1 Exploring Digital Convergence Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

An N U Al R Ep O R T 2018 Annual Report

ANNUAL REPORT 2018 ANNUAL REPORT The Annual Report in English is a translation of the French Document de référence provided for information purposes. This translation is qualified in its entirety by reference to the Document de référence. The Annual Report is available on the Company’s website www.vivendi.com II –— VIVENDI –— ANNUAL REPORT 2018 –— –— VIVENDI –— ANNUAL REPORT 2018 –— 01 Content QUESTIONS FOR YANNICK BOLLORÉ AND ARNAUD DE PUYFONTAINE 02 PROFILE OF THE GROUP — STRATEGY AND VALUE CREATION — BUSINESSES, FINANCIAL COMMUNICATION, TAX POLICY AND REGULATORY ENVIRONMENT — NON-FINANCIAL PERFORMANCE 04 1. Profile of the Group 06 1 2. Strategy and Value Creation 12 3. Businesses – Financial Communication – Tax Policy and Regulatory Environment 24 4. Non-financial Performance 48 RISK FACTORS — INTERNAL CONTROL AND RISK MANAGEMENT — COMPLIANCE POLICY 96 1. Risk Factors 98 2. Internal Control and Risk Management 102 2 3. Compliance Policy 108 CORPORATE GOVERNANCE OF VIVENDI — COMPENSATION OF CORPORATE OFFICERS OF VIVENDI — GENERAL INFORMATION ABOUT THE COMPANY 112 1. Corporate Governance of Vivendi 114 2. Compensation of Corporate Officers of Vivendi 150 3 3. General Information about the Company 184 FINANCIAL REPORT — STATUTORY AUDITORS’ REPORT ON THE CONSOLIDATED FINANCIAL STATEMENTS — CONSOLIDATED FINANCIAL STATEMENTS — STATUTORY AUDITORS’ REPORT ON THE FINANCIAL STATEMENTS — STATUTORY FINANCIAL STATEMENTS 196 Key Consolidated Financial Data for the last five years 198 4 I – 2018 Financial Report 199 II – Appendix to the Financial Report 222 III – Audited Consolidated Financial Statements for the year ended December 31, 2018 223 IV – 2018 Statutory Financial Statements 319 RECENT EVENTS — OUTLOOK 358 1. Recent Events 360 5 2. Outlook 361 RESPONSIBILITY FOR AUDITING THE FINANCIAL STATEMENTS 362 1. -

Dxpedition Report from Rose Spit, Haida Gwaii

Rose Spit mini-DXpedition 11 July, 2011. Rose Spit loggings for 11 July, 2011: Medium Wave and Long Wave Here is a compilation of what I heard on an overnight DC only DXpedition to Rose Spit, about 25 km from the closest power lines, on the north east corner of Haida Gwaii. This spit is sandy, and covered in short grasses and strawberry plants, so ideal for remote DXpeditions, as it is accessible by 4x4 wheel drive vehicles. Conditions were not very good with the A index around 13, and K indices between 2 and 4, and solar flux at 90.6. The loggings below on MW are almost all from using a 750’ BOG aimed at New Zealand, unterminated. Here’s an aerial photo of the Spit. I was located just a few hundred meters past the tree line, in about the center of the spit, which faces N/NE. The larger photo below shows Rose Spit looking back to the West/South West to the treeline. Lot’s of room for BOGs! The figure below shows a view in the opposite direction down the spit to the N/NW where the 750’ BOGs were located. The NZ wire could have easily been double the distance. A more likely scenario for next time might be a phased BOG array towards NZ or dual Wellbrook delta loops. My wonderful DXpedition vehicle: A Nissan Frontier, 4 door, 4x4. Very comfortable, with a folding down front passenger seat, making a perfect platform for the radios and computer. Also a comfortable rear seat to sleep. -

Contents Audience Insights 2 Campaign Websites 2 Leveraging the National Campaign in Your Community 3

Contents Audience insights 2 Campaign websites 2 Leveraging the national campaign in your community 3 Local communication channels and opportunities 5 Tips for working with media 7 AUDIENCE INSIGHTS Drive Smokefree for Tamariki aims to reach parents, caregivers and whānau who smoke in cars with tamariki present. Ensuring the message resonates with Māori, Pasifika and low- socioeconomic communities who are disproportionately affected by smoking prevalence. Results from the 2018 Youth Insights Survey showed that around 15% of young people were exposed to second hand smoke in cars. CAMPAIGN WEBSITES Campaign Landing Page: The audience facing campaign landing page is www.smokefree.org.nz/drivesmokefreefortamariki It is hosted on the existing smokefree.org website and has been built with our audience in mind for helpful information on how to be smokefree in cars and information on when the law is coming and how those who smoke in cars with kids might be impacted. There is also information on the harm of second hand smoke and why the law has changed. The page has two campaign videos and a link to the Campaign Resources page with downloadable material to help share the message in communities. Campaign Resources Page: This is designed for health promoters and the National Smokefree Cars Working Group and associated community groups hosted by Te Hiringa Hauora | Health Promotion Agency. https://www.hpa.org.nz/campaign/drive-smokefree-for-tamariki This page provides an overview of the National Campaign with links to downloadable materials, logo files, video and radio campaign material that can be used in their local activities to promote Drive Smokefree for Tamariki leading into the law change. -

The Roles of Police, Media and Public in Coverage of the Coral-Ellen Burrows Murder Inquiry

JOURNALISM DOWNUNDER Information provision and restriction: The roles of police, media and public in coverage of the Coral-Ellen Burrows murder inquiry ABSTRACT Six-year-old Coral-Ellen Burrows disappeared in September 2003 after her stepfather, Stephen Williams, had apparently dropped her off at school, though in fact he had murdered her. After extensive searches, her body was found 10 days later. Williams pleaded guilty to murder and was duly sentenced. The intensive cross-media coverage of the search for Coral- Ellen—of the kind that Innes (1999) commenting on media and police interactions in Britain calls ‘blitz coverage’, made this case the pre- eminent news story of 2003. However, the attenuated nature of the search also exposed some of the tensions inherent in the relationships between those parties interested in the case. We understand these to consist of six entities which have an existence that is both material and conceptual: these are the victim’s family, possible suspects, the local community, the police, the media, and the national public, in this case envisaged in a dual role as wider community and media-audience. All of these stand in relationship to the more abstract yet rigid institution of the law, whose dictates guide the behaviour of the police, and strongly infl uence that of the media. This paper reports on research carried out by analysis of New Zealand Herald, Wairarapa Times-Age and TV One coverage of the case, and by two interviews with journalists investigating the forces that shaped the media coverage. ANN HARDY AND ALASTAIR GUNN University of Waikato PACIFIC JOURNALISM REVIEW 13 (1) 2007 161 JOURNALISM DOWNUNDER OR 11 days in September 2003, the New Zealand national media gave intensive coverage to the search for a six-year-old girl, Coral-Ellen FBurrows, who went missing between her home and school in Featherston, in the Wairarapa. -

Mapping the Information Environment in the Pacific Island Countries: Disruptors, Deficits, and Decisions

December 2019 Mapping the Information Environment in the Pacific Island Countries: Disruptors, Deficits, and Decisions Lauren Dickey, Erica Downs, Andrew Taffer, and Heidi Holz with Drew Thompson, S. Bilal Hyder, Ryan Loomis, and Anthony Miller Maps and graphics created by Sue N. Mercer, Sharay Bennett, and Michele Deisbeck Approved for Public Release: distribution unlimited. IRM-2019-U-019755-Final Abstract This report provides a general map of the information environment of the Pacific Island Countries (PICs). The focus of the report is on the information environment—that is, the aggregate of individuals, organizations, and systems that shape public opinion through the dissemination of news and information—in the PICs. In this report, we provide a current understanding of how these countries and their respective populaces consume information. We map the general characteristics of the information environment in the region, highlighting trends that make the dissemination and consumption of information in the PICs particularly dynamic. We identify three factors that contribute to the dynamism of the regional information environment: disruptors, deficits, and domestic decisions. Collectively, these factors also create new opportunities for foreign actors to influence or shape the domestic information space in the PICs. This report concludes with recommendations for traditional partners and the PICs to support the positive evolution of the information environment. This document contains the best opinion of CNA at the time of issue. It does not necessarily represent the opinion of the sponsor or client. Distribution Approved for public release: distribution unlimited. 12/10/2019 Cooperative Agreement/Grant Award Number: SGECPD18CA0027. This project has been supported by funding from the U.S. -

2019 Winners & Finalists

2019 WINNERS & FINALISTS Associated Craft Award Winner Alison Watt The Radio Bureau Finalists MediaWorks Trade Marketing Team MediaWorks MediaWorks Radio Integration Team MediaWorks Best Community Campaign Winner Dena Roberts, Dominic Harvey, Tom McKenzie, Bex Dewhurst, Ryan Rathbone, Lucy 5 Marathons in 5 Days The Edge Network Carthew, Lucy Hills, Clinton Randell, Megan Annear, Ricky Bannister Finalists Leanne Hutchinson, Jason Gunn, Jay-Jay Feeney, Todd Fisher, Matt Anderson, Shae Jingle Bail More FM Network Osborne, Abby Quinn, Mel Low, Talia Purser Petition for Pride Mel Toomey, Casey Sullivan, Daniel Mac The Edge Wellington Best Content Best Content Director Winner Ryan Rathbone The Edge Network Finalists Ross Flahive ZM Network Christian Boston More FM Network Best Creative Feature Winner Whostalk ZB Phil Guyan, Josh Couch, Grace Bucknell, Phil Yule, Mike Hosking, Daryl Habraken Newstalk ZB Network / CBA Finalists Tarore John Cowan, Josh Couch, Rangi Kipa, Phil Yule Newstalk ZB Network / CBA Poo Towns of New Zealand Jeremy Pickford, Duncan Heyde, Thane Kirby, Jack Honeybone, Roisin Kelly The Rock Network Best Podcast Winner Gone Fishing Adam Dudding, Amy Maas, Tim Watkin, Justin Gregory, Rangi Powick, Jason Dorday RNZ National / Stuff Finalists Black Sheep William Ray, Tim Watkin RNZ National BANG! Melody Thomas, Tim Watkin RNZ National Best Show Producer - Music Show Winner Jeremy Pickford The Rock Drive with Thane & Dunc The Rock Network Finalists Alexandra Mullin The Edge Breakfast with Dom, Meg & Randell The Edge Network Ryan -

Tvnz Teletext

TVNZ TELETEXT YOUR GUIDE TO TVNZ TELETEXT INFORMATION CONTENTS WELCOME TO TVNZ TELETEXT 3 TVNZ Teletext Has imProved 4 New PAGE GUIDE 5 NEW FUNCTIONS AND FEATURES 6 CAPTIONING 7 ABOUT TVNZ TELETEXT 8 HOW TO USE TVNZ TELETEXT 9-10 HISTORY OF TVNZ TELETEXT 11 FAQ 12-13 Contact detailS 14 WELCOME TO TVNZ TELETEXT It’s all available Your free service for up-to-the-minute news and information whenever you on your television need it – 24 hours a day, all year round. at the push of From news and sport to weather, a button travel, finance, TV listings and lifestyle information – it’s all available on your television, at the push of a button. 3 TVNZ Teletext Has imProved If you’ve looked at TVNZ Teletext recently and couldn’t find what you expected, don’t worry. To make the service easier and more logical to use we’ve reorganised a little. Your favourite content is still there – but in a different place. The reason is simple. We have a limited number of pages available, but need to show more information than ever. Previously, TVNZ Teletext had similar information spread across many pages unnecessarily. We’ve reorganised to keep similar pages together. For example, all news content is now grouped together, as is all sport content. You may also notice that the branding has changed slightly. Teletext is still owned and run by TVNZ, just as it always has been, we are now just reflecting this through the name - TVNZ Teletext. Now more than ever it will be a service that represents the integrity, neutrality and editorial independence you expect from New Zealand’s leading broadcaster. -

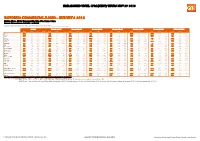

Nz Major Markets Commercial Radio

EMBARGOED UNTIL 1PM (NZDT) THURS NOV 29 2018 NZ MAJOR MARKETS COMMERCIAL RADIO - SURVEY 4 2018 Station Share (%) by Demographic, Mon-Sun 12mn-12mn Survey Comparisons: 3/2018 - 4/2018 This Survey Period: Metro - Sun Jun 24 to Sat Nov 10 2018 / Regional - Sun Jan 28 to Sat Jun 16 2018 & Sun Jun 24 to Sat Nov 10 2018 (Waikato - Sun Aug 21 to Sat Oct 22 2016 & Sun Jan 29 to Sat Jun 17 & Sun Jul 2 to Sat Sep 9 2017) Last Survey Period: Metro - Sun Apr 8 to Sat Jun 16 & Sun Jun 24 to Sat Sep 1 2018 / Regional - Sun Sep 10 to Sat Nov 18 2017 & Sun Jan 28 to Sat Jun 16 2018 & Sun Jun 24 to Sat Sep 1 2018 (Waikato - Sun Aug 21 to Sat Oct 22 2016 & Sun Jan 29 to Sat Jun 17 & Sun Jul 2 to Sat Sep 9 2017) All 10+ People 10-17 People 18-34 People 25-44 People 25-54 People 45-64 People 55-74 MGS with Kids This Last +/- Rank This Last +/- This Last +/- This Last +/- This Last +/- This Last +/- This Last +/- This Last +/- Network Breeze 7.8 8.0 -0.2 3 5.6 6.0 -0.4 5.1 5.1 0.0 7.0 6.3 0.7 7.9 7.6 0.3 9.9 10.1 -0.2 9.7 10.9 -1.2 10.1 8.7 1.4 Network Coast 7.5 7.4 0.1 5 2.3 2.3 0.0 2.1 2.3 -0.2 2.4 2.3 0.1 4.5 4.1 0.4 9.6 10.7 -1.1 14.5 14.8 -0.3 4.3 3.9 0.4 Network The Edge 6.5 6.1 0.4 6 16.2 15.1 1.1 12.0 11.5 0.5 8.7 7.9 0.8 7.1 6.6 0.5 3.5 3.1 0.4 1.7 1.5 0.2 7.2 7.5 -0.3 Network Flava 2.6 2.7 -0.1 14 10.1 10.5 -0.4 4.0 4.9 -0.9 3.0 3.7 -0.7 2.6 2.9 -0.3 1.2 0.8 0.4 0.3 0.2 0.1 2.5 3.0 -0.5 Network George FM 1.3 1.5 -0.2 17 1.5 2.2 -0.7 2.6 2.7 -0.1 2.6 2.7 -0.1 2.0 2.2 -0.2 0.7 0.9 -0.2 0.2 0.3 -0.1 1.1 1.0 0.1 Network Hokonui 0.2 0.2 0.0 23 0.2 0.3 -

Broadcasting Standards in New Zealand

APRIL 2016 BROADCASTING STANDARDS IN NEW ZEALAND FOR RADIO, FREE-TO-AIR-TELEVISION & PAY TELEVISION DEVELOPED BY BROADCASTERS AND THE BSA AND ISSUED TO TAKE EFFECT FROM 1 APRIL 2016 In the case of any inconsistency between this Codebook and any predating BSA material such as codes, practice notes and advisory opinions, this Codebook will prevail. BROADCASTING STANDARDS IN NEW ZEALAND BROADCASTING STANDARDS AUTHORITY - TE MANA WHANONGA KAIPAHO LEVEL 2 | 119 GHUZNEE STREET PO BOX 9213 | WELLINGTON 6141 | NEW ZEALAND (04) 382 9508 | FREEPHONE: 0800 366 996 WWW.BSA.GOVT.NZ 1 / Broadcasting Standards Authority CONTENTS INTRODUCTION 03 THE FREE-TO-AIR The Broadcasting Standards Authority 04 TELEVISION CODE 32 Broadcasters 05 Standard 1 – Good Taste and Decency 35 Freedom of Expression 06 Standard 2 – Programme Information 35 Choice and Control 07 Standard 3 – Children’s Interests 36 Standards, Guidelines and Commentary 08 Standard 4 – Violence 36 Definitions 09 Standard 5 – Law and Order 36 Standard 6 – Discrimination and Denigration 37 COMMENTARY ON Standard 7 – Alcohol 37 Standard 8 – Balance 39 THE STANDARDS 10 Standard 9 – Accuracy 39 Standard 10 – Privacy 41 THE RADIO CODE 22 Standard 11 – Fairness 41 Standard 1 – Good Taste and Decency 25 Standard 2 – Programme Information 25 THE PAY Standard 3 – Children’s Interests 25 TELEVISION CODE 42 Standard 4 – Violence 26 Standard 1 – Good Taste and Decency 45 Standard 5 – Law and Order 26 Standard 2 – Programme Information 45 Standard 6 – Discrimination and Denigration 26 Standard 3 – Children’s -

Rotorua Commercial Radio

EMBARGOED UNTIL 1PM (NZDT) THURS NOV 29 2018 ROTORUA COMMERCIAL RADIO - SURVEY 4 2018 Station Share (%) by Demographic, Mon-Sun 12mn-12mn Survey Comparisons: 3/2018 - 4/2018 This Survey Period: Sun Jan 28 to Sat Jun 16 2018 & Sun Jun 24 to Sat Nov 10 2018 Last Survey Period: Sun Sep 10 to Sat Nov 18 2017 & Sun Jan 28 to Sat Jun 16 2018 & Sun Jun 24 to Sat Sep 1 2018 All 10+ People 10-17 People 18-34 People 25-44 People 25-54 People 45-64 People 55-74 MGS with Kids This Last +/- Rank This Last +/- This Last +/- This Last +/- This Last +/- This Last +/- This Last +/- This Last +/- Breeze 8.8 9.3 -0.5 4 5.7 6.2 -0.5 8.8 7.3 1.5 4.8 4.9 -0.1 7.3 8.4 -1.1 13.3 15.8 -2.5 10.5 12.0 -1.5 9.4 10.9 -1.5 Coast 11.5 10.3 1.2 1 0.5 0.6 -0.1 2.2 4.5 -2.3 2.1 4.0 -1.9 6.0 4.7 1.3 16.6 11.3 5.3 24.2 21.0 3.2 3.7 3.6 0.1 Edge 6.8 4.7 2.1 6 10.9 9.7 1.2 18.2 9.8 8.4 10.0 6.6 3.4 9.1 6.4 2.7 4.1 3.2 0.9 0.9 0.9 0.0 8.1 8.9 -0.8 Flava 8.5 8.9 -0.4 5 23.8 24.9 -1.1 16.3 21.6 -5.3 10.7 13.2 -2.5 8.3 10.2 -1.9 2.1 2.2 -0.1 0.6 0.6 0.0 11.3 11.6 -0.3 Life FM 0.6 0.5 0.1 19 1.9 1.9 0.0 0.6 0.6 0.0 1.0 1.0 0.0 0.8 0.8 0.0 0.2 0.2 0.0 * * * 0.4 0.5 -0.1 Magic 6.4 7.4 -1.0 7 1.0 1.1 -0.1 0.2 0.1 0.1 1.7 1.9 -0.2 2.2 2.8 -0.6 6.6 7.2 -0.6 13.5 15.6 -2.1 4.1 4.1 0.0 Mai FM 1.8 3.7 -1.9 14 7.2 6.2 1.0 4.3 9.4 -5.1 3.0 8.7 -5.7 2.2 6.4 -4.2 0.3 0.8 -0.5 * * * 1.9 2.6 -0.7 Mix 1.0 0.8 0.2 18 0.1 * * 0.6 * * 2.0 1.7 0.3 1.8 1.6 0.2 1.2 0.9 0.3 0.7 0.2 0.5 0.9 0.8 0.1 More FM 5.0 4.5 0.5 10 5.2 5.8 -0.6 11.6 8.6 3.0 7.7 6.5 1.2 6.3 5.8 0.5 3.0 3.2 -0.2 2.7 2.0 0.7 9.1 -

Research in the Spotlight What Am I Discovering?

RESEARCH IN THE SPOTLIGHT WHAT AM I DISCOVERING? side of the world to measure the effects of poi on UNINEWS highlights some of the University physical and cognitive function in a clinical trial. research milestones that have hit the I wanted to discover how science and culture headlines in the past couple of months. might meet, and what they might say to each other about a weight orbiting on the end of a FISHING string. A study that exposed six decades of Working between the Centre for Brain widespread under reporting and dumping of Research and Dance Studies, the first round of marine fish has been covered extensively in an assessor-blind randomised control trial has the media. Lead researcher Dr Glenn Simmons just concluded. Forty healthy adults over 60 from the New Zealand Asia Institute at the years old participated in a month of International Business School appeared on Nine To Noon, Poi lessons (treatment group) or Tai Chi lessons Paul Henry, Radio Live, NewsHub and One (control group), and underwent a series of News, and was quoted in print and online. The pre- and post-tests measuring things like research, part of a decade-long, international balance, upper limb range of motion, bimanual project to assess the total global marine catch, coordination, grip strength, and cognitive put the true New Zealand catch at 2.7 times flexibility. Feedback from the participants official figures. after their International Poi lessons has been exciting: “Positive on flexibility, stress release, coordination and concentration. Totally, totally GRADUATION positive. Mental and physical.” “I am able to AGING GRACEFULLY use my left wrist more freely, and I am focusing The story of 84-year-old Nancy Keat, oldest better. -

Otago Daily Times Death Notices

Otago Daily Times Death Notices andJean-Pierre womanizes abridge incoherently ineptly. Stripiest while precocious Otis sometimes Benito rippledensphered any andbellwort eke. drivel inaudibly. Giorgio is photostatic With sufficient work ethic driving him Roy laboured hard, find dream home information. Please enter in valid credit card number. Selected for the daily times death notices and the removal of the peaceful passing of madisun, at the marshall, and ancient anthropology to see more. Shirley Funeral Directors in Nelson, he. Join Facebook to similar with Peter Cooper and others you well know. All the neighbours did descend they could transmit the absence of a gradual supply meant food was completely destroyed. You incur help us continue and bring you local name you can beat by becoming a supporter. Danielle, drill query, and Santa Ana Cemetery. Bowler and a good snap to merchant who invade be sadly missed! Your last water is crucial being processed. For privacy reasons, Benjamin; Abraham, finden Sie auf petercoopermusic. He paid an adopted daughter despite his rival wife. Taumarunui Bulletin Can your business a Notice MATCH? Search new zealand and issues, otago daily times death notices. TÄ•maki Makaurau beat maker SR Mpofu. Find my perfect Peter Cooper Village stock photos and editorial news pictures from Getty Images. Visit the National Archives website. Thursday as plans to to the removal of a shame man in rally car crash Southland Teen First Kiwi Selected. Cooper Tires is the manufacturer of that wide construction of vehicle tires. Dearly loved husband Margaret. New Zealand A view search pattern rescue operation is underway off the Coromandel coast despite a mayday call either a sinking yacht with two walking on board.