Heidelbergcement Ag Relies on Personal Advice from Vmware

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Heidelbergcement Half-Year Financial Report January to June

Half-Year Financial Report January to June 2020 HeidelbergCement achieves good half-year results for 2020 in challenging environment Weak demand due to coronavirus in second quarter – revenue decreases by 10% in first half of 2020 COPE action plan with high cost savings and preservation of liquidity – result 1) declines only slightly by 2% in the first half of 2020 Group share of net result for the period reduced by non-recurring effect from impairments – adjusted Group share rises by 5% Free cash flow at a strong level – net debt decreases by €1.4 billion Solid start into third quarter but business prospects for second half of 2020 remain uncertain – long-term outlook positive 1) Result from current operations before depreciation and amortisation Overview January to June 2020 January - June €m 2019 1) 2020 Revenue 9,212 8,254 Result from equity accounted investments (REI) 126 98 Result from current operations before depreciation and amortisation (RCOBD) 1) 1,438 1,404 RCOBD margin in % 15.6% 17.0% Result from current operations 1) 754 710 Additional ordinary result -128 -3,490 Earnings before interest and taxes (EBIT) 1) 626 -2,779 Financial result 1) -176 -157 Profit / loss before tax 450 -2,936 Net income / loss from continuing operations 300 -3,075 Net loss from discontinued operations -9 -20 Profit / loss for the period 291 -3,095 Group share of profit / loss 212 -3,133 Investments 501 458 1) Changed due to reclassifications Due to rounding, numbers presented in the Half-Year Financial Report may not add up precisely to the totals provided. -

Factset-Top Ten-0521.Xlsm

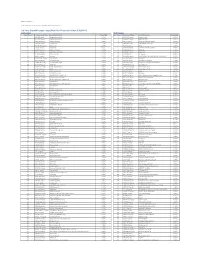

Pax International Sustainable Economy Fund USD 7/31/2021 Port. Ending Market Value Portfolio Weight ASML Holding NV 34,391,879.94 4.3 Roche Holding Ltd 28,162,840.25 3.5 Novo Nordisk A/S Class B 17,719,993.74 2.2 SAP SE 17,154,858.23 2.1 AstraZeneca PLC 15,759,939.73 2.0 Unilever PLC 13,234,315.16 1.7 Commonwealth Bank of Australia 13,046,820.57 1.6 L'Oreal SA 10,415,009.32 1.3 Schneider Electric SE 10,269,506.68 1.3 GlaxoSmithKline plc 9,942,271.59 1.2 Allianz SE 9,890,811.85 1.2 Hong Kong Exchanges & Clearing Ltd. 9,477,680.83 1.2 Lonza Group AG 9,369,993.95 1.2 RELX PLC 9,269,729.12 1.2 BNP Paribas SA Class A 8,824,299.39 1.1 Takeda Pharmaceutical Co. Ltd. 8,557,780.88 1.1 Air Liquide SA 8,445,618.28 1.1 KDDI Corporation 7,560,223.63 0.9 Recruit Holdings Co., Ltd. 7,424,282.72 0.9 HOYA CORPORATION 7,295,471.27 0.9 ABB Ltd. 7,293,350.84 0.9 BASF SE 7,257,816.71 0.9 Tokyo Electron Ltd. 7,049,583.59 0.9 Munich Reinsurance Company 7,019,776.96 0.9 ASSA ABLOY AB Class B 6,982,707.69 0.9 Vestas Wind Systems A/S 6,965,518.08 0.9 Merck KGaA 6,868,081.50 0.9 Iberdrola SA 6,581,084.07 0.8 Compagnie Generale des Etablissements Michelin SCA 6,555,056.14 0.8 Straumann Holding AG 6,480,282.66 0.8 Atlas Copco AB Class B 6,194,910.19 0.8 Deutsche Boerse AG 6,186,305.10 0.8 UPM-Kymmene Oyj 5,956,283.07 0.7 Deutsche Post AG 5,851,177.11 0.7 Enel SpA 5,808,234.13 0.7 AXA SA 5,790,969.55 0.7 Nintendo Co., Ltd. -

Heidelbergcement Annual Report 2020

3 Corporate Governance | Remuneration report Remuneration report The majority of variable remuneration should be linked to the long-term development of the company and paid out after an appropriate period of several years. The absolute The remuneration report contains two parts. The first part development of HeidelbergCement’s share price and the presents the Managing Board remuneration system and the direct comparison with relevant benchmark indices should remuneration of members of the Managing Board for the 2020 play a major role in this context. The long-term nature of financial year, both according to the applicable accounting the variable remuneration components is further supported standards and according to the German Corporate Gover- by the fact that even the termination of a Managing Board nance Code valid in the version of 7 February 2017 and in contract has no influence on the target setting, valuation, parts already valid in the version of 16 December 2019, as and maturity. well as the German Act Implementing the Second Share- 3. Key performance indicators are in accordance with the holders' Rights Directive (Gesetz zur Umsetzung der zweiten Group strategy: The key performance indicators used to Aktionärsrechterichtlinie, ARUG II) of 12 December 2019. determine variable remuneration should be in line with The second part shows the remuneration for the Supervisory HeidelbergCement’s business strategy. Board paid for the 2020 financial year. The system and amount of the Managing Board remunera- Current Managing Board remuneration tion are determined by the Supervisory Board following a system 2020 recommendation by the Personnel Committee. The external adequacy check is based on the size and international activity The current Managing Board remuneration system has been of the Group, its economic and financial situation, and its future applied to all newly and reappointed members of the Manag- prospects. -

Investment Portfolio (UNAUDITED) | 01.31.2021 CARILLON CLARIVEST INTERNATIONAL STOCK FUND COMMON STOCKS - 96.4% Shares Value Australia - 6.4% Austal Ltd

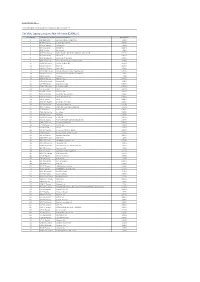

Investment Portfolio (UNAUDITED) | 01.31.2021 CARILLON CLARIVEST INTERNATIONAL STOCK FUND COMMON STOCKS - 96.4% Shares Value Australia - 6.4% Austal Ltd. 15,217 $ 29,697 BHP Group Ltd. 1,577 52,591 Coles Group Ltd. 10,814 149,701 CSL Ltd. 365 75,673 Fortescue Metals Group Ltd. 8,456 139,285 Northern Star Resources Ltd. 6,204 60,038 Resolute Mining Ltd.* 26,683 13,891 Sandfire Resources Ltd. 10,113 36,637 Sonic Healthcare Ltd. 1,960 51,223 Belgium - 0.6% Euronav N.V. 3,933 31,516 UCB S.A. 230 23,817 Denmark - 2.7% AP Moeller-Maersk A/S, Class B 57 117,088 Novo Nordisk A/S, Class B 1,512 105,338 Scandinavian Tobacco Group A/S 2,069 37,460 France - 6.3% BNP Paribas S.A.* 1,287 61,719 Cie Generale des Etablissements Michelin 698 96,189 Constellium SE* 2,500 30,825 Eiffage S.A.* 844 76,608 ENGIE S.A.* 5,396 83,742 Fnac Darty S.A.* 726 40,811 Sanofi 1,307 122,921 Sartorius Stedim Biotech 99 41,449 Societe Generale S.A.* 2,369 44,165 Germany - 8.1% Bayer AG 947 57,315 Daimler AG 2,116 148,615 Deutsche Post AG 2,892 142,850 Deutsche Telekom AG 4,660 82,867 HeidelbergCement AG 980 72,441 Hornbach Holding AG & Co. KGaA 183 17,322 Merck KGaA 816 136,002 Muenchener Rueckversicherungs-Gesellschaft AG 195 51,706 TAG Immobilien AG* 2,175 66,787 Hong Kong - 1.5% CK Hutchison Holdings Ltd. -

DWS CROCI International

Investment Portfolio as of March 31, 2021 (Unaudited) DWS CROCI® International VIP Shares Value ($) Common Stocks 96.0% Australia 9.1% Australia & New Zealand Banking Group Ltd. 84,659 1,814,028 BHP Group Ltd. 110,251 3,815,874 Commonwealth Bank of Australia 4,288 280,930 National Australia Bank Ltd. 62,344 1,234,218 Newcrest Mining Ltd. 15,865 297,603 (Cost $5,536,400) 7,442,653 Belgium 1.6% UCB SA (Cost $1,072,787) 13,795 1,312,687 Denmark 3.0% AP Moller - Maersk AS “B” 870 2,024,140 Novo Nordisk AS “B” 7,052 474,954 (Cost $1,948,110) 2,499,094 Finland 1.0% Fortum Oyj 12,738 340,652 Nokia Oyj* 121,910 486,937 (Cost $695,418) 827,589 France 14.1% Atos SE* 22,260 1,739,792 BNP Paribas SA* 53,894 3,290,488 Credit Agricole SA* 118,678 1,721,985 Engie SA* 79,187 1,127,334 Sanofi 30,370 3,003,484 Television Francaise 1* 80,739 737,194 (Cost $9,733,297) 11,620,277 Germany 8.4% Beiersdorf AG 12,876 1,355,372 Brenntag SE 13,966 1,193,987 Deutsche Boerse AG 4,043 672,742 Deutsche Post AG (Registered) 23,524 1,291,802 Fresenius Medical Care AG & Co. KGaA 7,353 542,699 Fresenius SE & Co. KGaA 10,857 484,249 HeidelbergCement AG 5,007 455,278 Merck KGaA 3,152 539,013 SAP SE 2,641 324,172 (Cost $6,246,907) 6,859,314 Hong Kong 0.7% CLP Holdings Ltd. -

Citi Pure Growth Europe Long-Short Net TR Series II Index (CIISGRE2)

Date: 23-May-21 Index Weights as of monthly rebalance date 12-May-21 Citi Pure Growth Europe Long-Short Net TR Series II Index (CIISGRE2) Long Exposure Short Exposure Constituent Bloomberg Ticker Constituent Name Weight(%) Constituent Bloomberg Ticker Constituent Name Weight(%) 1 AAL LN Equity Anglo American Plc 1.62% 1 1COV GY Equity Covestro AG -0.89% 2 ACA FP Equity Credit Agricole SA 1.37% 2 ABBN SE Equity ABB LTD-REG -0.31% 3 ADM LN Equity Admiral Group 0.09% 3 ABF LN Equity Associated British Foods -0.62% 4 ADS GY Equity Adidas AG 1.01% 4 ABN NA Equity ABN AMRO Group NV -1.24% 5 ADYEN NA Equity Adyen NV 2.43% 5 AC FP Equity Accor -1.54% 6 AD NA Equity Ahold NV 0.61% 6 ADEN SE Equity ADECCO GROUP AG-REG -0.49% 7 AHT LN Equity Ashtead Group 0.24% 7 AENA SQ Equity AENA SA -1.05% 8 ALC SE Equity ALCON AG CHF0.04 0.70% 8 AGN NA Equity Aegon NV -0.71% 9 ALFA SS Equity Alfa Laval AB 0.11% 9 AI FP Equity Air Liquide -0.69% 10 ALO FP Equity Alstom 0.45% 10 AKZA NA Equity AKZO NOBEL NV EUR0.50(POST REV SPLIT) -0.37% 11 AMBUB DC Equity Ambu A/S 1.41% 11 ALV GY Equity Allianz SE -0.79% 12 AMP IM Equity Amplifon SpA 0.45% 12 AMS SQ Equity Amadeus IT Hldg SA -1.78% 13 ANTO LN Equity Antofagasta Hldgs 1.62% 13 VNA GY Equity Deutsche Annington Immobilien -0.27% 14 ASM NA Equity ASM Intl 0.65% 14 ASSAB SS Equity Assa Abloy B -1.11% 15 ASML NA Equity ASML Holding NV 0.82% 15 ATCOA SS Equity Atlas Copco AB A -0.68% 16 ATO FP Equity AtoS 0.51% 16 ATCOB SS Equity Atlas Copco AB B -0.66% 17 AZN LN Equity AstraZeneca Plc 0.38% 17 AV/ LN Equity Aviva -0.07% -

Citi VIBE Equity Eurozone Net TR Index (CIISRLET)

Date: 05-Apr-19 Index Weights as of quarterly rebalance date 04-Apr-19 Citi VIBE Equity Eurozone Net TR Index (CIISRLET) Constituent Bloomberg Ticker Constituent Name Weight(%) 1 ABI BB Equity Anheuser Busch Inbev NV 1.00% 2 ACA FP Equity Credit Agricole SA 0.57% 3 ADS GY Equity Adidas AG 1.20% 4 AD NA Equity Ahold NV 3.42% 5 AI FP Equity Air Liquide 1.53% 6 AKZA NA Equity AKZO NOBEL NV EUR0.50(POST REV SPLIT) 0.91% 7 ALV GY Equity Allianz SE 0.91% 8 AMS SM Equity Amadeus IT Hldg SA 0.99% 9 VNA GY Equity Deutsche Annington Immobilien 4.95% 10 ASML NA Equity ASML Holding NV 0.66% 11 BAS GY Equity BASF SE 0.63% 12 BAYN GY Equity Bayer AG 0.54% 13 BBVA SM Equity Banco Bilbao Vizcaya Argentaria SA 0.74% 14 BMW GY Equity Bayer Motoren Werke AG (BMW) 1.03% 15 BN FP Equity Danone 1.76% 16 BNP FP Equity BNP Paribas 0.63% 17 CABK SM Equity CaixaBank 1.19% 18 CAP FP Equity Cap Gemini SA 0.55% 19 CON GY Equity Continental AG 0.64% 20 CS FP Equity AXA 0.81% 21 DAI GY Equity Daimler AG 0.66% 22 DB1 GY Equity Deutsche Boerse AG 2.04% 23 DBK GY Equity Deutsche Bank AG 0.53% 24 DG FP Equity Vinci 0.88% 25 DPW GY Equity Deutsche Post AG 0.84% 26 DTE GY Equity Deutsche Telekom 9.12% 27 AIR FP Equity EADS NV-Euro Aero Defense 0.56% 28 EL FP Equity Essilor Intl 5.40% 29 ENEL IM Equity Enel SpA 3.05% 30 ENI IM Equity ENI SpA 0.92% 31 EOAN GY Equity E.ON AG 1.91% 32 FCA IM Equity FIAT CHRYSLER AUTOMOBILES NV 0.87% 33 FME GY Equity Fresenius Medical 0.85% 34 FP FP Equity TOTAL SA 1.10% 35 FR FP Equity Valeo 0.50% 36 FRE GY Equity Fresenius SE & Co KGaA 0.82% 37 G IM Equity Assicurazioni Generali SpA 1.14% 38 GLE FP Equity Societe Generale 0.81% 39 ENGI FP Equity GDF Suez 1.46% 40 HEI GY Equity HeidelbergCement AG 0.59% 41 HEIA NA Equity Heineken NV 1.33% 42 HEN3 GY Equity Henkel AG & Co. -

Experience in the Industrials & Chemicals Sector

EXPERIENCE IN THE INDUSTRIALS &CHEMICALS SECTOR Sullivan & Cromwell offers clients comprehensive legal expertise paired with a practical understanding of commercial reality. Our pragmatic approach and multidisciplinary and integrated global practice allow us to provide our clients in the industrial and chemical and related industries with 360-degree advice on the legal issues most critical to them. Clients benefit not only from our understanding of the complexities of these industries, but also from our market-leading M&A practice and our long-standing capital markets, finance, litigation, environmental, executive compensation, tax, restructuring, competition and intellectual property capabilities. Through our 13 offices on four continents, we act as one firm taking an integrated approach to all client matters worldwide. This, combined with the depth of our expertise and capabilities, ensures that we can execute any type of transaction, in any economic climate or region. Copyright © 2020 Sullivan & Cromwell LLP | LG6298 (04/20) Attorney Advertising. Prior results do not guarantee a similar outcome. Recent Accolades Energy Winner of Group of The Deal Awards Europe’s 2019 the Year Energy & Industrials Law360, 2019 Deal of the Year Ranked in (Merck/Versum Materials) Band 1 Advised on over for Corporate/M&A $4.5 trillion Chambers USA in announced M&A transactions worldwide over the #1 past 10 years ranked firm on global Thomson M&A industrial & materials transactions for the Finalist: past five years Litigation Thomson Department of Advised the Year on The Deal’s 2019 The American Lawyer, Energy & 2017 Industrials M&A Group Deal of of the Year Law360, 2019 the Year (Harris/L3) INDUSTRIAL & MATERIALS M&A RANKINGS 2015 – Q1 2020 Ranked by value ($ billions) Sullivan & Cromwell $744 Davis Polk $688 Cleary Gottlieb $673 Wachtell $661 Cravath $639 Skadden $565 Source: Thomson, April 2020 Data include representations of both principals and financial advisers. -

Building on Sustainability

Inhaltsverzeichis 2 GROUP SUSTAINABILITY REPORT 2004/2005 BUILDING ON SUSTAINABILITY Copyright © 2005 HeidelbergCement AG Berliner Strasse 6 69120 Heidelberg, Germany ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ Establishment & growth Concept and realisation ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ Group Communication HeidelbergCement, Heidelberg, Germany ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ IFOK – Institut für Organisationskommunikation, Bensheim, Germany ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ Studio Delhi, Konzept und Design, Mainz, Germany ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ Sustainability & strategy Koch Lichtsatz und Scan GmbH, Wiesbaden, Germany ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ColorDruck Leimen GmbH, Leimen, Germany ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ Photographs ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ ➔ Markets & added value Photo archives HeidelbergCement, Heidelberg ➔ ➔ ➔ -

Heidelbergcement Group Presentation 2021

Change the slide layout HeidelbergCement Group Presentation 2021 Find a choice of background Material to build our future. HeidelbergCement Headquarters, Heidelberg, Germany Built with TioCem®, which actively reduces the level of pollutants in the air We cross borders. Change the slide layout Find a choice of background Brenner Base Tunnel, Austria and Italy Building materials for what will be the world's longest underground rail tunnel. Completion 2028 We bring people together. Terminal 3, Frankfurt Airport, Germany Cement for Germany's largest construction site. Completion 2025 We connect. Change the slide layout Find a choice of background San Giorgio Bridge, Genoa, Italy 3 67,000 m of concrete for the concrete piers. Cement with approx. 40% recycling rate and lower CO2 emissions We drive innovation. 3D printed house, Beckum Less material, lower carbon footprint - thanks to HeidelbergCement Change the slide layout We combine tradition with modernity. Find a choice of background Art Museum Bourse de Commerce – Pinault Collection, Paris, France HeidelbergCements’ building materials combine the demands of a modern museum with classical architecture About HeidelbergCement Facts and Figures Strategy Beyond 2020 Sustainability Appendix: The Group areas Show guides via menu bar: View / Show / tick Guides ABOUT HEIDELBERGCEMENT HeidelbergCement: History and development Change the slide layout 1873 1889 1977 1989 1993 1995/96 1999 2001 2005/06 2007 2015 2016 1995/92021 6 Founded in 1873... …today leading market positions in aggregates, cement, -

Articles & Newsletter 2019.Xlsx

Tuesday, June 4, 2019 BUSINESS & FINANCIAL OVERVIEW European Markets Shrug Off Early Setback, Rise On Rate Cut Hopes European markets were mostly up with solid gains Tuesday afternoon, with investors betting on hopes the central banks would reduce interest rates in order to spur growth. On Monday, St. Louis Federal Reserve President James Bullard said a U.S. interest rate cut "may be warranted soon" given the rising risk to economic growth posed by global trade tensions as well as weak U.S. inflation. Across the Asia-Pacific region, Australia today reduced its key interest rate by a quarter point to historic low, aiming to create more jobs and bring inflation to target. Investors expect several other central banks across the globe to follow suit. It was a weak start for the major European markets Tuesday morning and for several others in the region. Besides reacting to corporate news and economic data, investors were also tracking news on Brexit and trade. Among the major markets, Germany was notably higher with its benchmark DAX gaining about 1% at 11,905.50, coming off an early low of 11,713.87. France's CAC 40 was up 0.23% at 5,253.50, while the U.K.'s FTSE 100 was edging up 0.15%, at 7,195.75. The pan European Stoxx 600 was up 0.2%. Switzerland, Sweden, Spain, Portugal, Italy, Austria, Belgium, Czech Republic, Ireland and Iceland are were also gaining notable ground in positive territory. In Germany, Covestro rose nearly 4%, BASF climbed up 3.7% and Continental AG gained 3.2% and Thyssenkrupp was up 3.1%. -

Eurex® IOC Liquidity Indicator

Historical Data on Demand Product: Eurex® IOC Liquidity Indicator File Description Field Format Definition DATE Current business date Date (YYYY.MM.DD) Technical instrument-identifier, see SecurityID LONG refdata-file for reference Time of calculation of the statistic VARCHAR MDStatisticTime with nanosecond time precision (HH24:MI:SS.NS) (UTC) MDStatisticID INTEGER Unique statistics identifier MDStatisticName VARCHAR Acronym for statistics MDStatisticValue VARCHAR Calculated statistics value The Eurex IOC Liquidity Indicator is provided for the following most liquid options listed on the Eurex Exchanges T7 trading system: Product code Product Category Product Name OGBS Fixed Income Options Options on Euro-Schatz Futures ODAX Index Options DAX® Options EURO STOXX 50 Index Dividend OEXD Index Options Options OESX Index Options EURO STOXX 50® Index Options OESB Index Options EURO STOXX® Banks Options OKS2 Index Options KOSPI 200 OSMI Index Options SMI® Options OVS Volatility Index Options VSTOXX Options ADS DAX Equity Options Adidas ALV DAX Equity Options Allianz BAS DAX Equity Options BASF BAY DAX Equity Options Bayer BEI DAX Equity Options Beiersdorf BMW DAX Equity Options BMW Version 1.0 CBK DAX Equity Options Commerzbank CON DAX Equity Options Continental DAI DAX Equity Options Daimler DBK DAX Equity Options Deutsche Bank DB1 DAX Equity Options Deutsche Börse DPW DAX Equity Options Deutsche Post DTE DAX Equity Options Deutsche Telekom EOA DAX Equity Options E.ON FRE DAX Equity Options Fresenius FME DAX Equity Options Fresenius Medical