Seattle Jobs Initiative Electric Vehicles Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fidelity® Total Market Index Fund

Quarterly Holdings Report for Fidelity® Total Market Index Fund May 31, 2021 STI-QTLY-0721 1.816022.116 Schedule of Investments May 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 99.3% Shares Value Shares Value COMMUNICATION SERVICES – 10.1% World Wrestling Entertainment, Inc. Class A (b) 76,178 $ 4,253,780 Diversified Telecommunication Services – 1.1% Zynga, Inc. (a) 1,573,367 17,055,298 Alaska Communication Systems Group, Inc. 95,774 $ 317,970 1,211,987,366 Anterix, Inc. (a) (b) 16,962 838,941 Interactive Media & Services – 5.6% AT&T, Inc. 11,060,871 325,521,434 Alphabet, Inc.: ATN International, Inc. 17,036 805,292 Class A (a) 466,301 1,099,001,512 Bandwidth, Inc. (a) (b) 34,033 4,025,764 Class C (a) 446,972 1,077,899,796 Cincinnati Bell, Inc. (a) 84,225 1,297,065 ANGI Homeservices, Inc. Class A (a) 120,975 1,715,426 Cogent Communications Group, Inc. (b) 66,520 5,028,912 Autoweb, Inc. (a) (b) 6,653 19,028 Consolidated Communications Holdings, Inc. (a) 110,609 1,035,300 Bumble, Inc. 77,109 3,679,641 Globalstar, Inc. (a) (b) 1,067,098 1,707,357 CarGurus, Inc. Class A (a) 136,717 3,858,154 IDT Corp. Class B (a) (b) 31,682 914,343 Cars.com, Inc. (a) 110,752 1,618,087 Iridium Communications, Inc. (a) 186,035 7,108,397 DHI Group, Inc. (a) (b) 99,689 319,005 Liberty Global PLC: Eventbrite, Inc. (a) 114,588 2,326,136 Class A (a) 196,087 5,355,136 EverQuote, Inc. -

SBA Franchise Directory Effective March 31, 2020

SBA Franchise Directory Effective March 31, 2020 SBA SBA FRANCHISE FRANCHISE IS AN SBA IDENTIFIER IDENTIFIER MEETS FTC ADDENDUM SBA ADDENDUM ‐ NEGOTIATED CODE Start CODE BRAND DEFINITION? NEEDED? Form 2462 ADDENDUM Date NOTES When the real estate where the franchise business is located will secure the SBA‐guaranteed loan, the Collateral Assignment of Lease and Lease S3606 #The Cheat Meal Headquarters by Brothers Bruno Pizza Y Y Y N 10/23/2018 Addendum may not be executed. S2860 (ART) Art Recovery Technologies Y Y Y N 04/04/2018 S0001 1‐800 Dryclean Y Y Y N 10/01/2017 S2022 1‐800 Packouts Y Y Y N 10/01/2017 S0002 1‐800 Water Damage Y Y Y N 10/01/2017 S0003 1‐800‐DRYCARPET Y Y Y N 10/01/2017 S0004 1‐800‐Flowers.com Y Y Y 10/01/2017 S0005 1‐800‐GOT‐JUNK? Y Y Y 10/01/2017 Lender/CDC must ensure they secure the appropriate lien position on all S3493 1‐800‐JUNKPRO Y Y Y N 09/10/2018 collateral in accordance with SOP 50 10. S0006 1‐800‐PACK‐RAT Y Y Y N 10/01/2017 S3651 1‐800‐PLUMBER Y Y Y N 11/06/2018 S0007 1‐800‐Radiator & A/C Y Y Y 10/01/2017 1.800.Vending Purchase Agreement N N 06/11/2019 S0008 10/MINUTE MANICURE/10 MINUTE MANICURE Y Y Y N 10/01/2017 1. When the real estate where the franchise business is located will secure the SBA‐guaranteed loan, the Addendum to Lease may not be executed. -

Discover Automobility La Discover La Auto Show

2017RECAP DISCOVER AUTOMOBILITY LA DISCOVER LA AUTO SHOW https://automobilityla.com/videos/ https://laautoshow.com/video/recap-2017-la-auto-show/ PHOTOS: KEYNOTE PRESENTATION BY CEO OF PANASONIC NORTH AMERICA (LEFT), MERCEDES-BENZ PROJECT ONE RECEPTION (RIGHT), VOLKSWAGEN I.D. BUZZ CONCEPT (COVER) ABOUTAUTOMOBILITY LA AutoMobility LA brings together the entire new mobility ecosystem. The four-day press and trade event brings automakers, tech companies, designers, developers, startups, investors, dealers, government officials and analysts together in Los Angeles each year to unveil the future of transportation before media from around the world. “The century-old L.A. Auto Show…is one of the largest, longest-running and most popular car exhibitions in the world. The 110th edition of show…draws not only thousands of car fans but also a huge contingent of industry workers and automotive and technology journalists who want a close-up look at the newest things on wheels.” LOS ANGELES TIMES 2 AUTOMOBILITY LA KICKOFF PARTY Nov. 27 3 TECHNOLOGY PAVILION AUTO-TECH EXHIBITS Nov. 28 PHOTO: HYUNDAI BLUE LINK® EXHIBIT 4 AUTOMOBILITY LA HACKATHON AUTOMOBILITY LA NETWORKING RECEPTION PRESENTED BY HONDA INNOVATIONS Nov. 27 Nov. 27 AUTOMOBILITY LA TECH TOURS SECURING MOBILITY SUMMIT PRESENTED BY SBD AUTOMOTIVE Nov. 27 Nov. 28-30 5 AUTO-TECH PRESS CONFERENCES Nov. 28 PHOTO: VULOG PRESS CONFERENCE IN THE TECHNOLOGY PAVILION 6 AUTOMOBILITY LA TEST DRIVES AUTOMOBILITY LA KEYNOTES & PANELS TOP TEN AUTOMOTIVE STARTUPS COMPETITION Nov. 28-30 Nov. 28-29 PRESENTED BY MAGNA INTERNATIONAL, INC. Nov. 28 AUTOMOBILITY LA DESIGN & DEVELOPER CHALLENGE MIDDLECOTT SKETCHBATTLE EXPERIMENT PRESENTED BY MICROSOFT PRESENTED BY BASF Nov. -

Arcimoto Inc Form 1-A/A Filed 2017-07-31

SECURITIES AND EXCHANGE COMMISSION FORM 1-A/A Offering statement under Regulation A [amend] Filing Date: 2017-07-31 SEC Accession No. 0001144204-17-039247 (HTML Version on secdatabase.com) FILER Arcimoto Inc Mailing Address Business Address 544 BLAIR BLVD 544 BLAIR BLVD CIK:1558583| IRS No.: 261449404 | State of Incorp.:OR | Fiscal Year End: 1231 EUGENE OR 97402 EUGENE OR 97402 Type: 1-A/A | Act: 33 | File No.: 024-10710 | Film No.: 17992796 541-683-6293 SIC: 3751 Motorcycles, bicycles & parts Copyright © 2017 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document PRELIMINARY OFFERING CIRCULAR DATED JULY 31, 2017 Arcimoto, Inc. 544 Blair Blvd. Eugene, OR 97402 www.arcimoto.com UP TO 4,600,000 SHARES OF COMMON STOCK SEE “SECURITIES BEING OFFERED” AT PAGE 38 Total Number of Underwriter Proceeds to Issuer Common Price Per Share Shares Being Discounts Before Expenses, Discounts Shares to Public Offered and Commissions** and Commissions** Total Minimum $6.50 * 160,000 $ 62,400 $ 1,040,000 Total Maximum $6.50 4,600,000 $ 1,794,000 $ 29,900,000 ** The company has engaged W.R. Hambrecht & Co., LLC to serve as its sole and exclusive underwriter to assist in the placement of its securities. If the underwriter identifies all the investors and the maximum amount of shares are sold, the maximum amount the company would pay the underwriter is $1,794,000. The company has also agreed to reimburse certain expenses incurred by the underwriter in connection with the offering. In addition to the commission and expense reimbursements, the company anticipates the underwriter will have the right to acquire warrants to purchase shares of the company’s common stock equal to 5.0% of the aggregate shares sold in the offering. -

Cleantech & Industrial Growth

Craig Irwin, (646) 358-1910 [email protected] Annapoorni C.S, CFA, (646) 616-2791 [email protected] Sales (800) 933-6830, Trading (800) 933-6820 COMPANY NOTE | EQUITY RESEARCH | November 01, 2018 Cleantech & Industrial Growth Arcimoto, Inc. | FUV - $3.00 - NASDAQ | Buy Initiation of Coverage Stock Data FUV: Ming the Merciless Would Love the FUV; 52-Week Low - High $2.26 - $5.48 Initiating at Buy with a $9.00 PT Shares Out. (mil) 16.02 Mkt. Cap.(mil) $48.1 Arcimoto is an emerging EV producer tapping into a unique market of short- 3-Mo. Avg. Vol. 30,370 distance commuters looking for a fun and safe option for short daily drives. The 12-Mo.Price Target $9.00 flagship FUV has a striking profile where one could easily imagine Ming the Cash (mil) $2.1 Merciless comfortable behind the wheel, and a ride experience somewhere Tot. Debt (mil) $1.7 between a safe motorcycle and a sports car. Strong pre-orders, reasonable Tot. Debt (mil): Includes capital lease obligation pricing, a 70 mile range, and fun factoring into buying decisions, all support EPS $ our view Arcimoto should see positive momentum. Yr Dec —2018E— —2019E— —2020E— ■ Initiating coverage on Arcimoto at Buy with a $9.00 target. The Curr Curr company's flagship $15k FUV is a two-seater, three wheel, all-electric 1Q (0.13)A (0.17)E - vehicle that has an enhanced safety profile from the open safety cage, and is 2Q (0.14)A (0.17)E - 3Q (0.21)E (0.17)E - technically classified by NHTSA as a motorcycle. -

Amping up Electric Vehicle Manufacturing in the PNW OPPORTUNITIES for BUSINESS, WORKFORCE, and EDUCATION

Amping Up Electric Vehicle Manufacturing in the PNW OPPORTUNITIES FOR BUSINESS, WORKFORCE, AND EDUCATION Seattle Jobs Initiative 1200 12TH AVENUE SOUTH | SEATTLE, WASHINGTON 1 Contents Contents ........................................................................................................................................................ 2 Tables ............................................................................................................................................................ 3 Figures .......................................................................................................................................................... 3 Abbreviations ................................................................................................................................................ 4 Executive Summary ...................................................................................................................................... 5 The Openings for New Business that Electric Vehicle Production Can Create ............................................ 8 Good News: The Barriers to Entry Are Lower in EV-Related Industries ................................................... 9 Who Could Enter the EV Field? The Supply Chain in More Detail ......................................................... 10 Existing and Potential Businesses in the EV-Related Industries ................................................................ 13 Identifying EV-Related Firms in Oregon and Washington ...................................................................... -

Filed Pursuant to Rule 424(B)(3) Registration No

Filed Pursuant to Rule 424(b)(3) Registration No. 333-248543 Prospectus 276,667 Shares of Common Stock and Shares of Common Stock Underlying Warrants The selling stockholder named in this prospectus may use this prospectus to offer and resell from time to time up to 276,667 shares of our common stock (the “Shares”) issued to Palladium Capital Advisors, LLC (“Palladium”) as part of Palladium’s compensation for serving as the financial advisor of DropCar, Inc. in connection with the Merger (defined herein) and which have been transferred to Palladium Holdings, LLC (“Palladium Holdings”). The issuance of the Shares to Palladium was exempt under Section 4(a) (2) of the Securities Act of 1933, as amended (the “Securities Act”). We will not receive any of the proceeds from the sale of our common stock by the selling stockholder. The selling stockholder named in this prospectus, or its donees, pledgees, transferees or other successors-in-interest, may offer or resell the Shares from time to time through public or private transactions at prevailing market prices, at prices related to prevailing market prices or at privately negotiated prices. The selling stockholder will bear all commissions and discounts, if any, attributable to the sale of Shares. We will bear all costs, expenses and fees in connection with the registration of the Shares. For additional information on the methods of sale that may be used by the selling stockholder, see “Plan of Distribution” beginning on page 19 of this prospectus. Effective as of 6:05 pm Eastern Time on May 26, 2020, we filed an amendment to our Amended and Restated Certificate of Incorporation to effect a reverse stock split of the issued and outstanding shares of our common stock, at a ratio of one share for ten shares. -

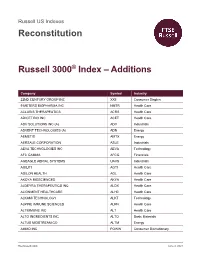

Reconstitution Russell 3000® Index – Additions

Russell US Indexes Reconstitution Russell 3000® Index – Additions Company Symbol Industry 22ND CENTURY GROUP INC XXII Consumer Staples 9 METERS BIOPHARMA INC NMTR Health Care ACLARIS THERAPEUTICS ACRS Health Care ADICET BIO INC ACET Health Care ADV SOLUTIONS INC (A) ADV Industrials ADVENT TECHNOLOGIES (A) ADN Energy AEMETIS AMTX Energy AERSALE CORPORATION ASLE Industrials AEVA TECHNOLOGIES INC AEVA Technology AFC GAMMA AFCG Financials AGEAGLE AERIAL SYSTEMS UAVS Industrials AGILITI AGTI Health Care AGILON HEALTH AGL Health Care AKOYA BIOSCIENCES AKYA Health Care ALDEYRA THERAPEUTICS INC ALDX Health Care ALIGNMENT HEALTHCARE ALHC Health Care ALKAMI TECHNOLOGY ALKT Technology ALPINE IMMUNE SCIENCES ALPN Health Care ALTIMMUNE INC ALT Health Care ALTO INGREDIENTS INC ALTO Basic Materials ALTUS MIDSTREAM CO ALTM Energy AMMO INC POWW Consumer Discretionary ftserussell.com June 4, 2021 AMPIO PHARMACEUTICALS AMPE Health Care APPHARVEST INC APPH Consumer Staples AQUABOUNTY TECHNOLOGIES AQB Consumer Staples ARBUTUS BIOPHARMA CORP ABUS Health Care ARCIMOTO FUV Consumer Discretionary ARKO CORP (A) ARKO Consumer Discretionary ASANA ASAN Technology ASENSUS SURGICAL INC ASXC Health Care ASHFORD HOSPITALITY AHT Real Estate ATERIAN INC ATER Consumer Discretionary ATLAS TECHNICAL CONS (A) ATCX Industrials ATOSSA THERAPEUTICS INC ATOS Health Care AVEANNA HEALTHCARE HOLDI AVAH Health Care AVIAT NETWORKS INC AVNW Telecommunications AVITA Medical RCEL Health Care BABCOCK & WILCOX ENT BW Industrials BARNES & NOBLE EDUCATION BNED Consumer Discretionary BASSETT -

Small-Cap Research M

August 17, 2017 Small-Cap Research M. Marin 312-265-9211 [email protected] scr.zacks.com 10 S. Riverside Plaza, Chicago, IL 60606 Arcimoto, Inc. Zacks Company Report OUTLOOK Arcimoto is a development stage company Bringing a new product to market is risky, but positioning itself to benefit from pending transitions in Arcimoto has displayed a conservative mobility with the SRK, an ultra-efficient, economical commitment to minimizing its costs during the electric vehicle under development. The SRK weighs development process. The company has delivered roughly 25% what a standard car weighs and has its latest generation SRK at what management only about 33% of the footprint. Its smaller size and believes is a fraction of the cost most other lighter weight mean it can help combat urban road manufacturers incur to get to a similar stage of congestion, maneuver into parking spaces more development. easily and is more energy efficient than most cars. The SRK’s 70 mile range per charge or up to 130 miles with a battery upgrade is more than ample for most daily driving needs. Regulation A Offering Price $6.50 SUMMARY DATA 52 -Week High N/A Risk Level High 52 -Week Low N/A Type of Stock Growth One -Year Return (%) N/A Industry Automotive Beta N/A Zacks Rank in Industry N/A Average Daily Volume (sh) N/A ZACKS ESTIMATES Shares Outstanding (mil) 10 Market Capitalization ($mil) N/A Revenue (in millions of $) Short Interest Ratio (days) N/A Q1 Q2 Q3 Q4 Year Institutional Ownership (%) N/A Insider Ownership (%) 60.8 (Mar) (Jun) (Sep) (Dec) (Dec) 2016 N/A N/A N/A N/A 0.0 A Annual Cash Dividend $0.00 2017 N/A N/A N/A N/A 0.8 E Dividend Yield (%) 0.00 2018 N/A N/A N/A N/A 29 E 2019 N/A N/A N/A N/A 120 E 5-Yr. -

Zacks Small-Cap Research M

June 14, 2018 Zacks Small-Cap Research M. Marin 312-265-9211 Sponsored Impartial - Comprehensive [email protected] scr.zacks.com 10 S. Riverside Plaza, Chicago, IL 60606 Arcimoto, Inc. (FUV-NASDAQ) FUV: Leveraging Transitions in Mobility OUTLOOK Arcimoto is positioning itself to benefit from pending transitions in mobility as governments mandate lower Bringing a new product to market is risky, but car emissions, consumers adopt green mobile Arcimoto has displayed a conservative solutions and technology companies enter the financial approach and a commitment to automotive space. Following a successful Reg A minimizing costs during the development offering, the company is developing an efficient, low- process. The company is also launching a cost, three-wheeled, two-person electric vehicle. The rentail model to drive both cash flow and Arcimoto FUV is designed to address two major vehicle sales. problems that limit the commercial appeal of most alternative vehicles: cost and range. Current Price (06/13/18) $2.73 Valuation $5.00 SUMMARY DATA 52-Week High $6.35 Risk Level High 52-Week Low $2.50 Type of Stock Small-cap One-Year Return (%) N/A Industry Automotive Beta N/A Zacks Rank in Industry N/A Average Daily Volume (sh) 29,587 ZACKS ESTIMATES Shares Outstanding (mil) 16 Market Capitalization ($mil) $44 Revenue (in millions of $) Short Interest Ratio (days) N/A Q1 Q2 Q3 Q4 Year Institutional Ownership (%) N/A Insider Ownership (%) 56 (Mar) (Jun) (Sep) (Dec) (Dec) 2017 0.0A NA NA NA 0.1A Annual Cash Dividend $0.00 2018 0.0A 0.2E 1.8E 2.6E 4.6E Dividend Yield (%) 0.00 2019* 61.4E 5-Yr. -

Membership List; Russell 2000 Index

Russell US Indexes Membership list Russell 2000® Index Company Ticker Company Ticker 1-800-FLOWERS.COM CL A FLWS AFC GAMMA AFCG 1LIFE HEALTHCARE ONEM AFFIMED N.V. AFMD 1ST SOURCE SRCE AGEAGLE AERIAL SYSTEMS UAVS 22ND CENTURY GROUP INC. XXII AGENUS AGEN 2U TWOU AGILITI AGTI 3-D SYSTEMS DDD AGILYSYS AGYS 4D MOLECULAR THERAPEUTICS FDMT AGIOS PHARMACEUTICALS AGIO 89BIO ETNB AGREE REALTY ADC 8X8 EGHT AIR TRANSPORT SERVICES GROUP ATSG 9 METERS BIOPHARMA INC NMTR AKEBIA THERAPEUTICS AKBA 908 DEVICES MASS AKERO THERAPEUTICS AKRO A10 NETWORKS ATEN AKOUOS AKUS AAON INC AAON AKOUSTIS TECHNOLOGIES INC AKTS AAR CORP AIR AKOYA BIOSCIENCES AKYA ABERCROMBIE & FITCH A ANF ALAMO GROUP ALG ABM INDUSTRIES INC ABM ALARM.COM HOLDINGS ALRM ACACIA RESEARCH - ACACIA TECHNOLOGIES ACTG ALBANY INTERNATIONAL A AIN ACADEMY SPORTS AND OUTDOORS ASO ALBIREO PHARMA ALBO ACADIA PHARMACEUTICALS ACAD ALDEYRA THERAPEUTICS ALDX ACADIA REALTY AKR ALECTOR ALEC ACCEL ENTERTAINMENT (A) ACEL ALERUS FINANCIAL CORP. ALRS ACCELERATE DIAGNOSTICS AXDX ALEXANDER & BALDWIN INC. ALEX ACCO BRANDS ACCO ALEXANDERS INC ALX ACCOLADE ACCD ALIGNMENT HEALTHCARE ALHC ACCRETIVE HEALTH RCM ALIGOS THERAPEUTICS ALGS ACCURAY ARAY ALKAMI TECHNOLOGY ALKT ACI WORLDWIDE ACIW ALKERMES PLC ALKS ACLARIS THERAPEUTICS ACRS ALLAKOS ALLK ACUSHNET HOLDINGS GOLF ALLEGHENY TECHNOLOGIES ATI ACUTUS MEDICAL AFIB ALLEGIANCE BANCSHARES ABTX ADAPTHEALTH AHCO ALLEGIANT TRAVEL ALGT ADDUS HOMECARE ADUS ALLETE ALE ADICET BIO INC ACET ALLIED MOTION TECHNOLOGIES AMOT ADIENT PLC ADNT ALLOGENE THERAPEUTICS ALLO ADTALEM GLOBAL EDUCATION -

Profunds Semiannual Report

Toppan Merrill - ProFunds Funds VP Main Semi-Annual Report [Funds] 06-30-2021 ED [AUX] | bliteck | 24-Aug-21 00:06 | 21-1908-3.aa | Sequence: 1 CHKSUM Content: 54117 Layout: 6120 Graphics: 61486 CLEAN Semiannual Report JUNE 30, 2021 ProFunds VP Access VP High Yield Short Small-Cap Asia 30 Small-Cap Banks Small-Cap Growth Basic Materials Small-Cap Value Bear Technology Biotechnology Telecommunications Bull UltraBull Consumer Goods UltraMid-Cap Consumer Services UltraNasdaq-100 Dow 30 UltraShort Dow 30 Emerging Markets UltraShort Nasdaq-100 Europe 30 UltraSmall-Cap Falling U.S. Dollar U.S. Government Plus Financials Utilities Government Money Market Health Care Industrials International Internet Japan Large-Cap Growth Large-Cap Value Mid-Cap Mid-Cap Growth Mid-Cap Value Nasdaq-100 Oil & Gas Pharmaceuticals Precious Metals Real Estate Rising Rates Opportunity Semiconductor Short Dow 30 Short Emerging Markets Short International Short Mid-Cap Short Nasdaq-100 JOB: 21-1908-3 CYCLE#;BL#: 7; 0 TRIM: 8.25" x 10.75" AS: New York: 212-620-5600 COLORS: ~note-color 2, Black GRAPHICS: ProFunds_CVR_logo_k.eps, ProFunds_FC_art_k.eps V1.5 Toppan Merrill - ProFunds Funds VP Main Semi-Annual Report [Funds] 06-30-2021 ED [AUX] | bliteck | 24-Aug-21 00:06 | 21-1908-3.ac | Sequence: 1 CHKSUM Content: 53432 Layout: 22726 Graphics: 0 CLEAN Table of Contents 1 Message from the Chairman 188 ProFund VP Short Emerging Markets 3 Financial Statements and 192 ProFund VP Short International Financial Highlights 196 ProFund VP Short Mid-Cap 4 ProFund Access VP High Yield