Proposed Regulations, Property by Air; Aircraft Management Michael H

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

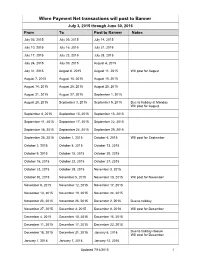

Transactions Posted to Pathway

When Payment Net transactions will post to Banner July 3, 2015 through June 30, 2016 From To Post to Banner Notes July 03, 2015 July 09, 2015 July 14, 2015 July 10, 2015 July 16, 2015 July 21, 2015 July 17, 2015 July 23, 2015 July 28, 2015 July 24, 2015 July 30, 2015 August 4, 2015 July 31, 2015 August 6, 2015 August 11, 2015 Will post for August August 7, 2015 August 13, 2015 August 18, 2015 August 14, 2015 August 20, 2015 August 25, 2015 August 21, 2015 August 27, 2015 September 1, 2015 August 28, 2015 September 3, 2015 September 9, 2015 Due to holiday at Monday Will post for August September 4, 2015 September 10, 2015 September 15, 2015 September 11, 2015 September 17, 2015 September 22, 2015 September 18, 2015 September 24, 2015 September 29, 2015 September 25, 2015 October 1, 2015 October 6, 2015 Will post for September October 2, 2015 October 8, 2015 October 13, 2015 October 9, 2015 October 15, 2015 October 20, 2015 October 16, 2015 October 22, 2015 October 27, 2015 October 23, 2015 October 29, 2015 November 3, 2015 October 30, 2015 November 5, 2015 November 10, 2015 Will post for November November 6, 2015 November 12, 2015 November 17, 2015 November 13, 2015 November 19, 2015 November 24, 2015 November 20, 2015 November 26, 2015 December 2, 2015 Due to holiday November 27, 2015 December 3, 2015 December 8, 2018 Will post for December December 4, 2015 December 10, 2015 December 15, 2015 December 11, 2015 December 17, 2015 December 22, 2015 December 18, 2015 December 31, 2015 January 6, 2016 Due to holiday closure Will post for December -

2021 Calandar

Harbortown Point Marina Resort & Club 2021 Reservation Calendar Written request can be taken at dates indicated Please note: you can only book in Prime season if you own in Prime Season and only below. The dates inform book in High Season if you own in High Season you when the 2021 weeks to the left Friday Saturday Sunday become abailable to Week No. Dates Dates Dates reserve. 1 Jan 1 - Jan 8 Jan 2 - Jan 9 Jan 3 - Jan 10 October 22, 2019 2 Jan 8 - Jan 15 Jan 9 - Jan 16 Jan 10 - Jan 17 October 29, 2019 3 Jan 15 - Jan 22 Jan 16 - Jan 23 Jan 17 - Jan 24 November 5, 2019 4 Jan 22 - Jan 29 Jan 23 - Jan 30 Jan 24 - Jan 31 November 12, 2019 5 Jan 29 - Feb 5 Jan 30 - Feb 6 Jan 31 - Feb 7 November 19, 2019 6 Feb 5 - Feb 12 Feb 6- Feb 13 Feb 7 - Feb 14 November 26, 2019 7 Feb 12 - Feb 19 Feb 13 - Feb 20 Feb 14 - Feb 21 December 3, 2019 8 Feb 19 - Feb 26 Feb 20 - Feb 27 Feb 21 - Feb 28 December 10, 2019 9 Feb 26 - Mar 5 Feb 27 - Mar 6 Feb 28 - Mar 7 December 18, 2018 HIGH 10 Mar 5 - Mar 12 Mar 6 - Mar 13 Mar 7 - Mar 14 December 17, 2019 11 Mar 12 - Mar 19 Mar 13 - Mar 20 Mar 14 - Mar21 December 24, 2019 12 Mar 19 - Mar 26 Mar 20 - Mar 27 Mar 21 - Mar 28 December 31, 2019 13 Mar 26 - Apr 2 Mar 27 - Apr 3 Mar 28 - Apr 4 January 7, 2020 14 April 2 - April 9 April 3 - April 10 April 4 - April 11 January 14, 2020 15 April 9 - April 16 Apr 10 - Apr 17 Apr 11 - Apr 18 January 21, 2020 16 April 16 - April 23 Apr 17 - Apr 24 Apr 18 - Apr 25 January 28, 2020 17 April 23 - April 30 Apr 24 - May 1 Apr 25 - May 2 February 4, 2020 18 Apr 30 - May 7 May 1 - May -

2021 7 Day Working Days Calendar

2021 7 Day Working Days Calendar The Working Day Calendar is used to compute the estimated completion date of a contract. To use the calendar, find the start date of the contract, add the working days to the number of the calendar date (a number from 1 to 1000), and subtract 1, find that calculated number in the calendar and that will be the completion date of the contract Date Number of the Calendar Date Friday, January 1, 2021 133 Saturday, January 2, 2021 134 Sunday, January 3, 2021 135 Monday, January 4, 2021 136 Tuesday, January 5, 2021 137 Wednesday, January 6, 2021 138 Thursday, January 7, 2021 139 Friday, January 8, 2021 140 Saturday, January 9, 2021 141 Sunday, January 10, 2021 142 Monday, January 11, 2021 143 Tuesday, January 12, 2021 144 Wednesday, January 13, 2021 145 Thursday, January 14, 2021 146 Friday, January 15, 2021 147 Saturday, January 16, 2021 148 Sunday, January 17, 2021 149 Monday, January 18, 2021 150 Tuesday, January 19, 2021 151 Wednesday, January 20, 2021 152 Thursday, January 21, 2021 153 Friday, January 22, 2021 154 Saturday, January 23, 2021 155 Sunday, January 24, 2021 156 Monday, January 25, 2021 157 Tuesday, January 26, 2021 158 Wednesday, January 27, 2021 159 Thursday, January 28, 2021 160 Friday, January 29, 2021 161 Saturday, January 30, 2021 162 Sunday, January 31, 2021 163 Monday, February 1, 2021 164 Tuesday, February 2, 2021 165 Wednesday, February 3, 2021 166 Thursday, February 4, 2021 167 Date Number of the Calendar Date Friday, February 5, 2021 168 Saturday, February 6, 2021 169 Sunday, February -

COVID-19 Dashboard - Friday, July 31, 2020 Dashboard of Public Health Indicators

7/31/2020 Duplicate of Public Health Indicators Massachusetts Department of Public Health COVID-19 Dashboard - Friday, July 31, 2020 Dashboard of Public Health Indicators Newly Reported Total Confirmed Newly Reported Total Deaths Confirmed Cases Cases Deaths among among Confirmed Today* Confirmed Today Cases 387 109,787 14 8,389 New Individuals Total Individuals Below is the status as of June 5, 2020: Tested by Tested by Molecular Tests Molecular Tests Measure Status 19,151 1,180,605 COVID-19 positive test rate ⚫ Number of individuals who died from COVID-19 ⚫ Total Molecular Legend Number of patients with COVID-19 in hospitals ⚫ Tests Healthcare system readiness ⚫ Administered Testing capacity ⚫ 1,535,835 Contact tracing capabilities ⚫ *PLEASE NOTE: Delays in the reporting of test results to DPH from multiple laboratories, including large national commercial laboratories, are reflected in today’s case counts. However, these positive test results have been assigned retrospectively to the appropriate date of test. The front page of the dashboard has been reformatted. Probable case and death information can be found on page 21. Antibody tests (individual and total numbers) can be found on page 7. For more information on the COVID-19 case 1 definition, see https://cdn.ymaws.com/www.cste.org/resource/resmgr/2020ps/Interim-20-ID-01_COVID-19.pdf 1/1 7/31/2020 Public Health Indicators2 Massachusetts Department of Public Health COVID-19 Dashboard - Friday, July 31, 2020 Percent Change Since Dashboard of Public Health Indicators April 15th 7 Day -

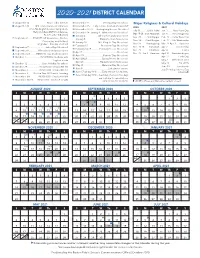

2020–2021District Calendar

2020–2021 DISTRICT CALENDAR August 10-14 ...........................New Leader Institute November 11 .................... Veterans Day: No school Major Religious & Cultural Holidays August 17-20 ........ BPS Learns Summer Conference November 25 ..... Early release for students and staff 2020 2021 (TSI, ALI, English Learner Symposium, November 26-27 ....Thanksgiving Recess: No school July 31 ..........Eid al-Adha Jan. 1 ........New Year’s Day Early Childhood/UPK Conference, December 24- January 1 ..Winter Recess: No school Sep. 19-20 ..Rosh Hashanah Jan. 6 ......Three Kings Day New Teacher Induction) January 4.................... All teachers and paras report . Sep. 28 .........Yom Kippur Feb. 12 .... Lunar New Year September 1 ......REMOTE: UP Academies: Boston, January 5...................... Students return from recess Nov. 14 ...... Diwali begins Feb. 17 ... Ash Wednesday Dorchester, and Holland, January 18..................M.L. King Jr. Day: No school all grades − first day of school Nov. 26 .......Thanksgiving Mar. 27-Apr. 3 ..... Passover February 15 .................... Presidents Day: No school September 7 .......................... Labor Day: No school Dec. 10-18 .......Hanukkah Apr. 2 ............ Good Friday February 16-19.............February Recess: No school September 8 .............. All teachers and paras report Dec. 25 ............Christmas Apr. 4 ...................... Easter April 2 ...................................................... No school September 21 ..........REMOTE: ALL Students report Dec. -

2021-2022 Special Per Diem Rates

2021-2022 Special Per Diem Rates Notice 2021-52 SECTION 1. PURPOSE This annual notice provides the 2021-2022 special per diem rates for taxpayers to use in substantiating the amount of ordinary and necessary business expenses incurred while traveling away from home, specifically (1) the special transportation industry meal and incidental expenses (M&IE) rates, (2) the rate for the incidental expenses only deduction, and (3) the rates and list of high-cost localities for purposes of the high-low substantiation method. This notice also modifies Notice 2020-71, 2020-40 I.R.B. 786, to change the portion of the year Sedona, Arizona is a high-cost locality under section 5 of Notice 2020-71. SECTION 2. BACKGROUND Rev. Proc. 2019-48, 2019-51 I.R.B. 1392 (or successor), provides rules for using a per diem rate to substantiate, under § 274(d) of the Internal Revenue Code and § 1.274-5 of the Income Tax Regulations, the amount of ordinary and necessary business expenses paid or incurred while traveling away from home. Taxpayers using the rates and list of high-cost localities provided in this notice must comply with Rev. Proc. 2019-48 (or successor). Notice 2020-71, as modified by this notice, provides the rates and list of high-cost localities for the period October 1, 2020, to September 30, 2021. SECTION 3. SPECIAL M&IE RATES FOR TRANSPORTATION INDUSTRY The special M&IE rates for taxpayers in the transportation industry are $69 for any locality of travel in the continental United States (CONUS) and $74 for any locality of travel outside the continental United States (OCONUS). -

July 17, 2020

July 17, 2020 COVID-19 Resources: CMHA has developed a curated set of COVID-19-related resources and announcements from a range of reputable state and national sources. That curated set of resources, which will be regularly updated, is available by CLICKING HERE. CMH Association and Member Activities ............................................................................... 3 CMHA CHI2 report on performance of Michigan’s public mental health system featured in podcast .. 3 Cultural and linguistic competence resources provided via CMHA/MHTTC/SAMHSA partnership ....... 3 Social media posts to highlight findings of CMHA/CHI2 white paper “A Tradition of Excellence and Innovation: Measuring the Performance of Michigan’s Public Mental Health System” ........................ 4 State & National Developments and Resources ...................................................................... 5 Most recent BHDDA COVID-related guidance documents ..................................................................... 5 MDHHS announces delay in EVV implementation ................................................................................. 6 Medicaid bulletin issued on Psychiatric Collaborative Care Model ........................................................ 6 Michigan removes co-payment by Medicaid beneficiaries for SUD medications .................................. 6 Michigan Health Policy Forum to hold discussion of Health Disparities: Where Racism Intersects Health .................................................................................................................................................... -

Pay Week Begin: Saturdays Pay Week End: Fridays Check Date

Pay Week Begin: Pay Week End: Due to UCP no later Check Date: Saturdays Fridays than Monday 7:30am week 1 December 10, 2016 December 16, 2016 December 19, 2016 December 30, 2016 week 2 December 17, 2016 December 23, 2016 December 26, 2016 week 1 December 24, 2016 December 30, 2016 January 2, 2017 January 13, 2017 week 2 December 31, 2016 January 6, 2017 January 9, 2017 week 1 January 7, 2017 January 13, 2017 January 16, 2017 January 27, 2017 week 2 January 14, 2017 January 20, 2017 January 23, 2017 January 21, 2017 January 27, 2017 week 1 January 30, 2017 February 10, 2017 week 2 January 28, 2017 February 3, 2017 February 6, 2017 week 1 February 4, 2017 February 10, 2017 February 13, 2017 February 24, 2017 week 2 February 11, 2017 February 17, 2017 February 20, 2017 March 3, 2017 week 1 February 18, 2017 February 24, 2017 February 27, 2017 ***1 Week Pay Period Transition*** week 1 February 25, 2017 March 3, 2017 March 6, 2017 March 17, 2017 week 2 March 4, 2017 March 10, 2017 March 13, 2017 week 1 March 11, 2017 March 17, 2017 March 20, 2017 March 31, 2017 week 2 March 18, 2017 March 24, 2017 March 27, 2017 week 1 March 25, 2017 March 31, 2017 April 3, 2017 April 14, 2017 week 2 April 1, 2017 April 7, 2017 April 10, 2017 week 1 April 8, 2017 April 14, 2017 April 17, 2017 April 28, 2017 week 2 April 15, 2017 April 21, 2017 April 24, 2017 week 1 April 22, 2017 April 28, 2017 May 1, 2017 May 12, 2017 week 2 April 29, 2017 May 5, 2017 May 8, 2017 week 1 May 6, 2017 May 12, 2017 May 15, 2017 May 26, 2017 week 2 May 13, 2017 May 19, 2017 May -

Investment Plan Reemployment Table

INVESTMENT PLAN Termination and Reemployment Limitations Renewed membership is allowed for reemployed service on or after July 1, 2017. Distribution Month Termination Requirement Reemployment (Retired) January 2020 January 2020‐July 31, 2020 August 1, 2020‐January 31, 2021 February 2020 February 2020‐August 31, 2020 September 1, 2020‐February 28, 2021 March 2020 March 2020‐September 30, 2020 October 1, 2020‐March 31, 2021 April 2020 April 2020‐October 31, 2020 November 1, 2020‐April 30, 2021 May 2020 May 2020‐November 30, 2020 December 1, 2020‐May 31, 2021 June 2020 June 2020‐December 31, 2020 January 1, 2021‐June 30, 2021 July 2020 July 2020‐January 31, 2021 February 1, 2021‐July 31, 2021 August 2020 August 2020‐February 28, 2021 March 1, 2021‐August 31, 2021 September 2020 September 2020‐March 31, 2021 April 1, 2021‐September 30, 2021 October 2020 October 2020‐April 30, 2021 May 1, 2021‐October 31, 2021 November 2020 November 2020‐May 31, 2021 June 1, 2021‐November 30, 2021 December 2020 December 2020‐June 30, 2021 July 1, 2021‐December 31, 2021 January 2021 January 2021‐July 31, 2021 August 1, 2021‐January 31, 2022 February 2021 February 2021‐August 31, 2021 1 September 1, 2021‐February 28, 2022 March 2021 March 2021‐September 30, 2021 October 1, 2021‐March 31, 2022 April 2021 April 2021‐October 31, 2021 November 1, 2021‐April 30, 2022 May 2021 Months May 2021‐November 30, 2021 December 1, 2021‐May 31, 2022 6 distributions June 2021 June 2021‐December 31, 2021 January 1, 2022‐June 30, 2022 July 2021 July 2021‐January 31, 2022 February -

July 31, 2020

July 31, 2020 Summary The United States has 4,496,737 confirmed COVID-19 cases and 152,074 reported related deaths. NIAID Director Fauci, CDC Director Redfield, and Assistant Health Secretary Giroir testified on COVID-19 during a hearing of the House Select Subcommittee on the Coronavirus Crisis. Redfield commented that wearing face masks, social distancing, avoiding gathering in large groups, and maintaining hand hygiene would provide “the same bang for the buck as if we just shut down the entire economy.” Giroir noted that 75% of COVID-19 test results in the country are received within five days. Fauci projected that a “safe and effective” vaccine would likely be available by late fall or early winter. Department of Health and Human Services announced a $2.1 billion agreement with Sanofi and GlaxoSmithKline to support late stage development, clinical trials, and large-scale manufacturing of 100 million doses of an investigational COVID-19 vaccine. The House Oversight and Reform Committee released a report analyzing a federal contract with Philips Respironics for ventilators and projected that the Health Department overpaid for the machines by as much as $500 million. Florida announced 257 COVID-19 fatalities on Friday, July 31, setting a record high of COVID- 19 deaths for the fourth day in a row. A University of South Florida public health expert commented that “what we’re seeing now is the result of the push to open the state” too quickly. In Texas, Governor Abbott announced that schools will be required to provide in-person instruction this fall, but that some districts may be eligible for extended waivers on a “case-by- case basis.” United Airlines plans to add more than 25 international routes to its September schedule, include destinations in Europe and Asia. -

ACADEMIC and ADMINISTRATIVE CALENDAR 2021–22 University of California, Santa Cruz

ACADEMIC AND ADMINISTRATIVE CALENDAR 2021–22 UniversitY OF CALIFORNIA, Santa CruZ Key Dates Fall ’21 Winter ’22 Spring ’22 Summer ’22 Fall ’21 Winter ’22 Spring ’22 Summer ’22 QUARTER BEGINS Sept 18 Jan 3 Mar 28 June 20 E-BILLS AVAILABLE Aug 27 Nov 23 Feb 25 Varies* Sat Mon Mon Mon ON UCSC eBILL/ePAY Fri Tues Fri Including registration and housing fees. ORIENTATION See orientation schedule for details (orientation.ucsc.edu). STUDENT HEALTH Sept 15 Dec 15 Mar 15 Jul 15 INSTRUCTION BEGINS Sept 23 Jan 3 Mar 28 June 20 Wed Wed Tues Thurs Thur Mon Mon Mon INSURANCE Deadline to apply for waiver. Cowell Student Health Center. INSTRUCTION ENDS Dec 3 Mar 11 June 3 Aug 26 Sept 14 Dec 28 Mar 21 N/A Fri Fri Fri Fri MINIMUM CREDIT LIMIT ENFORCED Wed Tues Mon FINAL EXAMINATIONS Dec 6-10 Mar 14–18 June 6–9 varies Twelve credits for undergraduates and five credits for graduates. Mon–Fri Mon–Fri Mon–Thur FINANCIAL AID DISBURSED Sept 14 Dec 28 Mar 21 Varies* QUARTER ENDS Dec 10 Mar 18 June 9 Aug 26 Fri Fri Thur Fri TO STUDENT ACCOUNTS Wed Tues Mon NUMBER OF DAYS M-10, T-10, W- M-8, T-10, W- M-9, T-10, W- HOUSING AND DINING Sept 16 Dec 15 Mar 22 Varies* OF INSTRUCTION 10, Th-9, F-10 10, Th-10, F-10 10, Th-10, F-10 FEES DUE Thur Wed Tues TOTAL DAYS OF 49 48 49 Late housing fee of $25 assessed after this date. -

2021 Working Day Calendar-5 Day-Alternative Format

2021 Working Days Calendar – 5 day The Working Day Calendar is used to compute the estimated completion date of a contract. To use the calendar, find the start date of the contract, add the working days to the number of the calendar date (a number from 1 to 1000), and subtract 1, find that calculated number in the calendar and that will be the completion date of the contract Date Number of the Calendar Date Friday, January 1, 2021 Non-working Day Saturday, January 2, 2021 Non-working Day Sunday, January 3, 2021 Non-working Day Monday, January 4, 2021 938 Tuesday, January 5, 2021 939 Wednesday, January 6, 2021 940 Thursday, January 7, 2021 941 Friday, January 8, 2021 942 Saturday, January 9, 2021 Non-working Day Sunday, January 10, 2021 Non-working Day Monday, January 11, 2021 943 Tuesday, January 12, 2021 944 Wednesday, January 13, 2021 945 Thursday, January 14, 2021 946 Friday, January 15, 2021 947 Saturday, January 16, 2021 Non-working Day Sunday, January 17, 2021 Non-working Day Monday, January 18, 2021 Non-working Day Tuesday, January 19, 2021 948 Wednesday, January 20, 2021 949 Thursday, January 21, 2021 950 Friday, January 22, 2021 951 Saturday, January 23, 2021 Non-working Day Sunday, January 24, 2021 Non-working Day Monday, January 25, 2021 952 Tuesday, January 26, 2021 953 Wednesday, January 27, 2021 954 Thursday, January 28, 2021 955 Friday, January 29, 2021 956 Saturday, January 30, 2021 Non-working Day Sunday, January 31, 2021 Non-working Day Monday, February 1, 2021 957 Tuesday, February 2, 2021 958 Wednesday, February 3,