Audit Report on the Accounts of District Government Toba Tek Singh Audit Year 2016-17

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Electoral Politics in Pakistan: a Case Study of NA-94 Abstract

Abdul Qadir Mushtaq1 Muhammad Ibrahim2 Electoral Politics In Pakistan: A Case Study of NA-94 Abstract: This constituency consists of Kamalia, Pirmahal and its sournding villages. Before 1985 elections, it was the part of district Faisalabad but before 1985, Zia regime decided to establish new district Toba Tek Singh. Kamalia is the Tehsil head quater of T. T. singh but its area has been divided into two constituencies. Few villages fall in NA and other villages are situated in NA. 94. The major bridaries of this constituency are, Syed, Arian, Jutt, Rajput, Rajput Bhatti, Kharals, Fityyana. Before 1985, the main leadership was in the hands of Syeds. Two different groups existed among them; one was leading Syed Nasir Deen Shah and second was under the control of Makhdoom Nazir Deen shah. These two groups ruled over district council Faisalabad for many years. Zia regime tried to dismental its influence and decided to divide the follwers of these two groups onto different districts. Few villages of their followers had been given in district Jaranwala, few were given in district Faisalabad and few came in the vicinity of district Toba Teksingh. In this way, the power of the Syed family came to an end. Now in the existing set up, the leadership is in the hands of three major families i.e. Syed, Arian and Fatiana. This paper presents the historical background of the electoral politics and role of bradrise in the victory of the candidates. Introduction Kamalia is a Tehsil of Toba Tek Singh District which is situated in Punjab, Pakistan. -

Branches of Ubl to Collect Board's Dues

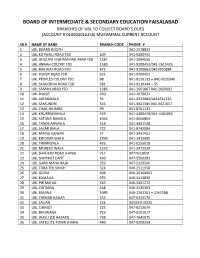

BOARD OF INTERMEDIATE & SECONDARY EDUCATION FAISALABAD BRANCHES OF UBL TO COLLECT BOARD’S DUES (ACCOUNT # 010901016256) MUKAMMAL CURRENT ACCOUNT SR.# NAME OF BANK BRANCH CODE PHONE. # 1 UBL BOARD BOOTH - 041-2578833 2 UBL KOTWALI ROAD FSD 109 041-9200453 3 UBL GHULAM MUHAMMAD ABAD FSD 1287 041-2694655 4 UBL JINNAH COLONY FSD 1580 041-9200452/041-2615425 5 UBL RAILWAY ROAD FSD 472 041-9200662/0419200884 6 UBL DIJKOT ROAD FSD 531 041-9200451 7 UBL PEOPLES COLONY FSD 98 041-9220133 – 041-9220346 8 UBL SARGODHA ROAD FSD 581 041-9210344 – 35 9 UBL SAMAN ABAD FSD 1286 041-2661867 041-2660092 10 UBL DIJKOT 260 041-2670031 11 UBL JARANWALA 36 041-4312983/0414311126 12 UBL SAMUNDRI 326 041-3421585 041-3421657 13 UBL CHAK JHUMRA 99 041-8761131 14 UBL KHURRIANWALA 429 041-4360429/041-4364050 15 UBL SATANA BANGLA 1066 041-4600804 16 UBL TANDLIANWALA 518 041-3441548 17 UBL SALAR WALA 722 041-8742084 18 UBL MAMU KANJAN 37 041-3431452 19 UBL KHIDDAR WALA 1590 041-3413005 20 UBL THIKRIWALA 433 041-0255018 21 UBL MUREED WALA 1332 041-3472529 22 UBL SHAHEED ROAD JHANG 217 0477613829 23 UBL SHORKOT CANT 430 047-5500281 24 UBL GARH MAHA RAJA 359 047-5320506 25 UBL TOBA TEK SINGH 324 046-2511958 26 UBL GOJRA 404 046-35160062 27 UBL KAMALIA 970 046-3413830 28 UBL PIR MAHAL 545 046-3361272 29 UBL CHITIANA 668 046-2545363 30 UBL RAJANA 1093 046-2262201 – 2261588 31 UBL CHENAB NAGAR 153 047-6334576 32 UBL LALIAN 154 04533-610225 33 UBL CHINIOT 225 047-6213676 34 UBL BHOWANA 726 047-6201017 35 UBL WASU (18 HAZARI) 738 047-7645075 36 UBL SATELLITE TOWN JHANG 440 047-9200254 BOARD OF INTERMEDIATE & SECONDARY EDUCATION FAISALABAD BRANCHES OF MCB TO COLLECT BOARD’S DUES (ACCOUNT # (0485923691000100) PK 365 GOLD SR.# NAME OF BANK BRANCH CODE PHONE. -

Final Schedule of 18Th FAS-QAT.Xlsx

QAT Conduct Schedule of 18th FAS‐QAT Cluster EMIS CODE Sr. No. SHIFT Time SCHOOL_NAME Address TEHSIL DISTRICT DATE OF QAT Number / SCHOOL CODE ATK01 A 9.00 am 9‐ATK‐0009 Misali Arqum Science Academy/Sec School Vpo Ikhlas Pindi Ghaib Attock 12/11/2017 1 ATK01 B 12.30 pm 9‐ATK‐0011 Pak Public Higher Secondary School V.P.O Ikhlas Pindi Ghaib Attock 12/11/2017 2 ATK02 A 9.00 am 6‐ATK‐0022 The Village Model School Ikhlas Chowk Pindi Ghaib Attock 12/11/2017 3 ATK03 B 12.30 pm 6‐ATK‐0028 Minhaj Public School Village Hattar Fateh Jang Attock 12/11/2017 4 ATK03 A 9.00 am 7‐ATK‐0026 Fine Public Elementary School V. Po Hattar Fateh Jang Attock 12/11/2017 5 ATK04 A 9.00 am 6‐ATK‐0030 New Mehran Public School Near T.H.Q Hospital Fateh Jang Attock 12/11/2017 6 ATK05 A 9.00 am 8‐ATK‐0004 Al‐Huda Madrasa‐Tul‐Banat R.S Injra Jand Attock 12/11/2017 7 ATK05 B 12.30 pm 9‐ATK‐0014 Muhammad Ali Islamia Public School P.O Village Kani Jand Attock 12/11/2017 8 ATK06 A 9.00 am 9‐ATK‐0004 Green Land Elementary School Mohallah Shah Faisal Abad Attock Attock 12/11/2017 9 ATK06 B 12.30 pm 9‐ATK‐0006 Modern Public Elementary School Moh.Masjid Usmania Shinbagh Attock Attock 12/11/2017 10 ATK07 A 9.00 am 9‐ATK‐0010 Faiz Grammar Public School New Town Bihar Colony Attock Attock 12/11/2017 11 BWN01 A 9.00 am 54 Al Hurmat Public Middle School Qaimabad Canal Colony Bahawalnagar Bahawalnagar 1/3/2018 12 BWN01 B 12.30 pm 216 Fatima Jinnah Public School Mohallah Islam Nagar Bahawalnagar Bahawalnagar 1/3/2018 13 BWN02 A 9.00 am 55 Faisal Public High School Faisal Colony Bahawalnagar -

LA Kamalia Filling Station FAISALABAD LARI ADDA

Customer Name Region Location LA Kamalia Filling Station LARI ADDA KAMALIA,,Mouza Kamalia,,Tobatek FAISALABAD Singh Lasani Filling Station TOTAL Petrol Pump, Pull 111,,,Sargodha FAISALABAD Faisalabad Road,Sargodha Safron Filling Station P-53,Jaranwala Road,,Colony, Jaranwala FAISALABAD Road,Faisalabad Speedway Filling Station Opposite DIG House, College,,University FAISALABAD Road,Sargodha Khawaja Filling Station FAISALABAD Lylpur Plywood, Sargodha Road,,,,Faisalabad Nagina Filling Station Chak # 212 RB,Faisalabad City,,,Jinnah FAISALABAD Road,Faisalabad Layllpur Filling Station FAISALABAD P - 8, Jail Road,,,,Faisalabad Sangam Filling Station Chak No 66 JB Sudhar Bypass, FAISALABAD Jhang,,,Faislabad - Punjab Elite Filling Station FAISALABAD Aqsa Town, Millat Road,,,Faisalabad Puri Filling Station Tehsil Chowk, Chinniot - Fasialabad,, FAISALABAD Road,,Chinniot Sultania Filling Station FAISALABAD Garh More, Garh Maharaja,,,,Distt Jhang S.M. Anwar Filling Station FAISALABAD Sargodha Road,,,Khushab Ittefaq Filling Station 13-14 Km,From Jhang,Malvana More,,Jhang FAISALABAD Bhakar Road,Jhang Jani Filling Station Adjacent Zia Autoes, Sargodha FAISALABAD Road,,,Mianwali Bismillah Filling Station FAISALABAD Bismillah Trades, Plot # 93,,,,Faisalabad AL-MADINA FILLING STATION Lalazar Town#1, Chak#46, South,,Tehsil and FAISALABAD District,Sargodha Ch. Hakim Ali & Co. Near power Station,Samundary FAISALABAD Road,,,Faisalabad Sandal Bar Filling Station FAISALABAD ROAD JHANG 7KM,,EAR MANSHA FAISALABAD HOTEL BYPASS,Jhang Dildar Filling Station FAISALABAD -

Part-I: Post Code Directory of Delivery Post Offices

PART-I POST CODE DIRECTORY OF DELIVERY POST OFFICES POST CODE OF NAME OF DELIVERY POST OFFICE POST CODE ACCOUNT OFFICE PROVINCE ATTACHED BRANCH OFFICES ABAZAI 24550 Charsadda GPO Khyber Pakhtunkhwa 24551 ABBA KHEL 28440 Lakki Marwat GPO Khyber Pakhtunkhwa 28441 ABBAS PUR 12200 Rawalakot GPO Azad Kashmir 12201 ABBOTTABAD GPO 22010 Abbottabad GPO Khyber Pakhtunkhwa 22011 ABBOTTABAD PUBLIC SCHOOL 22030 Abbottabad GPO Khyber Pakhtunkhwa 22031 ABDUL GHAFOOR LEHRI 80820 Sibi GPO Balochistan 80821 ABDUL HAKIM 58180 Khanewal GPO Punjab 58181 ACHORI 16320 Skardu GPO Gilgit Baltistan 16321 ADAMJEE PAPER BOARD MILLS NOWSHERA 24170 Nowshera GPO Khyber Pakhtunkhwa 24171 ADDA GAMBEER 57460 Sahiwal GPO Punjab 57461 ADDA MIR ABBAS 28300 Bannu GPO Khyber Pakhtunkhwa 28301 ADHI KOT 41260 Khushab GPO Punjab 41261 ADHIAN 39060 Qila Sheikhupura GPO Punjab 39061 ADIL PUR 65080 Sukkur GPO Sindh 65081 ADOWAL 50730 Gujrat GPO Punjab 50731 ADRANA 49304 Jhelum GPO Punjab 49305 AFZAL PUR 10360 Mirpur GPO Azad Kashmir 10361 AGRA 66074 Khairpur GPO Sindh 66075 AGRICULTUR INSTITUTE NAWABSHAH 67230 Nawabshah GPO Sindh 67231 AHAMED PUR SIAL 35090 Jhang GPO Punjab 35091 AHATA FAROOQIA 47066 Wah Cantt. GPO Punjab 47067 AHDI 47750 Gujar Khan GPO Punjab 47751 AHMAD NAGAR 52070 Gujranwala GPO Punjab 52071 AHMAD PUR EAST 63350 Bahawalpur GPO Punjab 63351 AHMADOON 96100 Quetta GPO Balochistan 96101 AHMADPUR LAMA 64380 Rahimyar Khan GPO Punjab 64381 AHMED PUR 66040 Khairpur GPO Sindh 66041 AHMED PUR 40120 Sargodha GPO Punjab 40121 AHMEDWAL 95150 Quetta GPO Balochistan 95151 -

Election Commission of Pakistan List of Polling

ELECTION COMMISSION OF PAKISTAN FORM-28 [see rule 50] LIST OF POLLING STATIONS FOR A CONSTITUENCY Election to the National Assembly Provincial Assembly of the Punjab Sindh Khuber Pakhtunkhwa Balochistan No. and name of constituency PP-118 Toba Tek Singh-I Number of Voters assigned Number of Polling In Case of Rural Areas In Case of Urban Areas S.No. of Voters on the to Polling Station Booths electoral roll in case of Sr.No No. and Name of Polling Station electoral area is Census Block Census Name of electoral area Name of electoral area bifurcated Male Female Total Male Female Total Code Block Code 1 2 3 4 5 6 7 8 9 10 11 12 13 CHAK 278/JB CHAK USMAN KOT 162010101 340 0 340 CHAK 278/JB CHAK USMAN KOT 162010102 518 0 518 1 1. Govt.Boys High School 278/JB Usman Kot (Male) (P) CHAK 278/JB CHAK USMAN KOT 162010103 301 0 301 TOTAL 1159 0 1159 2 0 2 CHAK 278/JB CHAK USMAN KOT 162010101 0 278 278 2 2. Girls High School 278/JB. Usman Kot (Female) (P) CHAK 278/JB CHAK USMAN KOT 162010102 0 429 429 CHAK 278/JB CHAK USMAN KOT 162010103 0 259 259 TOTAL 0 966 966 0 2 2 CHAK 278/JB CHAK USMAN KOT 162010104 367 0 367 3. Govt.Model Primary School 278/JB. Chak Mahra (Male) CHAK 278/JB CHAK USMAN KOT 162010105 386 0 386 3 (P) CHAK 278/JB CHAK USMAN KOT 162010106 140 0 140 TOTAL 893 0 893 2 0 2 CHAK 278/JB CHAK USMAN KOT 162010104 0 312 312 4 4. -

List of Branches Authorized for Overnight Clearing (Annexure - II) Branch Sr

List of Branches Authorized for Overnight Clearing (Annexure - II) Branch Sr. # Branch Name City Name Branch Address Code Show Room No. 1, Business & Finance Centre, Plot No. 7/3, Sheet No. S.R. 1, Serai 1 0001 Karachi Main Branch Karachi Quarters, I.I. Chundrigar Road, Karachi 2 0002 Jodia Bazar Karachi Karachi Jodia Bazar, Waqar Centre, Rambharti Street, Karachi 3 0003 Zaibunnisa Street Karachi Karachi Zaibunnisa Street, Near Singer Show Room, Karachi 4 0004 Saddar Karachi Karachi Near English Boot House, Main Zaib un Nisa Street, Saddar, Karachi 5 0005 S.I.T.E. Karachi Karachi Shop No. 48-50, SITE Area, Karachi 6 0006 Timber Market Karachi Karachi Timber Market, Siddique Wahab Road, Old Haji Camp, Karachi 7 0007 New Challi Karachi Karachi Rehmani Chamber, New Challi, Altaf Hussain Road, Karachi 8 0008 Plaza Quarters Karachi Karachi 1-Rehman Court, Greigh Street, Plaza Quarters, Karachi 9 0009 New Naham Road Karachi Karachi B.R. 641, New Naham Road, Karachi 10 0010 Pakistan Chowk Karachi Karachi Pakistan Chowk, Dr. Ziauddin Ahmed Road, Karachi 11 0011 Mithadar Karachi Karachi Sarafa Bazar, Mithadar, Karachi Shop No. G-3, Ground Floor, Plot No. RB-3/1-CIII-A-18, Shiveram Bhatia Building, 12 0013 Burns Road Karachi Karachi Opposite Fresco Chowk, Rambagh Quarters, Karachi 13 0014 Tariq Road Karachi Karachi 124-P, Block-2, P.E.C.H.S. Tariq Road, Karachi 14 0015 North Napier Road Karachi Karachi 34-C, Kassam Chamber's, North Napier Road, Karachi 15 0016 Eid Gah Karachi Karachi Eid Gah, Opp. Khaliq Dina Hall, M.A. -

(Pvt) Ltd. Shop No. 01, Ground

Network Position of Exchange Companies and Exchange Companies of 'B' Category As on September 27, 2021 S# Name of Company Address Outlet Type City District Province Remarks Shop No. 01, Ground Floor, Opposite UBL, Mirpur Chowk, 1 Ravi Exchange Company (Pvt) Ltd. Branch Bhimber Bhimber AJK Active Mirpur Road, Bhimber, Azad Jammu & Kashmir Shop No. 01, Plot No. 67, Junaid Plaza, College Road, Near 2 Royal International Exchange Company (Pvt) Ltd. Maqbool Butt Shaheed Chowk, Tehsil Dadyal, Distt. Mirpur Branch Dadyal Dadyal AJK Active Azad Kashmir Office No. 05, Lower Floor, Deen Trade Centre, Shaheed 3 Sky Exchange Company (Pvt) Ltd. Branch Kotli Kotli AJK Active Chowk, Kotli, AJK. Shop # 3&4 Gulistan Plaza Pindi Road Adjacent to NADRA 4 Pakistan Currency Exchange Company (Pvt) Ltd. Branch Kotli Kotli AJK Active off AJK Shop # 1,2,3 Ch Sohbat Ali shopping center near NBP main 5 Pakistan Currency Exchange Company (Pvt) Ltd. Branch Chaksawari Mirpur AJK Active bazar Chaksawari Azad Kashmir Shop No. 119-A/3, Sub Sector C/2, Quaid-e-Azam Chowk, 6 Pakistan Currency Exchange Company (Pvt) Ltd. Branch Dadyal Mirpur AJK Active Mirpur, District Mirpur, Azad Kashmir 7 Dollar East Exchange Company (Pvt.) Ltd. Shop # 39-40, Muhammadi Plaza, Allama Iqbal Road, Mirpur Branch Mirpur Mirpur AJK Active Shop No. 1-A, Ground Floor, Kalyal Building, Naik Alam 8 HBL Currency Exchange (Pvt) Ltd. Branch Mirpur Mirpur AJK Active Road, Chowk Shaheedan, Mirpur, AJK Sector A-5, Opp. NBP Br., Allama Iqbal Road, Mirpur Azad 9 NBP Exchange Company Ltd. Branch Mirpur Mirpur AJK Active Kashmir. -

Directorate General Health Services Punjab

0 TELEPHONE DIRECTORY DIRECTORATE GENERAL HEALTH SERVICES PUNJAB. D.G.H.S Office [DIRECTORATE GENERAL HEALTH SERVICES, PUNJAB] Sr. Code Name of Office Office No./Fax # No. DGHS, Punjab. 1. 042 99201139-40 (PSO) 99201139-40 ( P.A ) 2. 042 Fax 99201142 99238505 3. DHS (HQ) 042 99201141 DHS (EPI) 99201143 4. 042 99202812 Fax 99200405 ADG (Dengue) (EP&C) 99203235 042 5. Fax 99203235 DHS (P&D) 6. 042 99203793 7. DHS (MIS) 042 99205510 Program Manager( NCD) 8. 042 9. DHS (Dental). 042 99203751 Director (Pharmacy) 99201145 042 10. 99204622 DHS (CDC) 11. 042 99200970 DHS (TB). 35408894 12. 042 Fax 99203750 Director (Accounts). 13. 042 99202487 Additional Director (Admn). 99200987 14. 042 Fax 99201095 36118382 Res Additional Director (EPI) 15. 042 99200535 Additional Director (Malaria ) 16. 042 99202970 A. D (F&N/NCD) 99203749 042 17. Fax. 99204190 (Micronutrient) 99204014 18. 042 36290201 Fax Addl. Director (IRMNCH) 99205330-26 19. 042 99201098 Fax-9203394 1 Sr. Code Name of Office Office No./Fax # No. Addl. Director-I, IRMNCH 99200982 20. 042 99201098 Fax-9203394 P.M Hepatitis 21. 042 99204129 Addl. Director (MS&DC) 22. 042 99203505 Usman Ghani 23. 042 99200969 Additional Director (H.E). Media Manager 24. 042 99200969 Additional Director (TB-DOTS) 25. 042 99203750 Transport Manager, TMO 26. Workshop 042 35155845 27. (Supt.TPT) Budget & Accounts Officer 28. 042 99203487 Additional Director (Homeo) Shahid (Homeo Dr) 29. 042 99204191 Litigation Officer 30. Mr.Imran Ur Rehman 042 99200983 Computer Programer 31. 042 99200990 G.M (MSD) 35758336 32. 042 35873989 99201257 33. Bacteriologist 042 99200108 PD (HIV/AIDS). -

CORPORATE MEMBERS for the YEAR 2021-2022 Page 1

THE FAISALABAD CHAMBER OF COMMERCE & INDUSTRY LIST OF CORPORATE MEMBERS FOR THE YEAR 2021-2022 Page 1 1. MEMBER ID 1100032-7 6. MEMBER ID 1100149-35 11. MEMBER ID 1100225-72 MIAN ZAFAR & CO S.K.TEXTILE SALEEM TEXTILES COMPANY. 68-GULSITAN MARKET, RAILWAY ROAD, CHAK NO 209 RB STOP 209 CHAK PLOT#5, BLOCK# 8, 1/F, REGENCY STREET FAISALABAD JARANWALA ROAD FAISALABAD CIVIL LINES, FAISALABAD TEL : 041-2644031,2620061 TEL : 041-8001377 TEL : 041-2612841, 2619924 MOBILE : 0300-8662834 MOBILE : 0321-6687400,324-2630000 MOBILE : 0300-8664480, 03008661920 FAX : 041-2618916,2646199 FAX : NIL FAX : 041-2619527 E-MAIL : [email protected] E-MAIL : nil E-MAIL : [email protected], REP : MIAN ZAFAR IQBAL REP : MUHAMMAD SAEED [email protected] REP : MIAN HABIB ULLAH 2. MEMBER ID 1100039-1351 7. MEMBER ID 1100206-63 12. MEMBER ID 1100243-82 HAROON CORPORATION REHAN TEX INTERNATIONAL TAUSEEF ENTERPRISES P-417, NISAR COLONY, FAISALABAD P-129, MADINA INDUSTRIAL ESTATE, 119- P-20, BILAL ROAD, CIVIL LINES TEL : 041-2660888,2660788, JB, SAMANA, SARGODHA ROAD FAISALABAD MOBILE : 0300-8662988 FAISALABAD TEL : 041-2616779,2616673 FAX : 041-2663003 TEL : 041-8811245 MOBILE : 0322-8555555 E-MAIL : [email protected], MOBILE : 0323-6509523 FAX : 041-2619189 [email protected] FAX : 041-8811246 E-MAIL : [email protected], REP : MUHAMMAD QASIM E-MAIL : [email protected] [email protected] REP : BASHIR AHMAD REHAN REP : SALAMAT ALI 3. MEMBER ID 1100081-1446 8. MEMBER ID 1100214-66 13. MEMBER ID 1100283-94 GENIUS TEXTILES NETWORK BISMILLAH FABRICS AMEER ENTERPRISES CHAK NO 82 JB 3KM GOJRA ROAD 1579/D,GALI # 4, GHULAM 11 KM, JARANWALA ROAD, NEAR GOUSIA PANSARA FAISALABAD MUHAMMADABAD, FAISALABAD. -

List of Hospitals Province-Wise with Isolation Facilities

LIST OF HOSPITALS PROVINCE-WISE WITH ISOLATION FACILITIES Sr Districts Hospitals Beds Islamabad 1. Islamabad Pakistan Institute of Medical Sciences (PIMS) 10 TOTAL 1 (Medical Facility) 10 Balochistan Sr Districts Hospitals Beds 1. BHU Dalbandin 4 2. Chaghi DHQ Hospital Dalbandin 10 3. Pakistan House, Taftan 9 4. Panjgur DHQ Hospital Panjgur 12 5. Kech DHQ Hospital Kech 10 6. Gwadar GDA Hospital 10 7. Washuk DHQ Hospital Washuk 5 8. Chaman DHQ Hospital Chaman 10 9. Killa Abdullah DHQ Hospital Killa Abdullah 14 10. Killa Saifullah DHQ Hospital Killa Saifullah 15 11. Zhob DHQ Hospital and BHU Qamardin Karez 5 12. Sheikh Khalifa Bin Zayed Hospital 225 Quetta 13. Fatima Jinnah General and Chest Hospital 200 14. Lasbella DHQ Hospital Lasbella 5 TOTAL 14 (Medical Facilities) 534 Khyber Pakhtunkhwa Sr Districts Hospitals Beds 1. DHQ Hospital Abbottabad 15 2. Ayub Teaching Hospital 24 3. Abbottabad Medical Complex 10 4. Gillani Hospital 5 5. Cat-D Hospital Havellian 5 Abbottabad 6. Cat-D Hospital Lora 5 7. Cat-D Hospital Boi 5 8. Nathiagali 4 9. Khairagali 5 10. Sherwan 3 11. Bajaur DHQ Hospital Khar 8 12. DHQ Hospital Bannu 10 13. KGN Hospital Bannu 6 14. Type-D Hospital Kakki 4 15. Bannu Type-D Hospital Janni Khel 4 16. RHC Domel 3 17. RHC Ghori Wala 8 18. DHQ Hospital Battagram 10 19. Type-D Hospital Banna 5 20. Battagram RHC Thakot 4 21. Kozabanda 12 22. Buner DHQ Hospital Buner 4 23. DHQ Hospital Charsadda 5 24. THQ Hospital Shabqadar 2 Charsadda 25. THQ Hospital Tangi 4 26. -

List of Loan Centers

Loan Center/ Branch Sr.No. Province District PO Name City / Tehsil Focal Person Contact No. Union Council/ Location Address Name Azad Jammu Akhuwat Islamic College Chowk Oppsite Boys College Sudan Galli 1 Bagh Bagh Bagh Nadeem Ahmed 0314-5273451 and Kashmir Microfinance (AIM) Road Baagh Azad Jammu Akhuwat Islamic 2 Bagh Dhir Kot Dhir Kot Nadeem Ahmed 0314-5273451 Muzaffarabad Road Near main bazar dhir kot and Kashmir Microfinance (AIM) Azad Jammu Akhuwat Islamic 3 Bagh Harighel Harighel Nadeem Ahmed 0314-5273451 Mang bajri arja near chambar hotel Harighel and Kashmir Microfinance (AIM) Azad Jammu Akhuwat Islamic 4 Bhimber Bhimber Bhimber Arshad Mehmood 0346-4663605 Kotli Mor Near Muslim & School and Kashmir Microfinance (AIM) Azad Jammu Akhuwat Islamic 5 Bhimber Barnala Barnala Arshad Mehmood 0346-4663605 Main Road Bimber & Barnala Road and Kashmir Microfinance (AIM) Azad Jammu Akhuwat Islamic Main choki Bazar near Sir Syed girls College choki 6 Bhimber Samahni Samahni Arshad Mehmood 0346-4663605 and Kashmir Microfinance (AIM) Samahni Azad Jammu Akhuwat Islamic Akhuwat office House No Master Sadeeq Near jame 7 Haveli Haveli Haveli Muhammad Faraz 0304-8302417 and Kashmir Microfinance (AIM) masjid hafsa Azad Jammu Akhuwat Islamic Akhuwat office main bazar palange Jamia Faiz 8 Haveli Mumtazabad Mumtazabad Muhammad Faraz 0304-8302417 and Kashmir Microfinance (AIM) Madinda Masjid Mumtazabad Azad Jammu Akhuwat Islamic 9 Jehlum Valley Hattian Bala Hattian Bala Nadeem Ahmed 0314-5273451 Pull Bazar Near Al Mustafa masjid hatian bala and Kashmir