Euronav NV and the Entities Included in the Consolidation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TEACHERS' RETIREMENT SYSTEM of the STATE of ILLINOIS 2815 West Washington Street I P.O

Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Performed as Special Assistant Auditors for the Auditor General, State of Illinois Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Table of Contents Schedule Page(s) System Officials 1 Management Assertion Letter 2 Compliance Report Summary 3 Independent Accountant’s Report on State Compliance, on Internal Control over Compliance, and on Supplementary Information for State Compliance Purposes 4 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 8 Schedule of Findings Current Findings – State Compliance 10 Supplementary Information for State Compliance Purposes Fiscal Schedules and Analysis Schedule of Appropriations, Expenditures and Lapsed Balances 1 13 Comparative Schedules of Net Appropriations, Expenditures and Lapsed Balances 2 15 Comparative Schedule of Revenues and Expenses 3 17 Schedule of Administrative Expenses 4 18 Schedule of Changes in Property and Equipment 5 19 Schedule of Investment Portfolio 6 20 Schedule of Investment Manager and Custodian Fees 7 21 Analysis of Operations (Unaudited) Analysis of Operations (Functions and Planning) 30 Progress in Funding the System 34 Analysis of Significant Variations in Revenues and Expenses 36 Analysis of Significant Variations in Administrative Expenses 37 Analysis -

2021 Annual General Meeting and Proxy Statement 2020 Annual Report

2020 Annual Report and Proxyand Statement 2021 Annual General Meeting Meeting General Annual 2021 Transocean Ltd. • 2021 ANNUAL GENERAL MEETING AND PROXY STATEMENT • 2020 ANNUAL REPORT CONTENTS LETTER TO SHAREHOLDERS NOTICE OF 2021 ANNUAL GENERAL MEETING AND PROXY STATEMENT COMPENSATION REPORT 2020 ANNUAL REPORT TO SHAREHOLDERS ABOUT TRANSOCEAN LTD. Transocean is a leading international provider of offshore contract drilling services for oil and gas wells. The company specializes in technically demanding sectors of the global offshore drilling business with a particular focus on ultra-deepwater and harsh environment drilling services, and operates one of the most versatile offshore drilling fleets in the world. Transocean owns or has partial ownership interests in, and operates a fleet of 37 mobile offshore drilling units consisting of 27 ultra-deepwater floaters and 10 harsh environment floaters. In addition, Transocean is constructing two ultra-deepwater drillships. Our shares are traded on the New York Stock Exchange under the symbol RIG. OUR GLOBAL MARKET PRESENCE Ultra-Deepwater 27 Harsh Environment 10 The symbols in the map above represent the company’s global market presence as of the February 12, 2021 Fleet Status Report. ABOUT THE COVER The front cover features two of our crewmembers onboard the Deepwater Conqueror in the Gulf of Mexico and was taken prior to the COVID-19 pandemic. During the pandemic, our priorities remain keeping our employees, customers, contractors and their families healthy and safe, and delivering incident-free operations to our customers worldwide. FORWARD-LOOKING STATEMENTS Any statements included in this Proxy Statement and 2020 Annual Report that are not historical facts, including, without limitation, statements regarding future market trends and results of operations are forward-looking statements within the meaning of applicable securities law. -

To Arrive at the Total Scores, Each Company Is Marked out of 10 Across

BRITAIN’S MOST ADMIRED COMPANIES THE RESULTS 17th last year as it continues to do well in the growing LNG business, especially in Australia and Brazil. Veteran chief executive Frank Chapman is due to step down in the new year, and in October a row about overstated reserves hit the share price. Some pundits To arrive at the total scores, each company is reckon BG could become a take over target as a result. The biggest climber in the top 10 this year is marked out of 10 across nine criteria, such as quality Petrofac, up to fifth from 68th last year. The oilfield of management, value as a long-term investment, services group may not be as well known as some, but it is doing great business all the same. Its boss, Syrian- financial soundness and capacity to innovate. Here born Ayman Asfari, is one of the growing band of are the top 10 firms by these individual measures wealthy foreign entrepreneurs who choose to make London their operating base and home, to the benefit of both the Exchequer and the employment figures. In fourth place is Rolls-Royce, one of BMAC’s most Financial value as a long-term community and environmental soundness investment responsibility consistent high performers. Hardly a year goes past that it does not feature in the upper reaches of our table, 1= Rightmove 9.00 1 Diageo 8.61 1 Co-operative Bank 8.00 and it has topped its sector – aero and defence engi- 1= Rotork 9.00 2 Berkeley Group 8.40 2 BASF (UK & Ireland) 7.61 neering – for a decade. -

Filing Port Code Filing Port Name Manifest Number Filing Date Next

Filing Port Call Sign Next Foreign Trade Official Vessel Type Total Dock Code Filing Port Name Manifest Number Filing Date Next Domestic Port Vessel Name Next Foreign Port Name Number IMO Number Country Code Number Agent Name Vessel Flag Code Operator Name Crew Owner Name Draft Tonnage Dock Name InTrans 5204 WEST PALM BEACH, FL 5204-2021-00375 1/14/2021 - TROPIC MIST FREEPORT, GRAND BAHAMA I J8NZ 8204183 BS 3 400204 TROPICAL SHIPPING CO. VC 333 TROPICAL SHIPPING AND CONSTRUCTION COMPANY LTD. 14 TROPICAL SHIPPING AND CONSTRUCTION 15'0" 548 PORT OF PALM BEACH BERTHS NOS. 8 & 9 (2012) DLX 1803 JACKSONVILLE, FL 1803-2021-00350 1/14/2021 - SLNC MAGOTHY (EX. NORFLOK) GUANTANAMO BAY WDI3067 9418975 CU 3 1262669 CB AGENCIES US 310 ARGENT MARINE OPERATIONS, INC. 17 HS MAGOTHY LLC 27'0" 6089 BLOUNT ISLAND - BERTHS 4 - 6 LY 4601 NEW YORK/NEWARK AREA 4601-2021-01122 1/14/2021 BALTIMORE, MD MAERSK VILNIUS - 9V8503 9408956 - 6 395877 NORTON LILLY INTERNATIONAL SG 310 A.P. MOLLER MAERSK A/S 22 A.P. MOLLER SINGAPORE PTE, LTD 28'3" 8602 PORT NEWARK CONTAINER TERM (PNCT) BERTHS 53, 55, 57, 59 DFL 5301 HOUSTON, TX 5301-2021-01995 1/14/2021 - CHEMSTAR TIERRA ARATU 3EXM9 9827451 BR 2 49547-18 GENERAL STEAMSHIP INC. PA 112 IINO MARINE SERVICE CO., LTD. 24 SIETEMAR, S.A. 34'0" 6474 KINDER MORGAN GALENA PARK L 4601 NEW YORK/NEWARK AREA 4601-2021-01121 1/14/2021 NORFOLK, VA MELCHIOR SCHULTE - 9V3053 9676723 - 6 399740 Turkon America SG 310 BEACH ROAD PARK SHIPPING CO. -

A New Inquiry by the Science & Innovation Committee

Committee Secretary Standing Committee on Science and Innovation House of Representatives Parliament House CANBERRA ACT 2600 Email [email protected] Dear Committee-members, I am pleased to provide the response of the Australian Geoscience Council to the Inquiry by the House of Representatives Standing Committee on Science and Innovation into Australian technological innovation and pathways to commercialisation. The Australian Geoscience Council is the Peak Council of geoscientists in Australia. It represents nine major Australian geoscientific societies and has a membership of over 7000 professionals. We believe that the geosciences are critical for Australia, as shown by the accompanying sample of innovative technology case studies in the geosciences. Our submission is made in four parts: • This cover letter and a one page Executive Summary containing the Geoscience Council’s eight recommendations, • Eleven pages responding to the eight Terms of Reference for the Inquiry and developing the rationale behind the Geoscience Council’s recommendations, • Twenty one appendices (pages 14 to 46), each providing a summary case study of technological innovation in the geosciences, • Appendix 22 (page 47) which describes a relevant activity from another country. The resource industry in Australia is characterised by sustained innovation, and the sector continues to create new wealth for Australia with long lead times. Resources (including gold) achieved more of Australia’s export earnings in 2004 than any other sector, while also delivering employment and other flow-on benefits to the community in both urban and remote regions. However, these achievements derive from successful exploration of decades past. In order to project past performance into the future, Australia needs greater innovation in technologies, concepts and knowledge, as well as sustained levels of qualified people. -

OF the SECURITIES EXCHANGE ACT of 1934 (Amendment No

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 SCHEDULE 14A INFORMATION PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE SECURITIES EXCHANGE ACT OF 1934 (Amendment No. ) Filed by the Registrant Filed by a Party other than the Registrant ¨ Check the appropriate box: ¨ Preliminary Proxy Statement ¨ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) Definitive Proxy Statement ¨ Definitive Additional Materials ¨ Soliciting Material under §240.14a-12 Schlumberger N.V. (Schlumberger Limited) (Name of Registrant as Specified in Its Charter) Name of Person(s) Filing Proxy Statement if other than the Registrant) Payment of Filing Fee (Check the appropriate box): No fee required. ¨ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ¨ Fee paid previously with preliminary materials. ¨ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. (1) -

Technical Programme

DAY ONE TUESDAY 23 NOVEMBER 2021 TECHNICAL PROGRAMME 08:30 - 09:30 Conference, Exhibition and Registration Open 09:30 - 10:00 Keynote Address: Phil Kirk | Harbour Energy AUDITORIUM 10:00 - 10:30 Keynote Address: TotalEnergies Exploration for the Future | Emmanuelle Garinet, TotalEnergies 10:30 - 11:15 | Refreshment Break & Exploring the Exhibition Exploration: UK Multi-azimuth seismic Machine Learning / Digital A Pressure Cell Summary of the Highly Multi-azimuth Acquisition and High- Mining Data at Scale Using Deep Prospective Central North Sea HPHT resolution Model Building and Imaging Learning 11:15 - 11:45 Domain from Shallow to Deep Reservoir - A Case Chin Hang Lun, CGG Eva Zimmer, Oil & Gas Authority Study from Offshore Morocco Andrew Furber, WesternGeco Revealing the Zechstein Potential of the Improved Imaging Of The Marte Leveraging Supervised Machine Mid North Sea High, UK Reservoir With A Multi Azimuth Q-FWI Learning for Rapid Lithology Prediction 11:45 - 12:15 Neil Hurst, ION Model Rebecca Head, Halliburton John Northall, BP HALL 1 HALL 2 HALL 3 Characterising Basement and Calibrating A Novel and Efficient Multi-azimuth Petrographic Thin Section Analysis with Thermal History to Further the Towed-streamer Solution to Address Machine Learning Understanding of Petroleum Systems in Complex Illumination Challenges, Edward Jarvis, CGG 12:15 - 12:45 the Faroe-Shetland Basin Established in the Viking Graben, North Julian Moore, Applied Petroleum Sea Technology Julien Oukili, PGS 12:45 - 13:45 | Lunch & Exploring the Exhibition Exploration: -

Design Innovation Unrivaled Experience Proven

ChartLNGIcover-9-15-OP.pdf 1 9/9/2015 3:32:28 PM LN G INDUSTRY | October 2015 October 2015 C M Y CM MY CY CMY K DESIGN INNOVATION UNRIVALED EXPERIENCE www. PROVEN PERFORMANCE lngindustry .com ENERGY for life “The light and energy of Seoul ignites great ideas.” Mina Cheon - Artist Energy powers our world, it enriches our lives. Korean artist Mina Cheon uses energy as an inspiration for her art. It fuels her imagination. RasGas provides clean, reliable energy for Qatar and the world. Energy for Life. South Korea RG_KoreaA3E-Adi.indd 2 9/15/15 12:12 PM ENERGY for life “The light and energy of Seoul ignites great ideas.” Mina Cheon - Artist Energy powers our world, it enriches our lives. Korean artist Mina Cheon uses energy as an inspiration for her art. It fuels her imagination. RasGas provides clean, reliable energy for Qatar and the world. Energy for Life. South Korea RG_KoreaA3E-Adi.indd 2 9/15/15 12:12 PM Modular, scalable, cleaner energy. Fueling the future of natural gas. A skid-mounted, plug-n-play natural gas liquefaction plant that provides a cleaner more abundant LNG fuel source for remote locations. GE’s small scale LNG plants mean faster commissioning times and reduced installation costs. Imagination at work. www.geoilandgas.com/smallscalelng ISSN 1747-1826 CONTENTS2015 OCTOBER 05 Comment 81 A helpful tool 07 LNG news Bjarte Lund, Kyma a.s, Norway, introduces a software module to help optimise the efficiency on DFDE LNG carriers. 14 Looking for growth 87 Working together Mike Johnston, T.A. -

Review of Maritime Transport 2020 37

2 The present chapter focuses on key developments related to the supply of maritime transport during this past year. It also assesses the early impact of the COVID-19 pandemic on the supply of maritime transport services and industries and discusses the responses, lessons learned and possible implications of the pandemic in terms of forces shaping supply and the industry’s long-term goal of decarbonization. The pandemic has had a significant impact on the shipping industry. On the one hand, lockdowns and factory closures gradually affected demand for maritime transport, due to reduced cargo volumes (see chapter 1). On the other hand, safety measures applied to contain the spread of the virus, such as lockdowns and travel restrictions, affected the movement of maritime transport workers and procedural changes introduced in ports, and induced operational disruptions in the supply of maritime transport. These prompted changes in shipping operations and requests for government support in the sector. They made the industry reflect on ways to enhance resilience of the sector to future shocks. This chapter reviews world fleet developments such as MARITIME annual fleet growth, changes to the structure and age of the fleet. It considers selected segments of the maritime TRANSPORT supply chain, such as shipbuilding, ship recycling, ship ownership, ship registration and the maritime workforce, SERVICES AND emphasizing the impacts of the pandemic on maritime INFRASTRUCTURE transport and marine manufacturing industries and on the supply of shipping services. SUPPLY It also examines the impact of the pandemic on the container, dry bulk and tanker freight markets; government responses to support shipping; and industry prospects, in particular with regard to accelerated digitalization and the prioritization of environmental sustainability. -

TERMS and CONDITIONS DATED 2010-05-01 Revised December 2014 (§39)

PREEM AB 1 PREEM AB CHARTERPARTY TERMS AND CONDITIONS DATED 2010-05-01 Revised December 2014 (§39) SECTION 1 1. Basic Provisions 2. Worldscale and Overage 3. Misrepresentation 4. I T F Clause 5. Safe Port/Berth 6. Deviation 7. Agency 8. Expected to Arrive 9. Notice of Readiness 10. Time Bar 11. Statement of Facts 12. Calculation of laytime 13. Weather and seagoing clause 14. Retention 15. Letter of Indemnity and Invocation of Short Form Undertaking 16. Port Authority's Instruction 17. Competent Crew 18. Crew's Duties 19. Bunkers Onboard 20. Charterers Inspection 21. Cleaning 22. Cargo Temperature at Loading/Heating 23. Pumping 24. Closed Loading 25. Insurance 26. Vessel Certification 27. Remaining on Board 28. Pollution Clause 29. P&I Insurance 30. Drug and Alcohol Clause 31. ITOPF Clause 32. Small Claims Arbitration 33. Address Commission 34. Logbooks 35. Vessel Vetting Clause 36. Early Loading Clause 37. ISPS Clause, International Ship & Port Facility Safety Code 38. Charterers Mail 39. Accidents to Vessel and / or Cargo 40. Document of Compliance / ISM Clause, International Safety Management Code 41. Administration Clause PREEM AB 2 SECTION 2 A. Crude Oil Washing B. Inert Gas C. Speed Clause D. Lightering Execution Clause E. Tank Stripping F. Lightering Stability G. Arab Clause H. Early Departure Clause I. Hydrogen Sulphide Clause SECTION 1 1 The clauses hereinafter are, to the extent they are not added to, deleted or otherwise 2 changed by mutual consent, deemed incorporated into the ASBATANKVOY 3 Charterparty part 1 section M or otherwise, as appropriate, deemed incorporated into 4 such other Charterparty form the parties have agreed shall govern the charter. -

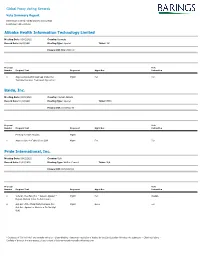

Global Proxy Voting Records

Global Proxy Voting Records Vote Summary Report Date range covered: 03/01/2021 to 03/31/2021 Location(s): All Locations Alibaba Health Information Technology Limited Meeting Date: 03/01/2021 Country: Bermuda Record Date: 02/23/2021 Meeting Type: Special Ticker: 241 Primary ISIN: BMG0171K1018 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction 1 Approve Revised Annual Cap Under the Mgmt For For Technical Services Framework Agreement Baidu, Inc. Meeting Date: 03/01/2021 Country: Cayman Islands Record Date: 01/28/2021 Meeting Type: Special Ticker: BIDU Primary ISIN: US0567521085 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction Meeting for ADR Holders Mgmt 1 Approve One-to-Eighty Stock Split Mgmt For For Pride International, Inc. Meeting Date: 03/01/2021 Country: USA Record Date: 12/01/2020 Meeting Type: Written Consent Ticker: N/A Primary ISIN: US74153QAJ13 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction 1 Vote On The Plan (For = Accept, Against = Mgmt For Abstain Reject; Abstain Votes Do Not Count) 2 Opt Out of the Third-Party Releases (For = Mgmt None For Opt Out, Against or Abstain = Do Not Opt Out) * Instances of "Do Not Vote" are normally owing to: - Share-blocking - temporary restriction of trading by the Sub-Custodian following vote submission - Client restrictions - Conflicts of Interest. For any queries, please contact [email protected] Global Proxy Voting Records Vote Summary Report Date range covered: 03/01/2021 to 03/31/2021 Location(s): All Locations The -

BG Group's LNG Business

FACT SHEET – LIQUEFIED NATURAL GAS BG Group’s LNG business BG Group’s LNG activities are founded on a deep understanding of our target markets and customers, along with a unique combination of infrastructure, flexible supply, shipping capacity and marketing capabilities. We have a strong presence in all segments of the chain, from upstream exploration and production, through liquefaction, shipping and regasification, to the end market. In liquefaction, we have a track record of execution, having been materially involved in the delivery of six liquefaction trains at projects in Trinidad and Tobago and Egypt. In shipping, we have one of the largest LNG fleets of any international oil and gas company consisting of (as of March 2012) around 25 owned or chartered modern vessels that are able to meet BG Group LNG sales terminal equity and/or capacity BG Group LNG sales terminal short/medium term BG Group LNG long term contracted sources BG Group LNG short term sources the needs of a rapidly changing market. In regasification, we have supply rights or terminal capacity in the UK, the US and Singapore, valuable entry points for agreement for LNG exports from the LNG supply position by around 50% LNG into these markets, as well as long- US, with a purchase of 5.5 mtpa from above current levels over the next three term sales to customers in Chile, Japan the Sabine Pass LNG terminal being years, targeting 20 million tonnes per and China. developed by Cheniere Energy Partners, annum (mtpa) by 2015. In light of our L.P., and are progressing plans for export progress at QCLNG, together with the The Group has developed an industry from the Lake Charles facility, where we growth potential inherent within the leading portfolio of flexible long-term hold 100% of the import capacity.