Financial Sustainability Evaluation and Forecasting Using the Markov Chain: the Case of the Wine Business

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

''The Only Fault of Wine Is That There Is Always a Lack of Wine''

Ukrainian WineHub #1 at Eastern 2020 Europe rinks market! page 7 clockOnline Newspaper: Eastern news and Western trends www.drinks.uaD Christian ‘‘The only fault Wolf: ‘MUNDUS VINI feels like Oa family’ of is that wine page14 there is always a lack of wine’’ Legend of Ukraine is not Georgia, that’s true. Yes, this country is not Saracena: a cradle of wine and cannot boast of its 8-thousand-year Drink less, read more! a unique peerless history. And the history recorded in the annals is just as sad ancient dessert wine as the history of the entire Ukrainian nation: “perestroika”, a row of economic crises, criminalization of the alcohol sector. page 32 The last straw was the occupation of Crimea by Russia and the loss of production sites and unique vineyards, including autochthonous varieties. Nevertheless, the industry is alive. It produces millions of decalitres, and even showed a Steven revival in the last year. At least on a moral level t. Spurrier: Continued on page 9 “The real Judgement of Paris movie was never made” page 21 2 rinks Dclock By the glass O Azerbaijan Wines from decline to a revival The production of Azerbaijani winemakers may be compared to the Phoenix bird. Just like this mythological creature, in the 21st century, Azerbaijani wine begins to revive after almost a complete decline in the 90s, when over 130 thousand hectares of vineyards were cut out in the country not only with technical varieties but which also opens up an incredibly also with unique table varieties. vast field of activity for crossing the As a new century set in, they Pan-Caucasian and local variet- managed to breathe a new life ies. -

Cuisine Menu

• MENU • We are glad to welcome You at WHISKY CORNER! Our Scottish House is much more than just a restaurant. It is a place where friends, like-minded persons and people of good taste meet. At WHISKY CORNER, we have built for You the largest whisky collection in Eastern Europe: over 900 specimens from Scotland, Ireland, USA, Japan, Taiwan, India... As well as our own exclusive whisky releases, which are available only at our restaurant and at international festivals. WHISKY CORNER is the headquarters of Ukrainian Whisky Connoisseurs Club named after Aleksey Yakovlevich Savchenko. Thanks to this outstanding man Ukraine fell in love with whisky culture, learned the traditions and nuances of its production. Our restaurant also appeared as the result of his initiative. He inspired us with the dream of our own house for the Club — the Scottish House, where it will be so nice to taste whisky, discover new culinary pleasures, listen to a piper, enjoy the spirit of Scotland, and just to have a good time with friends. We made the dream come true! Nowadays, the ideas of the Whisky Club and the Scottish House are being kept and developed by the founder's son Aleksey Alekseevich Savchenko and his wife Irina Anatolyevna, as well as the members of the Club and the entire WHISKY CORNER team. Being in love with whisky — this noble, multifaceted drink — we have created a fine gastronomic accompaniment for it. In our menu, You will find Scottish specialties, European classics, and creative dishes. A duet of great whiskies and delicious, well-balanced meals makes the art of perfect dinning! 2 WHISKY RELEASES CRAFTED BY WHISKY CORNER Aleksey Yakovlevich Savchenko had one more dream of creating his own whisky. -

UKRAINIAN FOOD JOURNAL 2014 V.3 Is.4.Pdf

ISSN 2313-5891 (Online) ISSN 2304-974X (Print) Ukrainian Food Journal Volume 3, Issue 4 2014 Kyiv Kиїв 2014 УДК 663/664 Ukrainian Food Journal is an Ukrainian Food Journal – міжнародне international scientific journal that наукове періодичне видання для publishes innovative papers of expert in the публікації результатів досліджень fields of food science, engineering and фахівців у галузі харчової науки, техніки technology, chemistry, economics and та технології, хімії, економіки і management. управління. The advantage of research results Перевага в публікації результатів publication available to students, graduate досліджень надається студентам, students, young scientists. аспірантам та молодим вченим. Ukrainian Food Journal is abstracted and Ukrainian Food Journal індексується indexed by scientometric databases: наукометричними базами: Index Copernicus (2012) EBSCO (2013) Google Scholar (2013) UlrichsWeb (2013) Global Impact Factor (2014) CABI full text (2014) Online Library of University of Southern Denmark (2014) Directory of Research Journals Indexing (DRJI) (2014) Universal Impact Factor (2014) Directory of Open Access scholarly Resources (ROAD) (2014) European Reference Index for the Humanities and the Social Sciences (ERIH PLUS) (2014) Ukrainian Food Journal включено у перелік наукових фахових видань України з технічних наук, в якому можуть публікуватися результати дисертаційних робіт на здобуття наукових ступенів доктора і кандидата наук (Наказ Міністерства освіти і науки України № 1609 від 21.11.2013) Editorial office address: Адреса редакції: National University Національний університет of Food Technologies харчових технологій Volodymyrska str., 68 вул. Володимирська, 68 Ukraine, Kyiv 01601 Київ 01601 e-mail: [email protected] Scientific Council of the National Рекомендовано вченою радою University of Food Technologies Національного університету recommends the journal for printing. харчових технологій. -

About the Efficiency of Ukrainian Wineries

Scientific Papers Series Management, Economic Engineering in Agriculture and Rural Development Vol. 15, Issue 4, 2015 PRINT ISSN 2284-7995, E-ISSN 2285-3952 ABOUT THE EFFICIENCY OF UKRAINIAN WINERIES Anatoliy G. GONCHARUK, Natalia O. LAZAREVA International Humanitarian University, Department of Business Administration and Corporate Security, 33 Fontanskaya doroga str., Odessa 65009, Ukraine, E-mails: [email protected]; [email protected] Corresponding author: [email protected] Abstract This study highlights the dynamic, regional and structural aspects of winemaking in Ukraine. The authors identified the level of efficiency of the Ukrainian wineries using three-criteria approach. The study found that Crimean wineries are at the top of the ranking for all efficiency indicators. The study did not identify a single leader by efficiency, but it detected ineffectiveness of small business in the Ukrainian wine industry. Key words: efficiency, evaluation, ranking, Ukraine, winery INTRODUCTION 450 Winemaking is the production of wine, 400 starting from the selection of the grapes or other produce and ending with bottling of 350 finished wine. The science of wine and winemaking is known as oenology [12]. A 300 person who makes wine is traditionally called 250 a winemaker. Traditionally known as a vintner, a winemaker is a person engaged in 200 making wine. They are generally employed by 2006 2007 2008 2009 2010 2011 2012 2013 2014 wineries or wine companies. Fig.1. Grape processing in Ukraine in 2006-2014, There are all necessary conditions for the thousand tons development of wine-making in Ukraine: the land, the climate, human resources and The dynamics of wine production in Ukraine technologies. -

Ukraine and NATO: Deadlock Or Re-Start? Ukraineukraine and and NATO: NATO: Ukraine Has Over the Past Ten Years Developed a Very Close Partnership with NATO

Ukraine and NATO: Deadlock or Re-start? UkraineUkraine and and NATO: NATO: Ukraine has over the past ten years developed a very close partnership with NATO. Key areas of Deadlock or Re-start? consultation and co-operation include, for instance, peacekeeping operations, and defence and Deadlock or Re-start? security sector reform. NATO’s engagement serves two vital purposes for Ukraine. First, it enhan- Jakob Hedenskog ces Ukraine’s long-term security and serves as a guarantee for the independence of the state; and JAKOB HEDENSKOG second, it promotes and encourages democratic institutionalisation and spreading of democratic norms and values in the country. JAKOB HEDENSKOG Ukraine and NATO: Deadlock or Re-start NATO’s door for Ukraine remains open. The future development of the integration depends on Ukraine’s correspondence to the standards of NATO membership, on the determination of its political leadership, and on an effective mobilisation of public opinion on NATO membership. This report shows that Ukraine has made progress in reaching the standards for NATO membership, especially in the spheres of military contribution and interoperability. However the absence of national consensus and lack of political will and strategic management of the government hamper any effective implementation of Ukraine’s Euro-Atlantic integration. It is also crucial to neutralise Russia’s influence, which seriously hampers Ukraine’s Euro-Atlantic course. Leading representati- ves of the current leadership, especially Prime Minister Viktor Yanukovych and his Party of Regions of Ukraine, prefer for the moment continued stable relations with Russia rather than NATO mem- ? bership. Jakob Hedenskog is a security policy analyst at the Swedish Defence Re- search Agency (FOI) specialised on Ukraine. -

Euromaidan Newsletter # 339 CIVIC SECTOR of EUROMAIDAN

CIVIC SECTOR OF EUROMAIDAN 20 GRASSROOTS MOVEMENT 20 , EuroMaidan Newsletter # 339 20 - 4 Six years of MH17 lies Why are Russian hackers targeting COVID-19 vaccine laboratories? July 1 . 9 Russia urged to accept responsibility on sixth Ukraine, Canada, Sweden, Afghanistan, UK 3 anniversary of MH17 downing. demand that Iran conduct full, transparent, 3 # independent flight safety investigation into UIA The Hague vs. Russian fakes: how Dutch plane crash. prosecutors gathered evidence in the MH17 case. At least 240 arrested in Belarus protests against Six years of MH17 lies: the Kremlin is losing its barring of opposition candidates (photos, videos). own game. Why are Russian hackers targeting COVID-19 Russian arguments in The Hague: the defense vaccine laboratories? strategy of the accused in the MH17 trial. An army of trolls pushing the Russian narrative on U.S. threatens to expand sanctions on Nord Stream MH17: Who are they? 2 as Russia moves to complete pipeline. NEWSLETTER U.S. at OSCE: It's time for Russia to stop 'theater of the absurd' in peace talks with Ukraine. Left: Newspeak as editorial policy: the Kremlin goes Orwellian on Orwell Right: “We’re against the Putin regime!” Fifth day of protests in Russia’s Far Eastern city of Khabarovsk Russia is preparing for new war What does 30 UAH/USD exchange rate mean for inflation? The gathering autumn clouds. Perceptions of #KremlinNarratives: Andrii Palchevsky on weakness drive the Kremlin’s hybrid aggression external governance. against America and Ukraine to new heights. The Kremlin’s new take on Colour Revolutions. Russia is preparing for new war, just like it was in What does 30 UAH/USD exchange rate mean for Georgia in 2008 or Ukraine in 2014. -

A Parentage Study of Closely Related Ukrainian Wine Grape Varieties

УДК 634.85:631.526.32:577.21(477) Introduction. The south of Ukraine has a long S. GORYSLAVETS 1, V. RISOVANNA 1, R. BACILIERI 2, standing tradition of growing table and wine grape J.F. HAUSMAN 3, M. HEUERTZ 3, 4, 5 * varieties. The latter are made into wines distin guished for their excellent quality. Recently, new 1 National Institute for Vine and Wine «Magarach»; Ampelography, Breeding and Genetics of Grapevine, Yalta, Ukraine wine grapes produced by generative breeding are Email: [email protected] being introduced into commercial cultivation. 2 Institut National de la Recherche Agronomique, Centre INRA de This helps improving and enlarging the countryґs Montpellier 2 Place Viala, 34000 Montpellier, France wine grape assortment since such varieties have 3 Centre de Recherche PublicGabriel Lippmann; Environment and better economical characters. Four newlybred AgroBiotechnology; rue du Brill 41; L4422 Belvaux, Luxembourg promising vintage varieties are the focus of this 4 Université Libre de Bruxelles; Evolutionary and Ecology cp160/12; av. F.D. Roosevelt 50; B1050 Brussels, Belgium paper: ‘Rubin Golodrigi’, bred in 1974 and 5 Centre of Forest Research CIFORINIA; Forest Systems and Resources; released by the Research Company «Ampelos»; ctra. de la Coruña km 7.5; E28040 Madrid, Spain ‘Rubinovyi Magaracha’, ‘Antey Magarachskii’, A PARENTAGE STUDY OF CLOSELY and ‘Granatovyi Magaracha’ were bred, respec tively, in 1928, 1971 and 1982 and released by the RELATED UKRAINIAN WINE GRAPE National Institute for Vine and Wine «Magarach». VARIETIES USING MICROSATELLITE These varieties are highly resistant to diseases and can be elaborated into table and dessert wines. MARKERS They have started to be widely grown in Russia and in Ukraine. -

State and Development Prospects of Viticulture and Wine-Making Objective

UDC 634.833.38.109.733.38. 109.84 © 2015 V.V. Vlasov, Corresponding Member of NAAS, doctor of agricultural sciences I.V. Belous, candidate of economic sciences NSC "Institute of viticulture and winemaking named after V.E. Tayirova State and development prospects of viticulture and wine-making Objective. Definition of strategic guidelines for the development of the wine-growing and wine-growing subcomplex on the basis of the introduction of an innovative model of industry development. Methods. Statistical groupings, graphical and qualitative, correlation-regression analysis. Results The main principles of strategic development are: creation of favorable conditions for the integration of industries into the world economic space; Growth of socio-economic well-being of society; Formation of scientifically grounded and socially oriented innovative model of structural modernization of viticulture and winemaking. Conclusions For the further effective development of viticulture and winemaking, technical and technological re-equipment and organizational and economic provision of wine-growing, seedling and winemaking enterprises should be carried out according to modern world standards. Key words: strategy, viticulture and winemaking, modern state, prospects of development. In today's globalized world, the place and role of viticulture and winemaking in Ukraine depend on the ability to effectively realize its objective advantages of the resource-resource potential in the global division of labor and international competition. With the accession of Ukraine to the WTO (2008), viticulture and winemaking were in conditions of perfect market competition, which led to the restriction of state protectionism of national producers, most of which proved to be of low competitiveness. Due to the non-conformity of national quality standards of European products, the inability to meet the technical, sanitary and phytosanitary conditions for the export of their products of national commodity producers has actually been eliminated from trade on the world market. -

Wine from Ethiopia, Ukraine . . . Where Next? | Financial Times

4-5-2021 Wine from Ethiopia, Ukraine . where next? | Financial Times FT Magazine Wine Wine from Ethiopia, Ukraine . where next? ‘Every time I encounter a new wine-producing region or country, I see it as proof of how widely my wonder and excitement are shared’ Jancis Robinson MAY 1 2021 The most admired classic wines are great but, heavens, life would be boring if they were the only wines available. I love making discoveries. Unfamiliar names remind me just how miraculous it is that the fermented juice of a single fruit can offer such variety and stimulation. Every time I encounter a new wine-producing region or country, I see it as proof of how widely my wonder and excitement are shared. I had heard that Ethiopia (along with at least another 11 African countries) produced wine but had never tasted it until someone, who seemed to be a coffee trader judging by his email address, offered to send me some last month. Six bottles of Rift Valley wine eventually made their way through the obstacle course that wine samples have to navigate post-Brexit. They were all made from familiar international grape varieties, which somewhat diminished their mystique, but the fact that two of them carried no vintage year, while the rest were labelled 2018 and seemed rather younger than that, was certainly unusual. As was the odour of dirty dishcloths I picked up on one or two of the reds. But the two Ethiopian Chardonnays were excellent by any measure. They all come from an operation run by Castel, which established vineyards and a winery south of Addis Ababa in 2007. -

Research of Factors That Influence the Trademark Policy of an Enterprise

Економіка підприємств: ISSN 2226-3780 Економіка та управління підприємством 11. Demianenko, M. Ya. Finansovyi slovnyk-dovidnyk [Text] / 22. Lynovytska, O. Universytetski reitynhy, yak nevidiemna skla- M. Ya. Demianenko, Yu. Ya. Luzan, P. T. Sabluk, V. M. Skupyi dova intehratsiinykh protsesiv v ekonomitsi i suspilstvi rotsi et al.; ed. by M. Ya. Demianenka. – Kyiv: IAE UAAN, 2003. – [Electronic resource] / O. Lynovytska // HO Tsentr mizhn- 555 p. arodnykh proektiv «Yevroosvita». – May 27, 2016. – Avail- 12. Donets, L. I. Ekonomichni ryzyky ta metody yikh vymiriuvannia able at: \www/URL: http://www.euroosvita.net/index.php/ [Text]: Handbook / L. I. Donets. – Kyiv: TsUL, 2006. – 312 p. ?category=1&id=4757 13. Morgan, J. Р. Risk Metrics–Technical Document [Electronic re- 23. Peremishcheni VNZ: try roky na novomu mistsi [Electronic source] / J. Р. Morgan. – New York, 1996. – Available at: \www/ resource] / Vyshcha osvita. – December 19, 2016. – Available at: \www/URL: http://vnz.org.ua/statti/9793-peremischenni- URL: https://www.msci.com/documents/10199/5915b101-4206- vnz-try-roky-na-novomu-mistsi 4ba0-aee2-3449d5c7e95a 24. Breus, S. V. Vykorystannia zbalansovanoi systemy pokaznykiv u 14. Smeliantsev, A. P. Problema zahroz interesam bezpeky Ukrainy diialnosti vyshchykh navchalnykh zakladiv [Text] / S. V. Breus, (sotsialno-filosofskyi analiz) [Text]: Abstract’s PhD thesis / Ye. B. Khaustova // Aktualni problemy ekonomiky. – 2016. – A. P. Smeliantsev. – Kharkiv, 2001. – 18 p. No. 9 (183). – P. 109–116. 15. Liashenko, O. M. Kontseptualizatsiia upravlinnia ekonomichnoiu bezpekoiu pidpryiemstva [Text]: Monograph / O. M. Liashenko. – исслЕдованиЕ риска в дЕятЕльности высШиХ учЕБных Luhansk: SNU im. V. Dalia, 2011. – 400 p. ЗавЕдЕний в контЕкстЕ оБЕспЕчЕния иХ экономичЕской 16. Kozhenevski, L. -

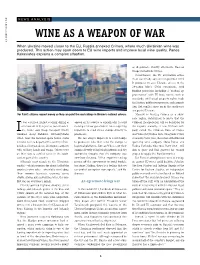

Wine As a Weapon Of

NEWS ANALYSIS UKRAINE WINE AS A WEAPON OF WAR 5/14 MEININGER’S WBI 5/14 MEININGER’S When Ukraine moved closer to the EU, Russia annexed Crimea, where much Ukrainian wine was produced. This action may open doors to EU wine imports and improve local wine quality. Panos Kakaviatos explains a complex situation. as illegitimate. Shortly afterwards, Russian troops moved into Crimea. Nevertheless, the EU association agree- ment was finally agreed in September 2014. It promises to give Ukraine access to the 28-nation bloc’s 500m consumers, with binding provisions including a “gradual ap- proximation” with EU trade norms, such as standards, intellectual property rights, trade facilitation, public procurement, and competi- tion. But conflict rages on in the south-east- ern part of Ukraine. ‘For Paint’: citizens request money so they can paint the road railings in Ukraine’s national colours. Moscow is treating Crimea as a show- case region, determined to prove that the t was a surreal August evening, dining at appeal on its website to explain why it could Crimean incorporation will be beneficial for a restaurant in Kyiv just as rocket launch- no longer follow government rules requiring the region’s economy. A new Crimean com- Iers, tanks and troop transport trucks importers to send excise stamps directly to pany called the Crimean Buro of Grapes rumbled along Bohdana Khmelnytskoho producers. and Wine (Krymskoe buro vinograda i vina) street, near the national opera house. Some The law obliges importers to send stamps created by Boris Titov, the owner of the Russian vehicles were to be part of the country’s Inde- to producers who then send the stamps to sparkling wine company Abrau-Durso, and pendence Day parade on 24 August, complete logistical platforms. -

Wine & Winemaking

XII InternatIonal SPecIalIzed eXhIbItIonS WIne & WInemakIng general Partner HIgH Degree Salon of CHampagne anD SparklIng WIneS Salon of CognaC general Partner of the SalonS offIcIal catalogue february 23-25, 2012 odeSSa / concert & eXhIbItIon hall of the odeSSa Sea trade Port organIzer SPecIal thankS to Ministry of Economical development and trade of Ukraine Ministry of Agrarian policy and food of Ukraine Antitrust committee of Ukraine Odessa Region State Administration National scientific centre - Tairov Wine Growing and Winemaking Institute of NAAS Magarach Grapes and Wine National Institute of Ukrainian Academy of Agrarian Science NAAS Odessa National Academy of Food Technologies Wine Tasting Commission Odessa 93 23-25.02.2012 Dear participants and visitors! I sincerely congratulate you on the opening of XII International Specialized exhibitions “Wine and Wine making“ and “High degree»! «Wine and Winemaking» and «High degree» exhibitions has traditionally been a meeting place for producers, distributors and consumers, as well as companies engaged in the development and introduction of new technologies for the production of wine and spirits. Every year in our country is growing the quality and range of wine products, along with famous brands new brands appear. Ukrainian producers of wines and spirits harmoniously combine favorable soil and climatic conditions in their regions, traditions and modern technologies, creating a full cycle production, introducing new equipment. It is so nice that among the exhibitors are not only the companies that create high-quality alcoholic beverages and develop the distribution system, but there are also producers of modern equipment, materials, packaging, grapes from Ukraine and abroad The extensive program of the events is one of the components, which makes the exhibitions «Wine and Winemaking» and «High degree» successful.