Alternative Lending Complaint

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CAMPUS MAP a - Boettcher Auditorium

A B C D E F G H I LEGEND ACADEMIC BUILDINGS B 1 Ammi Hyde Building D-8 U C H 2 Boettcher West D-7 T EL CAMPUS MAP A - Boettcher Auditorium BO 1 U University of Denver 3 Chambers Center for the Advancement of Women B-3 LE VA Light Rail Station 4 Craig Hall B-5 R 54 D 5 Daniels College of Business F-5 6 English Language Center I-3 7 Fisher Early Learning Center A-4 8 Frontier Hall B-5 9 Iliff School of Theology Campus E/F-6 E. COLORADO AVE 10 Johnson-McFarlane Hall B-6 A - Theatre: Black Box Studio & White Box Studio 11 Knoebel School of Hospitality Management C-5 12 Knudson Hall F-7 13 Margery Reed Building F-5 33 14 Mass Communications E-8 15 Metallurgy E-8 2 16 Newman Center for the Performing Arts/Lamont School of Music F-7 60 A - Trevorrow Hall 53 B - Hamilton Recital Hall C - Gates Concert Hall D - Byron Theatre SOUTH WILLIAMS ST SOUTH HIGH ST BUCH TEL BO 17 Olin Hall D-7 61 ULEVA RD 18 Physics Building D-8 EAST JEWELL AVE 48 EAST JEWELL AVE EAST JEWELL AVE 19 Ricketson Law Building E-4 59 20 Ricks Center for Gifted Children F-4 21 Ritchie School for Engineering & Computer Science E-7 22 Ruffatto Hall B-4 55 58 23 Seeley Mudd Science Building D-7 24 Shwayder Art Building D-3 24A A - Nagel Art Studios 3 25 Sie International Relations Complex D-6 A - Sié Chéou-Kang Center K 6 71 26 Sturm Hall C-4 3 24 27 Wesley Hall D-7 35 OTHER BUILDINGS/FACILITIES 28 Academic Office Annex E-8 SOUTH YORK ST SOUTH YORK EAST ASBURY AVE EAST ASBURY AVE 29 Anderson Academic Commons E-5 A - Main Library 26 44 30 Aspen Hall C-6 38 31 Buchtel Bungalow I-5 -

History of Arapahoe County

History of Arapahoe County Arapahoe County was named for the Arapaho Indians, one of the In the late 1820s, trappers searched larger tribes of plains Indians, who along with the Cheyenne occupied this region for beavers to supply Arapahoe County east of the foothills running into what is now western the great demand for mens beaver Kansas. Arapahoe County is Colorado’s first county, since almost hats. In the late 1830s and 1840s, half of the entire area now Colorado was Arapahoe County of the the demand shifted to buffalo Kansas territory. In 1861, when Kansas was made a state, Colorado skins. In 1832, the first trading was made a territory with Arapahoe County as one of the 17 original post on the South Platte River was counties. built on Cherry Creek, which was then part of Arapahoe County. The original Arapahoe County was 30 miles wide and extended from Sheridan Boulevard, the present western boundary of Denver, Adams In 1848, gold prospectors on and Arapahoe counties to the Kansas border. This peculiar shape was their way to California stopped in due to the practice of giving counties with large amounts of plains Colorado long enough to pan its territory at least some of the foothill territory where there was water streams. They found gold on West for mining and irrigation. Even though Arapahoe County did not Dartmouth Avenue, just west of reach the foothills, the streams running from the mountains supplied Englewood where Dry Creek flows water. As settlers came in and took up lands on the eastern portions into the Platte River. -

1 DISTRICT COURT, CITY and COUNTY of DENVER, COLORADO 1437 Bannock Street Denver, CO 80202 the PEOPLE of the STATE of COLORADO

DISTRICT COURT, CITY AND COUNTY OF DENVER, COLORADO 1437 Bannock Street Denver, CO 80202 THE PEOPLE OF THE STATE OF COLORADO, v. Jose Roberto MORENO-OLIVAS a/k/a PAUL Victor Antonio BAUTISTA-CERVANTES a/k/a NEGRI Jesus Alfredo VALDEZ-LEON a/k/a ALFREDO Baltazar IBARRA-ALVAREZ a/k/a IBARRA Gildardo VALDEZ-CRUZ a/k/a LAGRIMAS Miriam RIVERA Tawnia WHITE Denise RIVERA-REYES Dolores IBARRA-ESPINOZA Jose Ignacio VALDEZ-SOLIS a/k/a Jesus URIAS-LOPEZ a/k/a PELON Anakaren PEREZ Janett SANCHEZ-RUIZ Adiel ACOSTA-LEYVA Karla VILLA-CEBALLOS Maximilliano ACOSTA Samuel QUINONEZ-HERRERA FNU LNU a/k/a NARICLES Omar BAUTISTA-CUEVAS Alfredo NUNEZ-TARANGO Ivan ABOYTE-VALDEZ FNU LNU a/k/a Unidentified Male #1207 Jesus Alberto LOPEZ-MEDINA Ossler MARQUEZ-GUZMAN a/k/a OLDER Erubiel IBARRA-ALVAREZ a/k/a HUACHE FNU LNU a/k/a Unidentified Male #5123 Jesus BARBA-OCHOA Ivan Felix QUINTERO a/k/a CHAYANNE Gerardo MURILLO a/k/a GERA Jose Luis SALAS-LUGO a/k/a CABIN Eladio MORENO-OLIVAS a/k/a LAYO Jose Luis QUINTERO-SOLANO Jaziel QUINTERO-SOLANO Defendants. COURT USE ONLY 1 PHILIP J. WEISER, Attorney General Case No: ANNEMARIE L. BRAUN* Senior Assistant Attorney General GJ Case No.: 20CR01 Registration Number: 39877 ALISON CONNAUGHTY* Ctrm: 259 Senior Assistant Attorney General Registration Number: 42548 1300 Broadway, 9th Floor Denver, CO 80203 720-508-6701 *Counsel of Record COLORADO STATE GRAND JURY INDICTMENT – SUPERSEDING 2-11-21 Of the 2020-2021 term of the Denver District Court in the year 2021; 2020- 2021 Colorado State Grand Jurors, chosen, selected and sworn -

2020 City of Denver Creative Economy Report with Initial Impacts of the COVID-19 Crisis

2020 City of Denver Creative Economy Report with Initial Impacts of the COVID-19 Crisis Lisa Gedgaudas Program Administrator, Create Denver Denver Arts & Venues, City of Denver Prepared by: Dr. Michael Seman Colorado State University LEAP Institute for the Arts Regional Economic Development Institute Table of Contents Executive Summary .............................................................................................................. ii Introduction ........................................................................................................................ 1 Creative Industries Employment ........................................................................................ 1 Creative Occupations Employment .................................................................................... 3 Rising Regional Housing Costs and Creative Occupations ...................................... 4 Creative Industries Revenue ............................................................................................... 6 Initial Impacts of the COVID-19 Crisis ................................................................................. 7 Background ............................................................................................................. 7 Impacts .................................................................................................................... 8 Conclusion ............................................................................................................... 9 Acknowledgements -

Adams County, Colorado Districts Providing Water and Sanitation Service

Adams County, Colorado Districts Providing Water and Sanitation Service WELD R t E ve S E Bridge St E 160th A D t (!7 L k S r U o y l l Y O o B H Bromley Ln E 152nd Ave d d d R R R t t y l t S s n d l d i e o S c v R d t l i v t e r a a B n b n c a h u c u e e Z i l H D 85 w u o b o L ¤£ P Q a m E P I s F 25 S E 136th Ave e M ¨¦§ y O 76 a H O d ¨¦§ R R B E 128th Ave s 470 n )" i k t a E 120th Ave W t d S R n s o r r e u E 112th Ave d b t v H l S m B a a o h y d a C l a Denver International Airport r e E 104th Av a o 79 l ! m ( i o H C E 96th Ave ER NV (!2 DE N O E 88th A ve S R d E v l W 84th Ave F B F n E Rocky Mountain Arsenal d a J R d 36 i National Wildlife Refuge r ¤£ y t e e l h S 224 k S E 72nd Ave c W 72nd Ave n (! u o t t B S g n s i o h c s E 64th Ave e a 270 P W ¨¦§ E 58th Ave E 56th Ave d 85 d R R ¤£ d r n e R o w s n E 48th Ave 2 o d (! a T d u h R g H d 70 a k R n § c ¨¦ o b a b 225 u M l r a ¨¦§ C H n Palmer Av e u ve d G E 26th Ave x A fa R E Col h t 79 i (! r n ARAPAHOE P e Hwy 36 Adams County Buisness Soloutions Group 4430 South Adams County Parkway, 1st Floor 0 0.5 1 2 3 4 5 Water and Sanitation District Brighton, CO 80601 Tel: 720.523.6800 DISTRICT Box Elder Water and Bromley Park Metro Crestview Water and Greatrock North Water Horse Creek Metro North Washington Water Riverdale Peaks II Metro South Beebe Draw Metro www.adcogov.org/gis Miles Aberdeen Metro District 1 Sanitation District 6 Sanitation and Sanitation District and Sanitation District District Aberdeen Metro District 2 Brighton Crossing Metro Buffalo Ridge -

COMMUNITY PROFILE Boulder COLORADO

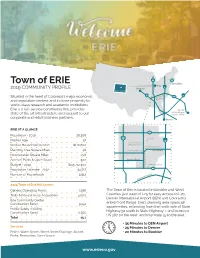

287 Town of ERIE Fort Collins Erie 25 2019 COMMUNITY PROFILE Boulder COLORADO 36 76 Situated in the heart of Colorado’s major economic 470 Northwest and population centers and in close proximity to Parkway world-class research and academic institutions, Erie is a full-service community that provides Denver International state of the art infrastructure and support to our Airport (DEN) corporate and retail business partners. Denver ERIE AT A GLANCE 52 Population - 2019 28,308 287 Town Hall Median Age 37 25 Erie Police Station Median Household Income $116,860 & Municipal Court Erie Community Library Planning Area Square Miles 48 Erie Community Center Erie Parkway Incorporated Square Miles 19.8 Acres of Parks & Open Space 300 Arapahoe Road Budget - 2019 $115,712,300 Erie Municipal Airport County Line Road Line County Population Estimate - 2032 34,717 7 Number of Households 9,912 Northwest Parkway 2019 Town of Erie Mill Levies: General Operating Funds 7.288 The Town of Erie is located in Boulder and Weld Trails & Natural Areas Acquisition 4.000 Counties, just west of I-25 for easy access to I-70, Denver International Airport (DEN) and Colorado’s Erie Community Center Construction Bond 3.252 entire Front Range. Erie’s planning area spans 48 square miles, extending from the north side of State Public Safety Building Highway 52 south to State Highway 7, and between Construction Bond 0.550 US 287 on the west and Interstate 25 to the east. Total 15.1 • 35 Minutes to DEN Airport Services • 25 Minutes to Denver Police, Water, Sewer, Street, Storm -

Adams County Community Needs Assessment Analysis of Existing Research Report

ADAMS COUNTY COMMUNITY NEEDS ASSESSMENT ANALYSIS OF EXISTING RESEARCH REPORT PREPARED BY: ABLE OF CONTENTS BACKGROUND AND INTRODUCTION ..............................................................................................................1 METHODOLOGY ..................................................................................................................................................1 SUMMARY OF FINDINGS .....................................................................................................................................2 MACRO-LEVEL FORCES IMPACTING ADAMS COUNTY ................................................................................5 A SNAPSHOT OF ADAMS COUNTY....................................................................................................................9 INCOME DISTRIBUTION .................................................................................................................................9 POVERTY...........................................................................................................................................................9 EMPLOYMENT PATTERNS............................................................................................................................10 INDUSTRIES IN ADAMS COUNTY................................................................................................................11 EDUCATIONAL ATTAINMENT.....................................................................................................................12 -

Lakewood, Colorado October 2013

Preliminary Feasibility Study Lakewood, Colorado October 2013 Prepared for SC SUSTAINABLE COMMUNITIES INITIATIVE DENVER REGIONAL COUNCIL OF GOVERNMENTS City of Lakewood 40 West Arts Denver Regional District Council of Governments ARTSPACE 250 Third Avenue N., Suite 500 Minneapolis, MN 55401 612.333.9012 www.artspace.org Introduction he City of Lakewood, Colorado, owes its name to a railroad man, W. A. H. Loveland, who platted its first lots in the 1880s. But it owes much of its mid-20th century T growth to America’s love of the automobile and the commercial activities that support the “love of the open road” lifestyle. Before the interstate system was built, U.S. Route 40 was the main drag between Denver and Salt Lake City, and it passed right through the heart of Lakewood on West Colfax Avenue. Although I-70 has supplanted U.S. 40 as the path of preference through the Rockies, West Colfax Avenue remains a major thoroughfare, and much of its historic character has survived. Indeed, to drive along West Looking west along Colfax Avenue in the late 1960s (Photo: Wikipedia Commons) Colfax Avenue today is to be reminded of an era when gas stations, roadside diners and indie motels were staples of the American landscape. But Lakewood itself has moved far past the 1950s. Today it has more than 140,000 residents and is the fifth largest city in Colorado, trailing only Denver, Colorado Springs, Aurora, and Fort Collins. A measure of its status is the new W light rail line, which opened earlier this year, connecting Union Station in downtown Denver to the Jefferson County Courthouse in Golden. -

Legal Resources: Custody & Divorce

Legal Resources: Custody & Divorce Jefferson County Jefferson County Domestic Clerk 720-772-2510 Can answer questions about filing a new case Most clinics require participants to bring appropriate forms, Self Help Desk which can be found at 720-772-2501 www.courts.state.co.us (Click 100 Jefferson County Pkwy, Golden, CO 80401 Room 1050 “Forms, then “Domestic/Family”) Assistance with general questions, court forms, resource referral, Jefferson County - page 1-2 policies and procedures, list of discounted attorneys and legal clinics as well as information about divorce/legal separation/custody. Other Counties (serving all areas) - page 2-5 Monday-Friday, 8:00 am -4 pm Domestic Violence - page 4-5 Family Law Clinic 720-772-2501 Internet Sites - page 5 100 Jefferson County Pkwy, Golden, CO 80401 *Some clinics are informational Website: only and do not provide legal advice, help completing forms, or This clinic is informational ONLY. It covers the process of divorce, legal legal representation. separation, dissolution of civil union, and APR Please contact Navigation for o Second Wednesday of each month, 12:00 pm-1:30 pm additional Domestic Violence o No reservations required legal resources as needed. o Located in Jury Assembly Office, 1st floor If you notice any changes or o Topics include: initial filings, temporary orders, separation inconsistencies with our agreements, parenting plans, maintenance/child support, custody, resources, please inform disclosure, sworn financial statements, and status conferences Navigation to help us -

National Register of Historic Places Registration Form

NFS Form 10-900 (Oct. 1990) OMB No. 10024-0018 United States Department of the Interior National Park Service National Register of Historic Places Registration Form This form is for use in nominating or requesting determination for individual ;wction in How to Complete the National Register of Historic Places Registration Form (National Regisfle , fete each item by marking "x" in the appropriate box or by entering the information requested. lfa#fl_ ply to the property being documented, enter "N/A" for "not applicable." For functions, architectural classi 1 and areas of significance, enter only categories and subcategories from the instructions, flace additi __ items on continuation sheets (NFS Form 10-900a). Use a typewriter, word processor! or com items. 1. Name of Property historic name Reno Park Addition__________ other names/site number 5JF1 942 2. Location street & number 7799-7899 W. 57th Ave.: 7801-7906 Grandview Ave.. N/A] not for publication 7800 and/884 :TaTston Kd.: bb'03-b/2U Yarrow St.: b/UT75723 Yukon St.; and b6U4-b/23 Zephyr St: city or town Arvada [N/A] vicinity state Colorado code CO county Jefferson code 059 zip code 80002 3. State/Federal Agency Certification As the designated authority under the National Historic Preservation Act, as amended, I hereby certify that this [ x ] nomination f ] request for determination of eligibility meets the documentation standards for registering properties in the National Register of Historic Places and meets the procedural and professional requirements set forth in 36 CFR Part 60. In my opinion, the property [ x ] meets [ ] does not meet the National Register criteria. -

Denver Federal Center Visitor Guide

GSA Rocky Mountain Region The Denver Federal Center Updated 2015-0903 visitor guide & map Hours of Operation Banking The Denver Federal Center (DFC) is open to the The Credit Union of Denver is located on the public from 6:00 a.m. to 6:00 p.m., Monday through lower floor of Building 67, and is open Tuesday and Friday, except federal holidays. After-hours admit- Thursday from 8:00 a.m. to 3:30 p.m. They can be tance must be authorized prior to required date. reached at 303.236.1700. Please call the DFC Service Center for further information at 303.236.1970. A US Bank branch and cash machine are located in Building 41 on the first floor. Open Monday through Visitor Access Friday from 7:00 a.m. to 4:00 p.m. For more informa- Kipling near Alameda Ave. Gate 1 tion on its services please call 303.237.2014. Lane 1 is for visitors, Lanes 2 and 3 are for employ- ees. Lane 2 is the 24 hr key card access on week- Public Transportation ends and after hours. Any weekend deliveries would Public bus transportation is available on the DFC come through Gate 1. Hours of operation are from through the Regional Transportation District (RTD). 6:00 a.m. to 6:00 p.m., Monday - Friday. It is the only For information on routes and schedules, call gate open on weekends. 303.299.6000 or visit the RTD Website at www.rtd- denver.com. Gate 2 Kipling and Center Ave. Employee access only and all deliveries are to come Safe & Secure through this gate during the week. -

June 2021 | Economic & Revenue Forecast

Colorado Legislative Council Staff June 2021 | Economic & Revenue Forecast June 18, 2021 June 2021 | Economic & Revenue Forecast Contents Executive Summary ........................................................................................................................................... 3 General Fund Budget Overview ...................................................................................................................... 5 TABOR Outlook ............................................................................................................................................... 15 General Fund Revenue .................................................................................................................................... 19 Cash Fund Revenue ......................................................................................................................................... 27 Economic Outlook ........................................................................................................................................... 37 Colorado Economic Regions .......................................................................................................................... 57 Appendix: Historical Data .............................................................................................................................. 82 Contributors Kate Watkins, Chief Economist Marc Carey Louis Pino Greg Sobetski Elizabeth Ramey Jeff Stupak David Hansen Anna Gerstle Christina Van Winkle Debbie Grunlien