Sierra Leone Fish Value Chain with Special Emphasis on Tonkolili District

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Comprehensive Food Security and Vulnerability Analysis Data Collected November–December 2020 Overall Supervision Denis K

SAVING In partnership with the Government of Sierra Leone Main Report MAY 2021 LIVES CHANGING LIVES STATE OF FOOD SECURITY IN SIERRA LEONE 2020 Comprehensive Food Security and Vulnerability Analysis Data collected November–December 2020 Overall Supervision Denis K. Vandi, Former Honourable Minister, MAF Prof. Osman Sankoh, Statistician General, Stats SL Stephen Nsubuga, Representative WFP Yvonne Forsen, Deputy Country Director WFP Team Leader Sahib Haq, International Consultant Concept, Planning and Design Ballah Musa Kandeh, WFP Sahib Haq, International Consultant Robin Yokie, FAO Dr. Mohamed Ajuba Sheriff, MAF Dr. Kepifri Lakoh, MAF Momodu M. Kamara, Stats SL Field Supervision and Coordination Ballah Musa Kandeh, WFP Dr. Mohamed Ajuba Sheriff, MAF Dr. Kepifri Lakoh, MAF Momodu M. Kamara, Stats SL Aminata Shamit Koroma, MoHS Allison Dumbuya, WFP Data Processing and Analysis, Food Security Sahib Haq, WFP International Consultant Brian Mandebvu, WFP Ballah Musa Kandeh, WFP Nutrition Analysis Brian Mandebvu, WFP MoHS Nutrition Directorate Report Writing and Editing Yvonne Forsen, WFP Brian Mandebvu, WFP Ballah Musa Kandeh, WFP Sahiba Turgesen, WordWise Consulting Photo credit Evelyn Fey William Hopkins Software and data transfer Allison Dumbuya, WFP Comprehensive Food Security and Vulnerability Analysis Sierra Leone 2020 Comprehensive Food Security and Vulnerability Analysis Sierra Leone 2020 2 Preface The State of Food Security in Sierra Leone 2020 showcases findings from the Comprehensive Food Security and Vulnerability Analysis (CFSVA). The CFSVA provides a trend analysis on food insecurity and is conducted every five years. This is the third CFSVA conducted in Sierra Leone. Despite the ongoing global COVID-19 pandemic, the CFSVA was undertaken as planned in November and December 2020, underscoring the commitment of food security partners. -

BTI 2020 Country Report — Sierra Leone

BTI 2020 Country Report Sierra Leone This report is part of the Bertelsmann Stiftung’s Transformation Index (BTI) 2020. It covers the period from February 1, 2017 to January 31, 2019. The BTI assesses the transformation toward democracy and a market economy as well as the quality of governance in 137 countries. More on the BTI at https://www.bti-project.org. Please cite as follows: Bertelsmann Stiftung, BTI 2020 Country Report — Sierra Leone. Gütersloh: Bertelsmann Stiftung, 2020. This work is licensed under a Creative Commons Attribution 4.0 International License. Contact Bertelsmann Stiftung Carl-Bertelsmann-Strasse 256 33111 Gütersloh Germany Sabine Donner Phone +49 5241 81 81501 [email protected] Hauke Hartmann Phone +49 5241 81 81389 [email protected] Robert Schwarz Phone +49 5241 81 81402 [email protected] Sabine Steinkamp Phone +49 5241 81 81507 [email protected] BTI 2020 | Sierra Leone 3 Key Indicators Population M 7.7 HDI 0.438 GDP p.c., PPP $ 1604 Pop. growth1 % p.a. 2.1 HDI rank of 189 181 Gini Index 34.0 Life expectancy years 53.9 UN Education Index 0.403 Poverty3 % 81.3 Urban population % 42.1 Gender inequality2 0.644 Aid per capita $ 71.8 Sources (as of December 2019): The World Bank, World Development Indicators 2019 | UNDP, Human Development Report 2019. Footnotes: (1) Average annual growth rate. (2) Gender Inequality Index (GII). (3) Percentage of population living on less than $3.20 a day at 2011 international prices. Executive Summary General elections were held in Sierra Leone in March 2018 to elect the president, parliament and local councils. -

Adjustment and Debt

9832 Public Disclosure Authorized The World Bank Research Program 1990 Public Disclosure Authorized Abstracts of Public Disclosure Authorized Current Studies Public Disclosure Authorized THE WORLD BANK RESEARCH PROGRAM 1990 ABSTRACTS OF CURRENT STUDIES The World Bank Washington, D.C. Copyright @ 1991 by the International Bank for Reconstruction and Development/Ihe World Bank 1818 H Street, N.W., Washington, D.C. 20433, U.S.A. All rights reserved. First printing: July 1991 Manufactured in the United States of America ISSN 0258-3143 ISBN 0-8213-1885-3 RESEARCH AT THE WORLD BANK The term "research," in its broadest definition, en- Policy Council (RPPC) chaired by the Senior Vice Presi- compasses a wide spectrum of Bank activities. Much dent, Policy, Research, and External Affairs, sets priority economic and sector work - analytical work to support guidelines for all Bank-supported research. RPPC mem- operations - generates new knowledge about member bers are drawn from the ranks of Bank senior managers, countries. Outside the Bank, this work might well be seen mainly vice presidents. as research. By convention, however, Bank research is Bank research is funded through two sources: de- defined more narrowly to include only analytical work partmental resources, mainly staff time, and the Research designed to produce results with relatively wide applica- Support Budget. The RSB also supports severa activities bility. Although clearly motivated by policy concerns, that, while not properly research projects, add to the value Bankresearchisusuallydriven notbytheimmediateneeds of Bank research and enhance the Bank's image as an of a particular Bank lending operation or a particular intellectual leader in the field of development research. -

G U I N E a Liberia Sierra Leone

The boundaries and names shown and the designations Mamou used on this map do not imply official endorsement or er acceptance by the United Nations. Nig K o L le n o G UINEA t l e a SIERRA Kindia LEONEFaranah Médina Dula Falaba Tabili ba o s a g Dubréka K n ie c o r M Musaia Gberia a c S Fotombu Coyah Bafodia t a e r G Kabala Banian Konta Fandié Kamakwie Koinadugu Bendugu Forécariah li Kukuna Kamalu Fadugu Se Bagbe r Madina e Bambaya g Jct. i ies NORTHERN N arc Sc Kurubonla e Karina tl it Mateboi Alikalia L Yombiro Kambia M Pendembu Bumbuna Batkanu a Bendugu b Rokupr o l e Binkolo M Mange Gbinti e Kortimaw Is. Kayima l Mambolo Makeni i Bendou Bodou Port Loko Magburaka Tefeya Yomadu Lunsar Koidu-Sefadu li Masingbi Koundou e a Lungi Pepel S n Int'l Airport or a Matotoka Yengema R el p ok m Freetown a Njaiama Ferry Masiaka Mile 91 P Njaiama- Wellington a Yele Sewafe Tongo Gandorhun o Hastings Yonibana Tungie M Koindu WESTERN Songo Bradford EAS T E R N AREA Waterloo Mongeri York Rotifunk Falla Bomi Kailahun Buedu a i Panguma Moyamba a Taiama Manowa Giehun Bauya T Boajibu Njala Dambara Pendembu Yawri Bendu Banana Is. Bay Mano Lago Bo Segbwema Daru Shenge Sembehun SOUTHE R N Gerihun Plantain Is. Sieromco Mokanje Kenema Tikonko Bumpe a Blama Gbangbatok Sew Tokpombu ro Kpetewoma o Sh Koribundu M erb Nitti ro River a o i Turtle Is. o M h Sumbuya a Sherbro I. -

Download PDF File

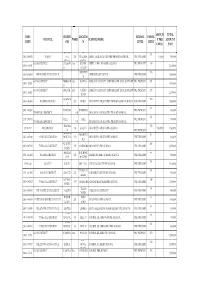

AMOUN TOTAL EMIS CHIEFD LOCATIO SCHOOL ENROL COUNCIL WARD SCHOOL NAME T PER AMOUNT CODE OM N LEVEL MENT CHILD PAID WATERL 45 85 5103-3-09029 WARDC OO 391 WILLIAM ABDUL JALIL ACADEMY PRE-PRIMARY SCHOOL PRE-PRIMARY 10,000 850,000 RURAL STREET KONO DISTRICT TANKOR East DOWN ABDULAI IBN ABASS PRE-SCHOOL PRE PRIMARY 110 1391-1-01995 1,100,000 O BALOP ABERDEE 106 5208-2-10849 FREETOWN CITY COUNCIL ABERDEEN MUNICIPAL PRE-PRIMARY 1,060,000 N KONO DISTRICT NIMIKOR East KOMAO AFRICA COMMUNITY EMPOERMENT DEVELOPMENT PRE PRIMARY 151 1309-1-02125 1,510,000 O KONO DISTRICT GBENSE East YARDU AFRICA COMMUNITY EMPOERMENT DEVELOPMENT PRE PRIMARY 127 1391-1-01802 1,270,000 ROAD MAGBEM 102 3105-1-02506 KAMBIA DISTRICT 201 ROBAT AHMADIYYA MUSLIM PRE PRIMARY SCHOOL-ROBAT PRE-PRIMARY 1,020,000 A 60 2401-1-05230 DANSOGO BUMBUNA PRE-PRIMARY 600,000 TONKOLILI DISTRICT 185 AHMADIYYA MUSLIM PRE-PRIMARY SCHOOL 54 2417-1-05764 YELE YELE PRE-PRIMARY 540,000 TONKOLILI DISTRICT 176 AHMADIYYA MUSLIM PRE-PRIMARY SCHOOL TIKONK 150 311301112 BO DISTRICT 289 KAKUA AHMADIYYA MUSLIM PRE-SCHOOL 10,000.00 1,500,000 O PRE-PRIMARY KHOLIFA MAGBURA 83 2407-1-05340 TONKOLILI DISTRICT ROWALL 170 AHMADIYYA MUSLIM PRE-SCHOOL PRE-PRIMARY 830,000 KA A KUNIKE- 105 2410-1-05521 TONKOLILI DISTRICT 179 MASINGBI AHMADIYYA PRE-SCHOOL PRE-PRIMARY 1,050,000 SANDA MAKENI ROGBOM/ 83 2191-1-04484 BOMBALI DISTRICT 123 ALHADI ISLAMIC NURSERY SCHOOL PRE-PRIMARY 830,000 CITY MAKENI 151 319101126 BO CITY KAKUA BO NO 2 ALHAJI NAZI-ALIE PRE-SCHOOL PRE-PRIMARY 1,510,000 TIMBO/M 80 2191-1-04505 BOMBALI DISTRICT -

Sierra Leone Unamsil

13o 30' 13o 00' 12o 30' 12o 00' 11o 30' 11o 00' 10o 30' Mamou The boundaries and names shown and the designations used on this map do not imply ger GUINEA official endorsemenNt ior acceptance by the UNAMSIL K L United Nations. o l o e l n a Deployment as of t e AugustKindia 2005 Faranah o o 10 00' Médina 10 00' National capital Dula Provincial capital Tabili s a Falaba ie ab o c K g Dubréka Town, village r n a o c M S Musaia International boundary t Gberia Coyah a Bafodia UNMO TS-11 e Provincial boundary r Fotombu G Kabala Banian Konta Bendugu 9o 30' Fandié Kamakwie Koinadugu 9o 30' Forécariah Kamalu li Kukuna Fadugu Se s ie agbe c B Madina r r a e c SIERRA LEONE g Jct. e S i tl N Bambaya Lit Ribia Karina Alikalia Kurubonla Mateboi HQ UNAMSIL Kambia M Pendembu Yombiro ab Batkanuo Bendugu l e Bumbuna o UNMO TS-1 o UNMO9 00' HQ Rokupr a 9 00' UNMO TS-4 n Mamuka a NIGERIA 19 Gbinti p Binkolo m Kayima KortimawNIGERIA Is. 19 Mange a Mambolo Makeni P RUSSIA Port Baibunda Loko JORDAN Magburaka Bendou Mape Lungi Tefeya UNMO TS-2 Bodou Lol Rogberi Yomadu UNMO TS-5 Lunsar Matotoka Rokel Bridge Masingbi Koundou Lungi Koidu-Sefadu Pepel Yengema li Njaiama- e Freetown M o 8o 30' Masiaka Sewafe Njaiama 8 30' Goderich Wellington a Yonibana Mile 91 Tungie o Magbuntuso Makite Yele Gandorhun M Koindu Hastings Songo Buedu WESTERN Waterloo Mongeri Falla York Bradford UNMO TS-9 AREA Tongo Giehun Kailahun Tolobo ia Boajibu Rotifunk a T GHANA 11 Taiama Panguma Manowa Banana Is. -

Letter to African Minerals Limited and Response

HUMAN RIGHTS WHOSE DEVELOPMENT? Human Rights Abuses in Sierra Leone’s Mining Boom WATCH Whose Development? Human Rights Abuses in Sierra Leone’s Mining Boom Copyright © 2014 Human Rights Watch All rights reserved. Printed in the United States of America ISBN: 978-1-62313-1067 Cover design by Rafael Jimenez Human Rights Watch is dedicated to protecting the human rights of people around the world. We stand with victims and activists to prevent discrimination, to uphold political freedom, to protect people from inhumane conduct in wartime, and to bring offenders to justice. We investigate and expose human rights violations and hold abusers accountable. We challenge governments and those who hold power to end abusive practices and respect international human rights law. We enlist the public and the international community to support the cause of human rights for all. Human Rights Watch is an international organization with staff in more than 40 countries, and offices in Amsterdam, Beirut, Berlin, Brussels, Chicago, Geneva, Goma, Johannesburg, London, Los Angeles, Moscow, Nairobi, New York, Paris, San Francisco, Tokyo, Toronto, Tunis, Washington DC, and Zurich. For more information, please visit our website: http://www.hrw.org FEBRUARY 2014 978-1-62313-1067 Whose Development? Human Rights Abuses in Sierra Leone’s Mining Boom Map of Sierra Leone ............................................................................................................ i Summary .......................................................................................................................... -

African Markets Managing Natural Resources a Report from the Economist Intelligence Unit

African Markets Managing natural resources A report from The Economist Intelligence Unit Sierra Leone Commissioned by: March 2013 African Capacity Building Foundation www.eiu.com African Markets Managing natural resources Country profile: Sierra Leone Politics and institutions Sierra Leone has a largely presidential system of government. The president and members of parliament are elected every five years by universal adult suffrage. A constituency system was adopted in 2007, replacing the national list proportional representation system, which had been in place since the end of the civil war in 2002. The country’s third democratic election, in 2007, was held in relative peace and led to the first peaceful handover of power from one party to another in post-independence history. The country has a legacy of civil war and military coups, although it has held three peaceful democratic elections since the end of the 1991-2002 civil war. This war was launched by the rebel Revolutionary United Front (RUF) and undermined the already weak institutions and fragile government. In 2002, after an estimated 50,000 deaths, the war was officially declared over, following the deployment of UN peacekeeping forces. However, the causes of political instability in Sierra Leone, such as corruption and socio-economic imbalances, have not been addressed. Creating networks of patronage in return for support at the polls is a long-established tradition in Sierra Leone, and one that continues today. Political parties The political scene is dominated by two parties; the ruling All People’s Congress (APC) and the Sierra Leone People’s Party (SLPP). The APC dominates the Temne communities in the north and west, while the SLPP draws most of its support from the Mende ethnic group in the south and east of Sierra Leone. -

Participant List

Participant List 10/20/2019 8:45:44 AM Category First Name Last Name Position Organization Nationality CSO Jillian Abballe UN Advocacy Officer and Anglican Communion United States Head of Office Ramil Abbasov Chariman of the Managing Spektr Socio-Economic Azerbaijan Board Researches and Development Public Union Babak Abbaszadeh President and Chief Toronto Centre for Global Canada Executive Officer Leadership in Financial Supervision Amr Abdallah Director, Gulf Programs Educaiton for Employment - United States EFE HAGAR ABDELRAHM African affairs & SDGs Unit Maat for Peace, Development Egypt AN Manager and Human Rights Abukar Abdi CEO Juba Foundation Kenya Nabil Abdo MENA Senior Policy Oxfam International Lebanon Advisor Mala Abdulaziz Executive director Swift Relief Foundation Nigeria Maryati Abdullah Director/National Publish What You Pay Indonesia Coordinator Indonesia Yussuf Abdullahi Regional Team Lead Pact Kenya Abdulahi Abdulraheem Executive Director Initiative for Sound Education Nigeria Relationship & Health Muttaqa Abdulra'uf Research Fellow International Trade Union Nigeria Confederation (ITUC) Kehinde Abdulsalam Interfaith Minister Strength in Diversity Nigeria Development Centre, Nigeria Kassim Abdulsalam Zonal Coordinator/Field Strength in Diversity Nigeria Executive Development Centre, Nigeria and Farmers Advocacy and Support Initiative in Nig Shahlo Abdunabizoda Director Jahon Tajikistan Shontaye Abegaz Executive Director International Insitute for Human United States Security Subhashini Abeysinghe Research Director Verite -

The West Indian Mission to West Africa: the Rio Pongas Mission, 1850-1963

The West Indian Mission to West Africa: The Rio Pongas Mission, 1850-1963 by Bakary Gibba A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Graduate Department of History University of Toronto © Copyright by Bakary Gibba (2011) The West Indian Mission to West Africa: The Rio Pongas Mission, 1850-1963 Doctor of Philosophy, 2011 Bakary Gibba Department of History, University of Toronto Abstract This thesis investigates the efforts of the West Indian Church to establish and run a fascinating Mission in an area of West Africa already influenced by Islam or traditional religion. It focuses mainly on the Pongas Mission’s efforts to spread the Gospel but also discusses its missionary hierarchy during the formative years in the Pongas Country between 1855 and 1863, and the period between 1863 and 1873, when efforts were made to consolidate the Mission under black control and supervision. Between 1873 and 1900 when additional Sierra Leonean assistants were hired, relations between them and African-descended West Indian missionaries, as well as between these missionaries and their Eurafrican host chiefs, deteriorated. More efforts were made to consolidate the Pongas Mission amidst greater financial difficulties and increased French influence and restrictive measures against it between 1860 and 1935. These followed an earlier prejudiced policy in the Mission that was strongly influenced by the hierarchical nature of nineteenth-century Barbadian society, which was abandoned only after successive deaths -

U N I T E D N a T I O

U N I T E D N A T I O N S Office for the Coordination of Humanitarian Affairs SIERRA LEONE HUMANITARIAN SITUATION REPORT SEPTEMBER 2003 KEY EVENTS district. A concern raised in Kono is that none of the Watsan implementing partners had the facilities or machines for testing water • Yellow Fever outbreak samples. This has been reported to the MOHS. • Security Council extends UNAMSIL’s mandate • UN Agencies and GoSL celebrate World Peace Day SECURITY HIGHLIGHTS • Nigerian lawmakers call on UNAMSIL Overall security UNAMSIL (United Nations Mission in Sierra Leone) reports the overall security situation in HUMANITARIAN HIGHLIGHTS the country to be calm. However there have been some concerns about security along the Yellow Fever outbreak border regions, particularly along the Mano The Ministry of Health and Sanitation (MOHS) River Union Bridge in the south. Similarly the has reported a total of 90 cases of Yellow Sierra Leone Police (SLP) are concerned Fever, from eight districts in the country: about the porous nature of the border in the Tonkolili, Bombali, Kenema, Koinadugu, Port Kamakwie, Tambakha and Koinadugu areas, Loko, Kambia and Kono. Of the 90 reported in the Northern Province that have resulted in cases (as of 29 September) four laboratory increased smuggling of goods across the cases were confirmed, all from the Tonkolili borders. The police have also reported hunters District, where majority of the suspected cases from Guinea, coming across, poaching and emanate from. Earlier, the MOHS gave out crossing back into Guinea. 100,000 doses of vaccine in four chiefdoms in the district. They have now finally secured UNAMSIL’s mandate extended funds to carry out mass immunization The UN Security Council has extended campaign in the remaining seven chiefdoms of UNAMSIL’s mandate, which was to expire on the district. -

Sierra Leone - Mobile Money Transfer Market Study

Sierra Leone - Mobile Money Transfer Market Study FINAL REPORT, March 2013 March 2013 Report prepared by PHB Development, with the support of Disclaimer The contents of this report are the responsibility of PHB Development and do not necessarily reflect the views of Cordaid. The information contained in this report and any errors or mistakes that occurred are the sole responsibility of PHB Development. 2 Contents Introduction………………………………………………………………………………3 Executive Summary and Recommendations………………………………............... 9 I. Module 1 Regulation and Partnerships (Supply side)……………………………….23 II. Module 2 Markets and products (Demand side )……………………………………..56 III. Module 3 Distribution Networks………………………………………………………..74 IV. Module 4 MFI Internal Capacity………………………………………………………..95 V. Module 5 Scenario's for Mobile Money Transfers and the MFIs in Sierra Leone...99 3 Introduction Cordaid has invited PHB Development to execute a market study on Mobile Money Transfers (MMT) in Sierra Leone and on the opportunities this market offers for Microfinance Institutions (MFIs). This study follows on the MITAF1 programme that Cordaid co-financed in the period 2004-2011. The results of the market study were shared in an interactive workshop in Sierra Leone on 26 February 2013. 27 persons attended, representing MFIs, MMT providers, the Bank of Sierra Leone and the donor. This final report represents an overview of the information collected, on which the workshop has been based. Moreover, information obtained during the workshop is reflected in this document. In addition, the MFIs have received individual assessment reports on their readiness for MMT. This report starts with an executive summary followed by recommendations for the MFIs and Cordaid. Chapters 1-5 provide detailed information on the regulation and the supply side of market players and MMT partnerships (module 1), on the demand for financial products (module 2) and the agent networks in Sierra Leone (module 3).