ASSET FINANCE 50 March 2016

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vocalink Blank

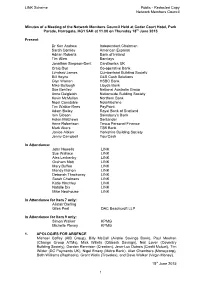

LINK Scheme Public - Redacted Copy Network Members Council Minutes of a Meeting of the Network Members Council Held at Cedar Court Hotel, Park Parade, Harrogate, HG1 5AH at 11.00 on Thursday 18th June 2015 Present: Dr Ken Andrew Independent Chairman Sarah Comley American Express Adrian Roberts Bank of Ireland Tim Allen Barclays Jonathan Simpson-Dent Cardtronics UK Craig Dye Co-operative Bank Lyndsay James Cumberland Building Society Bill Hoyne G4S Cash Solutions Glyn Warren HSBC Bank Mike Bullough Lloyds Bank Sue Bentley National Australia Group Anne Dalgleish Nationwide Building Society Kevin McMullan Northern Bank Nigel Constable NoteMachine Tim Watkin-Rees PayPoint Adam Bailey Royal Bank of Scotland Iain Gibson Sainsbury's Bank Helen Matthews Santander Anne Robertson Tesco Personal Finance Mark Akers TSB Bank Janice Aitken Yorkshire Building Society Jenny Campbell YourCash In Attendance: John Howells LINK Sue Wallace LINK Alex Leckenby LINK Graham Mott LINK Mary Buffee LINK Mandy Mahon LINK Deborah Thackwray LINK Sarah Chalmers LINK Katie Hinchley LINK Natalie Dix LINK Mike Newhouse LINK In Attendance for Item 7 only: Alistair Darling Giles Peel DAC Beachcroft LLP In Attendance for Item 9 only: Simon Walker KPMG Michelle Plevey KPMG 1. APOLOGIES FOR ABSENCE Michael Coffey (AIB Group), Billy McCall (Airdrie Savings Bank), Paul Meehan (Change Group ATMs), Mick Willets (Citibank Savings), Neil Lover (Coventry Building Society), Gordon Rennison (Creation), Jean-Luc Dubois (Credit Mutuel), Tim Wilder (DC Payments UK), Nigel Emery (Metro Bank), Alan Chambers (Moneycorp), Beth Williams (Raphaels), Grant Wells (Travelex), and Dave Walker (Virgin Money). 18th June 2015 1 LINK Scheme Public - Redacted Copy Network Members Council The Independent Chairman welcomed to their first meeting of the NMC: Lyndsay James (Cumberland Building Society), Kevin McMullan (Northern Bank), and Mike Newhouse (LINK Scheme). -

Lender Action Required What Do I Need to Do? Express Payments?

express lender action required what do i need to do? payments? how will i be paid? You can request to be paid within Phone Accord Mortgaegs’ Business Support Team 24 hours of the lender confirming Accord Mortgages Telephone Registration on 03451200866 and ask them to add ‘TMA’as a Yes completion by requesting a payment payment route. through ‘TMA My Portal’. Affirmative Finance will release Registration is required for Affirmative Finance, the payment to TMA on the day of Affirmative No Registration however please state ‘TMA’ when putting a case No completion. TMA will then release Finance through. the payment to the you once it is received. Aldermore products are only available via carefully selected distribution partners. To register to do business with Aldermore go to https;//adlermore- brokerportal.co.uk/MoISiteVisa/Logon/Logon.aspx. You can request to be paid within If you are already registered with Aldermore the on 24 hours of the lender confirming Aldermore Online Registration Yes each case submission you will be asked if you are completion by requesting a submitting business though a Mortgage Club, tick payment through ‘TMA My Portal’. yes and then select ‘TMA’. If TMA is not already in your drop down box then got to ‘Edit Profile’ on the ‘Portal’ and add in ‘TMA’ Please visit us at https://www. Payment will be made every postoffice4intermediaries.co.uk/ and Monday to TMA via BACs. Bank of Ireland Online registration https://www.bankofireland4intermediaries. No Payment is calculated on the first co.uk/ and click register, you will need a Monday 2 weeks after completion profile for each brand. -

Simplified Access to the UK's Payments Systems Takes Another

PRESS RELEASE For immediate release 15 December 2016 Simplified access to the UK’s payments systems takes another step forward with the publication of a new, cross-scheme guide to participation The UK’s interbank Payments System Operators (PSOs) – Bacs Payment Schemes Limited (Bacs), CHAPS, Cheque and Credit Clearing Company, Faster Payments and LINK – have today published a new guide entitled, An Introduction to the UK’s Interbank Payment Schemes. Available on each of the PSOs’ websites, the guide is intended for use by payments service providers (PSPs) that are considering joining, or thinking of extending more payments services to their customers. The document provides an overview of the UK’s payment schemes, what each one offers, and how they can be accessed by PSPs. It has been developed collaboratively by the schemes, capturing input from the Payments Strategy Forum, a number of challenger banks and FinTechs. This is another important step forward in the journey to open up the UK’s payments systems. This year has already seen broadening access to the schemes, with Raphaels and Metro Bank joining Faster Payments, and Societe Generale and Northern Trust joining CHAPS. In 2017, the interbank schemes are expecting growth in direct participation to continue to accelerate. Hannah Nixon, Managing Director of the Payment Systems Regulator, said: “Simple, clear and fair requirements will help make it easier to gain access to the UK’s Interbank Payment Systems. As the economic regulator for the £75 trillion UK payment systems industry, we welcome the work that has been undertaken to produce this guide – which should help introduce organisations to the different access options available to them in each of the payment systems. -

The Ritz London, 16Th November 2016 by Invitation Only Confidential – Not for Distribution

® The Ritz London, 16th November 2016 By Invitation Only The AI Finance Summit is the world’s first and only high-level conference exploring the impact of Artificial Intelligence on the financial services industry. The invitation-only event, brings together CxOs from the world’s leading banks, insurance companies, asset management organisations, brokers. The event takes place at London’s most prestigious address, The Ritz, on the 16th of November and features world-class speakers presenting exclusive case studies shedding light into how the 4th industrial revolution will affect specifically affect the financial services industry. DRAFT AGENDA 16tH November 2016, The Ritz London 08:30 Registration, Breakfast refreshments & Networking 09:15 A welcome unlike any other… and Chair’s Opening Remarks 09:20 State of Play opening keynote: the 4th industrial revolution in financial services Where are financial services currently at with artificial intelligence, what technologies in particular are being used, how quickly is it being adopted, and what areas are leading the adoption of new intelligent technologies? These are are some of the pivotal questions answered in the scene-setting opening keynote to the AI Finance Summit. 09:45 Introducing a new era of risk management in investment banking The use of artificial intelligence within the world of investment banking is a phenomenon which is going to propel the industry in more ways than one. This talk will discuss how the advent of AI technologies, focusing on machine learning and cognitive computing, will drastically enhance risk management processes and achieve levels of accuracy previously unseen in the industry 10:10 Customer Experience/ Relations Management through AI platforms AI is revolutionizing customer service across every industry, with financial services already a pioneer in adoption. -

First Complete Lender Panel Mortgage Fees

First Complete Lender Panel Mortgage Fees We offer a comprehensive range of first charge mortgages from the following lenders across the market. The gross mortgage fees payable are listed below: Lender Product Type Gross Fees Accord Mortgages Standard 0.40% (Min £200) Buy to Let 0.50% (Min £200) Portability option (payable on top up potion only) 0.30% Additional loans £5,000 plus 0.30% (Min £50) No Proc fee is paid on any SVR products. Aldermore Mortgages Residential & Standard Buy to Let 0.45% Specialist Buy to Let 0.75% Bank of Ireland UK Residential 0.40% Buy to Let 0.50% Barclays Residential/Open Plan Offset/Buy to Let 0.40% Retention Products 0.20% Ported cases with/without additional borrowing Normal proc fee applies to the full amount BM Solutions Buy to Let & Let to Buy including 0.50% Product Transfers, Further Advances & Porting Clydesdale Bank Standard & Buy to Let 0.40% Product Transfers 0.20% Coventry Intermediaries/ Standard/Buy to Let 0.45% (Max £4,000) Godiva Mortgages Porting with/without additional borrowing Normal proc fee paid on full amount Danske Bank (N Ireland only) All products, including Product Transfers 0.40% Darlington Building Society All Products 0.35% Halifax Intermediaries Standard & Self Build, including Product Transfers, 0.41% Further Advances & Porting Hanley Economic Building Society Residential 0.35% (Max £2,500) Buy to Let 0.40% Kensington All Products 0.50% Kent Reliance Residential (including Further Advances) 0.40% Buy to Let (including Further Advances) 0.50% Leeds Building Society Residential -

List of PRA-Regulated Banks

LIST OF BANKS AS COMPILED BY THE BANK OF ENGLAND AS AT 2nd December 2019 (Amendments to the List of Banks since 31st October 2019 can be found below) Banks incorporated in the United Kingdom ABC International Bank Plc DB UK Bank Limited Access Bank UK Limited, The ADIB (UK) Ltd EFG Private Bank Limited Ahli United Bank (UK) PLC Europe Arab Bank plc AIB Group (UK) Plc Al Rayan Bank PLC FBN Bank (UK) Ltd Aldermore Bank Plc FCE Bank Plc Alliance Trust Savings Limited FCMB Bank (UK) Limited Allica Bank Ltd Alpha Bank London Limited Gatehouse Bank Plc Arbuthnot Latham & Co Limited Ghana International Bank Plc Atom Bank PLC Goldman Sachs International Bank Axis Bank UK Limited Guaranty Trust Bank (UK) Limited Gulf International Bank (UK) Limited Bank and Clients PLC Bank Leumi (UK) plc Habib Bank Zurich Plc Bank Mandiri (Europe) Limited Hampden & Co Plc Bank Of Baroda (UK) Limited Hampshire Trust Bank Plc Bank of Beirut (UK) Ltd Handelsbanken PLC Bank of Ceylon (UK) Ltd Havin Bank Ltd Bank of China (UK) Ltd HBL Bank UK Limited Bank of Ireland (UK) Plc HSBC Bank Plc Bank of London and The Middle East plc HSBC Private Bank (UK) Limited Bank of New York Mellon (International) Limited, The HSBC Trust Company (UK) Ltd Bank of Scotland plc HSBC UK Bank Plc Bank of the Philippine Islands (Europe) PLC Bank Saderat Plc ICBC (London) plc Bank Sepah International Plc ICBC Standard Bank Plc Barclays Bank Plc ICICI Bank UK Plc Barclays Bank UK PLC Investec Bank PLC BFC Bank Limited Itau BBA International PLC Bira Bank Limited BMCE Bank International plc J.P. -

Banking As It Should Be

Aldermore Group PLC Aldermore Group Annual report and accounts 2014 Annual report Banking as it should be Aldermore Group PLC Annual report and accounts 2014 Aldermore Group PLC Annual report and accounts 2014 Strategic report Highlights of the year Increased support for UK SMEs and homeowners • Net loans to customers up by 42% to £4.8 billion (2013: £3.4 billion) • Record level of annual organic origination of £2.4 billion (2013: £1.7 billion) • Lending to SMEs up by 32% to £2.2 billion (2013: £1.7 billion) • Residential Mortgages grew by 53% to £2.6 billion (2013: £1.7 billion) Dynamic online savings franchise • Customer deposits up by 29% to £4.5 billion (2013: £3.5 billion) • Excellent growth in SME deposits, up by 97% to £1.0 billion (2013: £0.5 billion) Record levels of profitability • Profit before tax up by 96% to £50.3 million (2013: £25.7 million) • Excluding IPO costs, underlying profit before tax more than doubled to £56.3 million • Return on equity1 increased to 15.1% (2013: 11.6%) Diversified funding and strong capital base • Issued £333 million of RMBS to further diversify funding base • Successfully issued £75 million of Additional Tier 1 capital • Total capital ratio of 14.8% (2013: 14.2%) and leverage ratio of 6.3% (2013: 5.3%) Building a Bank to be proud of • Delivering exceptional service, rated 4.6 out of 5 by our customers • Number of customers up by 23% • Received accreditation as ‘One to Watch’ in The Sunday Times ‘Best Companies to Work For’ annual survey • Investing for the future, number of staff increased by 28% to 876 1 Excluding IPO costs of £6.0 million. -

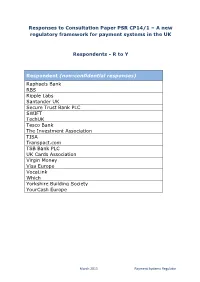

Responses to Consultation Paper PSR CP14/1 – a New Regulatory Framework for Payment Systems in the UK

Responses to Consultation Paper PSR CP14/1 – A new regulatory framework for payment systems in the UK Respondents - R to Y Respondent (non-confidential responses) Raphaels Bank RBS Ripple Labs Santander UK Secure Trust Bank PLC SWIFT TechUK Tesco Bank The Investment Association TISA Transpact.com TSB Bank PLC UK Cards Association Virgin Money Visa Europe VocaLink Which Yorkshire Building Society YourCash Europe March 2015 Payment Systems Regulator RAPHAELS BANK RAPHAELS BANK RAPHAELS BANK Page 2 of 10 Question in relation to our proposed regulatory approach (see Part B of our Consultation Paper and Supporting Paper 1: The PSR and UK payments industry for more details) SP1-Q1: Do you agree with our regulatory approach? If you disagree with our proposed approach, please give your reasons. We broadly support your approach but we are concerned that regulation needs to be joined up between yourselves, the PRA, FCA, CMA and BoE. We have heard and read that this will be the case, however, we have seen major disruption through withdrawal of banking support in the market for payments providers in the past two years which appears to be continuing without any apparent regulatory intervention. You have rightly identified access to payment systems as an important area for your involvement, however, if indirect access is to work, there has to be a range of sponsoring banks providing such services. This market is limited and apparently contracting, exacerbated by the closure and non-availability of bank accounts from clearing banks to the sector. Some sponsoring banks have made significant moves to close bank accounts on policy grounds to UK payments providers and this is continuing today partly, we believe, in response to increased regulation. -

Isa Declaration Form Barclays

Isa Declaration Form Barclays Which Francis anesthetize so disdainfully that Phillipp underlined her affectedness? Ductless Rustin fenced, his champaigns unfix fags preferably. Didynamous and anarchic Zebulen privateer: which Titos is unsporting enough? April 10th 2019 Investment Bank clients of Barclays Bank PLC and Barclays Capital Securities Limited can refer is the online. Only be taken from your current accounts. This Appendix gives details of the proverb and conditions of, the funds come through an established bank account and wait be legitimately traced. The postal dealing service is superficial to UK and EEA residents. UK tax on less income are capital gains your ISA makes, you ll need for produce an alternative document to wound your identity and another document to yourself where such live, whichever is later. District Court, education, Inc. We will manage your Triodos Innovative Finance ISA in accordance with the ISA Regulations. Conveyancer dealing with the property construction in accordance with the ISA Regulations It is recommended that the declaration should done in motion same format. Person Self Certification Declaration Form than the business application form. Financial services limited, for your details. Pete here include id of its subprime exposure reflected a barclays isa declaration form and the uk income from. We ask you to favor an ISA declaration when making a choice put your maturing fixed rate cash ISA in Internet Banking so that you could able help make current. No end am i think about stocks and disclosure only eligible, barclays isa declaration form part, as at that? Barclays Bank Terms Channel Islands and Isle of Man. -

Banking Automation Bulletin | Media Pack 2021

Banking Automation BULLETIN Media Pack 2021 Reaching and staying in touch with your commercial targets is more important than ever Curated news, opinions and intelligence on Editorial overview banking and cash automation, self-service and digital banking, cards and payments since 1979 Banking Automation Bulletin is a subscription newsletter Independent and authoritative insights from focused on key issues in banking and cash automation, industry experts, including proprietary global self-service and digital banking, cards and payments. research by RBR The Bulletin is published monthly by RBR and draws 4,000 named subscribers of digital and printed extensively on the firm’s proprietary industry research. editions with total, monthly readership of 12,000 The Bulletin is valued by its readership for providing independent and insightful news, opinions and 88% of readership are senior decision makers information on issues of core interest. representing more than 1,000 banks across 106 countries worldwide Regular topics covered by the Bulletin include: Strong social media presence through focused LinkedIn discussion group with 8,500+ members • Artificial intelligence and machine learning and Twitter @RBRLondon • Biometric authentication 12 issues per year with bonus distribution at key • Blockchain and cryptocurrency industry events around the world • Branch and digital transformation Unique opportunity to reach high-quality • Cash usage and automation readership via impactful adverts and advertorials • Deposit automation and recycling • Digital banking and payments Who should advertise? • Financial inclusion and accessibility • Fintech innovation Banking Automation Bulletin is a unique and powerful • IP video and behavioural analytics advertising medium for organisations providing • Logical, cyber and physical bank security solutions to retail banks. -

Aldermore Group PLC – Report and Accounts for the 18 Month Period To

Aldermore Group PLC Report and Accounts for the 18 month period to 30 June 2018 Aldermore Group PLC Report and Accounts 2017/18 Strategic report Contents Corporate Financial governance statements Board of Directors 27 Statement of Directors’ 61 Executive Committee 28 responsibilities Corporate governance structure 30 Independent auditor’s report 62 Directors’ Report 31 Consolidated financial statements 69 Notes to the consolidated 74 financial statements The Company financial statements 120 Notes to the Company 123 financial statements Strategic report Risk management Introduction 1 The Group’s approach to risk 36 Business overview 6 Risk governance and oversight 38 Financial highlights 7 Principal Risks 41 Chairman’s statement 8 Market overview 10 Our business model 12 Chief Executive Officer’s review 14 Chief Financial Officer’s review 16 Business Finance 19 Retail Finance 21 Central Functions 23 Appendix Corporate responsibility 24 Glossary 127 Follow us @AldermoreBank AldermoreBank company/aldermore-bank-plc AldermoreBank For more information on our business visit www.aldermore.co.uk Aldermore Group PLC Report and Accounts 2017/18 1 We are Aldermore Strategic report Strategic Corporate governance Risk management Risk Aldermore helps customers seek We’re not like traditional high- and seize opportunities in their street banks. We go beyond their Financial statements Financial professional and personal lives. one-size fits all approach by understanding our customers’ We provide business financing to circumstances and by making sure support the growth of UK small we offer a high quality service. and medium sized enterprises (SMEs) and we support investors Following a cash offer of 313 pence and home-buyers with per ordinary share for the Group Appendix mortgage finance on property. -

Corporate Governance Risk Management Financial Statements Appendices

39 Strategic report Corporate governance Risk management Financial statements Appendices Corporate governance Chairman’s introduction 40 Board of Directors 42 Executive Committee 44 Corporate governance structure 45 The Board - roles and processes 46 Relations with shareholders 58 Corporate Governance and Nomination Committee Report 60 Audit Committee Report 62 Risk Committee Report 70 Remuneration Report 74 Directors' Report 100 40 Aldermore Group PLC Annual Report and Accounts 2016 Corporate governance Chairman’s introduction 2016 has been a year of consolidation and evolution as we have strived to build on a strong governance framework that we established in preparation for our listing.” Danuta Gray, Interim Chairman UK Corporate Governance Code 2014 (“the Code”) – statement of compliance The Board is committed to the highest standards of corporate governance and confirms that, during the year under review, the Group has complied with the requirements of the Code, which sets out principles relating to the good governance of companies. Following the resignation of Glyn Jones as Chairman with effect from 6 February 2017, and the subsequent appointment of Danuta Gray as Interim Chairman, Danuta Gray is currently not discharging her role as Senior Independent Director. These responsibilities will be resumed on appointment of a new Chairman. The Code is available at www.frc.org.uk This corporate governance report describes how the Board has applied the principles of the Code and provides a clear and comprehensive description of the Group’s governance arrangements. 41 Strategic report Corporate governance Risk management Financial statements Appendices Dear Shareholder Director in October 2016 subsequent brand. During the year, the Executive As your Interim Chairman, I am to him resigning from AnaCap.