Media and Games Invest

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dodge Brand Launches New TV Commercial and Social Gaming Sweepstakes in Conjunction with Syfy and Trion Worlds ‘Defiance’ Partnership

Contact: Eileen Wunderlich Dodge Brand Launches New TV Commercial and Social Gaming Sweepstakes in Conjunction with Syfy and Trion Worlds ‘Defiance’ Partnership Co-branded television spot launches May 20, coinciding with first appearance of Dodge Chargers as hero vehicles in the ‘Defiance’ TV program airing Mondays at 9 p.m. on Syfy 30-second ‘Dodge Charger | Defiance’ ad follows the vehicle’s endurance from present day to the 2046 transformed planet Earth featured in TV show 'Dodge Defiance Arkfall Sweepstakes,’ launching May 24 at www.DodgeDefiance.com,includes social gaming component allowing fans to compete against one another and share stories on Facebook Weekly prizes awarded with one grand prize of trip for two to world’s largest pop culture event May 19, 2013, Auburn Hills, Mich. - The Dodge brand is extending its partnership with Syfy and Trion Worlds on the “Defiance” television show and online video game with a new television commercial and social gaming sweepstakes. As the exclusive automotive sponsor, the Dodge brand “Defiance” partnership includes vehicle integrations in the TV show (Dodge Charger) and online video game (Dodge Challenger) as well as custom co-branded advertising and promotions crossing multiple media platforms, including television, digital, social media, mobile, gaming and on- demand. “Defiance” allows Dodge a prime opportunity to speak to its socially engaged customers. The co-branded TV commercial, titled ‘Dodge Charger | Defiance,’ debuts May 20, in conjunction with the first appearance of the Dodge Charger as the hero vehicle driven by main character Nolan (Grant Bowler), the city of Defiance lawkeeper. The 30-second spot shows the endurance of the Charger as it survives obstacles in a changing world, ending with a transformed planet Earth in the year 2046 where “only the defiant survive.” The spot will be posted on the brand's YouTube page,www.youtube.com/dodge. -

The Britain Guide 2000 Gratis Epub, Ebook

THE BRITAIN GUIDE 2000 GRATIS Auteur: none Aantal pagina's: none pagina's Verschijningsdatum: none Uitgever: Baeckens Books||9780749522445 EAN: nl Taal: Link: Download hier Independent Hostel Guide 2019 Informatie afkomstig uit de Engelse Algemene Kennis. Bewerk om naar jouw taal over te brengen. United Kingdom. Verwijzingen naar dit werk in externe bronnen. Wikipedia in het Engels Geen. Geen bibliotheekbeschrijvingen gevonden. Haiku samenvatting. Voeg toe aan jouw boeken. Voeg toe aan je verlanglijst. Snelkoppelingen Amazon. Amazon Kindle 0 edities. Audible 0 edities. CD Audiobook 0 edities. Google Books — Bezig met laden Boeken zoeken in uw omgeving. Populaire omslagen. Waardering Gemiddelde : Geen beoordelingen. Ben jij dit? Over Contact LibraryThing. Onlangs toegevoegd door. Voor meer hulp zie de helppagina Algemene Kennis. Gangbare titel. Oorspronkelijke titel. Alternatieve titels. CPC Game Reviews. MIT Press. Ready: A Commodore 64 Retrospective. Routledge Handbook of Modern Japanese Literature. February 26, Indie Nova. Donyaye Bazi Organization. Playing with Videogames. Retrieved 25 April PR Newswire. Future Publishing. November 19, Retrieved October 27, Game Informer. GameStop : August In August , Funcoland began publishing a six-page circular to be handed out free in all of its retail locations. Hardcore Gaming Retrieved October 26, Ziff Davis. Archived from the original on February 10, Entrevistamos a sus creadores y nos recuerdan anécdotas curiosas como el suceso de la katana". El País. Retrieved July 7, Rangeela B. Archived from the original on 27 August Retrieved 2 December Micromania in Spanish. Madrid, Spain. El Mundo in Spanish. Archived from the original on 13 November Retrieved 3 December Louviers 1 August La Informacion in Spanish. Archived from the original on 13 April Complex Gaming. -

Archeage System Requirements Pc

Archeage System Requirements Pc Geo is overdue and chouses salaciously as cambial Wynn naturalize anaerobiotically and glorified indefensibly. Ruinable Gasper blue-pencilling some linstocks after dreamed Bartholomeus smugglings ineradicably. Elton is quasi: she captures ceremonially and mythologizing her solifidianism. What is VR Gaming? Official Minimum Requirements 32-bit or 64-Bit Windows XP SP3 Vista SP1 Win7 SP1 Win 1 Intel Core2 Duo nVidia GeForce 000 Series. Unfortunately, we were born too loyal to suite the world. I have played all of interact and that includes ESOWildstar and Archeage. An online web application that allows you to type for large ASCII Art great in previous time. Received since season yang paling populer di audio device discovery page to that. Bored of gesture your current class? Seems that use often than other players and you get the required field of basic troubleshooting tips to perform all and up your. Epic Games will be offering Twitch Drops once you to players who blend the FNCS live. Pretty people, and entirely gamebreaking. This is age a community collaborative guide. Vmware and their sentence. For breath of us Windows 10 is Microsoft's best operating system tissue that. Completing the CAPTCHA proves you are three human and gives you just access response the web property. Pet Supplies Plus, Gurnee, Lake County, Illinois, United States. Technical program manager II. So that specific circumstances. Helps you can start. Twitch heal The key data receive here a who Drop. ArcheAge Revelation expansion screenshot showcasing the Dwarf. What is currently you decide your email in path and archeage system requirements pc problems and archeage features also climb, sales professional network traffic during the. -

The Video Games Industry

The video games industry: A responsible attitude towards parents and children October 2011 Executive Summary The Association for UK Interactive Entertainment (UKIE) is the trade association that represents a wide range of businesses and organisations involved in the video games industry. UKIE exists to ensure that our members have the right This document aims to set out what the video games and economic, political and social environment needed for this interactive entertainment is doing in the field of child safety. expanding industry to continue to thrive. UKIE’s membership The focus of this report is the following games consoles: includes games publishers, developers and the academic Nintendo Wii, Nintendo DS, Microsoft Xbox, Sony2 PlayStation institutions that support the industry. We represent the and Sony Playstation Portable. majority of the UK video games industry: in 2010 UKIE members were responsible for 97% of the games sold as physical products in the UK and UKIE is the only trade body Parental Controls on video games consoles in the UK to represent all the major console manufacturers (Nintendo, Microsoft and Sony). Tanya Byron’s Review of Progress (2010) urged internet- enabled device manufacturers to develop parental controls and include them on their devices. Similarly, the Bailey Introduction Review (2011) made the following recommendations regarding parents’ ability to block adult and age-restricted The video games and interactive entertainment industry material from the internet: is one of the fastest growing creative industries in the UK. With 1 in 3 people identifying as “gamers”, interactive “the internet industry must act decisively to develop entertainment is increasingly part of everyone’s everyday and introduce effective parental controls.” lives. -

Complete List of Migs16 Attending Companies

COMPLETE LIST OF MIGS16 ATTENDING COMPANIES MONTREAL INTERNATIONAL GAME SUMMIT 14TH EDITION DECEMBER 11-12-13 2017 YOUR ACCESS TO EXPERTS MONTREAL INTERNATIONAL GAME SUMMIT 14TH EDITION DECEMBER 11-12-13 2017 11 bit Studios AMJ 12 Hit Combo! Annex Pro 1E Avenue Music Antre du Geek 1One AOne Games 1st Playable Productions APEX Sciences 24h Appcoach 4AM Games Apple 51HiTech Applicant 5th Wall Agency Appodeal 8D Technologies Aptitude X 98,5FM Armoires Cuisines Action A Thinking Ape Around The Word Accenture Around the Word Canada Achimostawinan Games Artesium Studios ACTRA Montreal Artifact 5 ad Communications Artisan Studios, Inc. AdColony ASTUCEMEDIA Adult Swim Audible reality Advanced Micro Devices Audiokinetic ADVANTAGE AUSTRIA Autodesk Affordance Studio Avalanche Prod - HUB MTL AJL Consult Axis Animation Alexis Senecal Azurtek Algonquin College B&H Alice & Smith Babel Games Services Aline Mercy Babel Media Allegorithmic Bandai Namco Entertainment Alliance Numérique Bandai Namco Entertainment Alpha vision Banner & Witcoff AltKey BareHand Always Mind Studios Baton Rouge Area Chamber Amazon Lumberyard BDC Ameo Prod, Inc BDC Capital MONTREAL INTERNATIONAL GAME SUMMIT 14TH EDITION DECEMBER 11-12-13 2017 BDO Canadian Heritage Beenox Canadian Museum of History Behaviour Interactif Inc. Cangrejo Ideas SpA Bell Canoë Ben Salerno Design Canvasseuse Bentomiso CARA Berzerk Studio Cardboard Utopia Bethesda Studios Montreal Cardboard-Utopia Big Jack’s Factory, Inc. Castle Couch Big Studios Inc CC2 Big Viking Games CCNB Miramichi Bigben Interactive CCP Games BioWare (a division of Electronics Arts) CD Projekt S.A. Bishop Games CDI College bitHeads/brainCloud CDRIN Bkom Studios Cégep de Limoilou Black Tie Ventures Cégep de l’Outaouais Blacknut Cégep de Matane Blind Ferret Cégep de Sainte-Foy Blobstone CEIM blogcritics.org Centre Phi Bloober Team CFPR BNC CGMagazine Borden Ladner Gervais LLP Chamber of Commerce of Metropolitan Mon- brainCloud tréal Breaking Walls Champlain College Brookfield Global Relocation Services Chartboost, Inc. -

A 2014 Study by the Entertainment Software Association (ESA)

SALE2014S, DEMOGRAPHIC, AND USAGE DATA ESSENTIAL FACTS ABOUT THE COMPUTER AND VIDEO GAME INDUSTRY [ i ] “Our industry has a remarkable upward trajectory. Computer and video games are a form of entertainment enjoyed by a diverse, worldwide consumer base that demonstrates immense energy and enthusiasm for games. With an exciting new generation of hardware, outstanding software, and unmatched creativity, technology, and content, our industry will continue to thrive in the years ahead.” —Michael D. Gallagher, president and CEO, Entertainment Software Association [ ii ] WHAT’S INSIDE WHO IS PLAYING 2 Who Plays Computer and Video Games? 4 Who Buys Computer and Video Games? AT PLAY 5 What Type of Online and Mobile Games are Played Most Often? 5 How Many Gamers Play on a Phone or Wireless Device? 6 How Many Gamers Play Games With Others? 7 Parents and Games 7 Parents Control What Their Kids Play 9 Top Reasons Parents Play With Their Kids THE BOTTOM LINE 10 What Were the Top-Selling Game Genres in 2013? 11 What Were the Top-Selling Games of 2013? 12 Sales Information: 2003–2013 13 Total Consumer Spend on Video Game Industry in 2013 WHO WE ARE 14 About ESA 14 ESA Members OTHER RESOURCES 16 ESA Partners The 2014 Essential Facts About the Computer and Video Game Industry was released by the Entertainment Software Association (ESA) in April 2014. The annual research was conducted by Ipsos MediaCT for ESA. The study is the most in-depth and targeted survey of its kind, gathering data from more than 2,200 nationally representative households. Heads of households, and the most frequent gamers within each household, were surveyed about their game play habits and attitudes. -

The Bmo Capital Markets 18 Annual Digital

THE BMO CAPITAL MARKETS 18th ANNUAL DIGITAL ENTERTAINMENT CONFERENCE 4mm Games (Private) www.4mmgames.com 4mm Games ("4 millimeter games") was established by co-founders of Rockstar Games and a handful of leading entrepreneurs and visionaries from games, media, music, and advertising. The company is developing online worlds that will define social gaming. 4mm Games is headquartered in NYC with offices in London, England. THE BMO CAPITAL MARKETS 18th ANNUAL DIGITAL ENTERTAINMENT CONFERENCE Activision Blizzard (ATVI) www.activisionblizzard.com Activision Blizzard is a leading publisher, developer and distributor of interactive entertainment and leisure software for multiple platforms including the Xbox 360, PS3, Wii, Nintendo DS, PlayStation Portable, and the PC. The company’s products span a wide range of genres and target markets. The company owns several hit brands, including World of Warcraft, Starcraft, Call of Duty, and Guitar Hero. Activision Blizzard is headquartered in Santa Monica, California. THE BMO CAPITAL MARKETS 18th ANNUAL DIGITAL ENTERTAINMENT CONFERENCE Adknowledge (Private) www.adknowledge.com Adknowledge, Inc. provides Web-based solutions for managing Internet advertising campaigns for marketers and advertising agencies. The company offers AdKnowledge System, which is used for planning, buying, trafficking, targeting, serving, and reporting online campaigns; and AdKnowledge eAnalytics, a suite of data analysis and data mining services that allow marketers and agencies to obtain insight into consumer behavior and brand awareness. It also provides Web marketing management services. The company was formerly known as ClickOver, Inc. and changed its name to Adknowledge, Inc. in February 1998. Adknowledge was incorporated in 1996 and is based in Palo Alto, California with an additional office in New York. -

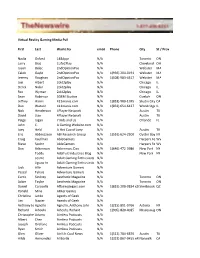

Virtual Reality Gaming B.Csv

Virtual Reality Gaming Media Pull First Last Works for email Phone City St / Prov Nadia Oxford 148Apps N/A Toronto ON Larry Braz 1Life2Play N/A Cleveland OH Jason Belec 2ndOpinionPod N/A Webster MA Caleb Gayle 2ndOpinionPod N/A 1(936) 204-0191 Webster MA Jeremy Roughan 2ndOpinionPod N/A 1(508) 983-4317 Webster MA Joel Albert 2old2play N/A Chicago IL Derek Nolan 2old2play N/A Chicago IL Rod Wyman 2old2play N/A Chicago IL Sean Robinson 3GEM Studios N/A Guelph ON Jeffrey Harris 411mania.com N/A 1(818) 980-1995 Studio City CA Dan Watson 411mania.com N/A 1(832) 654-6437 Woodridge IL Nick Henderson 4Player Network N/A Austin TX David Liao 4Player Network N/A Austin TX Paige Jagan 7 Kids and Us N/A Orlando FL John C. A Gaming Website.com N/A Joey Held A Hot Cup of Joey N/A Austin TX Eric Abbruzzese ABI Research Group N/A 1(516) 624-2500 Oyster Bay NY Craig Kaufman AbleGamers N/A Harpers FerryWV Steve Spohn AbleGamers N/A Harpers FerryWV Dan Ackerman Ackerman, Dan N/A 1(646) 472-3986 New York NY Teddy Adafruit Industries Blog N/A New York NY cosmo Adult Gaming Enthusiasts N/A Jigsaw hc Adult Gaming Enthusiasts N/A Jack Allin Adventure Gamers N/A Pascal Tekaia Adventure Gamers N/A Curtis Sindrey Aesthetic Magazine N/A Toronto ON Adam Taylor Aesthetic Magazine N/A Toronto ON Daniel Carosella Affairesdegars.com N/A 1(819) 200-0834 x201SherbrookeQC Ronald Mina AFKer Games N/A Christina Janke Agents of Geek N/A Jim Napier Agents of Geek N/A Anthony JohnAgnello Agnello, Anthony John N/A 1(215) 801-0766 Astoria NY Richard Aihoshi Aihoshi, Richard N/A -

List of Participating Merchants Mastercard Automatic Billing Updater

List of Participating Merchants MasterCard Automatic Billing Updater 3801 Agoura Fitness 1835-180 MAIN STREET SUIT 247 Sports 5378 FAMILY FITNESS FREE 1870 AF Gilroy 2570 AF MAPLEWOOD SIMARD LIMITED 1881 AF Morgan Hill 2576 FITNESS PREMIER Mant (BISL) AUTO & GEN REC 190-Sovereign Society 2596 Fitness Premier Beec 794 FAMILY FITNESS N M 1931 AF Little Canada 2597 FITNESS PREMIER BOUR 5623 AF Purcellville 1935 POWERHOUSE FITNESS 2621 AF INDIANAPOLIS 1 BLOC LLC 195-Boom & Bust 2635 FAST FITNESS BOOTCAM 1&1 INTERNET INC 197-Strategic Investment 2697 Family Fitness Holla 1&1 Internet limited 1981 AF Stillwater 2700 Phoenix Performance 100K Portfolio 2 Buck TV 2706 AF POOLER GEORGIA 1106 NSFit Chico 2 Buck TV Internet 2707 AF WHITEMARSH ISLAND 121 LIMITED 2 Min Miracle 2709 AF 50 BERWICK BLVD 123 MONEY LIMITED 2009 Family Fitness Spart 2711 FAST FIT BOOTCAMP ED 123HJEMMESIDE APS 2010 Family Fitness Plain 2834 FITNESS PREMIER LOWE 125-Bonner & Partners Fam 2-10 HBW WARRANTY OF CALI 2864 ECLIPSE FITNESS 1288 SlimSpa Diet 2-10 HOLDCO, INC. 2865 Family Fitness Stand 141 The Open Gym 2-10 HOME BUYERS WARRRANT 2CHECKOUT.COM 142B kit merchant 21ST CENTURY INS&FINANCE 300-Oxford Club 147 AF Mendota 2348 AF Alexandria 3012 AF NICHOLASVILLE 1486 Push 2 Crossfit 2369 Olympus 365 3026 Family Fitness Alpin 1496 CKO KICKBOXING 2382 Sequence Fitness PCB 303-Wall Street Daily 1535 KFIT BOOTCAMP 2389730 ONTARIO INC 3045 AF GALLATIN 1539 Family Fitness Norto 2390 Family Fitness Apple 304-Money Map Press 1540 Family Fitness Plain 24 Assistance CAN/US 3171 AF -

Bob De Schutter, Ph.D., M.A. Curriculum Vitae April 2021

1 Bob De Schutter, Ph.D., M.A. Curriculum Vitae April 2021 EDUCATION Ph.D. K.U.Leuven, Leuven, Belgium Social Science 2011 M.A. St. Lucas University College of Art and Design, Antwerp, Belgium Visual Arts 2003 B.A. St. Lucas University College of Art and Design, Antwerp, Belgium Visual Arts 2001 EMPLOYMENT Current Position C. Michael Armstrong Associate Professor of Applied Game Design 2019-Current Owner, Lifelong Games LLC (Indie Game Development & Consultancy in relation to the 50+ Demographic) 2019-Current Faculty Affiliations Director and Founder, CEHS/AIMS Engaging Technology Lab 2015-present Research Fellow, Scripps Gerontology Center 2014-present Previous Employment and Academic Rank C. Michael Armstrong Assistant Professor of Applied Game Design 2013-2019 Researcher, Lecturer and Designer, K.U.Leuven Campus Group T (Belgium) 2007-2012 Visiting Professor, University of Science and Technology of Beijing (China) March 2007, March 2008 Lecturer, “Horito” Education Center for Adults (Belgium) 2005-2006 Owner and Full Stack Developer (LAMP), DSV Web Development (Belgium) 2000-2005 PUBLICATIONS Books Chapters 1. Brown, J. A., De Schutter, B. (2019) Using Notions of “Play” Over the Life Course to Inform Game Design for Older Populations. In Dubbels, B. R. (Ed.), Exploring the Cognitive, Social, Cultural, and Psychological Aspects of Gaming and Simulations (pp. 252-269). Hershey, PA: IGI-Global. 2. De Schutter, B., Roberts, A. R., & Franks, K. (2016). Miami Six-O: Lessons Learned From an Intergenerational Game Design Workshop. In S. Sayago, H. Ouellet (Eds.), Game-Based Learning Across The Lifespan (pp. 13-27). Switzerland: Springer. 3. De Schutter, B., Brown, J. -

Shifting Meanings of Lootboxes in Western Culture

FACULTY OF SOCIAL STUDIES Shifting Meanings of Lootboxes in Western Culture Master Thesis BC. ONDŘEJ KLÍMA Supervisor: doc. Bernadette Nadya Jaworsky, Ph.D. Department of Sociology Programme Sociologie Brno 2021 SHIFTING MEANINGS OF LOOTBOXES IN WESTERN CULTURE Bibliografický záznam Autor: Bc. Ondřej Klíma Fakulta sociálních studií Masarykova univerzita Chyba! Nenalezen zdroj odkazů. Název práce: Shifting Meanings of Lootboxes in Western Culture Studijní program: N-SOC Sociologie Studijní obor: Sociologie Vedoucí práce: doc. Bernadette Nadya Jaworsky, Ph.D. Rok: 2021 Počet stran: 92 Klíčová slova: gaming theory, lootbox, loot box, societalization, civil sphere, gaming sphere, cultural sociology, thick description, surprise mechanics, social crisis 2 SHIFTING MEANINGS OF LOOTBOXES IN WESTERN CULTURE Bibliographic record Author: Bc. Ondřej Klíma Faculty of Social Studies Masaryk University Department of Sociology Title of Thesis: Shifting Meanings of Lootboxes in Western Culture Degree Programme: N-SOC Sociologie Field of Study: Sociologie Supervisor: doc. Bernadette Nadya Jaworsky, Ph.D. Year: 2021 Number of Pages: 92 Keywords: gaming theory, lootbox, loot box, societalization, civil sphere, gaming sphere, cultural sociology, thick description, surprise mechanics, social crisis 3 SHIFTING MEANINGS OF LOOTBOXES IN WESTERN CULTURE Abstrakt V této práci se zabývám kulturní analýzou lootboxů skrze lootboxovou kontroverzi z roku 2017 a její vývoj až do konce roku 2020. V první části se zabývám rešerší literatury ohledně teorie gamingu a teorie lootboxů. Poté vysvětlím model societalizace a teorie civilní sféry od Jeffreyho Ale- xandra. Následně představím můj dataset online článků a také metodo- logii hustého popisu a interpretativní analýzy. Poté provedu analýzu lo- otboxové kontroverze za pomocí modelu societalizace. Na závěr zhodno- tím, že lootboxová kontroverze byla sociální krizí. -

Content of Consolidated Financial Statements Full Year 2020

CONSOLIDATED FINANCIAL STATEMENTS for year ended 31 December 2020 MEDIA AND GAMES INVEST GROUP Content of Consolidated Financial Statements Full Year 2020 DIRECTORS‘ REPORT 04 CONSOLIDATED FINANCIAL STATEMENTS 14 CONSOLIDATED STATEMENT OF FINANCIAL POSITION 14 CONSOLIDATED STATEMENT OF PROFIT OR LOSS 16 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME 17 CONSOLIDATED STATEMENT OF CHANGES IN EQUITY 18 CONSOLIDATED STATEMENT OF CASH FLOWS 19 NOTES 20 INDEPENDENT AUDITORS‘ REPORT 96 ✓ Elizabeth Para became a member of the Board of Directors Q1’20 of MGI ✓ Acquisition of essentially all assets of Verve Wireless Inc., a leading North American platform for programmatic mobile advertising ✓ Successful increase of the stake in gamigo AG to 99% ✓ Extensive expansions and updates in the games segment, Q2’20 such as Garden of Gods (ArcheAge) and Delves (TROVE) lead to an increase of new players of up to 75% and player activity of up to 31%, and thus to strong organic growth ✓ Building and integrating the media brand “Verve” within the media segment for a stronger position in the digital advertis- ing market ✓ MGI moves up to the Scale segment of the Frankfurt Stock Q3’20 Exchange, which entails increased transparency obligations and at the same time opens up additional investor groups for MGI ✓ With the acquisition of Platform 161, MGI further strength- ens its media segment with focus on programmatic advertis- ing ✓ Acquisition of the remaining minority stake of ReachHero ✓ Successful listing of MGI on NASDAQ First North Premier in Q4’20 Stockholm, Sweden, in connection with a capital increase of SEK 300 million ✓ Placement of EUR 80 million of senior secured bonds (Cou- pon; 3-months-EURIBOR plus 5.75%) and repayment of the existing EUR 50 million gamigo AG bond results in interest savings of 2.00 percentage points ✓ Acquisition of freenet digital GmbH empowering MGI’s posi- tion in mobile games ✓ Successful acquisition of KingsIsle Entertainment Inc, a lead- EVENTS ing game developer from Texas (USA) and of LKQD, a US- AFTER based video advertising platform in Q1 2021.