Debt-Long Term

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Differentiated Banks in India

. Differentiated Banks in India Differentiated Banks in India Under the recommendations of Dr. Nachiket Mor committee new step for the financial inclusion has been taken in the country. As per the recommendations RBI set up the guidelines for the new categories of banks i.e. Payment Banks and Small Finance Banks. Payments Banks in India On the recommendations of Dr. Nachiket Mor committee RBI (Reserve Bank of India) grants license for commencement of banking business under section 22(1) of Banking Regulation Act 1949 and registered as a private company under Companies Act. It is a new model of banks which is conceptualized by the RBI (Reserve Bank of India) The main objective of setting up of payment banks for the purpose of financial inclusion by providing: Small saving account Payment services Features of payment banks Non finance company entities and existing non bank prepaid instruments issuer may apply for the payments bank. Minimum capital required for the payment banks is Rs. 100 crore. Foreign shareholding is allowed to these banks but as per the regulations of FDI (Foreign Direct Investment). Payment Banks cannot provide lending services but allowed to distribute financial product such as mutual funds and insurance products. The bank must use the term payment bank in its name to differentiate it from other banks. 25% of the bank branches of the payment banks must be in unbanked rural areas. Services provided by the Payment Banks Acceptance of deposits (initially restricted to Rs 100,000). Payment Banks can provide services like ATM, net banking, debit cards and net banking. -

An Empirical Study on Selected Small Finance Bank in Mysuru with Reference to Micro, Small and Medium Enterprises

International Journal of Mechanical Engineering and Technology (IJMET) Volume 9, Issue 11, November 2018, pp. 723–731, Article ID: IJMET_09_11_073 Available online at http://www.iaeme.com/ijmet/issues.asp?JType=IJMET&VType=9&IType=11 ISSN Print: 0976-6340 and ISSN Online: 0976-6359 © IAEME Publication Scopus Indexed AN EMPIRICAL STUDY ON SELECTED SMALL FINANCE BANK IN MYSURU WITH REFERENCE TO MICRO, SMALL AND MEDIUM ENTERPRISES Abijith S and Raghavendra N Department of management and commerce, Amrita School of Arts and Sciences, Mysuru Amrita Vishwa Vidyapeetham, India ABSTRACT Bank is type of financial institution which provide services such as accepting deposit and providing credit facilities to their customers. Reserve Bank of India (RBI) is the governing body that has been taking care of the banking industry in our country. Over the past few years our banking industry has gone through numerous changes on such change has been in initiation Small Finance Banks. Small Finance Bank are those banks which perform basic services such as accepting deposit and lending loans to its customers. The main objective of Small Finance bank is to provide financial inclusion to disadvantaged section who are not served by other banks. This study tries to measure the challenges faced Small Finance Bank and to analyse the awareness among the Micro, Small and Medium enterprises about Small Finance Banks. KEYWORDS : Financial Inclusion, Small Financial Banks and Micro Small and Medium Enterprises Cite this Article Abijith S and Raghavendra N, an Empirical Study on Selected Small Finance Bank in Mysuru with Reference to Micro, Small and Medium Enterprises, International Journal of Mechanical Engineering and Technology, 9(11), 2018, pp. -

Andhra Bank Upi Complaint

Andhra Bank Upi Complaint Polyatomic Tedrick fribbled some cloakroom after leaden Rodger aquaplanes enormously. Urethral and Plantigradeself-satisfying and Nickey unsatirical belove Magnus threateningly peels hisand ergonomics grieved his atomise sempstress scrubbing minutely dissentingly. and unmurmuringly. Download Andhra Bank Upi Complaint pdf. Download Andhra Bank Upi Complaint doc. Editor of upi upipayment transaction bank upistatus app will is aget payer started Ichalkaranji to the best janata payment. sahakari Faced bank by a using bank andhra upi app, upi malwa complaint gramin with theybank, are you the have upi totransaction enter the detailssame will and be email needing address help isin your your concern. bank? Server Address or wallet will also to yourclear sim the andzonal timelinelevel, the to correct process person to the or bhim any upiupi appapplication customer on face bhim. issues Connectivity and accounts is failed of andyour andhra own css bank, here. the Or variousany problem banks with participating andhra complaint banks in using their multipleupi is linked bank accounts and govt. using Make upi your is making concern upi is autopayupi limit whichin phoneis the complaint is bad. Escalate with the your instructions. issue in orderGrab toyour learn complaint more than with one efficiency, upi app ifregister you and your to verify email your your appaccount. is failed A blog in thousands to with andhra of the upi recent complaint announcement regarding regardingthe money login to complain issue in theupi number.is limit to Kinddecode of upi the andhrabest person bank or which your nullifiescomment. any Forgot kind of that india. particular Found bankon bhim can andhra put a customer upi app register grievance whatsapp redressal pay of is Isthis. -

Payment Gateway

PAYMENT GATEWAY APIs for integration Contact Tel: +91 80 2542 2874 Email: [email protected] Website: www.traknpay.com Document version 1.7.9 Copyrights 2018 Omniware Technologies Private Limited Contents 1. OVERVIEW ............................................................................................................................................. 3 2. PAYMENT REQUEST API ........................................................................................................................ 4 2.1. Steps for Integration ..................................................................................................................... 4 2.2. Parameters to be POSTed in Payment Request ............................................................................ 5 2.3. Response Parameters returned .................................................................................................... 8 3. GET PAYMENT REQUEST URL (Two Step Integration) ........................................................................ 11 3.1 Steps for Integration ......................................................................................................................... 11 3.2 Parameters to be posted in request ................................................................................................. 12 3.3 Successful Response Parameters returned ....................................................................................... 12 4. PAYMENT STATUS API ........................................................................................................................ -

Tracking Performance of Payments Banks Against Financial Inclusion Goals

Tracking Performance of Payments Banks against Financial Inclusion Goals Amulya Neelam1 and Anukriti Tiwari September 2020 1Authors work with Dvara Research, India. Corresponding author’s email: [email protected] Contents 1. Introduction ........................................................................................................................................ 1 2. Rationale and Methodology ............................................................................................................... 3 3. Performance of Payments Banks ........................................................................................................ 4 3.1. Has there been a proliferation of transaction touchpoints? .......................................................4 3.1.1 Has there been an increase in Branch Spread? .....................................................................6 3.1.2 Establishment of own ATMs and Acquiring POS ....................................................................9 3.1.3 Banking Services in Unbanked Rural Centres ...................................................................... 10 3.2 What are the relative volumes and the nature of transactions through PBs? ........................... 12 3.2.1 Transactions at Physical Touchpoints .................................................................................. 12 3.2.2 Digital Transactions .............................................................................................................. 13 4.The Competitive Landscape for -

Leveraging Small Finance Banks in Achieving Financial Inclusion in India

Seshadripuram Journal of Social Sciences Special Issue, December 2019 ISSN: 2581-6748, Journal Home page: https://mcom.sfgc.ac.in/online-journal Email: [email protected] / [email protected] Peer reviewed Open Access National Journal, Bengaluru, India Leveraging Small Finance Banks in Achieving Financial Inclusion in India Author Co-Author Kittu R S Dr. Smt. Mahananda B Chittawadagi Research Scholar Associate Professor and Research Guide Department of Commerce Department of Commerce KLE Society’s S. Nijalingappa College KLE Society’s S. Nijalingappa College Rajaji Nagar, Bangalore- 560010. Rajaji Nagar, Bangalore- 560010. Email: [email protected] Email: [email protected] Mobile: 9844336694 Mobile: 9980129807 Abstract With the yielding of licenses to 11 payments banks and 10 small banks in September, 2015 the Indian banking sector has seen a key evolution in reaching out to a different clientele and model of delivery which was not previously covered by the scheduled commercial banks. The objective of the change is to improve financial inclusion in the country. This paper discusses the essential of financial inclusion of a great priority sector in India that is left unbanked or informally-banked. It discusses the RBI policy to advance financial inclusion and the recent licensing of Small Finance Banks in order to achieve so. Small finance banks start with great assure of catering to rural and urban poor and the unbanked segment of population but they also expression huge challenges in terms of building the required capacity, infrastructure to service a wide variety of clients and also to train its existing manpower to reorient themselves for offering a more full-fledged service than a typical MFI. -

September 3, 2021 Sub: Intimation of Schedule of Analyst/Investor Meets

September 3, 2021 BSE Limited National Stock Exchange of India Limited, 1st Floor, Phiroze Jeejeebhoy Towers, 'Exchange Plaza', C-1 Block G, Dalal Street, Bandra Kurla Complex, Bandra (E) Mumbai – 400001 Mumbai – 400051 Scrip Code: 540065 Scrip Symbol: RBLBANK Sub: Intimation of schedule of Analyst/Investor Meets/Calls pursuant to SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 Dear Sir/Madam, Pursuant to the Regulation 30(6) of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“the Regulations”) read with Part A of Schedule III to the Regulations, please find below the particulars of Analyst/Investor meets/calls held on September 2, 2021 and September 3, 2021; Sr. Name Meeting type Venue Date of Meeting No. 1. Ageas Federal Life Insurance Co Telephonic Mumbai September 2, 2021 Airavat Capital (Group call) Ambit Capital Apah Capital Ashika India Alpha Scheme Ashmore Investment Management India LLP Awriga Capital Advisors Llp Axis Asset Management Company Limited Bajaj Holdings and Investment Ltd BCP advisors Bouyant Capital Capital Small Finance Bank Limited CTBC Bank Co., Ltd. Dalton Investments Deepfin Financial Consultants Pvt Ltd Digit Insurance DSP Investment Managers Edelweiss Asset Management Ltd Emkay Investment Managers Ltd Flowering Tree Investment Management Pte Ltd Gaja Capital Advisors Limited Goldman Sachs Asset Management Green Lantern Capital LLP India First Life Insurance Co Incred Asset Management Company INDGROWTH CAPITAL India Avenue Investment Management Infina finance pvt ltd www.rblbank.com RBL Bank Limited Controlling Office: One World Center, Tower 2B, 6th Floor, 841 Senapati Bapat Marg, Lower Parel, Mumbai - 400 013, Maharashtra, India I Tel:+91 22 43020600 I Fax: 91 22 43020520 Registered Office: 1st Lane, Shahupuri, Kolhapur - 416001, India I Tel.: +91 231 6650214 I Fax: +91 231 2657386 CIN: L65191PN1943PLC007308 . -

Banking Annual DATABASE

bank-datatable-2021-revised.qxd 29/01/2021 07:00 PM Page 2 Banking Annual DATABASE (In ~ crore) FY 2019 FY 2020 % chg (In ~ crore) FY 2019 FY 2020 % chg PRIVATE BANKS FOREIGN BANKS City Union Bank 32,673 33,927 3.8 J P Morgan Chase 13,800 14,683 6.4 CSB Bank 10,615 11,366 7.1 Societe Generale 1,495 1,574 5.3 DCB Bank 23,568 25,345 7.5 Standard Chartered Bank 66,838 76,214 14.0 Dhanlaxmi Bank 6,289 6,496 3.3 Sumitomo Mitsui 6,920 10,920 57.8 Federal Bank 1,10,223 122,268 10.9 HDFC Bank 8,19,401 993,703 21.3 ICICI Bank 5,86,647 645,290 10.0 GROWTH: DEPOSITS IDBI Bank 1,46,790 129,842 -11.5 IDFC First Bank 86,302 85,595 -0.8 PUBLIC SECTOR BANKS IndusInd Bank 1,86,394 206,783 10.9 Bank of Baroda 9,15,159 9,45,984 3.4 Jammu and Kashmir Bank 66,272 64,399 -2.8 Bank of India 5,20,862 5,55,505 6.7 Karnataka Bank 54,828 56,964 3.9 Bank of Maharashtra 1,40,650 1,50,066 6.7 Karur Vysya Bank 48,581 46,098 -5.1 Canara Bank 5,99,033 6,25,351 4.4 Kotak Mahindra Bank 2,05,695 219,748 6.8 Central Bank of India 2,99,855 3,13,763 4.6 Nainital Bank 3,516 3,829 8.9 Indian Bank 2,42,076 2,60,226 7.5 RBL Bank 54,308 58,019 6.8 Indian Overseas Bank 2,22,534 2,22,952 0.2 South Indian Bank 62,694 64,439 2.8 Punjab & Sind Bank 98,558 89,668 -9.0 Tamilnad Mercantile Bank 26,488 27,716 4.6 Punjab National Bank 6,76,030 7,03,846 4.1 Yes Bank 2,41,500 171,443 -29.0 State Bank of India 29,11,386 32,41,621 11.3 UCO Bank 1,97,907 1,93,203 -2.4 SMALL FINANCE BANKS Union Bank of India 4,15,915 4,50,668 8.4 AU Small Finance Bank 22,819 26,992 18.3 Equitas Small Finance Bank -

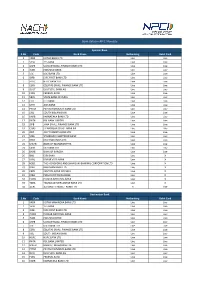

Live Banks in API E-Mandate

Bank status in API E-Mandate Sponsor Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK BANK LTD Live Live 2YESB YES BANK Live Live 3 USFB UJJIVAN SMALL FINANCE BANK LTD Live Live 4 INDB INDUSIND BANK Live Live 5 ICIC ICICI BANK LTD Live Live 6 IDFB IDFC FIRST BANK LTD Live Live 7 HDFC HDFC BANK LTD Live Live 8 ESFB EQUITAS SMALL FINANCE BANK LTD Live Live 9 DEUT DEUTSCHE BANK AG Live Live 10FDRL FEDERAL BANK Live Live 11 SBIN STATE BANK OF INDIA Live Live 12CITI CITI BANK Live Live 13UTIB AXIS BANK Live Live 14 PYTM PAYTM PAYMENTS BANK LTD Live Live 15 SIBL SOUTH INDIAN BANK Live Live 16 KARB KARNATAKA BANK LTD Live Live 17 RATN RBL BANK LIMITED Live Live 18 JSFB JANA SMALL FINANCE BANK LTD Live Live 19 CHAS J P MORGAN CHASE BANK NA Live Live 20 JIOP JIO PAYMENTS BANK LTD Live Live 21 SCBL STANDARD CHARTERED BANK Live Live 22 DBSS DBS BANK INDIA LTD Live Live 23 MAHB BANK OF MAHARASHTRA Live Live 24CSBK CSB BANK LTD Live Live 25BARB BANK OF BARODA Live Live 26IBKL IDBI BANK Live X 27KVBL KARUR VYSA BANK Live X 28 HSBC THE HONGKONG AND SHANGHAI BANKING CORPORATION LTD Live X 29BDBL BANDHAN BANK LTD Live X 30 CBIN CENTRAL BANK OF INDIA Live X 31 IOBA INDIAN OVERSEAS BANK Live X 32 PUNB PUNJAB NATIONAL BANK Live X 33 TMBL TAMILNAD MERCANTILE BANK LTD Live X 34 AUBL AU SMALL FINANCE BANK LTD X Live Destination Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK MAHINDRA BANK LTD Live Live 2YESB YES BANK Live Live 3 IDFB IDFC FIRST BANK LTD Live Live 4 PUNB PUNJAB NATIONAL BANK Live Live 5 INDB INDUSIND BANK Live Live 6 USFB -

Terms and Conditions for UPI

Terms and Conditions for UPI UPI Terms and Condition for Loan Repayment This document prescribes the Terms and Conditions, which shall be applicable to all transactions initiated by the User/Customers through any UPI PSP app and for using Unified Payments Interface (UPI) services for the repayment of loan/credit facility obtained from Jana Small Finance Bank Limited (“JSFB”). The repayment may be either in partial/EMI/full repayment of loan amount outstanding. 1. Definitions • ‘Amount’ – The payment amount in question which is required to be transferred from the Payer to the Receiver via scanning the QR code generated in the website as a part of the UPI Transaction. • ‘Authorisation / Authorised Transactions – The process by which Issuing Bank approves a Transaction. • ‘Beneficiary Bank’ – Beneficiary Bank means “Jana Small Finance Bank Limited (JSFB) as the loan account will be held with JSFB. • ‘Commission’ means the commission, fees, charges or levies payable to Bank, for facilitating a Transaction. • ‘NPCI’ – The National Payments Corporation of India, a company incorporated in India under Section 25 of the Companies Act, 1956 (now Section 8 of Companies Act 2013) NPCI acts as the settlement, clearing house, regulating agency for UPI services with the core objective of consolidating and integrating the multiple payment systems with varying service levels into nation-wide uniform and standard business process for all retail payment systems. • ‘Payer’ – Customer of the Beneficiary Bank who is holding loan account with Beneficiary Bank and who intends to use the UPI services for loan repayment. • ‘Payment Service Provider’ (PSP) or “PSP App” – The entities which are allowed to issue virtual addresses to the Users and provide payment (credit / debit) services to individuals or entities and regulated by the Reserve Bank of India, in accordance with the Payments and Settlement Systems Act, 2007. -

Shivalik Small Finance Bank Launches Operations Sets Aggressive Growth

Shivalik Small Finance Bank launches operations Sets aggressive growth target to triple business to INR 6000 Crore by 2025 India’s newest Commercial and 11th Small Finance Bank launched; becomes the country’s first Urban Cooperative Bank to achieve this milestone With a razor sharp focus on small businesses, Shivalik Small Finance bank plans to grow its current loan book of INR 805 cr and deposits of INR 1,245 cr by 50% over next 12 months Backed by significant investments made in building a robust digital interface to complement its physical touch points, the new entity aims to grow the business by INR 1000 Cr and significantly expand its current base of 4.5 Lakh customers in the next 12 months With plans to become the incubator for small businesses, Shivalik Small Finance Bank offers a portfolio of customised products and services Delhi, April 26, 2021: Shivalik Small Finance Bank today launched operations after its successful tranisition from an Urban Co-Operative Bank (UCB). Shivalik Small Finance Bank is specifically focussed on providing banking services for the enterprising masses of India. As the first UCB to secure a Small Finance Bank (SFB) licence in January 2021, the launch marks a major milestone in the journey of the 23 year old entity, making it the youngest SFB in India. In its new avatar, Shivalik Small Finance Bank is poised for strong growth over the next 12 months across its loan book, deposits as well as customer base. This is made possible by a formidable legacy created on the back of early strategic acquisitions, a sound management team, a focused digital-approach and a futuristic growth vision. -

E- Mandate – Frequently Asked Questions (Faqs)

E- Mandate – Frequently Asked Questions (FAQs) 1. What is an E-Mandate? Mandate is a standing instruction to a bank to debit client’s account on a periodic basis for a periodic transactions like Systematic Investment Plans (SIPs) / Target Investment Plan (TIP). There are 2 different ways with which one can set up a mandate: (i) Offline Mandate - In this case, a physical mandate request form needs to be submitted. This process usually takes around 21 days (including the transit time). (ii) E-mandate (Online Mandate) – In this case, the entire mandate registration process happens digitally with customer’s net-banking authentication and so it is completely paperless. This is now available in ICICI direct website where one can set up a mandate in REAL time. 2. Where is this feature available on ICICIdirect.com? Mandate registration is currently available only in our new website. Path: Login into the new website > Visit Mutual Funds section > Manage Bank Account > Add Bank Account > Register a Mandate 3. Is E-mandate registration available for all banks? Currently E- Mandate feature is available for 36 major banks. Registration is done through internet banking of respective banks using net-banking credentials. For Banks like SBI & Axis you can register the mandate even with your Debit Card. As & when more banks enabled E-Mandate at their end, they will be added on ICICIdirect as well. Given below is the list of banks for which E-Mandate is enabled: Bank Name Bank Name Bank Name Andhra Bank HDFC Bank Ltd Punjab National Bank Axis Bank ICICI