Sanden Holdings Corp

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Defendants and Auto Parts List

Defendants and Parts List PARTS DEFENDANTS 1. Wire Harness American Furukawa, Inc. Asti Corporation Chiyoda Manufacturing Corporation Chiyoda USA Corporation Denso Corporation Denso International America Inc. Fujikura America, Inc. Fujikura Automotive America, LLC Fujikura Ltd. Furukawa Electric Co., Ltd. G.S. Electech, Inc. G.S. Wiring Systems Inc. G.S.W. Manufacturing Inc. K&S Wiring Systems, Inc. Kyungshin-Lear Sales And Engineering LLC Lear Corp. Leoni Wiring Systems, Inc. Leonische Holding, Inc. Mitsubishi Electric Automotive America, Inc. Mitsubishi Electric Corporation Mitsubishi Electric Us Holdings, Inc. Sumitomo Electric Industries, Ltd. Sumitomo Electric Wintec America, Inc. Sumitomo Electric Wiring Systems, Inc. Sumitomo Wiring Systems (U.S.A.) Inc. Sumitomo Wiring Systems, Ltd. S-Y Systems Technologies Europe GmbH Tokai Rika Co., Ltd. Tram, Inc. D/B/A Tokai Rika U.S.A. Inc. Yazaki Corp. Yazaki North America Inc. 2. Instrument Panel Clusters Continental Automotive Electronics LLC Continental Automotive Korea Ltd. Continental Automotive Systems, Inc. Denso Corp. Denso International America, Inc. New Sabina Industries, Inc. Nippon Seiki Co., Ltd. Ns International, Ltd. Yazaki Corporation Yazaki North America, Inc. Defendants and Parts List 3. Fuel Senders Denso Corporation Denso International America, Inc. Yazaki Corporation Yazaki North America, Inc. 4. Heater Control Panels Alps Automotive Inc. Alps Electric (North America), Inc. Alps Electric Co., Ltd Denso Corporation Denso International America, Inc. K&S Wiring Systems, Inc. Sumitomo Electric Industries, Ltd. Sumitomo Electric Wintec America, Inc. Sumitomo Electric Wiring Systems, Inc. Sumitomo Wiring Systems (U.S.A.) Inc. Sumitomo Wiring Systems, Ltd. Tokai Rika Co., Ltd. Tram, Inc. 5. Bearings Ab SKF JTEKT Corporation Koyo Corporation Of U.S.A. -

If You Bought Or Leased a New Vehicle Or Bought Certain Replacement Parts for a Vehicle in the U.S

If You Bought or Leased a New Vehicle or Bought Certain Replacement Parts for a Vehicle in the U.S. Since 1995 You Could Get Money From Settlements Totaling Approximately $1.04 Billion A Federal Court authorized this Notice. This is not a solicitation from a lawyer. • Please read this Notice and the Settlement Agreements available at www.AutoPartsClass.com carefully. Your legal rights may be affected whether you act or don’t act. This Notice is a summary, and it is not intended to, and does not, include all the specific details of each Settlement Agreement. To obtain more specific details concerning the Settlements, please read the Settlement Agreements. • Separate lawsuits claiming that Defendants in each lawsuit entered into unlawful agreements that artificially raised the prices of certain component parts of qualifying new vehicles (described in Question 8 below) have been settled with 56 Defendants and their affiliates (“Settling Defendants”). Previously, settlements with 23 of the Settling Defendants (“Round 1 Settlements” totaling approximately $225 million and “Round 2 Settlements” totaling approximately $379 million) received final Court approval. Now, additional settlements totaling approximately $432,823,040 have been reached with 33 Settling Defendants. These Settling Defendants are called the “Round 3 Settling Defendants,” and the settlements with them are called the “Round 3 Settlements.” This Notice will give you details of those proposed Round 3 Settlements and your rights in these lawsuits. • Generally, you are included in the Settlement Classes for the Round 3 Settlements if, at any time between 1995 and 2018, depending upon the component part, you: (1) bought or leased a qualifying new vehicle in the U.S. -

Auto Parts Canadian Settlements

AUTO PARTS CANADIAN SETTLEMENTS Settlement Amount Action Settled Defendant(s) (CDN) Approved Hearing Date (unless otherwise indicated) Air Conditioning DENSO Corporation et al $4,943,000 Feb 28/20 n/a Systems Panasonic Corporation et al $126,000 n/a May 13/21 Marelli Corporation (f/k/a $878,935.99 n/a May 13/21 Calsonic Kansei Corporation) et al Air Flow Meters Hitachi, Ltd., et al $725,000 May 1/17 n/a DENSO Corporation et al $150,000 Feb 28/20 n/a Alternators Hitachi, Ltd., et al $950,000 May 1/17 n/a Mitsubishi Electric $2,200,000 Sept 21/18 n/a Corporation et al DENSO Corporation et al $5,120,000 Feb 28/20 n/a ATF Warmers and Oil T.RAD Co., Ltd. et al $113,476.33 Jun 19/18 n/a Coolers DENSO Corporation et al $302,000 Feb 28/20 n/a Marelli Corporation (f/k/a $64,867.52 n/a May 13/21 Calsonic Kansei Corporation) et al Autolights Mitsuba Corporation et al $150,000 May 28/19 n/a Koito Manufacturing Co., $3,666,000 Aug 27/20 n/a Ltd. et al. Automotive Brake Hitachi Metals, Ltd. et al $175,000 Feb 28/20 n/a Hoses Toyoda Gosei Co., Ltd. $97,419.03 Aug 27/20 n/a Automotive Constant- Toyo Tire & Rubber Co., $258,969.19 Aug 27/20 n/a Velocity-Joint Boot Ltd. et al Products Toyoda Gosei Co., Ltd. $105,846.66 Aug 27/20 n/a Automotive Exhaust DENSO Corporation et al $150,000 Feb 28/20 n/a Systems NGK Spark Plugs (U.S.A.), $66,510 Feb 28/20 n/a Inc., et al Eberspächer Gruppe GmbH $190,000 Aug 27/20 n/a & Co. -

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

Autodesk W Branży Motoryzacyjnej

Autodesk w Branży Motoryzacyjnej Name Surname Job Title Image courtesy of Local Motors Inc. Idea Koncepcja Wizualizacja Ergonomia Konstrukcja i optymalizacja Symulacja Organizacja procesu produkcyjnego Marketing 14 GENERAL MOTORS CORPORATION EXEDY CORPORATION IMABARI SHIPBUILDING CO.,LTD. WERNER BAIER UND GERHARD MEY TOYOTA MOTOR CORPORATION TSUNEISHI SHIPBUILDING COMPANY CENTRAL JAPAN RAILWAY COMPANY AMSTED INDUSTRIES INCORPORATED HONDA MOTOR CO., LTD. MAZDA MOTOR CORPORATION LINAMAR CORPORATION MITSUBISHI MOTORS AUSTRALIA LIMITED MITSUBISHI HEAVY INDUSTRIES, LTD. GENERAL ELECTRIC COMPANY CHINA SHIPBUILDING INDUSTRY CORPORATION CHINA STATE SHIPBUILDING CORPORATION MICHELIN ET CIE GM DAEWOO AUTO & TECHNOLOGY COMPANY NAMURA SHIPBUILDING CO.,LTD. KEIHIN CORPORATION NORTHROP GRUMMAN CORPORATION SIEMENS AG AUSTAL USA, LLC AKEBONO BRAKE INDUSTRY CO., LTD. FORD MOTOR COMPANY VALEO MAG IAS HOLDINGS, INC. COOPER-STANDARD HOLDINGS, INC. HYUNDAI HEAVY INDUSTRIES CO., LTD. L-3 COMMUNICATIONS HOLDINGS, INC. KOREA DELPHI AUTOMOTIVE SYSTEMS CENTRAL MOTOR CO.,LTD. ROBERT BOSCH GMBH DANA HOLDING CORPORATION STELLA VERM?GENSVERWALTUNGS GMBH L?RSSEN MARITIME BETEILIGUNGEN GMBH. VOLKSWAGEN AG SUZUKI MOTOR CORPORATION REPUBBLICA ITALIANA CHINA COMMUNICATIONS CONSTRUCTION KUBOTA CORPORATION SEMBCORP INDUSTRIES LTD THAI SUMMIT AUTOPARTS INDUSTRY COMPANY PARKER -HANNIFIN CORPORATION FIAT SPA ROLLS-ROYCE GROUP PLC NAVISTAR INTERNATIONAL CORPORATION DCNS MAGNA INTERNATIONAL INC AB VOLVO PRESCO, Y.K. JUNGHEINRICH AG BRIDGESTONE CORPORATION CKD CORPORATION UNITED TECHNOLOGIES CORPORATION MITSUBA CORPORATION CONTINENTAL AG NIENPAL EMPREENDIMENTOS E PARTICIPACOES YAZAKI CORPORATION YOKOHAMA RUBBER COMPANY, LIMITED, THE DAIMLER AG FUJI HEAVY INDUSTRIES LTD. BENTELER AG MUSASHI SEIMITSU INDUSTRY CO., LTD. STX OFFSHORE & SHIPBUILDING CO., LTD. SHANGHAI AUTOMOTIVE INDUSTRY CORP ABEKING & RASMUSSEN SCHIFFS- UND ALLISON TRANSMISSION, INC. NISSAN MOTOR CO., LTD. BROSE FAHRZEUGTEILE GMBH & CO. KG ODIM ASA STICHTING ADMINISTRATIEKANTOOR HUISMAN MITSUBISHI MOTORS CORPORATION HARLEY-DAVIDSON, INC. -

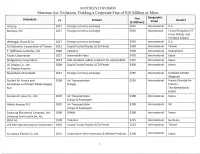

Auto Parts Canadian Settlements

AUTO PARTS CANADIAN SETTLEMENTS Settlement Amount Action Settled Defendant(s) (CDN) Approved Hearing Date (unless otherwise indicated) Air Conditioning DENSO Corporation et al $4,943,000 Feb 28/20 n/a Systems Air Flow Meters Hitachi, Ltd., et al $725,000 May 1/17 n/a DENSO Corporation et al $150,000 Feb 28/20 n/a Alternators Hitachi, Ltd., et al $950,000 May 1/17 n/a Mitsubishi Electric $2,200,000 Sept 21/18 n/a Corporation et al DENSO Corporation et al $5,120,000 Feb 28/20 n/a ATF Warmers and Oil T.RAD Co., Ltd. et al $113,476.33 Jun 19/18 n/a Coolers DENSO Corporation et al $302,000 Feb 28/20 n/a Autolights Mitsuba Corporation et al $150,000 May 28/19 n/a Koito Manufacturing Co., $3,666,000 n/a Aug 27/20 Ltd. et al. Automotive Brake Hitachi Metals, Ltd. et al $175,000 Feb 28/20 n/a Hoses Toyoda Gosei Co., Ltd. $97,419.03 n/a Aug 27/20 Automotive Constant- Toyo Tire & Rubber Co., $258,969.19 n/a Aug 27/20 Velocity-Joint Boot Ltd. et al Products Toyoda Gosei Co., Ltd. $105,846.66 n/a Aug 27/20 Automotive Exhaust DENSO Corporation et al $150,000 Feb 28/20 n/a Systems NGK Spark Plugs (U.S.A.), $66,510 Feb 28/20 n/a Inc., et al Eberspächer Gruppe GmbH $190,000 n/a Aug 27/20 & Co. et al Meritor, Inc. $141,361 n/a Aug 27/20 Tenneco Inc. -

Mitsuba Information

UNITED STATES DISTRICT COURT EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION UNITED STATES OF AMERICA, v. Violations: MITSUBA CORPORATION Count I: 15 U.S.C. § 1 Count II: 18 U.S.C. § 1519 Defendant. __________________________________/ INFORMATION COUNT ONE CONSPIRACY TO RESTRAIN TRADE (15 U.S.C. § 1) THE UNITED STATES, ACTING THROUGH ITS ATTORNEYS, CHARGES: Defendant and Co-Conspirators 1. Mitsuba Corporation (“Defendant”) is a corporation organized and existing under the laws of Japan with its principal place of business in Gunma, Japan. During the period covered by this Count, Defendant was engaged in the business of manufacturing and selling various automotive parts, including windshield wiper systems and components thereof, windshield washer systems and components thereof, starter motors, power window motors, and fan motors to Honda Motor Company Ltd., Fuji Heavy Industries Ltd., Nissan Motor Company Ltd., Toyota Motor Corporation, and Chrysler Group, LLC, and certain of their subsidiaries, affiliates, suppliers and others (collectively, “automobile manufacturers”) for installation in vehicles manufactured and sold in the United States and elsewhere. 2. Various corporations and individuals, not made defendants in this Count, participated as co-conspirators in the offense charged in this Count and performed acts and made statements in furtherance of it. 3. Whenever in this Count reference is made to any act, deed, or transaction of any corporation, the allegation means that the corporation engaged in the act, deed, or transaction by or through its officers, directors, employees, agents, or other representatives while they were actively engaged in the management, direction, control, or transaction of its business or affairs. Background of the Offense 4. -

MITSUBA Corporation Overview of Business Activities

Briefing on Business Results for FY Mar 2019 May 31, 2019 MITSUBA Corporation Overview of Business Activities 1. Industry Trends 2. Results for FY03/2019 3. Forecast for FY03/2020 * Results for FY03/2018 represent the 12-month closing figures in this report. <3> ■Summary of Business Results for FY03/2019 Sales and Income decreased due to a decline in passenger car sales in the North American market, as well as the high cost of dealing with quality defects and the impact of additional tariffs imposed as a result of the U.S.–China trade dispute. Consolidated Sales and Operating Income (JPY Bln) (JPYBln) Sales Operating Income Sales(1H) Sales(2H) Operating Income(Full Year) Operating Income(1H) 400.0 30.0 327.9 338.0 333.2 335.0 25.0 300.0 22.6 20.0 168.7 175.0 168.8 171.0 200.0 15.0 14.4 12.0 10.6 10.9 10.0 100.0 6.8 6.1 5.0 5.0 159.2 163.0 164.4 164.0 0.0 0.0 FY03/2017 FY03/2018 FY03/2019 FY03/2020 (Forecast) <4> 1. Industry Trends (1) Global automobile production volume forecast The Chinese market is expected to recover due to the government's subsidy policy, leading to a rebound in overall production. Unit: million cars 100.0 95.2 92.8 93.7 2.6 2.4 2.4 9.2 9.3 9.2 13.2 13.4 13.7 20.4 20.3 20.5 50.0 22.3 21.6 21.5 27.5 25.8 26.4 0.0 FY03/2018 FY03/2019 FY03/2020 China Europe Americas Asia Japan Others <5> 1. -

Automotive Hoses Class Action Complaint

2:15-cv-12893-MOB-MKM Doc # 1 Filed 08/14/15 Pg 1 of 98 Pg ID 1 REDACTED UNITED STATES DISTRICT COURT EASTERN DISTRICT OF MICHIGAN ) HALLEY ASCHER, GREGORY ASKEN, ) No. MELISSA BARRON, KIMBERLY BENNETT, ) DAVID BERNSTEIN, RON BLAU, TENISHA ) BURGOS, KENT BUSEK, JENNIFER CHASE, ) CLASS ACTION COMPLAINT FOR RITA CORNISH, NATHAN CROOM, LORI ) DAMAGES AND INJUNCTIVE CURTIS, JESSICA DECASTRO, ALENA ) RELIEF FARRELL, JANE FITZGERALD, CARROLL ) GIBBS, DORI GILELS, JASON GRALA, IAN ) GROVES, CURTIS GUNNERSON, PAUL ) JURY TRIAL DEMANDED GUSTAFSON, TOM HALVERSON, CURTIS ) HARR, ANDREW HEDLUND, GARY ARTHUR ) [REDACTED] HERR, JOHN HOLLINGSWORTH, LEONARD ) JULIAN, CAROL ANN KASHISHIAN, ) ELIZABETH KAUFMAN, ROBERT ) KLINGLER, KELLY KLOSTERMAN, JAMES ) MAREAN, NILSA MERCADO, REBECCA ) LYNN MORROW, EDWARD MUSCARA, ) STACEY NICKELL, SOPHIE O’KEEFE- ) ZELMAN, ROGER OLSON, SUSAN OLSON, ) WILLIAM PICOTTE, WHITNEY PORTER, ) CINDY PRINCE, JANNE RICE, ROBERT RICE, ) JR., FRANCES GAMMELL-ROACH, DARREL ) SENIOR, MEETESH SHAH, DARCY ) SHERMAN, ERICA SHOAF, ARTHUR ) STUKEY, KATHLEEN TAWNEY, JANE ) TAYLOR, KEITH UEHARA, MICHAEL WICK, ) THOMAS WILSON, PHILLIP YOUNG, on ) Behalf of Themselves and all Others Similarly ) Situated, ) ) Plaintiffs, ) vs. ) ) TOYODA GOSEI CO., LTD., TOYODA GOSEI ) NORTH AMERICA CORPORATION, TG ) KENTUCKY, LLC, TG FLUID SYSTEMS USA ) CORPORATION, SUMITOMO RIKO ) COMPANY LIMITED, DTR INDUSTRIES, INC. Defendants. 2:15-cv-12893-MOB-MKM Doc # 1 Filed 08/14/15 Pg 2 of 98 Pg ID 2 REDACTED Plaintiffs Halley Ascher, Gregory Asken, Melissa Barron, -

Automotive Hoses Consolidated Amended Class Action Complaint

UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION IN RE AUTOMOTIVE PARTS : 12-md-02311 ANTITRUST LITIGATION : Honorable Marianne O. Battani : : : : : IN RE: AUTOMOTIVE HOSES : 2:15-cv-03203-MOB-MKM : : THIS DOCUMENT RELATS TO: : : CONSOLIDATED AMENDED CLASS END-PAYOR ACTION : ACTION COMPLAINT : : JURY TRIAL DEMANDED : : [REDACTED] : REDACTED Plaintiffs Halley Ascher, Gregory Asken, Melissa Barron, Kimberly Bennett, David Bernstein, Ron Blau, Tenisha Burgos, Kent Busek, Jennifer Chase, Rita Cornish, Nathan Croom, Lori Curtis, Jessica Decastro, Theresia Dillard, Alena Farrell, Jane Fitzgerald, Carroll Gibbs, Dori Gilels, Jason Grala, Ian Groves, Curtis Gunnerson, Paul Gustafson, Tom Halverson, Curtis Harr, Andrew Hedlund, Gary Arthur Herr, John Hollingsworth, Carol Ann Kashishian, Elizabeth Kaufmann, Robert Klingler, Kelly Klosterman, James Marean, Rebecca Lynn Morrow, Edward Muscara, Stacey Nickell, Sophie O’Keefe-Zelman, Roger Olson, William Picotte, Whitney Porter, Cindy Prince, Janne Rice, Robert Rice, Jr., Frances Gammell-Roach, Darrel Senior, Meetesh Shah, Darcy Sherman, Erica Shoaf, Arthur Stukey, Kathleen Tawney, Jane Taylor, Keith Uehara, Michael Wick, and Phillip Young (“Plaintiffs”), on behalf of themselves and all others similarly situated (the “Classes” as defined below), upon personal knowledge as to the facts pertaining to themselves and upon information and belief as to all other matters, and based on the investigation of counsel, bring this class action for damages, injunctive relief, and -

International Corporate Investments in Ohio Operations

Research Office A State Affiliate of the U.S. Census Bureau International Corporate Investment in Ohio Operations 20 September 2007 June 20 June 2020 Table of Contents Introduction and Explanations Section 1: Maps Section 2: Alphabetical Listing by Company Name Section 3: Companies Listed by Country of Ultimate Parent Section 4: Companies Listed by County Location International Corporate Investment in Ohio Operations June 2020 THE DIRECTORY OF INTERNATIONAL CORPORATE INVESTMENT IN OHIO OPERATIONS is a listing of international enterprises that have an investment or managerial interest within the State of Ohio. The report contains graphical summaries of international firms in Ohio and alphabetical company listings sorted into three categories: company name, country of ultimate parent, and county location. The enterprises listed in this directory have 5 or more employees at individual locations. This directory was created based on information obtained from Dun & Bradstreet. This information was crosschecked against company Websites and online corporate directories such as ReferenceUSA®. There is no mandatory state filing of international status. When using this directory, it is important to recognize that global trade and commerce are dynamic and in constant flux. The ownership and location of the companies listed is subject to change. Employment counts may differ from totals published by other sources due to aggregation, definition, and time periods. Research Office Ohio Development Services Agency P.O. Box 1001, Columbus, Ohio 43266-1001 Telephone: (614) 466-2116 http://development.ohio.gov/reports/reports_research.htm International Investment in Ohio - This survey identifies 4,303 international establishments employing 269,488 people. - Companies from 50 countries were identified as having investments in Ohio. -

Sherman Act Violations Yielding a Corporate Fine of $10 Million Or More

ANTITRUST DIVISION Sherman Act Violations Yielding a Corporate Fine of $10 Million or More Fine Geographic Defendant FY Product Country ($ Millions S cop e Citicorp 2017 Foreign currency exchange $925 International U.S. Barclays, PLC 2017 Foreign currency exchange $650 International United Kingdom Of Great Britain And Northern Ireland JPMorgan Chase & Co. 2017 Foreign currency exchange $550 International U.S. AU Optronics Corporation of Taiwan 2012 Liquid Crystal Display (LCD) Panels $500 International Taiwan F. Hoffmann-La Roche, Ltd. 1999 Vitamins $500 International Switzerland Yazaki Corporation 2012 Automobile Parts $470 International Japan Bridgestone Corporation 2014 Anti-vibration rubber products for automobiles $425 International Japan LG Display Co., Ltd 2009 Liquid Crystal Display (LCD) Panels $400 International Korea LG Display America Royal Bank of Scotland 2017 Foreign currency exchange $395 International Scotland (United Kingdom) Societe Air France and 2008 Air Transportation $350 International France (Societe-Air Koninklijke Luchtvaart Maatschappij, (Cargo) France) N.V. The Netherlands (KLM) Korean Air Lines Co., Ltd. 2007 Air Transportation $300 International Korea (Cargo & Passenger) British Airways PLC 2007 Air Transportation $300 International UK (Cargo & Passenger) Samsung Electronics Company, Ltd. 2006 DRAM $300 International Korea Samsung Semiconductor, Inc. BASF AG 1999 Vitamins $225 International Germany CHI MEI Optoelectronics Corporation 2010 Liquid Crystal Display (LCD) Panels $220 International Taiwan Furukawa Electric Co. Ltd. 2012 Automotive Wire Harnesses & Related Products $200 International Japan 1 ANTITRUST DIVISION Shetrnan Act Violations Yielding a Corporate Fine of $10 Million or More Fine Geographic Defendant FY Product Country ($ Millions) Scop e Hitachi Automotive Systems, Ltd 2014 Automotive Wire Harnesses & Related Products $195 International Japan Mitsubishi Electric Corporation 2014 Automotive Wire Harnesses and Electronic $190 International Japan Components Hynix Semiconductor Inc.