Value Fund As of June 30, 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NYCHA Facilities and Service Centers

NYCHA Facilities and Service Centers BOROUGH DEVELOPMENT NAME ADDRESS Manhattan Baruch 595- 605 FDR Drive Staten Island Berry Houses 44 Dongan Hills Brooklyn Farragut 228 York Street Manhattan Harborview Terrace 536 West 56th Street Brooklyn Howard 1620 E N Y Avenue Manhattan Lexington 115 East 98th Steet Brooklyn Marcus Garvey 1440 E N Y Avenue Bronx Monroe 1802 Story Avenue Bronx Pelham Parkway 975 Waring Avenue Brooklyn Pink 2702 Linden Boulevard Queens Ravenswood 34-35A 12th Street Queens Ravenswood 34-35A 12th Street Brooklyn Red Hook East 110 West 9th Street Brooklyn Saratoga Square 930 Halsey Street Manhattan Washington Hts Rehab (Groups I and II) 500 West 164th Street Manhattan Washington Hts Rehab (Groups I and II) 503 West 177th Street Manhattan Wilson 405 East 105th Steet Manhattan Wise Towers/WSURA 136 West 91st Steet Brooklyn Wyckoff Gardens 266 Wyckoff Street Page 1 of 148 10/01/2021 NYCHA Facilities and Service Centers POSTCO STATUS SPONSOR DE Occupied Henry Street Settlement, Inc. Occupied Staten Island Mental Health Society, Inc. 10306 Occupied Spanish Speaking Elderly Council - RAICES Occupied NYCHA 10019 NYCHA HOLD NYCHA 11212 Occupied Lexington Children's Center 10029 Occupied Fort Greene Senior Citizens Council 11212 Vacant NYCHA Occupied Jewish Association Services For the Aged Occupied United Community Centers Occupied HANAC, Inc. 11106 Occupied HANAC, Inc. Occupied Spanish Speaking Elderly Council - RAICES Occupied Ridgewood-Bushwick Sr Citizens Council, Inc. Vacant NYCHA Occupied Provider Name Unknown Occupied -

Supersized Billboards in Times Square Command Ever-Increasing Rents

MARKETVIEW MANHATTAN RETAIL Manhattan Retail, Q1 2015 Supersized billboards in Times Square command ever-increasing rents U.S. Consumer Confidence Index U.S. Retail Sales U.S. Unemployment Rate U.S Retail Trade Employment (Mar 2015) 101.3 (Mar 2015) 0.9% (Mar 2015) 5.5% (Mar 2015) 26,000 *Arrows indicate month-over-month change Figure 1: Key Economic Indicators NYC NYC Manhattan NYC Unemployment Rate Retail Job Count Retail Sales Volume Private Sector Job Count 6.6% i352.3 K i1.5 B h23 K (March 2015) (March 2015) (Q1 2015) (March 2015) *Arrows indicate month-over-month change, except for Manhattan Retail Sales Volume, Sources: The Conference Board; U.S. Department of Commerce; U.S. Department of Labor; which is quarter-over-quater. New York State Department of Labor; Real Capital Analytics. RETAIL NEWS • Brookfield place celebrated its grand • Bloomingdale’s will debut its first outlet store opening after undergoing a $250 million located in an urban center, at 2085 redevelopment. With 375,000 sq. ft. of retail Broadway. Slated to open by fall 2015, the space, the luxury mall features Diane von company’s 14th outlet store will occupy Furstenberg, Tory Burch, Omega and Vince 25,000 sq. ft. across three stories. among its tenant roster, as well as innovative • General Growth Properties Inc. recently dining destinations Le District and Hudson purchased the retail co-op at 85 Fifth Avenue Eats. for $86 million. Located one block west of Union Square, the building contains 12,946 • Set to become the second largest residential sq. ft. of retail space across the ground floor building in Manhattan, 606 W. -

Sidewalk Clock, 1501 Third Avenue and the Proposed Designation of the Related Landmark Site (Item No

Landmarks Preservation Commission August 25, 1981, Designation List 147 LP-1169 SIDEWALK CLOCK, I501Third Avenue, Borough of Manhattan. Manufacturer: E. Howard Clock Company. Landmark Site: The portion of the sidewalk on which the described improvement is situated adjacent to Borough of Manhattan, Tax Map Block 1530, Lot 47. On May 13, 1980, the Landmarks Preservation CoIIIDlission held a public hearing on the proposed designation as a Landmark of the Sidewalk Clock, 1501 Third Avenue and the proposed designation of the related Landmark Site (Item No. 41). The hearing had been duly advertised in accordance with the provisions of law. Four witnesses spoke in favor of designation. There were no speakers in opposition to des ignation. DESCRIPTION AND ANALYSIS One of the most important and essential parts of New York's historical fabric is its "street furniture" -- Jiamp posts, street clocks, sign posts, and benches that enhance and maintain the intimacy and scale of neighborhood blocks. Perhaps the most striking of these street amenities are the oversize cast-iron post or sidewalk clocks that proudly dominate city sidewalks. These clocks proliferated in American cities well after the turn of the twentieth century but many have since fallen prey to automobile accidents and sidewalk ordinances. One of the few that existsin New York t oday is the clock at No. 1501 Third Avenue. Introduced in the 1860s, cast-iron street clocks we re popular both as everyday conveniences and as novel advertising devices. A small business concern that stayed in the same location year aft er year would buy a street clock and ins tall it directly in front of the store, often painting the name of the business onto the clock face. -

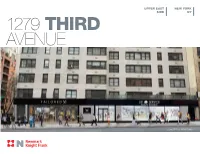

1279 Third Avenue 2020

UPPER EAST NEW YORK SIDE NY 1279 THIRD AVENUE CONCEPTUAL RENDERING SPACE DETAILS LOCATION GROUND FLOOR | PROPOSED DIVISIONS Southeast corner of East 74th Street APPROXIMATE SIZE Ground Floor 7,000 SF* Basement 1,588 SF Total 8,588 SF *Divisible POSSESSION Immediate TERM Long term FRONTAGE 101 FT 9 IN on Third Avenue EAST 74TH STREETEAST 74TH SITE STATUS Formerly Duane Reade NEIGHBORS Morton Williams, Nordstrom Local, Bluemercury, Paper Source, Joe & The Juice, Journelle, JG Mellon and Target COMMENTS Very dense affluent population Seven day and night pedestrian traffic Nearby access to the subway line at Second Avenue and East 72nd 49 FT 4 IN 52 FT 5 IN Street and the at Lexington Avenue and East 77th Street THIRD AVENUE Steps from the express and local Third Avenue and 72nd Street crosstown buses Within close proximity to Marymount Manhattan and Hunter Colleges AREA NEIGHBORS EAST 88TH STREET EAST 88TH STREET Shoga Brora The Gaf Margo Manhattan Immanuel Lutheran Church Thais Clothing Iris Nail Ichiro Sushi East 87 Wine Traders Fine Wines & Spirits Trek Bikes United Kick Boxing United Tae Kwan Do Bocado Café EAST 87TH STREET EAST 87TH STREET Anne & Valentin Alexander Florist EAST 86TH STREET EAST 86TH STREET Q Neue Café Demarchelier Galerie Sabarsky Restaurant Chuckies Morini Schaller & Weber Premier Cru Schaller's Stube Two Little Red Hens Heidelberg Restaurant Five Mile Stone EAST 85TH STREET EAST 85TH STREET New Amity Restaurant La Pulperia Schweitzer Linen PARK AVENUE PARK AVENUE PARK Million 84 Street Corner FIFTH AVENUE FIFTH Artbag THIRD AVENUE SECOND AVENUE MADISON AVENUE EAST 84TH STREET EAST 84TH STREET LEXINGTON AVENUE Koreana Art Bernard & and Antiques S. -

Manhattan New Construction & Proposed Multifamily Projects 4Q20

Manhattan New Construction & Proposed Multifamily Projects 4Q20 83 85 82 12 41 62 ID PROPERTY UNITS 6 30 Morningside Drive 205 Total Lease Up 205 12 HAP Seven NY 129 15 418 West 126th Street 75 19 Victoria Theatre 191 15 Total Under Construction 395 19 37 Broadway Development 130 6 41 210 Wadsworth Avenue 98 46 Total Planned 228 43 96th Street 171 43 46 Frederick Douglass Blvd 100 37 62 4037 Broadway 132 82 The Heights on Broadway 171 83 Sherman Plaza 272 85 3875 9th Avenue 614 Total Prospective 1,460 2000 ft Source: Yardi Matrix LEGEND Lease-Up Under Construction Planned Prospective Manhattan New Construction & Proposed Multifamily Projects 4Q20 44 73 ID PROPERTY UNITS 1 The Smile 233 3 Convivium 140 45 4 Sixty 125 141 4 39 23 26 5 Two Waterline Square 435 Total Lease Up 949 1 74 13 75 10 Sendero Verde Phase II 361 22 24 13 One East Harlem 404 25 Total Under Construction 765 49 22 15 West 118th Street 51 38 23 1971 Madison Avenue 93 10 24 72 East 120th Street 218 77 25 77 East 118th Street 202 47 26 East 127th Street 152 38 La Hermosa Tower 160 39 2031-2033 5th Avenue 240 Total Planned 1,116 48 44 58 West 135th Street 100 45 64-74 West 125th Street 200 47 1987-1991 3rd Avenue 59 76 48 1988-1996 2nd Avenue 185 49 248 East 120th Street 86 50 308 East 86th Street 68 78 52 Lenox Hill Hospital 200 73 Lenox Terrace Phase II 1,642 74 1800 Park Avenue 670 50 75 2460 2nd Avenue 730 3 76 321 East 96th Street 1,100 77 East River Plaza 1,100 52 5 78 Holmes Towers NextGen Development 339 Total Prospective 6,479 1000 ft Source: Yardi Matrix LEGEND -

Emergency Response Incidents

Emergency Response Incidents Incident Type Location Borough Utility-Water Main 136-17 72 Avenue Queens Structural-Sidewalk Collapse 927 Broadway Manhattan Utility-Other Manhattan Administration-Other Seagirt Blvd & Beach 9 Street Queens Law Enforcement-Other Brooklyn Utility-Water Main 2-17 54 Avenue Queens Fire-2nd Alarm 238 East 24 Street Manhattan Utility-Water Main 7th Avenue & West 27 Street Manhattan Fire-10-76 (Commercial High Rise Fire) 130 East 57 Street Manhattan Structural-Crane Brooklyn Fire-2nd Alarm 24 Charles Street Manhattan Fire-3rd Alarm 581 3 ave new york Structural-Collapse 55 Thompson St Manhattan Utility-Other Hylan Blvd & Arbutus Avenue Staten Island Fire-2nd Alarm 53-09 Beach Channel Drive Far Rockaway Fire-1st Alarm 151 West 100 Street Manhattan Fire-2nd Alarm 1747 West 6 Street Brooklyn Structural-Crane Brooklyn Structural-Crane 225 Park Avenue South Manhattan Utility-Gas Low Pressure Noble Avenue & Watson Avenue Bronx Page 1 of 478 09/30/2021 Emergency Response Incidents Creation Date Closed Date Latitude Longitude 01/16/2017 01:13:38 PM 40.71400364095638 -73.82998933154158 10/29/2016 12:13:31 PM 40.71442154062271 -74.00607638041981 11/22/2016 08:53:17 AM 11/14/2016 03:53:54 PM 40.71400364095638 -73.82998933154158 10/29/2016 05:35:28 PM 12/02/2016 04:40:13 PM 40.71400364095638 -73.82998933154158 11/25/2016 04:06:09 AM 40.71442154062271 -74.00607638041981 12/03/2016 04:17:30 AM 40.71442154062271 -74.00607638041981 11/26/2016 05:45:43 AM 11/18/2016 01:12:51 PM 12/14/2016 10:26:17 PM 40.71442154062271 -74.00607638041981 -

1122 Third Avenue Upper East Side 1122 Third Avenue

1122 THIRD AVENUE UPPER EAST SIDE 1122 THIRD AVENUE Ground Floor (Approx.) Basement (Approx.) 900 SF 500 SF ADDRESS 1122 Third Avenue, New York, NY 10065 (Between East 65th & 66th Streets) SIZE Ground Floor 900 SF Lower Level 500 SF FRONTAGE 17' on 3rd Avenue ASKING PRICE Upon Request POSSESSION Immediate COMMENTS • Previously True Religion • Densely populated shopping and residential district • Steps from the 6 Q F subway stations • All uses considered • Short term considered NEIGHBORING TENANTS Lululemon, Nike, Sant Ambroeus, Crunch, Flywheel, FlyBarre, SLT, Chase, Bank of America, AT&T, TD Bank, CitiBank, Pier 1 Imports, Oath Pizza, Swerve 17' 3rd Avenue 1122 THIRD AVENUE EAST 70TH STREET EAST 70TH STREET EAS T 70TH S T R E E T Hot & Tasty Bagels NEIGHBORHOOD MAP Fantastic Cleaners EAST 69TH STREET EAST 69TH STREET EAS T 69TH S T R E E T Jean Claude Biguine EAST 68TH STREET EAST 68TH STREET EAS T 68TH S T R E E T by Broadway Carpet EAST 67TH STREET EAST 67TH STREET EAS T 67TH S T R E E T Lexington Armory Beekman Theatre THIRD AVENUE PARK AVENUE LEXINGTON AVENUE EAST 66TH STREET SECOND AVENUE Madame Paulette FOR MORE INFORMATION CONTACT EXCLUSIVE AGENTS: EAST 65TH STREET STEVEN E. BAKER, PRESIDENT DANIYEL COHEN CLAUDIA MILLER 212.792.2636 212.792.2610 212.792.2604 [email protected] [email protected] [email protected] William Wayne & Co EAST 64TH STREET China Fun WINICK REALTY GROUP LLC Corrados OPTYX LICENSED REAL ESTATE BROKERS Bakery by gruen 655 Third Avenue, 17th Floor, New York, NY 10017 T. -

F. Vehicular Traffic

Chapter 9: Transportation (Vehicular Traffic) F. VEHICULAR TRAFFIC EXISTING CONDITIONS STREET AND ROADWAY NETWORK Traffic conditions in the study area vary in relation to a number of factors—the nature of the street and roadway network, surrounding land uses and the presence of major traffic generators, and the intensity of interaction between autos, taxis, trucks, buses, deliveries, and pedestrians. The study area contains five subareas, or zones—Lower Manhattan, the Lower East Side, East Midtown, the Upper East Side, and East Harlem—and each has different street and roadway characteristics along its length. East Midtown, the Upper East Side, and East Harlem are characterized by a regular street grid, with avenues running north-south and streets running east- west. Each of the major north-south avenues—First, Second, Third, Lexington, Park, Madison, and Fifth Avenues—are major traffic carriers. There is just one limited-access roadway, the FDR Drive, which extends around the eastern edge of the study area from its northern end to its southern end. A general overview of the character of the street and roadway network in each of the five zones is presented below. Lower Manhattan is characterized by an irregular grid pattern south of Canal Street. Except for a few major arterials, most streets within the area are narrow with usually just one "moving" lane. Travel is time-consuming and slow along them. Pedestrian traffic often overflows into the street space, further impeding vehicular traffic flow. Water Street and Broadway are the two key north-south streets in this area, and carry two or more effective travel lanes, yet are often difficult to negotiate due to frequent double-parked truck traffic. -

Press Release

Press Release For Immediate Release Contact: April 29, 2020 Tom Nolan/Francisco Miranda 212-741-2977 [email protected]/[email protected] Avison Young arranges sale of retail condominium at 1683 Third Avenue Upper East Side retail condo situated at the base of The Kent luxury condo sells for $28.712 million New York City – The Tri-State Investment Sales Group for Avison Young has arranged the $28.712 million sale of a retail condominium unit located at 1683 Third Avenue on behalf of the property’s ownership – a partnership headed by Extell Development Company, the property’s developer. The asset is located within the Yorkville submarket of Manhattan’s Upper East Side and situated at the base of The Kent, a newly constructed, 30-story luxury condominium building on the corner of Third Avenue and 95th street. An Avison Young team comprised of Principals James Nelson, Head of Tri-State Investment Sales, Vincent Carrega, Neil Heilman, Director Brent Glodowski and Associate Angela Mulder, represented the owner. The newly constructed property features 12,796 square feet at grade and a 9,767-square-foot lower level selling space for a total of 22,563 gross square feet. The NYC School Construction Authority currently has a long-term lease at the property occupying 11,492 square feet on the ground floor, while the remaining 1,304 square-foot ground floor space and entire 9,767-square- foot cellar were available for lease at the time of the sale. “The retail condominium at The Kent offered the opportunity to acquire a newly constructed retail space in the base of a beautiful luxury Upper East Side property with a built-in tenancy and an in- place cash flow, as well as future upside with the remaining available space,” notes Nelson. -

2252 THIRD AVENUE 50’ WIDE DEVELOPMENT SITE: ~ 51,000 BSF Within the New East Harlem Rezoning 2252 THIRD AVENUE - PROPERTY FEATURES

EXISTING STRUCTURE 2252 THIRD AVENUE 50’ WIDE DEVELOPMENT SITE: ~ 51,000 BSF Within The New East Harlem Rezoning 2252 THIRD AVENUE - PROPERTY FEATURES ASKING PRICE: $12,000,000 PPBSF: $236 Property Features: Location: West side of Third Avenue between East 122nd & East 123rd Streets Block & Lot: 1771 - 36 Lot Dimensions: 50.92' x 100' Lot Size: 5,092 sq ft (approx.) Zoning: R10 / C4-6 Residential FAR: 10.0 (Wide Street) Total Residential Buildable SF: 50,920 sq ft (approx.) Max Buildable Height: 235 ft Mandatory Inclusionary 20% or 25% of residential FAR Housing Requirement*: Existing Building Dimensions: 50.92' x 100' Existing Building SF: 14,500 sq ft (approx.) Available Air Rights: 36,420 sq ft (approx.) Assessment (17/18): $549,990 Taxes (17/18): $58,156 *For more information please visit page 7 Tax Map East 123rd Street 100’ Lot 39 Third Avenue Third Lot 38 Lexington Avenue Lexington Lot 33 100’ East 122nd Street Three connecting lots with potential for air rights transfer 2 PROPERTY OVERVIEW Property Overview 2252 Third Avenue is a 50’ wide residential development site with a commercial overlay located in the newly rezoned section of East Harlem. The site is located just two blocks south of 125th Street along the west side of 3rd Avenue and offers future development of just under 51,000 buildable square feet. Newly upzoned from a 4.0 FAR with a 85 foot maximum building height to a 10.0 FAR with a 235 foot maximum building height. 2252 3rd Avenue offers tremendous assemblage and development opportunities. Current Use The site is currently a three-story plus basement structure that is built full in its entirety on the 100 foot deep lot. -

Preventive Services Directory

PREVENTIVE SERVICES DIRECTORY Michael R. Bloomberg Mayor John B. Mattingly Commissioner Revised 8/07 NYC Administration for Children’s Services provides preventive services, directly or through contracted service providers, to allow children who are at risk of foster placement to remain at home. TABLE OF CONTENTS Contracted Preventive Program Types pg • General Preventive – Serves a specific catchment area and is able to address a wide 2 variety of family situations by providing case planning and counseling services. • Persons in Need of Supervision Diversion/Designated Assessment Services (PINS/DAS) – Provides short-term assessment, crisis intervention, mediation and counseling services as an alternative to applying for a PINS petition in Family Court. • PINS General Preventive – Attached to PINS/DAS provider. Offers longer-term case planning and counseling services to teens and their families. • Beacon School Based Model – Serves families in designated local schools. A “one stop shopping” model that includes education, recreation and socialization activities for the entire family. Some schools also have a General Preventive component, which greatly enhances the Beacon Model. pg • Family Rehabilitation Programs (FRP) – Serves families for whom parental substance 28 abuse is the presenting problem. Given the high-risk nature of this population, there is a lower case load and increased casework contact expectations. There is an enhanced staffing model with the incorporation of a case aide. pg • Intensive Preventive and Aftercare Services for Adolescents – Provides intensive 39 family support services for at-risk adolescents using evidence-based treatment models such as Multisystemic Therapy and Functional Family Therapy. pg • Enhanced Preventive Services for Teens and Babies – Serves teens and babies in 42 highest need communities, with enhanced clinical resources and specialists on staff. -

City of Longmont Historic Properties (May 2021)

City of Longmont Historic Properties (May 2021) Contributing NOT Within Building Original Plat Local National (National of Property Address Landmark Landmark District) Notes Longmont 1000 Block Fourth Avenue Yes WEST 1005 Third Avenue Yes WEST 1007 Third Avenue WEST 1009 Third Avenue WEST 1010 Third Avenue WEST 1011 Fourth Avenue WEST 1011 Third Avenue WEST 1012 Third Avenue WEST 1013 Fourth Avenue WEST 1017 Fourth Avenue WEST 1019 Third Avenue Yes WEST 102 Fourth Avenue Yes 1021 Third Avenue Yes WEST 1022 Third Avenue WEST 1025 Third Avenue WEST 1027 Fourth Avenue WEST 103 Main Street Yes 1032 Collyer Street Yes X 10662 Pike Road Yes X 1102 Third Avenue WEST 1106 Third Avenue WEST 1110 Fourth Avenue WEST 1110 Longs Peak Avenue Yes 1111 Fourth Avenue WEST 1114 Fourth Avenue WEST 1117 Neon Forest Circle Yes X 1117 Third Avenue Yes 1120 Third Avenue WEST 1121 Third Avenue WEST 1125 Third Avenue WEST 1126 Fourth Avenue WEST 1126 Third Avenue WEST 1127 17th Avenue YES X 1128 Fourth Avenue WEST 1130 Collyer Street Yes X 1203 Third Avenue WEST X 1206 Third Avenue Yes WEST X 1210 Third Avenue WEST X 1211 Third Avenue WEST X 1225 Third Avenue WEST X 1228 Third Avenue WEST X 1230 Third Avenue WEST X 1236 Third Avenue Yes WEST X 1237 Third Avenue Yes WEST X 1239 Third Avenue WEST X 1241 Third Avenue WEST X 1244 Third Avenue WEST X 1246 Third Avenue WEST X 1249 Third Avenue Yes WEST X 1255 Third Avenue WEST X 1266 Longs Peak Avenue Yes X 1283 Third Avenue Yes X Entire X Property is a National Entire 1303 Hover Street Yes District Property 13076 Pike Road Yes X 1309 Hover Street Yes X 136 S.