The Henderson Smaller Companies Investment Trust Plc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Marlborough SPECIAL SITUATIONS FUND

MARLBOROUGH SPECIAL SITUATIONS FUND INTERIM REPORT AND UNAUDITED FINANCIAL STATEMENTS for the six month period ended 20 June 2019 MARLBOROUGH SPECIAL SITUATIONS FUND Authorised Fund Manager and Registrar Marlborough Fund Managers Ltd Marlborough House 59 Chorley New Road Bolton BL1 4QP Investor Support: (0808) 145 2500 (FREEPHONE) Authorised and regulated by the Financial Conduct Authority. Trustee HSBC Bank plc 8 Canada Square London E14 5HQ Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Investment Adviser Hargreave Hale Limited Talisman House Boardmans Way Blackpool Lancashire FY4 5FY Authorised and regulated by the Financial Conduct Authority. Auditor Barlow Andrews LLP Carlyle House 78 Chorley New Road Bolton BL1 4BY Directors of Marlborough Fund Managers Ltd Andrew Staley Chairman Nicholas F J Cooling Deputy Chairman Allan Hamer Joint Managing Director Wayne D Green Joint Managing Director Dom Clarke Finance Director Geoffrey Hitchin Investment Director Helen Derbyshire Director – Compliance & Risk Richard Goodall Director – Strategy & Business Development Guy Sears Non-Executive Director David Kiddie Non-Executive Director MARLBOROUGH SPECIAL SITUATIONS FUND CONTENTS PAGE AUTHORISED INVESTMENT ADVISER’S REPORT 1 AUTHORISED STATUS AND GENERAL INFORMATION 3 DIRECTORS’ STATEMENT 3 COMPARATIVE TABLE 4 SYNTHETIC RISK AND REWARD INDICATOR 5 PORTFOLIO STATEMENT 6 PORTFOLIO TRANSACTIONS 11 UNAUDITED INTERIM FINANCIAL STATEMENTS STATEMENT OF TOTAL -

To Arrive at the Total Scores, Each Company Is Marked out of 10 Across

BRITAIN’S MOST ADMIRED COMPANIES THE RESULTS 17th last year as it continues to do well in the growing LNG business, especially in Australia and Brazil. Veteran chief executive Frank Chapman is due to step down in the new year, and in October a row about overstated reserves hit the share price. Some pundits To arrive at the total scores, each company is reckon BG could become a take over target as a result. The biggest climber in the top 10 this year is marked out of 10 across nine criteria, such as quality Petrofac, up to fifth from 68th last year. The oilfield of management, value as a long-term investment, services group may not be as well known as some, but it is doing great business all the same. Its boss, Syrian- financial soundness and capacity to innovate. Here born Ayman Asfari, is one of the growing band of are the top 10 firms by these individual measures wealthy foreign entrepreneurs who choose to make London their operating base and home, to the benefit of both the Exchequer and the employment figures. In fourth place is Rolls-Royce, one of BMAC’s most Financial value as a long-term community and environmental soundness investment responsibility consistent high performers. Hardly a year goes past that it does not feature in the upper reaches of our table, 1= Rightmove 9.00 1 Diageo 8.61 1 Co-operative Bank 8.00 and it has topped its sector – aero and defence engi- 1= Rotork 9.00 2 Berkeley Group 8.40 2 BASF (UK & Ireland) 7.61 neering – for a decade. -

Rotork Annual Report 2006

2006 Annual Report & Accounts Rotork 2006 Annual Report & Accounts Rotork p.l.c. Rotork House Brassmill Lane Bath BA1 3JQ www.rotork.com Celebrating fifty years of innovation 2006 Annual Report & Accounts Rotork 2006 Annual Report & Accounts Rotork p.l.c. Rotork House Brassmill Lane Bath BA1 3JQ www.rotork.com Celebrating fifty years of innovation FINANCIAL HIGHLIGHTSRotork Annual Report & Accounts 2006 01. Financial Highlights Order Intake The fifties: page 05 • Order intake up 19% at £223m • Revenue up 18% at £206.7m £223m • Operating profit up 23% at £45.1m up 19% The sixties: page 07 • Recommended final dividend of 11.65p, up 18% • £8m additional interim dividend during 2007 Order book Operational Highlights £76m The seventies: page 08 up 19% • Continued strong growth achieved in Rotork Fluid System The eighties: page 11 • Chinese market still buoyant • New Shanghai manufacturing plant commenced production on schedule in the year • Increased focus on Service and Support with new @ management structure The nineties: page 12 The Noughties: page 15 Financial Highlights 01 Revenue (£m) Chairman’s Statement 02 Business Review 04 Geographical Review 16 206.7 Operating Profit - (£m) (£m) Rotork Marketing 18 continuing operations Board of Directors 20 Order Input 223.4 174.8 45.1 Report of the Directors 21 136.0 146.9 Corporate Governance 23 7.7 133.5 18 36.5 Corporate Social Responsibility 26 Remuneration Report 28 30.4 151.8 28.4 Independent Auditors’ Report 35 136.9 26.6 131.3 Consolidated Income Statement 36 Consolidated Balance Sheet 37 Consolidated Statement of Cash Flows 38 Consolidated Statement of Recognised Income and Expense 39 Notes to the Group Financial Statements 40 02 03 04 05 06 Rotork p.l.c. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Fund Fact Sheet

Franklin Templeton Funds GB00B3ZGH246 FTF Franklin UK Mid Cap Fund - A 31 July 2021 (inc) Fund Fact Sheet For Professional Client Use Only. Not for distribution to Retail Clients. Fund Overview Performance Base Currency for Fund GBP Performance over 5 Years in Share Class Currency (%) Total Net Assets (GBP) 1.16 billion FTF Franklin UK Mid Cap Fund A (inc) FTSE 250 ex-Investment Trusts Index Fund Inception Date 17.10.2011 180 Number of Issuers 36 Benchmark FTSE 250 ex-Investment 160 Trusts Index IA Sector UK All Companies 140 ISA Status Yes 120 Summary of Investment Objective The Fund aims to grow in value by more than the FTSE 250 100 (ex-Investment Trusts) Index, from a combination of income and investment growth over a three to five-year period after all fees and costs are deducted. 80 07/16 01/17 07/17 01/18 07/18 01/19 07/19 01/20 07/20 01/21 07/21 Fund Management Discrete Annual Performance in Share Class Currency (%) Richard Bullas: United Kingdom 07/20 07/19 07/18 07/17 07/16 Mark Hall: United Kingdom 07/21 07/20 07/19 07/18 07/17 Dan Green, CFA: United Kingdom A (inc) 36.52 -12.79 -1.25 9.89 23.81 Marcus Tregoning: United Kingdom Benchmark in GBP 42.85 -15.10 -4.98 8.39 17.21 Ratings - A (inc) Performance in Share Class Currency (%) Cumulative Annualised Overall Morningstar Rating™: Since Since Asset Allocation 1 Mth 3 Mths 6 Mths YTD 1 Yr 3 Yrs 5 Yrs Incept 3 Yrs 5 Yrs Incept A (inc) 4.45 5.93 20.14 16.83 36.52 17.58 59.90 821.63 5.55 9.84 10.60 Benchmark in GBP 3.24 3.01 16.86 15.60 42.85 15.25 46.41 622.69 4.84 7.92 9.38 Prior to 7 August 2021, the Fund was named Franklin UK Mid Cap Fund. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Quarterly Investor Letter March 2015

Quarterly investor letter March 2015 ‘In the short term the market is like a voting machine tallying up which firms are popular and unpopular. In the long run, the mar- ket is like a weighing machine—assessing the substance of a company.’ Benjamin Graham Dear fellow shareholders, As long term investors, the partners at Castlebay are wary of measuring investment performance over short periods of time, such as a calendar quarter or even a year. Our approach to this quarterly letter is to set out for you our investment philosophy and to update you along the way, in what we hope will be a long and prosperous investment journey with us. As stock-pickers we shall highlight one or two stock examples in each letter. Through our commentary we aim to explain clearly how we ‘assess the substance of the companies’ in which we invest, whilst ignoring the market herd who ‘vote’ with increasing frequency and cost, due to their myopia. The value of investments can fall as well as rise and you might not get back what you have invested. Our guiding principles are set out below and we hope you enjoy the read! Our guiding principles: Transparency & alignment of best interests with our fellow shareholders Adherence to our investment philosophy and process—high quality & supportive valuations Independence of thought in order to avoid the market herd A focus on costs: management fees capped, low turnover of companies in the fund The Portfolio in the first quarter 2015 The launch of the fund at the end of January coincided with a strong recovery in Petrofac which had sold off heavily in the final quarter of 2014 as the price of oil plummeted & investors became irrational sellers of all oil related companies. -

2013 Agms: Key Trends and Issues from a Review of 215 FTSE 350 Companies June 2013

2013 AGMs: Key trends and issues from a review of 215 FTSE 350 companies June 2013 Statistics Commentary RESOLUTIONS Annual re-election of all directors 99% (213 companies) proposed annual re- 3% (7 companies) amended their articles to election of all directors reflect annual re-election Authority to allot shares: extra one 67% (144 companies) proposed a resolution This is similar to the results for 2012 third authority for the extra one third authority; 27% (57 companies) included a statement that where Under the UK Corporate Governance Code this extra one-third authority was used, the (Code) FTSE 350 directors should be subject directors would stand for re-election to annual election, so no longer necessary Any resolution to convene general 84% (181 companies) passed a resolution to NAPF recommends that companies should only meeting on 14 days’ notice convene a general meeting on 14 clear days’ call a general meeting on 14 clear days’ notice notice; 73% (158 companies) stated the in limited circumstances and these should be circumstances where meetings will be held on explained when tabling the resolution 14 clear days’ notice Details of any unusual resolution Resolutions proposed to approve an increase A few companies have increased this to in maximum aggregate fees payable to around £700,000 to allow them to appoint directors non-executive directors to the board Details of substantial vote (10-49%) 15% (33 companies) detailed substantial votes So far this year no FTSE 350 company has had against the directors’ remuneration against -

Morningstar Report

Report as of 23 Sep 2021 FTF Franklin UK Mid Cap Fund W (acc) Morningstar® Category Morningstar® Benchmark Fund Benchmark Morningstar Rating™ UK Mid-Cap Equity FTSE 250 Ex Investment Trust TR GBP FTSE 250 Ex Investment Trust TR GBP QQQ Used throughout report Investment Objective Performance The Fund aims to grow in value by more than the FTSE 250 192 (ex-Investment Trusts) Index, from a combination of 169 income and investment growth over a three to five-year 146 period after all fees and costs are deducted. The Fund will 123 invests at least two thirds (but typically significantly more) 100 in the shares of medium-sized companies that are 77 constituents of the FTSE 250 (ex-Investment Trusts) Index and that are incorporated/domiciled in the UK or which 2016 2017 2018 2019 2020 2021-08 have significant business operations in the UK. This will -0.23 26.43 -13.46 42.30 -14.19 23.11 Fund typically be around 30–50 companies. 5.08 18.24 -15.15 30.79 -8.48 22.42 Benchmark 5.27 19.55 -14.94 30.83 -2.93 19.16 Category Risk Measures Trailing Returns % Fund Bmark Cat Quarterly Returns % Q1 Q2 Q3 Q4 3Y Alpha 1.27 3Y Sharpe Ratio 0.45 3 Months 7.81 6.09 6.44 2021 5.67 6.24 - - 3Y Beta 1.03 3Y Std Dev 23.59 6 Months 16.57 13.73 13.19 2020 -34.73 13.41 -3.15 19.70 3Y R-Squared 95.57 3Y Risk Avg 1 Year 48.84 50.23 43.80 2019 10.97 6.77 5.53 13.81 3Y Info Ratio 0.27 5Y Risk Avg 3 Years Annualised 8.30 6.82 8.43 2018 -2.73 6.70 -3.28 -13.79 3Y Tracking Error 5.02 10Y Risk abv avg 5 Years Annualised 10.37 7.88 10.12 2017 6.51 6.02 4.41 7.23 Calculations -

What Makes an Outstanding Finance Director?

what makes an outstanding finance director? “ Right now as an FD, you can have a major impact – and if you don’t seize the moment they’ll find somebody else who will.” Steve Marshall, Chair, Balfour Beatty Plc In association with Directorbank Group Directorbank Group Comprising two market-leading brands, Hanson Green and Directorbank, the Directorbank Group offers a complete range of board level recruitment solutions to the full spectrum of companies from private equity backed businesses and family firms to FTSE and AIM listed organisations. Finance Director appointments are delivered by search consultants with many years experience in this specialist market. Directorbank is a leading provider of executive, Hanson Green is a specialist board practice Grant Thornton UK LLP is a leading financial and business adviser, operating non-executive and interim directors with a search firm with a market leading position in out of 28 offices. Led by 215 partners and employing nearly 4,000 of the market-leading position in the private equity the appointment of chairman and non-executive profession’s brightest minds, we provide personalised assurance, tax and sector. directors and a respected executive search specialist advisory services to over 40,000 individuals, privately-held practice. businesses and public interest entities. More than 70 leading private equity houses from across Europe retain Directorbank’s Hanson Green’s proven track record of solving Our offer to the market is great depth of expertise, delivered in a distinctive services to gain access to their exceptional clients’ recruitment challenges, combined with and personal way. Through proactive, client-centric relationships, our teams network of top level board directors for their the unrivalled quality of their service, has made deliver solutions to problems, not pre-packaged products and services. -

FTSE Factsheet

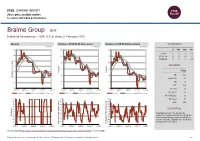

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 21 February 2020 Braime Group BMT Industrial Engineering — GBP 17.5 at close 21 February 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Feb-2020 21-Feb-2020 21-Feb-2020 26 110 120 1D WTD MTD YTD Absolute 0.0 0.0 6.1 -5.4 24 100 110 Rel.Sector 0.8 0.4 4.7 -1.1 Rel.Market 0.4 0.1 4.1 -3.9 22 90 100 VALUATION 20 80 90 Trailing 18 RelativePrice RelativePrice 70 80 PE 10.9 Absolute(localPrice currency) 16 EV/EBITDA 6.0 60 70 14 PB 1.7 PCF 10.7 12 50 60 Div Yield 0.7 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Price/Sales 0.7 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.2 100 90 100 Div Payout 7.0 90 80 90 ROE 17.4 80 70 80 70 Index) Share 70 Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 The principal activities of the group are the 40 40 RSI RSI (Absolute) 30 manufacture of metal presswork and the distribution 30 30 of bulk material handling components, trading from 20 20 20 locations in Australia, England, France, South Africa, 10 10 10 Thailand and the United States. -

Company Date Type Resid Proposal Vote Rescode CARR's GROUP

Company Date Type ResId Proposal Vote ResCode CARR'S GROUP PLC 07/01/2020 AGM 1 Receive the Annual Report Abstain 201 CARR'S GROUP PLC 07/01/2020 AGM 2 Approve the Dividend For 401 CARR'S GROUP PLC 07/01/2020 AGM 3 Elect Peter Page Oppose 301 CARR'S GROUP PLC 07/01/2020 AGM 4 Re-elect Tim Davies For 301 CARR'S GROUP PLC 07/01/2020 AGM 5 Re-elect Neil Austin For 301 CARR'S GROUP PLC 07/01/2020 AGM 6 Re-elect Alistair Wannop Oppose 301 CARR'S GROUP PLC 07/01/2020 AGM 7 Re-elect John Worby Oppose 301 CARR'S GROUP PLC 07/01/2020 AGM 8 Re-elect Ian Wood Oppose 301 CARR'S GROUP PLC 07/01/2020 AGM 9 Appoint the Auditors For 501 CARR'S GROUP PLC 07/01/2020 AGM 10 Allow the Board to Determine the Auditor's Remuneration For 503 CARR'S GROUP PLC 07/01/2020 AGM 11 Approve the Remuneration Report Oppose 202 CARR'S GROUP PLC 07/01/2020 AGM 12 Issue Shares with Pre-emption Rights For 601 CARR'S GROUP PLC 07/01/2020 AGM 13 Issue Shares for Cash For 602 CARR'S GROUP PLC 07/01/2020 AGM 14 Authorise Share Repurchase Oppose 607 CARR'S GROUP PLC 07/01/2020 AGM 15 Meeting Notification-related Proposal For 1511 DIPLOMA PLC 15/01/2020 AGM 1 Receive the Annual Report Oppose 201 DIPLOMA PLC 15/01/2020 AGM 2 Approve the Dividend For 401 DIPLOMA PLC 15/01/2020 AGM 3 Re-elect John Nicholas Oppose 301 DIPLOMA PLC 15/01/2020 AGM 4 Elect Johnny Thomson For 301 DIPLOMA PLC 15/01/2020 AGM 5 Re-elect Nigel Lingwood For 301 DIPLOMA PLC 15/01/2020 AGM 6 Re-elect Charles Packshaw For 301 DIPLOMA PLC 15/01/2020 AGM 7 Re-elect Andy Smith For 301 DIPLOMA PLC 15/01/2020 AGM 8