Valuinsight – Why Microsoft Might Really Get Bigger Than the Entire UK Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Portfolio Activity Q3 2018

Portfolio Activity Q3 2018 By Louis S. Foxwell, Research Analyst The following discussion mentions stocks that are widely — but not universally — held by clients of Horan Capital Management. Client portfolios are customized, so this commentary may or may not be directly applicable to any given client or account. Our intention is to provide general insight into portfolio holdings and into our overall approach and to highlight situations of interest, both positive and negative. The mention of any stock is neither advice nor a solicitation to buy or sell any particular investment and our opinions regarding securities are subject to change without notice. Investing involves risk of loss. See the legal disclosures at the end of this publication and on our website for more information. BUYS Booking Holdings Inc. (BKNG) Booking Holdings (formerly known as Priceline) operates as an Online Travel Agency (“OTA”). The company’s online platforms facilitate business transactions between travelers and hotels/airlines/rental car services. In most cases, Booking acts as a platform and receives a commission for lending its network to travelers and businesses. In other cases, Booking will act as the facilitator of payments, buying rooms in bulk and selling them individually at a profit. The company also generates advertising revenue on select platforms. Most of Booking’s revenue is generated in Europe where boutique hotels are commonplace and there is very little consolidation in the hotel industry. This lack of consolidation makes smaller hotels dependent on Booking’s services, giving the company a wide economic moat. The company has a pristine balance sheet, with net cash and investments. -

Booking Holdings (Nasdaq: BKNG) Sector: Consumer Discretionary

Booking Holdings (Nasdaq: BKNG) Sector: Consumer Discretionary Target Current 52 Week 52 Week P/E Market Dividend Beta Price Price High Low Cap Yield $2,152.00 $1,732.13 $1,592.45 $1,592.45 17.37 70.82B - 0.96 Business Overview: 10 Year Stock Performance: Booking Holdings is a world leader in online travel and related services. They provide to customers and partners in over 230 countries and territories in over 40 languages. They operate through six brands; Booking.com, Kayak, Priceline, RentalCars.com, Agoda, and OpenTable. Revenues are collected through three primary business segments; agency revenues, merchant revenues, and advertising & other revenues. Risks: Industry Outlook: One of the most prevalent risks during this time The travel industry is the second fastest is the Corona Virus. The spread and severity of growing sector in the world at a 3.9% CAGR. this virus has caused travelers to be more Travel demand is driven by consumer cautious when planning trips. In fact, there are spending, health of the economy, and advances certain countries that the CDC has prohibited in information technology. The sector is seeing U.S. citizens from making any non-essential a shift to more bookings on mobile platforms as travel to. Although Booking has already seen technology continues to develop and increased cancellations and decreases in future e-commerce grows. room bookings in affected areas, they have been through situations like this before. There Management: is no definite timeline of the virus, but they are ● Glenn D. Fogel- CEO confident in their capabilities to bounce back ● David I. -

Booking Holdings, Inc.'S (BKNG) CEO Glenn Fogel on Q4 2020 Results - Earnings Call Transcript | Seeking Alpha

2/26/2021 Booking Holdings, Inc.'s (BKNG) CEO Glenn Fogel on Q4 2020 Results - Earnings Call Transcript | Seeking Alpha Transcripts Services Booking Holdings, Inc.'s (BKNG) CEO Glenn Fogel on Q4 2020 Results - Earnings Call Transcript Feb. 24, 2021 11:48 PM ET | Booking Holdings Inc. (BKNG) SA Transcripts Follow 111.66K Followers | Bio Q4: 2021-02-24 Earnings Summary 10-K EPS of -$0.57 beats by $3.65 | Revenue of $1.24B (-62.92% Y/Y) beats by $76.86M Booking Holdings, Inc. (NASDAQ:BKNG) Q4 2020 Results Earnings Conference Call February 24, 2021 4:30 PM ET Company Participants Glenn Fogel - President and CEO David Goulden - Chief Financial Officer Conference Call Participants Lloyd Walmsley - Deutsche Bank Justin Post - Bank of America Kevin Kopelman - Cowen Eric Sheridan - UBS Doug Anmuth - JPMorgan Naved Khan - Truist Securities Stephen Ju - Credit Suisse Mario Lu - Barclays Jason Bazinet - Citi https://seekingalpha.com/article/4408829-booking-holdings-inc-s-bkng-ceo-glenn-fogel-on-q4-2020-results-earnings-call-transcript 1/29 2/26/2021 Booking Holdings, Inc.'s (BKNG) CEO Glenn Fogel on Q4 2020 Results - Earnings Call Transcript | Seeking Alpha Operator Welcome to Booking Holdings Fourth Quarter 2020 Conference Call. Booking Holdings would like to remind everyone that this call may contain forward-looking statements, which are made pursuant to the Safe Harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are not guarantees of future performance and are subject to certain risks, uncertainties and assumptions that are difficult to predict. Therefore, actual results may differ materially from those expressed, implied or forecasted in any such forward-looking statements. -

Mainstay WMC Growth Fund Q1 Holdings

MainStay MacKay Growth Fund Portfolio of Investments January 31, 2021† (Unaudited) Shares Value Common Stocks 99.9% Aerospace & Defense 0.1% Huntington Ingalls Industries, Inc. 3,791 $ 596,438 Air Freight & Logistics 0.6% United Parcel Service, Inc., Class B 32,175 4,987,125 Automobiles 3.2% (a) Tesla, Inc. 32,810 26,035,719 Beverages 0.3% Coca-Cola Co. (The) 17,778 856,011 PepsiCo, Inc. 14,841 2,026,835 2,882,846 Biotechnology 5.7% AbbVie, Inc. 31,475 3,225,558 Alkermes plc (a) 125,474 2,633,699 Amgen, Inc. 45,353 10,949,575 Biogen, Inc. (a) 19,841 5,607,265 Exelixis, Inc. (a) 222,526 4,942,303 Gilead Sciences, Inc. 8,818 578,461 Incyte Corp. (a) 43,832 3,933,922 Moderna, Inc. (a) 12,659 2,192,032 Regeneron Pharmaceuticals, Inc. (a) 13,324 6,713,164 Seagen, Inc. (a) 12,671 2,081,465 United Therapeutics Corp. (a) 10,649 1,744,519 Vertex Pharmaceuticals, Inc. (a) 7,737 1,772,392 46,374,355 Capital Markets 0.8% Lazard Ltd., Class A 41,097 1,693,196 LPL Financial Holdings, Inc. 43,402 4,702,173 6,395,369 Construction & Engineering 0.6% Quanta Services, Inc. 65,450 4,612,261 Consumer Finance 0.5% SLM Corp. 322,393 4,474,815 Diversified Consumer Services 0.0%‡ Graham Holdings Co., Class B 691 392,564 Electronic Equipment, Instruments & Components 0.5% Jabil, Inc. 97,473 4,032,458 Shares Value Common Stocks Entertainment 2.0% (a) Lions Gate Entertainment Corp., Class B 263,020 $ 3,250,927 Netflix, Inc. -

Polen Focus Growth Strategy

PORTFOLIO MANAGER COMMENTARY First Quarter 2018 POLEN FOCUS GROWTH STRATEGY Key Takeaways • During the first quarter of 2018, the Polen Focus Growth Composite Portfolio (the “Port- folio”) returned +3.41% gross of fees compared to +1.42% for the Russell 1000 Growth Index and -0.76% for the S&P 500 Index. • Our strong outperformance was driven by primarily what we own, but we also benefited from what we do not own. Company specific positives came from Adobe, Booking Hold- ings (formerly Priceline) and two of our healthcare companies: Align and Zoetis. From Dan Davidowitz, CFA a sector perspective, our lack of exposure to energy, materials and telecom companies Head of the Large Company also aided our relative performance. Growth Team & Portfolio Manager • Portfolio activity in the first quarter was higher than normal, although most of the changes were incremental adds and trims, with no new purchases in the quarter and only one outright sale. • Looking at the macroeconomic backdrop, there are some positive forces already in mo- tion such as accelerating GDP growth in the United States and abroad as well as lower tax rates coming to U.S. individuals and corporations. There are also risks to the current growth acceleration, namely the potential for protectionist trade wars and tariffs as well as higher interest rates. • For the first time in many years, there finally seems to be strong corporate earnings Damon Ficklin growth in the United States. For the full-year 2017, we calculated S&P 500 earnings Portfolio Manager growth was about 17%, well above its long-term annual average of approximately 7%, & Analyst and the highest it has been since 2010. -

OTA & Travel Distribution Update: Hopper Focuses on Hotel Bookings

Duff on Hospitality Law OTA & Travel Distribution Update: Hopper focuses on hotel bookings; Amazon's re-entry into travel; Facebook cryptocurrency a possible travel payment solution By Greg Duff on 6.28.19 | Posted in OTA Update Hopper Focuses on Hotel Bookings ("Hopper ramps up hotel booking with global private rates and price tracking," Phocus Wire on Jun 20, 2019 Over the past few years, we have featured a number of stories about Hopper and its many successes – though primarily in airline bookings. Now, Hopper is seeking to leverage some of that success in its pursuit of hotel bookings. Hopper currently features over 270,000 hotels worldwide and sources rooms from those hotels through both intermediaries and direct supplier relationships. Armed with its price predictive technology, Hopper claims to be able to provide users accurate rate forecasts for the hotels it features as well as unique “private” rates that are otherwise unavailable. Unlike typical booking channels, which generally promote and market their offerings broadly, Hopper derives 90% of its bookings through personalized “private” push notifications that are powered by Hopper’s personalization AI. Amazon’s Re-Entry Into Travel ("Alexa, how can I fly to Mumbai?," Reuters Technology on Jun 20, 2019) The recent news that Amazon has re-entered the travel industry has some in the airline industry concerned. Just when airlines were beginning to make demonstrable progress in creating direct booking relationships with its customers (and bypassing the many intermediaries who seek to control those relationships and charge handsomely for their services), along comes Amazon. While airlines such as AirAsia and easyJet are busy diversifying their products and services, many airlines are ill prepared. -

Portfolio Holdings Listing Select Consumer Discretionary Portfolio DUMMY As of August 31, 2021

Portfolio Holdings Listing Select Consumer Discretionary Portfolio DUMMY as of August 31, 2021 The portfolio holdings listing (listing) provides information on a fund’s investments as of the date indicated. Top 10 holdings information (top 10 holdings) is also provided for certain equity and high income funds. The listing and top 10 holdings are not part of a fund’s annual/semiannual report or Form N-Q and have not been audited. The information provided in this listing and top 10 holdings may differ from a fund’s holdings disclosed in its annual/semiannual report and Form N-Q as follows, where applicable: With certain exceptions, the listing and top 10 holdings provide information on the direct holdings of a fund as well as a fund’s pro rata share of any securities and other investments held indirectly through investment in underlying non- money market Fidelity Central Funds. A fund’s pro rata share of the underlying holdings of any investment in high income and floating rate central funds is provided at a fund’s fiscal quarter end. For certain funds, direct holdings in high income or convertible securities are presented at a fund’s fiscal quarter end and are presented collectively for other periods. For the annual/semiannual report, a fund’s investments include trades executed through the end of the last business day of the period. This listing and the top 10 holdings include trades executed through the end of the prior business day. The listing includes any investment in derivative instruments, and excludes the value of any cash collateral held for securities on loan and a fund’s net other assets. -

Booking Holdings Inc. Pitch

RESEARCHSeptember REPORT24, 2018 ASeptember Travel Industry 24, 2018 Leader Stock Rating BUY Price Target USD $2,547 Bear Price Bull Case Target Case $2,343 $2,547 $2,793 Ticker BKNG Booking Holdings Inc. Market Cap (MM) $92,890 A Travel Industry Leader EV / EBITDA 16.5x P / E 22.8x Booking Holdings operates several Online Travel Agencies (OTAs), including Booking.com, as well as meta-search websites, including 52 Week Performance KAYAK. 130 The company generated $12.4B of gross profit in 2017 with a 39.4% EBITDA margin. Booking Holdings is a high return business with secular growth trends, the potential for improved margins, and a competent management team. 115 Investment Thesis – Three long-term trends pave the runway for growth. 100 – Travel bookings are shifting from offline to online. – Millennials increasingly desire to travel. 85 – A rising middle-class in Asia will add new global travel 01-Sep-17 18-Feb-18 07-Aug-18 customers. BKNG S&P 100 Index – Two strong competitive advantages and an emerging third. – As the leader, the company benefits from economies of Consumers & Healthcare scale. Andrei Florescu – Network effects between customers and listings derive an unmatched value proposition. [email protected] – To generate higher returns, the company is working to Ioulia Malamoud create a brand competitive advantage. [email protected] – Glenn Fogel (CEO) is intelligent and aligned with investors. Connor Steckly [email protected] The information in this document is for EDUCATIONAL and NON-COMMERCIAL use only and is not intended to Bronwyn Ferris constitute specific legal, accounting, financial or tax advice for any individual. -

Monthly Holdings: U.S. Large Cap Equity Strategy

J.P. Morgan U.S. Large Cap Equity Strategy As of August 31, 2021 Sector Ticker Security Name Percent Autos & Transportation UNP UNION PACIFIC CORP 1.23% NSC NORFOLK SOUTHERN CORP 1.50% Autos & Transportation Sub Total 2.74% Basic Materials PPG PPG INDUSTRIES INC 0.86% LIN LINDE PLC 2.18% Basic Materials Sub Total 3.05% Big Banks & Brokers BAC BANK OF AMERICA CORP 1.29% SCHW SCHWAB (CHARLES) CORP 1.31% AXP AMERICAN EXPRESS CO 1.64% WFC WELLS FARGO & CO 1.88% MS MORGAN STANLEY 2.29% Big Banks & Brokers Sub Total 8.41% CASH & CASH EQUIVALENTS USD United States Dollar 1.07% CASH & CASH EQUIVALENTS Sub Total 1.07% Consumer Cyclical HLT HILTON WORLDWIDE HOLDINGS IN 0.77% BKNG BOOKING HOLDINGS INC 1.46% Consumer Cyclical Sub Total 2.23% Consumer Stable MDLZ MONDELEZ INTERNATIONAL INC-A 0.80% PEP PEPSICO INC 1.11% Consumer Stable Sub Total 1.91% Energy COP CONOCOPHILLIPS 0.59% PXD PIONEER NATURAL RESOURCES CO 0.91% Energy Sub Total 1.49% Financial Services WEX WEX INC 0.96% FISV FISERV INC 1.52% PYPL PAYPAL HOLDINGS INC 2.45% MA MASTERCARD INC - A 2.53% Financial Services Sub Total 7.47% Health Services & Systems UNH UNITEDHEALTH GROUP INC 2.77% Health Services & Systems Sub Total 2.77% Industrial Cyclical SWK STANLEY BLACK & DECKER INC 0.67% AME AMETEK INC 0.74% DE DEERE & CO 0.88% WCN WASTE CONNECTIONS INC 0.91% IR Ingersoll Rand INC COMMON STOCK 0.99% ETN EATON CORP PLC 1.06% J.P. Morgan U.S. -

Virtus Silvant Large-Cap Growth Stock Fund

Virtus Silvant Large-Cap Growth Stock Fund as of : 08/31/2021 (Unaudited) SECURITY SHARES TRADED MARKET VALUE % OF PORTFOLIO Microsoft Corp 52,609 $15,881,605 11.20 % Apple Inc 98,552 $14,963,150 10.56 % Amazon.com Inc 3,103 $10,769,861 7.60 % Facebook Inc 16,981 $6,442,252 4.55 % Alphabet, Inc.- Cl C 2,199 $6,397,419 4.51 % Alphabet, Inc.- Cl A 2,129 $6,161,220 4.35 % NVIDIA Corp 26,448 $5,920,385 4.18 % Visa Inc 21,825 $5,000,108 3.53 % PayPal Holdings Inc 11,231 $3,241,940 2.29 % UnitedHealth Group Inc 7,093 $2,952,603 2.08 % Costco Wholesale Corp 6,309 $2,873,686 2.03 % Mastercard Inc 7,632 $2,642,427 1.86 % Eli Lilly & Co 10,190 $2,631,975 1.86 % QUALCOMM Inc 17,626 $2,585,558 1.82 % Estee Lauder Cos Inc/The 6,642 $2,261,535 1.60 % Applied Materials Inc 16,213 $2,190,863 1.55 % O'Reilly Automotive Inc 3,640 $2,162,451 1.53 % Autodesk Inc 6,524 $2,023,027 1.43 % TJX Cos Inc/The 27,548 $2,003,291 1.41 % Boeing Co/The 9,075 $1,991,963 1.41 % Edwards Lifesciences Corp 16,997 $1,991,708 1.41 % 1 SECURITY SHARES TRADED MARKET VALUE % OF PORTFOLIO salesforce.com Inc 7,205 $1,911,270 1.35 % Deere & Co 4,672 $1,766,156 1.25 % Workday Inc 6,420 $1,753,687 1.24 % Mettler-Toledo International Inc 1,104 $1,714,324 1.21 % Dexcom Inc 3,073 $1,626,908 1.15 % Intuitive Surgical Inc 1,519 $1,600,358 1.13 % Comcast Corp 22,760 $1,381,077 0.97 % Equinix Inc 1,528 $1,288,792 0.91 % Twilio Inc 3,600 $1,285,056 0.91 % Booking Holdings Inc 549 $1,262,519 0.89 % American Express Co 7,604 $1,261,960 0.89 % Chipotle Mexican Grill Inc 649 $1,235,261 0.87 % IHS -

Usaa Fund Holdings Usaa Nasdaq-100 Index Fund

USAA FUND HOLDINGS As of June 30, 2021 USAA NASDAQ-100 INDEX FUND CUSIP TICKER SECURITY NAME SHARES/PAR/CONTRACTS MARKET VALUE 00507V109 ATVI ACTIVISION BLIZZARD INC 229,531.00 21,906,438.64 00724F101 ADBE ADOBE INC 141,201.00 82,692,953.64 007903107 AMD ADVANCED MICRO DEVICES 358,915.00 33,712,885.95 015351109 ALXN ALEXION PHARMACEUTICALS 65,289.00 11,994,242.19 016255101 ALGN ALIGN TECHNOLOGY INC 23,377.00 14,283,347.00 02079K107 GOOG ALPHABET INC - CLASS C 62,814.00 157,431,984.48 02079K305 GOOGL ALPHABET INC - CLASS A 58,382.00 142,556,583.78 023135106 AMZN AMAZON.COM, INC. 97,900.00 336,791,664.00 025537101 AEP AEP CO., INC. 147,626.00 12,487,683.34 031162100 AMGN AMGEN, INC. 169,722.00 41,369,737.50 032654105 ADI ANALOG DEVICES, INC. 108,951.00 18,757,004.16 03662Q105 ANSS ANSYS INC 25,745.00 8,935,059.70 037833100 AAPL APPLE, INC. 3,239,420.00 443,670,963.20 038222105 AMAT APPLIED MATERIALS, INC. 269,988.00 38,446,291.20 052769106 ADSK AUTODESK, INC. 65,007.00 18,975,543.30 053015103 ADP AUTOMATIC DATA PROCESSING 125,698.00 24,966,136.76 056752108 BIDU BAIDU INC 76,539.00 15,606,302.10 09062X103 BIIB BIOGEN INC 44,474.00 15,400,011.98 09857L108 BKNG BOOKING HOLDINGS INC 12,127.00 26,534,967.43 11135F101 AVGO BROADCOM INC 120,612.00 57,512,626.08 12514G108 CDW CDW CORP OF DELAWARE 41,416.00 7,233,304.40 126408103 CSX CSX CORP. -

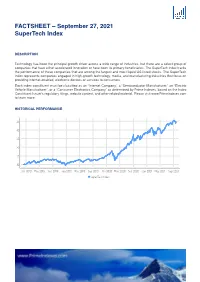

FACTSHEET – September 02, 2021 Supertech Index

FACTSHEET – September 27, 2021 SuperTech Index DESCRIPTION Technology has been the principal growth driver across a wide range of industries, but there are a select group of companies that have either accelerated innovation or have been its primary beneficiaries. The SuperTech index tracks the performance of these companies that are among the largest and most liquid US-listed stocks. The SuperTech index represents companies engaged in high-growth technology, media, and manufacturing industries that focus on providing internet-enabled, electronic devices or services to consumers. Each index constituent must be classified as an “Internet Company,” a “Semiconductor Manufacturer,” an “Electric Vehicle Manufacturer”, or a “Consumer Electronics Company” as determined by Prime Indexes, based on the Index Constituent Issuer’s regulatory filings, website content, and other related material. Please visit www.PrimeIndexes.com to learn more. HISTORICAL PERFORMANCE 35 30 25 20 15 10 Jan-2018 May-2018 Sep-2018 Jan-2019 May-2019 Sep-2019 Jan-2020 May-2020 Sep-2020 Jan-2021 May-2021 Sep-2021 SuperTech Index FACTSHEET – September 27, 2021 SuperTech Index CHARACTERISTICS ISIN / WKN DE000SL0CBX0 / SL0CBX Base Value / Base Date 10 Points / 07.12.2017 Bloomberg / Reuters TECH Index/.TECH Last Price 34.50 Index Calculator Solactive AG Dividends Not Included Index Type Price Return Calculation 9:30am to 16:50 (EST), every 15sec Index Currency USD History Available daily back to 07.12.2017 Index Members 15 STATISTICS 30D 90D 180D 360D YTD Since Inception Performance -1.29% 4.74% 20.21% 38.22% 20.97% 245.00% Performance (p.a.) - - - - - 38.46% Volatility (p.a.) 14.41% 13.88% 18.03% 24.44% 23.55% 29.60% High 35.67 35.67 35.67 35.67 35.67 35.67 Low 33.88 32.43 27.87 24.31 26.62 9.47 Sharpe Ratio -1.02 1.48 2.50 1.58 1.24 1.29 Max.