Broadband: the Revolution Underway

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

VIDEO Blu-Ray™ Disc Player BP330

VIDEO Blu-ray™ Disc Player BP330 Internet access lets you stream instant content from Make the most of your HDTV. Blu-ray disc playback Less clutter. More possibilities. Cut loose from Netflix, CinemaNow, Vudu and YouTube direct to delivers exceptional Full HD 1080p video messy wires. Integrated Wi-Fi® connectivity allows your TV — no computer required. performance, along with Bonus-view for a picture-in- you take advantage of Internet access from any picture. available Wi-Fi® connection in its range. VIDEO Blu-ray™ Disc Player BP330 PROFILE & PLAYABLE DISC PLAYABLE AUDIO FORMATS BD Profile 2.0 LPCM Yes USB Playback Yes Dolby® Digital Yes External HDD Playback Yes (via USB) Dolby® Digital Plus Yes BD-ROM/BD-R/BD-RE Yes Dolby® TrueHD Yes DVD-ROM/DVD±R/DVD±RW Yes DTS Yes Audio CD/CD-R/CD-RW Yes DTS-HD Master Audio Yes DTS-CD Yes MPEG 1/2 L2 Yes MP3 Yes LG SMART TV WMA Yes Premium Content Yes AAC Yes Netflix® Yes FLAC Yes YouTube® Yes Amazon® Yes PLAYABLE PHOTO FORMATS Hulu Plus® Yes JPEG Yes Vudu® Yes GIF/Animated GIF Yes CinemaNow® Yes PNG Yes Pandora® Yes MPO Yes Picasa® Yes AccuWeather® Yes CONVENIENCE SIMPLINK™ Yes VIDEO FEATURES Loading Time >10 Sec 1080p Up-scaling Yes LG Remote App Yes (Free download on Google Play and Apple App Store) Noise Reduction Yes Last Scene Memory Yes Deep Color Yes Screen Saver Yes NvYCC Yes Auto Power Off Yes Video Enhancement Yes Parental Lock Yes Yes Yes CONNECTIVITY Wired LAN Yes AUDIO FEATURES Wi-Fi® Built-in Yes Dolby Digital® Down Mix Yes DLNA Certified® Yes Re-Encoder Yes (DTS only) LPCM Conversion -

Ex Parte Presentation with Dickey Rural Telephone Cooperative

7852 Walker Drive, Suite 200 Greenbelt, Maryland 20770 phone: 301-459-7590, fax: 301-577-5575 internet: www.jsitel.com, e-mail: [email protected] November 16, 2012 Marlene H. Dortch, Secretary Federal Communications Commission 445 Twelfth Street, S.W. Washington, D.C. 20554 Re: WC Docket No. 10-90, GN Docket No. 09-51, WC Docket No. 07-135, WC Docket No. 05-337, CC Docket No. 01-92, CC Docket No. 96-45, WC Docket No. 03-109, WT Docket No. 10-208, WC Docket No. 11-42, WC Docket No. 03-109, WC Docket No. 12-23 Notice of Ex Parte Presentation Dear Ms. Dortch: On November 14, 2012, Jeff Wilson of Dickey Rural Telephone Cooperative (“DRTC” or “the Company”), Jeff Fastnacht, District Superintendent of Ellendale Public School, Derrick Owens of the Western Telecommunications Alliance and John Kuykendall of John Staurulakis, Inc. (“JSI”) met separately with Priscilla Argeris, Wireline Legal Advisor to Commissioner Rosenworcel, with Commissioner Mignon Clyburn and her Wireline Legal Advisor, Angela Kronenberg, and with Nicholas Degani, Wireline Legal Advisor to Commissioner Pai. In addition, Mike Romano of the National Telecommunications Cooperative Association, joined the November 14 meeting with Priscilla Argeris. On November 15, 2012, Jeff Wilson, Jeff Fastnacht, John Kuykendall, Mike Romano, and Derrick Owens met separately with Garnet Hanly and Lisa Hone of the Wireline Competition Bureau, and with Christine Kurth, Policy Director and Wireline Counsel to Commissioner McDowell. Mr. Wilson reviewed the successful broadband adoption efforts of DRTC in rural North Dakota throughout its expansive study area, roughly the size of Connecticut, where the Company serves approximately 1.71 access lines per square mile. -

Internet Peer-To-Peer File Sharing Policy Effective Date 8T20t2010

Title: Internet Peer-to-Peer File Sharing Policy Policy Number 2010-002 TopicalArea: Security Document Type Program Policy Pages: 3 Effective Date 8t20t2010 POC for Changes Director, Office of Computing and Information Services (OCIS) Synopsis Establishes a Dalton State College-wide policy regarding copyright infringement. Overview The popularity of Internet peer-to-peer file sharing is often the source of network resource allocation problems and copyright infringement. Purpose This policy will define Internet peer-to-peer file sharing and state the policy of Dalton State College (DSC) on this issue. Scope The scope of this policy includes all DSC computing resources. Policy Internet peer-to-peer file sharing applications are frequently used to distribute copyrighted materials such as music, motion pictures, and computer software. Such exchanges are illegal and are not permifted on Dalton State Gollege computers or network. See the standards outlined in the Appropriate Use Policy. DSG Procedures and Sanctions Failure to comply with the appropriate use of these resources threatens the atmosphere for the sharing of information, the free exchange of ideas, and the secure environment for creating and maintaining information property, and subjects one to discipline. Any user of any DSC system found using lT resources for unethical and/or inappropriate practices has violated this policy and is subject to disciplinary proceedings including suspension of DSC privileges, expulsion from school, termination of employment and/or legal action as may be appropriate. Although all users of DSC's lT resources have an expectation of privacy, their right to privacy may be superseded by DSC's requirement to protect the integrity of its lT resources, the rights of all users and the property of DSC and the State. -

* (Asterisk) in Google, 6 with Group Syntax, 215 in Name

CH27_228-236_Index.qxd 7/14/04 2:48 PM Page 229 INDEXINDEX * (asterisk) Applied Power, Principle of, brand names, 86–88 in Google, 6 102–106 Brooklyn Public Library, 119 with group syntax, 215 area codes, 169–170. See also browsers, 22–40 in name searches, 75 phone number searches bookmarklets with, 34–36 as wildcard, 6 art. See images gadgets for, 36–39 + (plus sign), 4–5. See also askanexpert.com, 93 iCab, 24 Boolean modifiers Ask Jeeves, 17–18 Internet Explorer, 23 – (minus sign), 4–5. See also for Kids, 210 listing, 25 Boolean modifiers toolbar, 32–33 Lynx, 24 | (pipe symbol), 5 associations Mozilla, 23 experts in, 91–93 Netscape, 23 finding, 92–93 Opera, 24 A audio, 154–163 plugins for, 27–29 finding, 159–160 Safari, 24–25 About.com, genealogy at, formats, 154–156 search toolbars with, 29–33 179–180 fun sites for, 162–163 security with, 25–26 address searches playing, 156–158 selecting, 25 driving directions and, 173 search engines/directories specialty toolbars with, 33 names in, 76–77 for, 160–162 speed optimization with, reverse lookups, 168–169 software sources, 158 26–27 229 for things/sites, 78 AU format, 155 turning off auto-password zip code helpers and, 172 reminders in, 26 AIFF format, 155 turning off Java in, 26 ALA Great Web Sites, 210 B turning off pop-ups in, 26 All Experts, 93–94 turning off scripting in, 25 AllPlaces, 134 Babelfish, 227 browser sniffer, 36–37 AlltheWeb, 160 BBB database, 195, 198 Bureau of Consumer Protection, almanacs, 186 Better Business Bureau, 195, 198 195 AltaVista, 148 biographical information, -

4036-0588 Tel: (435) 783-4361 Toll Free: (888) 292-1414 Fax: (435) 783-4928 Web

Albion Telephone Company, Inc. d/b/a ATC Communications 225 West North Street Albion, ID 83311 Tel: (208) 673-5335 Toll Free: () Fax: (208) 673-6200 Web: All West Utah, Inc. 50 West 100 North Kamas, UT 84036-0588 Tel: (435) 783-4361 Toll Free: (888) 292-1414 Fax: (435) 783-4928 Web: www.allwest.net Bear Lake Communications d/b/a CentraCom Interactive 35 South State Street Fairview, UT 84629 Tel: (435) 427-3331 Toll Free: (800) 427-8449 Fax: (435) 427-3200 Web: www.cut.net Beehive Telecom, Inc. 2000 East Sunset Road Lake Point, UT 84074-9779 Tel: (435) 837-6000 Toll Free: (800) 629-9993 Fax: (435) 837-6109 Web: www.beehive.net Carbon - Emery Telecom Inc. 455 East SR 29 Orangeville, UT 84537 Tel: (435) 748-2223 Toll Free: () Fax: (435) 748-5001 Web: www.emerytelcom.net Central Utah Telephone d/b/a CentraCom Interactive 35 South State Street Fairview, UT 84629 Tel: (435) 427-3331 Toll Free: (800) 427-8449 Fax: (435) 427-3200 Web: www.cut.net CenturyTel of Eagle, Inc. d/b/a CenturyLink 100 CenturyLink Drive Monroe, LA 71203 Tel: (318) 388-9081 Toll Free: (800) 562-3956 Fax: (318) 340-5244 Web: www.centurytel.com Citizens Telecommunications Company of Utah d/b/a Frontier Communications of Utah 1800 41st Street Everett, WA 98201 Tel: (801) 298-0757 Toll Free: Fax: (801) 298-0758 Web: Direct Communications Cedar Valley, LLC 150 South Main Rockland, ID 83271 Tel: (801) 789-2800 Toll Free: () Fax: (801) 789-8119 Web: Emery Telephone d/b/a/ Emery Telcom 455 East SR 29 Orangeville, UT 84537-0550 Tel: (435) 748-2223 Toll Free: Fax: (435) 748-5001 Web: www.etv.net Farmers Telephone Company, Inc 26077 Highway 666 Pleasant View, CO 81331 Tel: (970) 562-4211 Toll Free: (877) 828-8656 Fax: (970) 562-4214 Web: www.farmerstelcom.com Gunnison Telephone Company 29 South Main Street Gunnison, UT 84634 Tel: (435) 528-7236 Toll Free: () Fax: (435) 528-5558 Web: www.gtelco.net Hanksville Telecom, Inc. -

On the Fringe: a Practical Start-Up Guide to Creating, Assembling, and Evaluating a Fringe Festival in Portland, Oregon

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by University of Oregon Scholars' Bank ON THE FRINGE: A PRACTICAL START-UP GUIDE TO CREATING, ASSEMBLING, AND EVALUATING A FRINGE FESTIVAL IN PORTLAND, OREGON By Chelsea Colette Bushnell A Master’s Project Presented to the Arts and Administration program of the University of Oregon in partial fulfillment of the requirements for the degree of Master’s of Science in Arts and Administration November 2004 1 ON THE FRINGE: A Practical Start-Up Guide to Creating, Assembling, and Evaluating a Fringe Festival in Portland, Oregon Approved: _______________________________ Dr. Gaylene Carpenter Arts and Administration University of Oregon Date: ___________________ 2 © Chelsea Bushnell, 2004 Cover Image: Edinburgh Festival website, http://www.edfringe.com, November 12, 2004 3 Title: ON THE FRINGE: A PRACTICAL START-UP GUIDE TO CREATING, ASSEMBLING, AND EVALUATING A FRINGE FESTIVAL IN PORTLAND, OREGON Abstract The purpose of this study was to develop materials to facilitate the implementation of a seven- to-ten day Fringe Festival in Portland, Oregon or any similar metro area. By definition, a Fringe Festival is a non-profit organization of performers, producers, and managers dedicated to providing local, national, and international emerging artists a non-juried opportunity to present new works to arts-friendly audiences. All Fringe Festivals are committed to a common philosophy that promotes accessible, inexpensive, and fun performing arts attendance. For the purposes of this study, qualitative research methods, supported by action research and combined with fieldwork and participant observations, will be used to investigate, describe, and document what Fringe Festivals are all about. -

Curriculum Materials

FIGHT BACK WITH LOVE: Every Adult Has a Responsibility to Prevent Bullying Curriculum Materials Endorsement: The Greater Phoenix Child Abuse Prevention Council is pleased to endorse the contents of this video series. If the victim is a child--Bullying is child abuse— whether done by an adult or another child. These videos are making an important contribution to child abuse prevention. Chairpersons, April 2003 TABLE OF CONTENTS BY DESIGN--How to Use these videos and curriculum materials……………………….3 Why bullying is a focus today…………………………………………………………4 The BULLY……………………………………………………………………………………….7 The VICTIM……………………………………………………………………………………10 The BYSTANDER……………………………………………………………………………13 Gender Issues……………………………………………………………………………….15 Bullying in the community and workplace…………………………………..17 Handouts…………………………………………………………………………………….…18 Resources………………………………………………………………………………….....22 Copyright, 2003. Permission is given for duplication and use of all materials for educational purposes, not for commercial or for-profit uses. Citation credit to: Maricopa County Juvenile Probation Department FIGHT BACK WITH LOVE: Every Adult Has a Responsibility to Prevent Bullying Video and Curriculum Series http://www.superiorcourt.maricopa.gov/juvenileprob/ All materials have been created and prepared by the Maricopa County Juvenile Probation Dept. through grant funding from the Offices of Juvenile Justice and Delinquency Prevention. 2 By Design: How to use these videos and curriculum materials We have designed this set of videos to be as specific as possible to the behaviors and developmental phases of the two predominant age groups that fill our school campuses: the younger group, generally those beginning school through the fifth grade and the older group, roughly the middle school and high school students. Within these two groups studies have found that the discrete acts of bullying differ due to the developmental phases of the students but the goal of the bullying behavior is the same: dominance. -

Utah Telephone Assistance Program (Utap) Lifeline/Linkup Application

Form: DCC – UTAP UTAH TELEPHONE ASSISTANCE PROGRAM (UTAP) Rev. 0807 LIFELINE/LINKUP APPLICATION (Landline Only) APPLICANT NAME: (print) Date: __________________ Last First M.I. ADDRESS: APT. # CITY UT ZIP YOUR TELEPHONE NO.: _________________________ TELEPHONE COMPANY: (Landline only) Area Code Telephone Number Name of Telephone Company Is the telephone service in the applicant’s name? YES or NO . If no, whose name is it in? ____________ ________ If you do not currently have telephone service, you may be also eligible for LINKUP which may give you discounts with connection and/or reconnection fees. Do you want to apply for LINKUP? YES or NO . If YES, please leave a name and a telephone number where you can be reached or where a message can be retrieved so we can notify you if needed. NAME Of CONTACT: (print) TELEPHONE NO.: Area Code Telephone Number INSTRUCTIONS: The applicant for service must be the head of the household or person in whose name the property or rental agreement resides. A household member must be someone living at the property. Fill in all answers in the questionnaire below. NOTE: If a household member is participating in any program listed in Part A, you do NOT need to fill out Part B; however, verifications may be required. After completing the application and attaching needed verifications Mail to: Community & Culture/UTAP Program, 324 South State Street, Suite 500, Salt Lake City Utah 84111. Please check one of the boxes below if you or someone in your household receives one of the programs PART A listed below. -

“It's Gonna Be Some Drama!”: a Content Analytical Study Of

“IT’S GONNA BE SOME DRAMA!”: A CONTENT ANALYTICAL STUDY OF THE PORTRAYALS OF AFRICAN AMERICANS AND HISTORICALLY BLACK COLLEGES AND UNIVERSITIES ON BET’S COLLEGE HILL _______________________________________ A Dissertation presented to the Faculty of the Graduate School at the University of Missouri _______________________________________________________ In Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy _____________________________________________________ by SIOBHAN E. SMITH Dr. Jennifer Stevens Aubrey, Dissertation Supervisor DECEMBER 2010 © Copyright by Siobhan E. Smith 2010 All Rights Reserved The undersigned, appointed by the dean of the Graduate School, have examined the dissertation entitled “IT’S GONNA BE SOME DRAMA!”: A CONTENT ANALYTICAL STUDY OF THE PORTRAYALS OF AFRICAN AMERICANS AND HISTORICALLY BLACK COLLEGES AND UNIVERSITIES ON BET’S COLLEGE HILL presented by Siobhan E. Smith, a candidate for the degree of doctor of philosophy, and hereby certify that, in their opinion, it is worthy of acceptance. Professor Jennifer Stevens Aubrey Professor Elizabeth Behm-Morawitz Professor Melissa Click Professor Ibitola Pearce Professor Michael J. Porter This work is dedicated to my unborn children, to my niece, Brooke Elizabeth, and to the young ones who will shape our future. First, all thanks and praise to God, from whom all blessings flow. For it was written: “I can do all things through Christ which strengthens me” (Philippians 4:13). My dissertation included! The months of all-nighters were possible were because You gave me strength; when I didn’t know what to write, You gave me the words. And when I wanted to scream, You gave me peace. Thank you for all of the people you have used to enrich my life, especially those I have forgotten to name here. -

SEACHANGE INTERNATIONAL, INC. 2005 ANNUAL REPORT Seachange International, Inc

Building the framework for the future of television. SEACHANGE INTERNATIONAL, INC. 2005 ANNUAL REPORT the ever-increasing market on-demandentertainment for andinformation. the ever-increasing industry thetelevision isallowing that meet to thefoundation providing We’re services, newapplications, revenues. andincreased costs, andreduce operations streamline to companies expanded for allowing components. aresult, As enablebroadband, we broadcast, andnew media satellite based onascalable, distributedsoftware technology architectureandstandard store, digitalvideo. anddistributeprofessional-quality products are Ourinnovative television.Wefor powerful create server manage, that andsoftware systems SeaChange International, Inc. SeaChange International, SeaChange International, Inc. Financial Highlights (all numbers in thousands, except diluted earnings per share) 133,912 122,043 86,900 83,300 100,534 157,303 148,166 62,800 135,626 is aleaderinthemarketdigitalvideosystems for .34 .20 5 4 0 3 0 0 0 0 2 , 0 5 2 , 4 1 2 0 , 1 0 3 0 1 3 0 2 n 3 , 5 2 n a , 4 1 0 J n a 3 1 0 3 0 J a 0 3 0 2 J n , 0 2 n a , 1 2 5 J a , 1 3 4 0 J 1 3 3 0 0 n 3 0 0 2 n a , 0 2 J n a , 1 2 J a , 1 3 J 1 3 n 3 n a J n a J a J (.77) 3 0 0 DILUTED 2 , 1 EARNINGS 3 TOTAL REVENUE VOD SYSTEMS REVENUE n PER SHARE CASH AND INVESTMENTS a J President’s Letter Dear Shareholders, SeaChange is focused on a large emerging market for “personal television.” Worldwide, the business of television is shifting to meet viewers’ rising expectations for choice and convenience. -

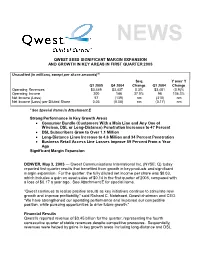

Qwest Sees Significant Margin Expansion and Growth in Key Areas in First Quarter 2005

QWEST SEES SIGNIFICANT MARGIN EXPANSION AND GROWTH IN KEY AREAS IN FIRST QUARTER 2005 Unaudited (in millions, except per share amounts)(a) Seq. Y over Y Q1 2005 Q4 2004 Change Q1 2004 Change Operating Revenues $3,449 $3,437 0.3% $3,481 (0.9)% Operating Income 200 146 37.0% 96 108.3% Net Income (Loss) 57 (139) nm (310) nm Net Income (Loss) per Diluted Share 0.03 (0.08) nm (0.17) nm a See Special Items in Attachment E Strong Performance in Ke y Growth Areas • Consumer Bundle (Customers With a Main Line and Any One of Wireless, DSL or Long-Distance) Penetration Increases to 47 Percent • DSL Subscribers Grow to Over 1.1 Million • Long-Distance Lines Increase to 4.6 Million and 34 Percent Penetration • Business Retail Access Line Losses Improve 59 Percent From a Year Ago Significant Margin Expansion DENVER, May 3, 2005 — Qwest Communications International Inc. (NYSE: Q) today reported first quarter results that benefited from growth in key products and significant margin expansion. For the quarter, the fully diluted net income per share was $0.03, which includes a gain on asset sales of $0.14 in the first quarter of 2005, compared with a loss of $0.17 a year ago. See Attachment E for special items. “Qwest continues to realize positive results as key initiatives continue to stimulate new growth and improve profitability,” said Richard C. Notebaert, Qwest chairman and CEO. “We have strengthened our operating performance and improved our competitive position, while pursuing opportunities to drive future growth.” Financial Results Qwest’s reported revenue of $3.45 billion for the quarter, representing the fourth consecutive quarter of stable revenues despite competitive pressures. -

ONN 6 Eng Codelist Only Webversion.Indd

6-DEVICE UNIVERSAL REMOTE Model: 100020904 CODELIST Need help? We’re here for you every day 7 a.m. – 9 p.m. CST. Give us a call at 1-888-516-2630 Please visit the website “www.onn-support.com” to get more information. 1 TABLE OF CONTENTS CODELIST TV 3 STREAM 5 STB 5 AUDIO SOUNDBAR 21 BLURAY DVD 22 2 CODELIST TV TV EQD 2014, 2087, 2277 EQD Auria 2014, 2087, 2277 Acer 4143 ESA 1595, 1963 Admiral 3879 eTec 2397 Affinity 3717, 3870, 3577, Exorvision 3953 3716 Favi 3382 Aiwa 1362 Fisher 1362 Akai 1675 Fluid 2964 Akura 1687 Fujimaro 1687 AOC 3720, 2691, 1365, Funai 1595, 1864, 1394, 2014, 2087 1963 Apex Digital 2397, 4347, 4350 Furrion 3332, 4093 Ario 2397 Gateway 1755, 1756 Asus 3340 GE 1447 Asustek 3340 General Electric 1447 Atvio 3638, 3636, 3879 GFM 1886, 1963, 1864 Atyme 2746 GPX 3980, 3977 Audiosonic 1675 Haier 2309, 1749, 1748, Audiovox 1564, 1276, 1769, 3382, 1753, 3429, 2121 2293, 4398, 2214 Auria 4748, 2087, 2014, Hannspree 1348, 2786 2277 Hisense 3519, 4740, 4618, Avera 2397, 2049 2183, 5185, 1660, Avol 2735, 4367, 3382, 3382, 4398 3118, 1709 Hitachi 1643, 4398, 5102, Axen 1709 4455, 3382, 0679 Axess 3593 Hiteker 3118 BenQ 1756 HKPro 3879, 2434 Blu:sens 2735 Hyundai 4618 Bolva 2397 iLo 1463, 1394 Broksonic 1892 Insignia 2049, 1780, 4487, Calypso 4748 3227, 1564, 1641, Champion 1362 2184, 1892, 1423, Changhong 4629 1660, 1963, 1463 Coby 3627 iSymphony 3382, 3429, 3118, Commercial Solutions 1447 3094 Conia 1687 JVC 1774, 1601, 3393, Contex 4053, 4280 2321, 2271, 4107, Craig 3423 4398, 5182, 4105, Crosley 3115 4053, 1670, 1892, Curtis