Financial Year 2018-19

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

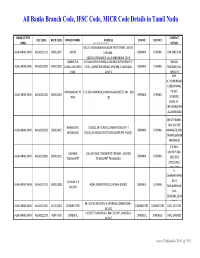

Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu

All Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu NAME OF THE CONTACT IFSC CODE MICR CODE BRANCH NAME ADDRESS CENTRE DISTRICT BANK www.Padasalai.Net DETAILS NO.19, PADMANABHA NAGAR FIRST STREET, ADYAR, ALLAHABAD BANK ALLA0211103 600010007 ADYAR CHENNAI - CHENNAI CHENNAI 044 24917036 600020,[email protected] AMBATTUR VIJAYALAKSHMIPURAM, 4A MURUGAPPA READY ST. BALRAJ, ALLAHABAD BANK ALLA0211909 600010012 VIJAYALAKSHMIPU EXTN., AMBATTUR VENKATAPURAM, TAMILNADU CHENNAI CHENNAI SHANKAR,044- RAM 600053 28546272 SHRI. N.CHANDRAMO ULEESWARAN, ANNANAGAR,CHE E-4, 3RD MAIN ROAD,ANNANAGAR (WEST),PIN - 600 PH NO : ALLAHABAD BANK ALLA0211042 600010004 CHENNAI CHENNAI NNAI 102 26263882, EMAIL ID : CHEANNA@CHE .ALLAHABADBA NK.CO.IN MR.ATHIRAMIL AKU K (CHIEF BANGALORE 1540/22,39 E-CROSS,22 MAIN ROAD,4TH T ALLAHABAD BANK ALLA0211819 560010005 CHENNAI CHENNAI MANAGER), MR. JAYANAGAR BLOCK,JAYANAGAR DIST-BANGLAORE,PIN- 560041 SWAINE(SENIOR MANAGER) C N RAVI, CHENNAI 144 GA ROAD,TONDIARPET CHENNAI - 600 081 MURTHY,044- ALLAHABAD BANK ALLA0211881 600010011 CHENNAI CHENNAI TONDIARPET TONDIARPET TAMILNADU 28522093 /28513081 / 28411083 S. SWAMINATHAN CHENNAI V P ,DR. K. ALLAHABAD BANK ALLA0211291 600010008 40/41,MOUNT ROAD,CHENNAI-600002 CHENNAI CHENNAI COLONY TAMINARASAN, 044- 28585641,2854 9262 98, MECRICAR ROAD, R.S.PURAM, COIMBATORE - ALLAHABAD BANK ALLA0210384 641010002 COIIMBATORE COIMBATORE COIMBOTORE 0422 2472333 641002 H1/H2 57 MAIN ROAD, RM COLONY , DINDIGUL- ALLAHABAD BANK ALLA0212319 NON MICR DINDIGUL DINDIGUL DINDIGUL -

Beyond the Tsunami

Beyond the Tsunami Current Status of Mangroves in Kerala and Tamil Nadu, India, with regard to Vegetation, Community Perceptions and Policy 2008 Nibedita Mukherjee, Farid Dahdouh-Guebas The Coastal and Marine Programme at ATREE and Kartik Shanker is interdisciplinary in its approach and applies skills in the natural and social sciences to its United Nations Team for Ashoka Trust for Research in Tsunami Recovery Support Ecology and the Environment research and conservation interventions. Beyond the Tsunami Current Status of Mangroves in Kerala and Tamil Nadu, India with regard to Vegetation, Community Perceptions and Policy Nibedita Mukherjee, Farid Dahdouh-Guebas and Kartik Shanker United Nations Team for Tsunami Recovery Support Author details: Kartik Shanker Adjunct Fellow, Ashoka Trust for Research in Ecology and the Environment (ATREE) 659, 5th Main Road, Hebbal, Bangalore 560092. India. and Assistant Professor, Centre for Ecological Sciences, Indian Institute of Science, Bangalore 560012. India. E-mail: [email protected] Nibedita Mukherjee Research Associate, Ashoka Trust for Research in Ecology and the Environment (ATREE) 659, 5th Main Road, Hebbal, Bangalore 560092. India. and PhD Student, Plant Biology and Nature Management (APNA), Vrije Universiteit Brussel – VUB, Pleinlaan, B-1050 Brussels, Belgium. E-mail: [email protected] Farid Dahdouh-Guebas Complexity and Dynamics of Tropical Systems, Université Libre deBruxelles – ULB, Av. F.D. Roosevelt 50, B-1050 Brussels, Belgium. E-mail: [email protected] Acknowledgements We would like to thank the United Nations Development Programme for funding this initiative. We would also like to thank the Forest Department of Kerala, Andhra Pradesh and Tamil Nadu for helping in the completion of this project. -

Updtd-Excel List of Doctors-2020.Xlsx

State / UT wise List of Doctors / Institution, authorised to issue Compulsory Health Certificate (for Shri Amarnathji Yatra 2020) Tamil Nadu Resident Medical Officers of the Medical College Hospitals under the control of Director of Medical Education,Chennai, Tamil Nadu mentioned below have been authorised to issue Compulory Health Certificate for the pilgrims of Shri Amarnathji Yqatra 2020 S.No District District Hospital Name of the Residential Phone / Mobile Medical Officer 1 Chennai Rajiv Gandhi Govt. Gen. Dr.Thirunavukkarasu S.K 9445030800 Hospital, Chennai 2 Govt. Stanley Hospital, Dr. Ramesh .M 98417-36989 Chennai 3 Kilpauk Medical College Dr. S. Rajakumar S 98842-26062 Hospital, Chennai 4 Institute of Mental Dr.Sumathi.S (I/C) 9677093145 Health, Chennai. 5 ISO &Govt.Kasturbna Dr.Elangovan S V 9840716412 Gandhi Hospital for Women & Children Chenai 6 Institute of Obstetrics Dr.Fatima (I/C) 7845500129 and Gyanecology and Govt.Hospital for Women & Children Chenai 7 Govt.Royapeetah Dr.Ananda Pratap M 9840053614 Hospital, Chennai 8 Institute of ChildHealth, Dr.Venkatesan (I/C) 8825540529 & Hospital for Children,Chennai-8 9 RIO & Govt. Opthalmic Dr.Senthil B 9381041296 Hospital, Chennai-8 10 Chengalpattu Chengalpattu Medical Dr. Valliarasi (I/c) 9944337807 College & Hospital,, Chengalpattu 11 thanjavur Thanjavur Medical Dr. Selvam 9443866578 , 9789382751 College & Hospital. thanjavur 12 Madurai Goverment Rajaji Dr. Sreelatha A. 9994793321 Hospital, Madurai 13 Coimbatore Coimbatore Medical Dr.Soundravel R 9842246171 College & Hospital 14 Salem Govt. Mohan Dr. Rani 9443246286 Kumaramangalam Medical College Hospital, Salem 15 Tirunelveli Tirunelveli Medical Dr. Shyam Sunder Singh N 9965580770 College & Hospital 16 Trichy Mahatma Gandhi Dr.Chandran (I/C) 9043500045 Memorial & Hospital, Trichy 17 Tuticorin Thoothukudi Medical Dr.Silesh Jayamani 9865131079 College & Hospital, Thoothukudi 18 Kanya kumari Govt. -

Study Report on Gaja Cyclone 2018 Study Report on Gaja Cyclone 2018

Study Report on Gaja Cyclone 2018 Study Report on Gaja Cyclone 2018 A publication of: National Disaster Management Authority Ministry of Home Affairs Government of India NDMA Bhawan A-1, Safdarjung Enclave New Delhi - 110029 September 2019 Study Report on Gaja Cyclone 2018 National Disaster Management Authority Ministry of Home Affairs Government of India Table of Content Sl No. Subject Page Number Foreword vii Acknowledgement ix Executive Summary xi Chapter 1 Introduction 1 Chapter 2 Cyclone Gaja 13 Chapter 3 Preparedness 19 Chapter 4 Impact of the Cyclone Gaja 33 Chapter 5 Response 37 Chapter 6 Analysis of Cyclone Gaja 43 Chapter 7 Best Practices 51 Chapter 8 Lessons Learnt & Recommendations 55 References 59 jk"Vªh; vkink izca/u izkf/dj.k National Disaster Management Authority Hkkjr ljdkj Government of India FOREWORD In India, tropical cyclones are one of the common hydro-meteorological hazards. Owing to its long coastline, high density of population and large number of urban centers along the coast, tropical cyclones over the time are having a greater impact on the community and damage the infrastructure. Secondly, the climate change is warming up oceans to increase both the intensity and frequency of cyclones. Hence, it is important to garner all the information and critically assess the impact and manangement of the cyclones. Cyclone Gaja was one of the major cyclones to hit the Tamil Nadu coast in November 2018. It lfeft a devastating tale of destruction on the cyclone path damaging houses, critical infrastructure for essential services, uprooting trees, affecting livelihoods etc in its trail. However, the loss of life was limited. -

Enhancing Climate Resilience of India's Coastal Communities

Annex II – Feasibility Study GREEN CLIMATE FUND FUNDING PROPOSAL I Enhancing climate resilience of India’s coastal communities Feasibility Study February 2017 ENHANCING CLIMATE RESILIENCE OF INDIA’S COASTAL COMMUNITIES Table of contents Acronym and abbreviations list ................................................................................................................................ 1 Foreword ................................................................................................................................................................. 4 Executive summary ................................................................................................................................................. 6 1. Introduction ............................................................................................................................................... 13 2. Climate risk profile of India ....................................................................................................................... 14 2.1. Country background ............................................................................................................................. 14 2.2. Incomes and poverty ............................................................................................................................ 15 2.3. Climate of India .................................................................................................................................... 16 2.4. Water resources, forests, agriculture -

Annexure III List of Backward Blocks in the State Coimbatore District 1 Annur 4 Pongalur 2 Gudimangalam 5 Sultanpet 3 Kinathukad

Annexure III List of Backward Blocks in the State Coimbatore District 1 Annur 4 Pongalur 2 Gudimangalam 5 Sultanpet 3 Kinathukadavu Cuddalore District 6 Annagramam 11 Mangalore 7 Kammapuram 12 Melbhuvanagiri 8 Kattumannarkoil 13 Nallur 9 Kumaratchi 14 Parangipettai (Portonovo) 10 Kurinjipadi Dharmapuri District 15 Harur 19 Palacode 16 Karimangalam 20 Pappireddipatti 17 Morappur 21 Pennagaram 18 Nallampalli Dindigul District 22 Guziliamparai 27 Shanarpatti 23 Natham 28 Thoppampatti 24 Nilakottai 29 Vadamadurai 25 Oddenchatram 30 Vedasandur 26 Reddiarchatram Erode District 31 Anthiyur 32 Kundadam 33 Thalavadi Kancheepuram District 34 Acharappakkam 38 Madurantagam 35 Chithamur 39 Thirukazhukundram 36 Kundrathur 40 Uthiramerur 37 Lathur 41 Walajabad Kanyakumari District 42 Rajakkamangalam 43 Thiruattar 44 Thovalai 36 Karur District 45 Aravakurichi 48 Krishnarayapuram 46 K.Paramathi 49 Thanthoni 47 Kadavur 50 Thogamalai Krishnagiri District 51 Bargur 55 Sulagiri 52 Kaveripattinam 56 Thally 53 Kelamangalam 57 Uthangarai 54 Mathur 58 Veppanapalli Madurai District 59 Alanganallur 65 T.Kallupatti 60 Chellampatti 66 Thirumangalam 61 Kalligudi 67 Thirupparankundram 62 Kottampatti 68 Usilampatti 63 Madurai East 69 Vadipatti 64 Sedapatti Nagapattinam District 70 Keelaiyoor 75 Sirkalai 71 Kelvalur 76 Talainayar 72 kollidam 77 Thirumarugal 73 Kuttalam 78 Vedaraniyam 74 Sembanar koil Namakkal District 79 Elachipalayam 84 Mohanur 80 Erumaipatti 85 Namagiripettai 81 Kabilarmalai 86 Puduchatram 82 Kollihills 87 Vennandur 83 Mallasamudram Nilgiris District -

Seasonal Behavior of a Shallow Estuary of the Lower Cauvery Basin, India

Aplinkos tyrimai, inžinerija ir vadyba, 2012. Nr. 3(61), P. 6-13 ISSN 1392-1649 (print) Environmental Research, Engineering and Management, 2012. No. 3(61), P. 6-13 ISSN 2029-2139 (online) http://erem.ktu.lt Seasonal Behavior of a Shallow Estuary of the Lower Cauvery Basin, India K.L. Priya, P. Jegathambal and E. J. James Karunya University, Coimbatore http://dx.doi.org/10.5755/j01.erem.61.3.2041 (received in July 2012, accepted in September, 2012) The effect of bifurcation at the estuary mouth was studied on the measurements of salinity, current and tidal depth in a shallow estuary during spring and neap tides of two different seasons. There was a considerable variation of salinity at the observed stations during the seasons. At the shallowest location of the estuary, salinity, as high as 37 ppt, was observed during the period of zero fresh water discharge. The flushing time of the estuary was higher at its western side compared to the eastern one. The diffusion coefficient was reached by using an advection-diffusion equation. The estuary was classified using a circulation/stratification diagram. Well mixed conditions persisted during pre monsoon and post monsoon in the Muthupet estuary. Keywords: Salinity, shallow estuary, bifurcating mouth, flushing time, diffusion coefficient, estuarine classification. 1. Introduction In estuaries chemical, geological and biological side in the Vashishti estuary. Jyothi et.al. 2000 transfers are dependent on their physical processes. observed seasonal fluctuation in the flushing time Major processes such as mixing, circulation and mainly due to the variation in the fresh water flow and transfer of materials are controlled by riverine fresh topography of the Gauthami Godavari estuary. -

Spatio-Temporal Analysis of Muthupet Lagoon Using Geomatics Techniques

Indian Journal of Geo Marine Sciences Vol.46 (01), January 2017, pp.74-77 Spatio-Temporal Analysis of Muthupet Lagoon Using Geomatics Techniques Balasaraswathi, P & Srinivasalu, S. Institute for ocean management, Anna University, Chennai-600 0025, India [E-mail: [email protected].] Received: 11 December 2015; revised: 30 October 2016 Present study consists the spatio-temporal analysis of the stored information, using a Toposheet of 1970 as a reference surface. A drastic increase of the surface area of the lagoon has been observed between the years 1970 and 1991 (from 12.82 to 18.49km2 of the lagoon reference surface. While there was no sand bar found in lagoon (1970), the presence of mud flats were identified in the year 1991 and started increasing, reached its maximum areal extent (0.56km2) in 2015. Analysis result deterioration in the width of the lagoon mouth from 1.03km, 1991 to 0.80km, 2015. [Keywords: Coastal lagoons, Geomatics, surface area, sand bars, spatio-temporal behavior] Introduction Imager) data products were available. For Wetlands, due to the ecological and economic handling the temporal dimension of the data, data significance to the society have become the target management tool in ArcGIS 10.2.1 is used. for much of the environmental dynamics that have come wide-spread this century as a by-product of anthropogenic activities. The studies about the changes of wetlands are highly essential for conservation, preservation of this unique resource. Remote sensing and geographical information system (GIS) have been shown essential tools for analyzing the nature and behavior of wetlands (1-3). -

A Feasibility Study on Use of Air Ambulance on East Coast Road

Int. J. Chem. Sci.: 14(4), 2016, 3064-3072 ISSN 0972-768X www.sadgurupublications.com A FEASIBILITY STUDY ON USE OF AIR AMBULANCE ON EAST COAST ROAD P. R. KALYANA CHAKRAVARTHY*, R. JANANI and S. CHEZHIYAN Department of Civil Engineering, Vels University, CHENNAI – 600117 (T.N.) INDIA ABSTRACT Everyone knows the importance of technological development happening day to day in the world. Air transport is one among them. This Air mode of transport has been effectively used by people to save time and cater the needs in long travel distances. As air transport reduces the travel time. It can be used as air ambulance to save life’s occurring due to road traffic accidents. Helipads are important for air ambulance by accepting and taking care of patients from remote areas without local hospitals or facilities. The feasibility of Air ambulance in East coast road is discussed in this study. Key words: Air ambulance, East coast road. INTRODUCTION The aim of this study is to analyze the Feasibility of using air ambulances for emergency operations during road traffic accidents (RTAs) to reduce the fatalities. During past two decades it has been observed that the RTAs has been increased and leads the list for causing death. Hence it is proposed to use air ambulances in order to reduce the death rate in road traffic accidents. Air ambulance services provides quick transportation and immediate first aid facility for the affected patients which is very much essential for life saving operations Air ambulance Air ambulance services are a critical component of the provincial health care system, providing Emergency life saving treatment and transporting patients across vast distances to the necessary level of care. -

Estimation of the Temporal Change in Carbon Stock of Muthupet Mangroves in Tamil Nadu Using Remote Sensing Techniques

Journal of Geography, Environment and Earth Science International 19(4): 1-7, 2019; Article no.JGEESI.47433 ISSN: 2454-7352 Estimation of the Temporal Change in Carbon Stock of Muthupet Mangroves in Tamil Nadu Using Remote Sensing Techniques K. Narmada1* and K. Annaidasan2 1Centre for Water Resources Management, University of Madras, Chennai, India. 2Department of Geography, Central University of Tamil Nadu, Thiruvarur, India. Authors’ contributions This work was carried out in collaboration between the two authors. Author KN designed the study, performed the statistical analysis, wrote the protocol and wrote the first draft of the manuscript. Author KA prepared the maps and managed the literature searches. Both the authors read and approved the final manuscript. Article Information DOI: 10.9734/JGEESI/2019/v19i430096 Editor(s): (1) Dr. Ojeh Vincent Nduka, Department of Geography, Taraba State University, Jalingo, Nigeria. (2) Dr. Jude Ndzifon Kimengsi, Department of Geography and Environmental Studies, Catholic University of Cameroon (CATUC), P.O. Box 782, Bamenda, Cameroon. Reviewers: (1) Paul Kweku Tandoh, KNUST- Kumasi, Ghana. (2) Bharat Raj Singh, Dr. APJ Abdul Kalam Technical University, India. Complete Peer review History: http://www.sdiarticle3.com/review-history/47433 Received 02 December 2018 Accepted 16 February 2019 Original Research Article Published 16 March 2019 ABSTRACT Aim: To study the carbon storage potential of Muthupet mangroves in Tamil Nadu using Remote sensing techniques. Place and Duration: The study is carried out in Muthupet Mangroves for the years 2000, 2010 and 2017. Methodology: In this study the remote sensing images were processed using the ERDAS and ArcGIS software and the NDVI (Normalized Difference Vegetation Index) has also been applied to estimate the quantity of carbon sequestration capability for the Avicennia marina mangrove growing in the Muthupet region for the period 2000-2017. -

Mangroves of Tamil Nadu: a Literature Review

© 2018 JETIR May 2018, Volume 5, Issue 5 www.jetir.org (ISSN-2349-5162) Mangroves of Tamil Nadu: A Literature Review T. J. Mahathalana and S. Jeeva Department of Botany, Scott Christian College (Autonomous), Nagercoil - 629 003 (Affiliated to Manonmaniam Sundaranar University, Tirunelveli), Tamil Nadu, India. Abstract Mangroves are a diverse group of salt-tolerant, mostly arboreal, flowering plants. They are primarily tropical and subtropical in distribution, and are generally more along the coastlines of the east than on the west of the continents. In India, mangroves are found along the coastline of nine states and four Union Territories, 70% on the east coast, 12% on the west coast and 18% on the Bay Islands. Indian mangroves have recorded 46 true mangrove species belonging to 14 families and 22 genera, 42 species and 4 natural hybrids. Of these, 16 mangroves belonging to 11 genera and 9 families have been recorded along the Tamil Nadu coast. Mangrove habitats are now threatened by various factors such as reduction in freshwater flow, marine and coastal pollution, siltation, sedimentation and excessive salinity. Key words: Mangroves, Distribution, habitats, pollution, siltation, sedimentation. Introduction Mangroves are salt-tolerant forest ecosystems distributed mainly in tropical and subtropical inter-tidal regions of the world. They are one of the most productive ecosystems on Earth with a mean production of 2.5 g C m-2 day-1 (Jennerjahn and Ittekkot, 2002). The combination of shallow waters, high level of nutrients, and high primary productivity makes these areas ideal for supporting intricate food webs in several environmental settings (Twilley and Rivera-Monroy, 2005). -

Mangrove Plants of Tamil Nadu

Mangrove Plants of Tamil Nadu Y. Selvam P. Eganathan Y.M. Karunagaran T. Ravishankar R. Ramasubramanian ,. < ~~ \ For Display J ~~~. __._-- M.S. Swaminathan Research Foundation Mangrove Plants of Tamil Nadu V. Selvam P. Eganathan V.M. Karunagaran T. Ravishankar R. Ramasubramanian M.S. Swaminathan Research Foundation Chennai M.S. Swaminathan Research Foundation 3rd Cross Street, Institutional Area Taramani, Chennai - 600 113 India. Tele + 91 44 2254 1229; 2254 1698 Fax + 9 1 44 2254 1319 E-mail: msswami @mssrf.res.in executi [email protected] vsel vam45 @hotmail.com MSSRF / MA / 04 /18 October 2004 This Orientation Guide was prepared with the generous support of the India-Canada Environment Facility, New Delhi 2 Preface The present publication on the Mangrove plants of Tamil Nadu is a timely publication, since there is growing public and political awareness of the importance of mangrove wetlands in preserving the ecological security of coastal areas and the livelihood security of coastal communities. The publication has been prepared in a user-friendly manner, particularly for the benefit of scholars and extension workers. An understanding of the facts mentioned in the publication will facilitate effective joint mangrove forest management by forest departments and local communities. The book will help to sensitize all concerned about the rich biodiversity associated with mangrove ecosystems. I hope it will be widely used by members of forest departments, scholars and students and by all interested in the conservation and sustainable and equitable management of mangrove bio-resources. M S Swaminathan 3 Content 1.0 Introduction 5 2.0 Mangrove Plants of India 8 3.0 Mangrove Plants of Tamil Nadu 11 4.0 About this manual 12 5.0 True mangrove species of Tamil Nadu 18 Acantlzus ilicifolius Aegiceras comiculatum Avicennia marina Avicennia officinalis Bruguiera cylindrica Ceriops decandra Ceriops tagal Excoecaria agallocha Lumnitzera racemosa Pemplzis acidula Rhizoplzora apiclliata Rlzizoplzora mllcronata Rlzizophora sp.