8 March 21 - April 3, 2021 Tuesday, April 6, 2021 by 4:00 p.m. 16-Apr-21 May-21 4 10 9 April 4 - April 17, 2021 Tuesday, April 20, 2021 by 4:00 p.m. 30-Apr-21 11 10 April 18 - May 1, 2021 Tuesday, May 4, 2021 by 4:00 p.m. 14-May-21 12 Jun-21 5 11 May 2 - May 15, 2021 Tuesday, May 18, 2021 by 4:00 p.m. 28-May-21 12 May 16 - May 29, 2021 Tuesday, June 1, 2021 by 4:00 p.m. 11-Jun-21 Jul-21 6 13 May 30 - June 12, 2021 Tuesday, June 15, 2021 by 4:00 p.m. -

Federal Register/Vol. 85, No. 173/Friday, September 4, 2020

55292 Federal Register / Vol. 85, No. 173 / Friday, September 4, 2020 / Notices DEPARTMENT OF HEALTH AND immunocompromised state, obesity, eviction or possessory action, shall not HUMAN SERVICES serious heart conditions, and diabetes, evict any covered person from any are at increased risk for severe illness residential property in any jurisdiction Centers for Disease Control and from COVID–19.1 to which this Order applies during the Prevention COVID–19 presents a historic threat to effective period of the Order. This Order public health. According to one recent does not apply in any State, local, Temporary Halt in Residential study, the mortality associated with territorial, or tribal area with a Evictions To Prevent the Further COVID–19 during the early phase of the moratorium on residential evictions that Spread of COVID–19 outbreak in New York City was provides the same or greater level of AGENCY: Centers for Disease Control and comparable to the peak mortality public-health protection than the Prevention (CDC), Department of Health observed during the 1918 H1N1 requirements listed in this Order. Nor and Human Services (HHS). influenza pandemic.2 During the 1918 does this order apply to American Samoa, which has reported no cases of ACTION: Agency Order. H1N1 influenza pandemic, there were approximately 50 million influenza- COVID–19, until such time as cases are SUMMARY: The Centers for Disease related deaths worldwide, including reported. Control and Prevention (CDC), located 675,000 in the United States. To In accordance with 42 -

Key Unemployment Insurance (UI)

Attachment II of UIPL No. 14-21 Important Dates for the American Rescue Plan Act of 2021 Benefit Programs Start Date End Date Program Actual Week Ending Statutory Actual Week Ending Start Date Date End Date Date PUA If agreement in place, February 8, 2020 September 6, 20212 September 4, 2021 Claims filed on or before January 27, 20201 (claim effective February December 27, 2020 2, 2020) PUA If agreement in place, December 12, 2020 September 6, 20212 September 4, 2021 Claims filed after December 1, 2020 (claim effective December December 27, 2020 6, 2020) PEUC Date of agreement April 4, 2020 September 6, 20212 September 4, 2021 (generally (claim effective March 29, March 28, 2020)3 2020) FPUC Date of agreement April 4, 2020 July 31, 20202 July 25, 2020 $600 amount (generally March 28, 2020)3 FPUC If agreement in place, January 2, 2021 September 6, 20212 September 4, 2021 $300 amount December 26, 20203 MEUC4 December 27, 2020 January 2, 2021 September 6, 20212 September 4, 2021 Note: Actual week ending date information is for states whose weeks end on a Saturday 1 Weeks of unemployment beginning on or after this date PUA = Pandemic Unemployment Assistance 2 Weeks of unemployment ending on or before this date PEUC = Pandemic Emergency Unemployment Compensation 3 Weeks of unemployment beginning after this date FPUC = Federal Pandemic Unemployment Compensation 4 This is an optional program for states to administer MEUC = Mixed Earners Unemployment Compensation II-1 Other Provisions Start Date End Date Statutory Actual Week Statutory Actual -

August 9 - September 3 September 4 - January 1St 2021 2021 2021 2022

at Conroe Aquatic Center August 9 - September 3 September 4 - January 1st 2021 2021 2021 2022 EDUCATIONAL POOL COMPETITION POOL: Monday - Friday Monday - Thursday 5:00am - 8:00am - Adult Lap Swim** 5:00am – 8:00am – Adult Lap Swim 10:00am - 3:30pm - Adult Lap Swim 10:00am – 12:55pm – Adult Lap Swim** 3:30pm – 4:00pm - Adult Lap Swim** 2:00pm – 8:00pm – Adult Lap Swim** 7:30pm – 8:00pm - Adult Lap Swim Saturday Friday 11:00am – 1:00pm – Adult Lap Swim 5:00am – 8:00am – Adult Lap Swim 9:00am – 1:00pm –Adult Lap Swim EDUCATION POOL: Monday - Thursday 2:00pm – 8:00pm – Adult Lap Swim 5:00am - 8:00am - Adult Lap Swim Saturday 10:00am – 12:55pm - Adult Lap Swim** 8:00am – 1:00pm – Adult Lap Swim** 2:00pm – 4:00 pm - Adult Lap Swim 6:30pm – 8:00pm - Adult Lap Swim** COMPETITION POOL Friday 5:00am – 8:00am - Adult Lap Swim Monday – Friday 9:00am – 12:55pm - Adult Lap Swim 5:00am – 8:00am – Adult Lap Swim 2:00pm - 8:00pm - Adult Lap Swim 10:00am – 4:00pm– Adult Lap Swim Rec Swim(All ages) – 4pm-6:30pm-Begins Sep24 7:30pm – 8:00pm – Adult Lap Swim Saturday Saturday 8:00am – 1:00pm - Adult Lap Swim** 11:00am – 1:00pm – Adult Lap Swim Rec Swim(All ages) – 11am-1pm-Begins Sep25 Subject to change Reduced Lane Space ** Frequently Asked Questions Lap Swim FAQ’s Below are some FAQ's (Frequently Asked Questions) about our Lap Swim. If you have a question that isn't answered after reading this page or are looking for more information, please call the Conroe Aquatic Center at 936-522-3930. -

2018 - 2019 Days of Rotation Calendar

2018 - 2019 DAYS OF ROTATION CALENDAR Day # Date Rotation Day Type Notes Day # Date Rotation Day Type Notes Saturday, October 13, 2018 Sunday, October 14, 2018 Monday, September 3, 2018 Holiday/Vaca Labor Day 27 Monday, October 15, 2018 Day 3 In Session 1 Tuesday, September 4, 2018 Day 1 In Session 28 Tuesday, October 16, 2018 Day 4 In Session 2 Wednesday, September 5, 2018 Day 2 In Session 29 Wednesday, October 17, 2018 Day 5 In Session 3 Thursday, September 6, 2018 Day 3 In Session 30 Thursday, October 18, 2018 Day 6 In Session 4 Friday, September 7, 2018 Day 4 In Session 31 Friday, October 19, 2018 Day 1 In Session Saturday, September 8, 2018 Saturday, October 20, 2018 Sunday, September 9, 2018 Sunday, October 21, 2018 Monday, September 10, 2018 Day Holiday/Vaca Rosh Hashanah 32 Monday, October 22, 2018 Day 2 In Session 5 Tuesday, September 11, 2018 Day 5 In Session 33 Tuesday, October 23, 2018 Day 3 In Session 6 Wednesday, September 12, 2018 Day 6 In Session 34 Wednesday, October 24, 2018 Day 4 In Session 7 Thursday, September 13, 2018 Day 1 In Session 35 Thursday, October 25, 2018 Day 5 In Session 8 Friday, September 14, 2018 Day 2 In Session 36 Friday, October 26, 2018 Day 6 In Session Saturday, September 15, 2018 Saturday, October 27, 2018 Sunday, September 16, 2018 Sunday, October 28, 2018 9 Monday, September 17, 2018 Day 3 In Session 37 Monday, October 29, 2018 Day 1 In Session 10 Tuesday, September 18, 2018 Day 4 In Session 38 Tuesday, October 30, 2018 Day 2 In Session Wednesday, September 19, 2018 Day Holiday/Vaca Yom Kippur 39 Wednesday, October 31, 2018 Day 3 In Session 11 Thursday, September 20, 2018 Day 5 In Session 40 Thursday, November 1, 2018 Day 4 In Session 12 Friday, September 21, 2018 Day 6 In Session 41 Friday, November 2, 2018 Day 5 In Session Saturday, September 22, 2018 Saturday, November 3, 2018 Sunday, September 23, 2018 Sunday, November 4, 2018 13 Monday, September 24, 2018 Day 1 In Session 42 Monday, November 5, 2018 Day 6 In Session 14 Tuesday, September 25, 2018 Day 2 In Session Tuesday, November 6, 2018 Prof Dev. -

Julian Date Cheat Sheet for Regular Years

Date Code Cheat Sheet For Regular Years Day of Year Calendar Date 1 January 1 2 January 2 3 January 3 4 January 4 5 January 5 6 January 6 7 January 7 8 January 8 9 January 9 10 January 10 11 January 11 12 January 12 13 January 13 14 January 14 15 January 15 16 January 16 17 January 17 18 January 18 19 January 19 20 January 20 21 January 21 22 January 22 23 January 23 24 January 24 25 January 25 26 January 26 27 January 27 28 January 28 29 January 29 30 January 30 31 January 31 32 February 1 33 February 2 34 February 3 35 February 4 36 February 5 37 February 6 38 February 7 39 February 8 40 February 9 41 February 10 42 February 11 43 February 12 44 February 13 45 February 14 46 February 15 47 February 16 48 February 17 49 February 18 50 February 19 51 February 20 52 February 21 53 February 22 54 February 23 55 February 24 56 February 25 57 February 26 58 February 27 59 February 28 60 March 1 61 March 2 62 March 3 63 March 4 64 March 5 65 March 6 66 March 7 67 March 8 68 March 9 69 March 10 70 March 11 71 March 12 72 March 13 73 March 14 74 March 15 75 March 16 76 March 17 77 March 18 78 March 19 79 March 20 80 March 21 81 March 22 82 March 23 83 March 24 84 March 25 85 March 26 86 March 27 87 March 28 88 March 29 89 March 30 90 March 31 91 April 1 92 April 2 93 April 3 94 April 4 95 April 5 96 April 6 97 April 7 98 April 8 99 April 9 100 April 10 101 April 11 102 April 12 103 April 13 104 April 14 105 April 15 106 April 16 107 April 17 108 April 18 109 April 19 110 April 20 111 April 21 112 April 22 113 April 23 114 April 24 115 April -

Pay Date Calendar

Pay Date Information Select the pay period start date that coincides with your first day of employment. Pay Period Pay Period Begins (Sunday) Pay Period Ends (Saturday) Official Pay Date (Thursday)* 1 January 10, 2016 January 23, 2016 February 4, 2016 2 January 24, 2016 February 6, 2016 February 18, 2016 3 February 7, 2016 February 20, 2016 March 3, 2016 4 February 21, 2016 March 5, 2016 March 17, 2016 5 March 6, 2016 March 19, 2016 March 31, 2016 6 March 20, 2016 April 2, 2016 April 14, 2016 7 April 3, 2016 April 16, 2016 April 28, 2016 8 April 17, 2016 April 30, 2016 May 12, 2016 9 May 1, 2016 May 14, 2016 May 26, 2016 10 May 15, 2016 May 28, 2016 June 9, 2016 11 May 29, 2016 June 11, 2016 June 23, 2016 12 June 12, 2016 June 25, 2016 July 7, 2016 13 June 26, 2016 July 9, 2016 July 21, 2016 14 July 10, 2016 July 23, 2016 August 4, 2016 15 July 24, 2016 August 6, 2016 August 18, 2016 16 August 7, 2016 August 20, 2016 September 1, 2016 17 August 21, 2016 September 3, 2016 September 15, 2016 18 September 4, 2016 September 17, 2016 September 29, 2016 19 September 18, 2016 October 1, 2016 October 13, 2016 20 October 2, 2016 October 15, 2016 October 27, 2016 21 October 16, 2016 October 29, 2016 November 10, 2016 22 October 30, 2016 November 12, 2016 November 24, 2016 23 November 13, 2016 November 26, 2016 December 8, 2016 24 November 27, 2016 December 10, 2016 December 22, 2016 25 December 11, 2016 December 24, 2016 January 5, 2017 26 December 25, 2016 January 7, 2017 January 19, 2017 1 January 8, 2017 January 21, 2017 February 2, 2017 2 January -

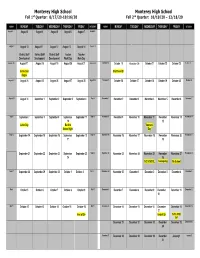

20-21 MHS FALL CALENDAR.Pdf

Monterey High School Monterey High School st nd Fall 1 Quarter: 8/17/20-10/16/20 Fall 2 Quarter: 10/19/20 – 12/18/20 SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDAY SATURDAY SUNDAY MONDAY TUESDAY WEDNESDAY THURSDAY FRIDIAY SATURDAY August 2 August 3 August 4 August 5 August 6 August 7 August 8 August 9 August 10 August 11 August 12 August 13 August 14 August 15 District Staff District Staff District Staff Teacher Teacher Development Development Development Work Day Work Day August 16 August 17 August 18 August 19 August 20 August 21 August 22 October 18 October 19 October 20 October 21 October 22 October 23 October 24 Instruction Start New Qtr Begins August 23 August 24 August 25 August 26 August 27 August 28 August 29 October 25 October 26 October 27 October 28 October 29 October 30 October 31 August 30 August 31 September 1 September 2 September 3 September 4 Sept 5 November 1 November 2 November 3 November 4 November 5 November 6 November 7 Sept 6 September 7 September 8 September 9 September September 11 Sept 12 November 8 November 9 November 10 November 11 November November 13 November 14 10 12 Labor Day Back to Veteran’s School Night Day Sept 13 September 14 September 15 September 16 September September 18 Sept 19 November 15 November 16 November 17 November 18 November November 20 November 21 17 19 September 21 September 22 September 23 September September 25 Sept 26 November 22 November 23 November 24 November 25 November November 27 November 28 24 26 NO SCHOOL Thanksgiving No School Sept 27 September 28 September 29 September -

2021 Park Hours

Holiday World & Splashin' Safari 2021 Operating Calendar May, 2021 Holiday World Hours Splashin' Safari Hours Special Events Saturday, May 1 Holiday World & Splashin' Safari are closed Sunday, May 2 Holiday World & Splashin' Safari are closed Monday, May 3 Holiday World & Splashin' Safari are closed Tuesday, May 4 Holiday World & Splashin' Safari are closed Wednesday, May 5 Holiday World & Splashin' Safari are closed Thursday, May 6 Holiday World & Splashin' Safari are closed Friday, May 7 Holiday World & Splashin' Safari are closed Saturday, May 8 Platinum Season Pass Preview Day: Holiday World is open from 10 AM until 6 PM Splashin' Safari is Closed Platinum Season Passholder Party Sunday, May 9 Passholder Preview Day: Holiday World is open from 10 AM until 6 PM Splashin' Safari is Closed Monday, May 10 Holiday World & Splashin' Safari are closed Tuesday, May 11 Holiday World & Splashin' Safari are closed Wednesday, May 12 Holiday World & Splashin' Safari are closed Thursday, May 13 Holiday World & Splashin' Safari are closed Friday, May 14 Holiday World & Splashin' Safari are closed for a private outing Saturday, May 15 Holiday World is open from 10 AM until 4 PM Splashin' Safari is Closed Sunday, May 16 Holiday World is open from 10 AM until 4 PM Splashin' Safari is Closed Monday, May 17 Holiday World & Splashin' Safari are closed Tuesday, May 18 Holiday World & Splashin' Safari are closed Wednesday, May 19 Holiday World & Splashin' Safari are closed Thursday, May 20 Holiday World & Splashin' Safari are closed Friday, May 21 Holiday