Township of Hampden Pennsylvania

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

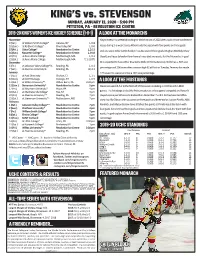

KING's Vs. STEVENSON

KING’S vs. STEVENSON SUNDAY, JANUARY 12, 2020 - 5:00 PM PITTSTON, PA - REVOLUTION ICE CENTRE 2019-20 KING’S WOMEN’S ICE HOCKEY SCHEDULE (1-8-1) A LOOK AT THE MONARCHS November King’s enters this weekend looking for their first win of 2020 after a pair of non-conference 9 (Sat.) at William Smith College* Geneva, NY L, 0-8 10 (Sun.) at #3 Elmira College* Pine Valley, NY L, 0-6 losses during the week. Josée Aitken leads the squad with four points on three goals 15 (Fri..) Utica College* Revolution Ice Centre L, 2-11 and one assist while Caitlin Redden has also scored three goals. Meghan Mietlicki, Mary 16 (Sat.) Nazareth College* Revolution Ice Centre L, 0-10 22 (Fri.) at Anna Maria College Marlborough, MA L, 0-1 Deyell, and Tessa Schaefer-Flynn have all recorded two assists for the Monarchs. In goal 23 (Sat.) at Anna Maria College Marlborough, MA T, 1-1 (OT) December KC is expected to have either Kiva Sierra Stoltz or Emma Zeveney. Stoltz has a .904 save 6 (Fri.) vs Lebanon Valley College^% Reading, PA L, 0-2 percentage and 206 saves after a season high 62 at Post on Tuesday. Zeveney has made 7 (Sat.) at Alvernia University% Reading, PA W, 4-2 January 172 saves this season and has a .901 save percentage. 7 (Tue.) at Post University Shelton, CT L, 1-5 8 (Wed.) at SUNY Oswego Oswego, NY L, 0-9 11 (Sat.) at Wilkes University*^ Wilkes-Barre, PA 3:30 pm A LOOK AT THE MUSTANGS 12 (Sun.) Stevenson University^ Revolution Ice Centre 5 pm Stevenson went 4-5-2 in the first half of the season including a 2-0-0 record in MAC 17 (Fri.) at Neumann University* Aston, PA 4 pm 18 (Sat.) at Manhattanville College* Rye, NY 3 pm games. -

17HB26800 2017-2018 Schedule Final

HERSHEY BEARS® HOCKEY CLUB 2017 2018 SEASON SCHEDULE SEPTEMBER OCTOBER NOVEMBER Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat 1 2 1 2 3 4 5 6 7 1 2 3 4 LV RCH TOR 7:05 7:05 7:00 3 4 5 6 7 8 9 8 9 10 11 12 13 14 5 6 7 8 9 10 11 BEL WBS SPR LV 7:00 3:05 7:05 7:00 10 11 12 13 14 15 16 15 16 17 18 19 20 21 12 13 14 15 16 17 18 LV MIL GR WBS SYR PRO 5:00 8:00 7:00 5:00 7:00 7:05 17 18 19 20 21 22 23 22 23 24 25 26 27 28 19 20 21 22 23 24 25 RFD WBS PRO PRO SPR HFD 5:00 7:05 7:00 1:05 7:00 7:00 24 25 26 Pre-season 27 28 29 Pre-season 30 29 30 31 26 27 28 29 30 Training Camp WBS WBS HFD BRI Begins 7:05 7:00 5:00 5:00 DECEMBER JANUARY FEBRUARY Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat 1 2 1 2 3 4 5 6 1 2 3 LV MIL CHA WBS CHA 7:05 7:00 7:00 7:05 7:00 3 4 5 6 7 8 9 7 8 9 10 11 12 13 4 5 7 8 10 WBS LV LV CHA SPR LV CHA 6 LV 9 HFD 5:00 7:05 7:00 5:00 7:00 7:05 2:00 7:05 7:00 10 11 12 13 14 15 16 14 15 16 17 18 19 LV 20 11 12 13 14 15 16 17 WBS PRO PRO LV SPR Outdoor Classic RCH LAV HFDBEL 5:00 Alumni Game 7:00 7:00 7:00 5:00 7:05 7:00 Outdoor Classic 5:00 7:30 7:007:00 17 18 19 20 21 22 23 21 22 23 24 25 26 27 18 19 20 21 22 23 24 CHA CHA BNG WBS PRO BRI TOR HFD RFD 7:00 7:00 7:00 7:00 7:05 7:00 3:00 7:15 7:00 24 30 28 29 30 25 26 BRI 27 28 SPR 29 WBS 31 WBS 25 26 27 28 31 7:00 7:05 7:00 3:05 MARCH APRIL Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat 1 LV 2 UTI 3 1 2 WBS 3 4 5 6 CHA 7 7:05 7:00 7:05 6:00 4 5 6 7 8 9 10 8 9 LV SYR BNG CHA 10 11 12 13 BRI 14 5:00 -

2011-12 Rochester Americans Media Guide (.Pdf)

Rochester Americans Table of Contents Rochester Americans Personnel History Rochester Americans Staff Directory........................................................................................4 All-Time Records vs. Current AHL Clubs ..........................................................................203 Amerks 2011-12 Schedule ............................................................................................................5 All-Time Coaches .........................................................................................................................204 Amerks Executive Staff ....................................................................................................................6 Coaches Lifetime Records ......................................................................................................205 Amerks Hockey Department Staff ..........................................................................................10 Presidents & General Managers ...........................................................................................206 Amerks Front Office Personnel ................................................................................................ 17 All-Time Captains ..........................................................................................................................207 Affiliation Timeline ........................................................................................................................208 Players Amerks Firsts & Milestones -

MILLERSVILLE UNIVERSITY • MEN’S SOCCER Table of Contents TABLE of CONTENTS/QUICK FACTS TABLE of CONTENTS Quick Facts

2010 MILLERSVILLE UNIVERSITY • MEN’S SOCCER Table of Contents TABLE OF CONTENTS/QUICK FACTS TABLE OF CONTENTS Quick Facts .........................................................................................................................2 2010 Schedule/Special Events ............................................................................................3 Athletic Tradition ................................................................................................................4 Athletic Administration ...................................................................................................5-6 Athletic Training .................................................................................................................7 Athletic Communications ...................................................................................................8 Student-Athlete Services ...................................................................................................9 Millersville Programs of Study ..........................................................................................10 Coaches ............................................................................................................................11 Head Coach Steve Widdowson..........................................................................................12 Assistant Coaches .............................................................................................................14 2010 Roster and Season Outlook ......................................................................................15 -

Thomas A. Mann, M.D

THOMAS A. MANN, M.D. CURRENT EMPLOYMENT Cornerstone Orthopaedics & Sports Medicine, P.C. 2000 – Present Sports Medicine & Arthroscopic Surgery Superior, Colorado EDUCATION Jefferson Medical College Sept. 1988 – June 1992 Cum Laude Alpha Omega Alpha Hobart Armory Hare Honor Medical Society Philadelphia, Pennsylvania Messiah College Sept. 1984 – May 1988 Summa Cum Laude Grantham, Pennsylvania POST GRADUATE TRAINING Fellowship: Sports Medicine August 1997 – July 1998 Ohio State University Columbus, Ohio Residency: Orthopaedic Surgery July 1993 – June 1997 Penn. State University Hospital Hershey, Pennsylvania Internship: General Surgery July 1992 – June 1993 Penn. State University Hospital Hershey Medical Center Hershey, Pennsylvania LICENSURE AND BOARD CERTIFICATIONS Colorado Medical License July 2000 – Present California Medical License July 1998 – 2001 American Board of Orthopaedic Surgery 2000 National Board of Medical Examiners 1993 MEMBERSHIPS American Orthopaedic Society for Sports Medicine Member American Academy of Orthopaedic Surgeons Fellow ORGANIZATIONS American Academy of Orthopedic Surgeons Candidate Member Christian Medical and Dental Society Associate Thomas A. Mann, M.D. (Page 1) SPORTS COVERAGE EXPERIENCE Pennsylvania Keystone State Games High School Pennsylvania: Harrisburg, ELCO, Annville-Cleona, East Pennsboro Ohio: Worthington Killborn California: Woodcreek (Roseville) Colorado: Ralston Valley Penn. State University – Spring Football, Gymnastics, W. Lacrosse Hershey Bears (AHL Professional Ice Hockey) Hershey Wildcats (A-League Professional Soccer) Columbus Chill (ECHL Professional Ice Hockey) Ohio State University – Football, Soccer, Field Hockey, etc. Sierra College – Football, Wrestling PUBLICATIONS 1. Pulmonary Considerations in Orthopaedic Trauma. Surgical Grand Rounds, Lehigh Valley Hospital, January 1995. Allentown, PA. 2. Residency Accuracy in Estimating Angles. Thomas A. Mann, MD. 28th American Orthopaedic Association Resident’s Meeting, March 1995. Pittsburgh, PA. -

Mechanicsburg

FREE! TAKE ONE CENTRALPENNPARENT.COM JUNE/JULY 2019 GoneGone fishin'fishin' FOR summersummer Gaming PLAIN YOUR 2019 at school MEDICINE Family Favorites! CENTRAL PA, THANK YOU for making us one of your favorites in 2019! WINNERS RUNNERS UP HOSPITAL PEDIATRICIAN FAMILY DOCTOR UPMC Pinnacle Harrisburg PinnacleHealth Heritage Good Hope Family Physicians Pediatrics PLACE TO HAVE A BABY UPMC Pinnacle URGENT CARE UPMC Pinnacle Harrisburg FAMILY COUNSELING AllBetterCare PinnacleHealth Psychological Associates UPMCPinnacle.com | 717-231-8900 WINNER CENTRAL PENN 1500 PAXTON ST., HARRISBURG, PA 17104 CENTRALPENNPARENT.COM | 717-236-4300 Editor's Note My obsession with rare, recessive disorders. with Th eranos and In the facility’s lower level, with neither fanfare ASSOCIATE PUBLISHER its beleaguered nor secrecy, sits a new Plain Insight Panel, a DNA Cathy Hirko [email protected] founder Elizabeth “sequencer” which can identify from one blood Holmes began with an early spring snow storm. My sample some 1,300 diff erent gene mutations found husband was out of town and my strong son was in Plain populations. Next-generation sequencing is EDITORIAL conveniently felled by a fever. Th e driveway wasn’t brand-new and hugely benefi cial; previously, separate EDITOR, Leslie Penkunas going to shovel itself. lab tests would have to be run to look for each [email protected] Looking for something, anything, that would keep mutation. Some of the dedicated staff at the Clinic my mind preoccupied during the arduous task before for Special Children, including both its executive and DESIGN me, I came upon the then-recently released, six-part laboratory directors, walked me through the ground- GRAPHIC DESIGNER, Kady Weddle podcast, ‘Th e Dropout.’ Halfway through the fi rst breaking research being done there. -

Mountaindale

MOUNTAINDALE About the Community Nestled at the base of the Blue Mountains and just east of the Susquehanna River is the award-winning neighborhood of Mountaindale. This Susquehanna Township community offers large home sites and a wide choice of single home designs, with the added benefit of many included features. Mountaindale’s location near Linglestown affords both natural beauty and easy access to the area’s abundant outdoor recreation, historical sites, and arts and entertainment venues. About the Area Home to the State Capital of Harrisburg, Dauphin County’s 525 square miles and 40 municipalities embrace an eclectic mix of rural, urban and suburban environments. Twelve public school districts serve the county’s population of 268,000+. The Susquehanna River borders Dauphin County on the west, providing scenic and recreational enjoyment year round. Most major routes serving the mid-Atlantic region converge here, creating a lively business, culture and entertainment center in this region of uncommon natural beauty. Schools Susquehanna Township School District serves the Mountaindale neighborhood. The elementary school is less than two miles away, and the high school is about five miles. A Sampling of Nearby Attractions Harrisburg Senators baseball • Harrisburg Symphony Orchestra • Hershey Bears Hockey • Hershey Park • Hershey Theater • National Civil War Museum • Penn National Race Course • State Capitol Complex • State Farm Show Complex • State Museum of Pennsylvania • Whitaker Center for Science and the Arts Resources Find out more -

Printable Pdf of the 2021-22 Hershey

HERSHEY BEARS® HOCKEY CLUB 2021 - 2022 SEASON SCHEDULE OCTOBER NOVEMBER DECEMBER Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat 1 2 1 2 3 4 5 6 1 2 3 4 SPR PRO LHV LHV 7:05 PM 7 PM 7:05 PM 7:05 PM 4 5 6 7 8 9 7 8 9 10 11 12 13 5 6 7 8 9 10 3 WBS SPR LHV SYR WBS WBS WBS 11 7:05 PM 3 PM 7 PM 7 PM 3 PM 7:05 PM 6:05 PM 11 12 13 14 15 16 14 15 16 17 18 19 20 13 14 15 17 18 LHV 10 LHV CLT CLT HFD LAV 12 16 SPR WBS 5 PM 7:05 PM 7 PM 5 PM 7 PM 5 PM 7:05 PM 7 PM 18 19 20 21 22 23 21 22 23 24 25 26 27 19 20 21 22 23 24 LHV 17 CLT CLT CLT PRO ROC ROC LHV 25 3 PM 7 PM 6 PM 5 PM 7 PM 7:05 PM 5 PM 7 PM 24 25 26 27 28 29 30 28 29 30 26 27 28 29 30 31 SYR CLE LHV WBS WBS 7 PM 7 PM 5 PM 7:05 PM 7 PM CLE 31 5 PM JANUARY FEBRUARY Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat 1 1 HFD 2 3 CLE 4 CLE 5 7 PM 7 PM 1 PM 2 BRI 3 4 5 6 SYR 7 WBS 8 6 7 8 9 10 LHV 11 BEL 12 3 PM 7 PM 7 PM 7:05 PM 7 PM 9 10 12 13 14 15 WBS 11 BRI TOR 13 14 15 16 17 PRO 18 BRI 19 5 PM 7 PM 7 PM 7:05 PM 7 PM 16 17 20 21 22 24 WBS 18 19 HFD 22 PRO 20 21 23 UTI 25 26 3:05 PM 7 PM 3:05 PM 7 PM 24 HFD 23 WBS 25 26 27 28 BRI 29 UTI 27 28 3 PM 7 PM 7 PM 5 PM LHV 30 31 3:05 PM MARCH APRIL Sun Mon Tue Wed Thu Fri Sat Sun Mon Tue Wed Thu Fri Sat 1 2 1 CLT 2 3 SPR 4 HFD 5 CLT CLT 7 PM 7:05 PM 7:30 PM 7 PM 6 PM 4 5 6 7 6 7 8 WBS 9 10 BRI 11 12 3 BRI LHV 8 SPR 9 7:05 PM 7 PM 10:30 AM 7:05 PM 7 PM 13 14 15 16 LHV 13 14 15 16 TOR 17 BEL 18 LAV 19 SPR 10 11 12 LHV WBS 5 PM 1:30 PM 7 PM 3 PM 5 PM 7:05 PM 7:05 PM 22 24 18 19 20 22 23 20 21 LHV 23 PRO 25 -

Opäť Lincoln, Ale Aj FC Kodaň a PAOK Futbalisti Slovana Včera Spoznali Svojich Súperov V Základnej Skupine Konferenčnej Ligy

www.nike.sk Sobota SUPERŠANCA 1X2 28. 8. 2021 103258 Manchester City – Arsenal 1,30 6,35 12,1 75. ročník • číslo 199 105575 Bayern Mníchov – Hertha 1,20 8,80 16,0 cena 1,00 pre predplatiteľov 0,70 106155 Real Betis – Real Madrid 4,45 4,00 1,88 107002 Juventus – Empoli 1,30 6,60 11,3 105579 Trenčín – Sereď 1,70 4,00 5,20 107001 Atalanta – Bologna 1,39 5,90 8,30 106156 Elche – FC Sevilla 5,55 3,60 1,81 107003 Lazio – Spezia 1,40 5,50 8,90 App Store pre iPad a iPhone / Google Play pre Android 104161 Sparta – České Budějovice 1,24 7,20 13,2 Strana 22 Strany 20 a 21 Už len krok Slovenskí hokejisti zdolali v kvalifikácii na ZOH Po¾sko 5:1, v nede¾u (17.30 h) od Pekingu ich èaká Bielorusko Zlatý i svetový Metelka Cyklista Jozef Metelka obhá- jil na paralympijských hrách v Tokiu zlato zo stíhacích pretekov na 4000 m. Do finále postúpil suverénnym spôsobom, keï v kvalifikácii utvoril èasom 4:22,772 min svetový rekord. FOTO SPV Prvý gól vèerajšieho zápasu proti Po¾sku strelil Adam Ružièka (za bránkou) a zavelil tak k povinnému víśazstvu. Slovenským hokejistom staèí na postup na zimné olympijské hry aj bod z nede¾òajšieho duelu proti Bielorusku. FOTO ŠPORT/JANO KOLLER Opäť Lincoln, ale aj FC Kodaň a PAOK Futbalisti Slovana včera spoznali svojich súperov v základnej skupine Konferenčnej ligy. Žreb im opäť prisú- Strany 3 – 5 dil Lincoln Red Imps z Gibraltáru, s ktorým sa v tejto sezóne už stretli v 3. -

Personnel-Section Doc 091815 Final

First Niagara Sabres Debit MasterCard® Score yours with a First Niagara consumer checking account. Stop by your local branch to open an account today. MasterCard® is a registered trademark of MasterCard® International Incorporated. The Sabres word mark and the Buffalo/Sabre logo design (Reg. U.S. Pat. & Tm. Off.), and the SABRETOOTH word mark are trademarks of Hockey Western New York, LLC. BANK / BORROW / INVEST / PROTECT 2015-16 MEDIA GUIDE TABLE OF CONTENTS CLUB PERSONNEL RECORD BOOK Allaire, J.T. ...........................................................................................22 The Last Time ......................................................................................198 Allen, Andrew ......................................................................................19 Penalty Shots ......................................................................................228 Babcock, George ..................................................................................23 Record by Day/Month .........................................................................195 Barch, Krys ..........................................................................................20 Regular-Season Overtime Goals ............................................................203 Barr, Dave ............................................................................................18 Sabres Streaks ....................................................................................200 Benson, Cliff .........................................................................................25 -

St. Cloud Ranked 8Th-Best Hockey Town in Country

St. Cloud ranked 8th-best hockey town in country HOME NEWS SPORTS OUTDOORS LIFE OPINION ENTERTAINMENT BUSINESS WATCHDOG PHOTO-VIDEO ARCHIVES USA TODAY St. Cloud ranked 8th-best hockey town in country Mick Hatten, [email protected] 3:24 p.m. CST February 4, 2016 304 St. Cloud has made a national list for one of the top 10 hockey towns to live in. St. Cloud is ranked eighth on the list, which was made for the second straight year by SmartAsset, which is a personal finance and technology Buy Photo company based in New York. (Photo: Dave Schwarz, [email protected]) "Hockey is definitely a pretty regional sport, so this is more of a regional question," said Nick Wallace, the data editor for SmartAsset. "We look at where people are choosing to live and why COMPLETEFlexible scheduling DENTAL and a peaceful, CARE they are choosing to live there. relaxingwhen atmosphere you allows need us to provideit the highest quality care to our patients. "We also do it for minor league baseball." There are a number of factors that SmartAsset looks at when making up the list, but there are a few that stand out. "We look at the overall level of fan interest and intensity in each city with average attendance and compared that to stadium capacity," Wallace said. "We also look at Google search traffic to get a sense of how much people are thinking about hockey in the area. "In St. Cloud, Minnesota, there's a ton of search traffic for hockey, almost as much as for food. -

Corporate Social Responsibility

CORPORATE SOCIAL RESPONSIBILITY 2018 SUMMARY TABLE OF CONTENTS 3 Letter From Our CEO 4 About Us 5 Hershey Entertainment & Resorts Company 7 Milton Hershey School Relationship 9 Corporate Social Responsibility Pillars 11 COMMUNITY 13 Supporting Our Community 15 Making A Difference 16 Hershey Bears® hockey team 17 ENVIRONMENT 18 Energy & Natural Resources 19 Recycling & Waste Management 20 Wildlife & Habitat 21 WORKPLACE 23 Employee Programs 24 Employee Resource Groups 26 Wellness & Safety 27 MARKETPLACE & GUEST FOCUS 29 Business Integrity & Collaboration 30 Safety & Security A LETTER FROM OUR PRESIDENT, CEO & CHAIRMAN ABOUT US In looking back at history, it can be easily argued that our founder, Milton S. Hershey, was one of the first people to practice corporate social responsibility (CSR). From his desire to ensure that his employees and townspeople had an OUR TEAM MEMBERS* idyllic community where they could safely and happily live, work, and play, to leaving his entire fortune to maintain and grow Milton Hershey School (MHS), Mr. Hershey lived his life with undeniable selflessness. Mr. Hershey’s rich history and focus on philanthropy serve as the foundation for Hershey 1,750 7,000 Entertainment & Resorts Company (HE&R)’s current-day approach to CSR, FULL-TIME PART-TIME which we are pleased to showcase in this report. EMPLOYEES & SEASONAL EMPLOYEES Our company is proud to share what our employees and guests have done to improve and nurture our community, environment, workplace, and EMPLOYEES RANGE IN AGE marketplace. I would like to personally thank our team members for continually FROM demonstrating HE&R’s core values - Devoted to the Legacy, Selfless Spirit of 14-90 Service, Team-Focused, and Respectful of Others - through countless hours of volunteerism, donating their time and resources to people in need, and OF OF ALL ALL diligently serving the students, teachers, and staff of MHS.