Rwandair Strategy & Challenges 2011-2020 Presented 14 December 2011 Strategic Focus ‐ the Business Model

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

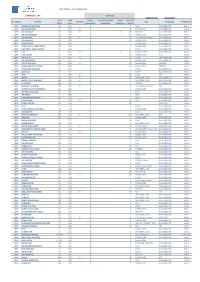

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

East and Central Africa 19

Most countries have based their long-term planning (‘vision’) documents on harnessing science, technology and innovation to development. Kevin Urama, Mammo Muchie and Remy Twingiyimana A schoolboy studies at home using a book illuminated by a single electric LED lightbulb in July 2015. Customers pay for the solar panel that powers their LED lighting through regular instalments to M-Kopa, a Nairobi-based provider of solar-lighting systems. Payment is made using a mobile-phone money-transfer service. Photo: © Waldo Swiegers/Bloomberg via Getty Images 498 East and Central Africa 19 . East and Central Africa Burundi, Cameroon, Central African Republic, Chad, Comoros, Congo (Republic of), Djibouti, Equatorial Guinea, Eritrea, Ethiopia, Gabon, Kenya, Rwanda, Somalia, South Sudan, Uganda Kevin Urama, Mammo Muchie and Remy Twiringiyimana Chapter 19 INTRODUCTION which invest in these technologies to take a growing share of the global oil market. This highlights the need for oil-producing Mixed economic fortunes African countries to invest in science and technology (S&T) to Most of the 16 East and Central African countries covered maintain their own competitiveness in the global market. in the present chapter are classified by the World Bank as being low-income economies. The exceptions are Half the region is ‘fragile and conflict-affected’ Cameroon, the Republic of Congo, Djibouti and the newest Other development challenges for the region include civil strife, member, South Sudan, which joined its three neighbours religious militancy and the persistence of killer diseases such in the lower middle-income category after being promoted as malaria and HIV, which sorely tax national health systems from low-income status in 2014. -

Real Estate and Late Urbanization in Kigali and Addis Ababa

This is a repository copy of Urban Fortunes and Skeleton Cityscapes: Real Estate and Late Urbanization in Kigali and Addis Ababa . White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/115778/ Version: Accepted Version Article: Goodfellow, T. orcid.org/0000-0001-9598-5292 (2017) Urban Fortunes and Skeleton Cityscapes: Real Estate and Late Urbanization in Kigali and Addis Ababa. International Journal of Urban and Regional Research, 41 (5). pp. 786-803. ISSN 0309-1317 https://doi.org/10.1111/1468-2427.12550 This is the peer reviewed version of the following article: Goodfellow, T. (2017), Urban Fortunes and Skeleton Cityscapes: Real Estate and Late Urbanization in Kigali and Addis Ababa. Int. J. Urban Reg. Res., 41: 786–803. doi:10.1111/1468-2427.12550 , which has been published in final form at https://doi.org/10.1111/1468-2427.12550. This article may be used for non-commercial purposes in accordance with Wiley Terms and Conditions for Self-Archiving Reuse Items deposited in White Rose Research Online are protected by copyright, with all rights reserved unless indicated otherwise. They may be downloaded and/or printed for private study, or other acts as permitted by national copyright laws. The publisher or other rights holders may allow further reproduction and re-use of the full text version. This is indicated by the licence information on the White Rose Research Online record for the item. Takedown If you consider content in White Rose Research Online to be in breach of UK law, please notify us by emailing [email protected] including the URL of the record and the reason for the withdrawal request. -

UPDATED ON: 18-03-2019 STATION AIRLINE IATA CODE AWB Prefix ON-LINE CARGO HANDLING FREIGHTER RAMP HANDLING RAMP LINEHAUL IMPORT

WFS CARGO - CUSTOMERS LIST DENMARK - CPH SERVICES UPDATED ON: 18-03-2019 IATA AWB CARGO FREIGHTER RAMP RAMP IMPORT STATION AIRLINE ON-LINE GSA TRUCKING TERMINAL CODE Prefix HANDLING HANDLING LINEHAUL EXPORT CPH AMERICAN AIRLINES AA 001 X E NAL WALLENBORN HAL 1 CPH DELTA AIRLINES DL 006 X X I/E PROACTIVE WALLENBORN HAL1 CPH AIR CANADA AC 014 X X X I/E HWF DK WALLENBORN HAL 1 CPH UNITED AIRLINES UA 016 X I/E NORDIC GSA WALLENBORN HAL1 CPH LUFTHANSA LH 020 X X I/E LUFTHANSA CARGO WALLENBORN HAL1 CPH US AIRWAYS US 037 X I/E NORDIC GSA WALLENBORN HAL1 CPH DRAGON AIR XH 043 X I NORDIC GSA WALLENBORN HAL1 CPH AEROLINEAS ARGENTINAS AR 044 X E CARGOCARE WALLENBORN HAL1 CPH LAN CHILE - LINEA AEREA LA 045 X E KALES WALLENBORN HAL1 CPH TAP TP 047 X X x I/E SCANPARTNER WALLENBORN HAL1 CPH AER LINGUS EI 053 X I/E NORDIC GSA N/A HAL1 CPH AIR France AF 057 X X I/E KL/AF KIM JOHANSEN HAL2 CPH AIR SEYCHELLES HM 061 X E NORDIC GSA WALLENBORN HAL1 CPH CZECH AIRLINES OK 064 X X I/E AviationPlus VARIOUS HAL1 CPH SAUDI AIRLINES CARGO SV 065 X I/E AviationPlus VARIOUS HAL1 CPH ETHIOPIAN AIRLINES ET 071 X E KALES WALLENBORN HAL1 CPH GULF AIR GF 072 X E KALES WALLENBORN HAL1 CPH KLM KL 074 X X I/E KL/AF JDR HAL2 CPH IBERIA IB 075 X X I/E UNIVERSAL GSA WALLENBORN HAL1 CPH MIDDLE EAST AIRLINES ME 076 X X E UNIVERSAL GSA WALLENBORN HAL1 CPH EGYPTAIR MS 077 X E HWF DK WALLENBORN HAL1 CPH BRUSSELS AIRLINES SN 020 X X I/E LUFTHANSA CARGO JDR HAL1 CPH SOUTH AFRICAN AIRWAYS SA 083 X E CARGOCARE WALLENBORN HAL1 CPH AIR NEW ZEALAND NZ 086 X E KALES WALLENBORN HAL1 CPH AIR -

The Rwandan Genocide

The copyright of this thesis vests in the author. No quotation from it or information derived from it is to be published without full acknowledgement of the source. The thesis is to be used for private study or non- commercial research purposes only. Published by the University of Cape Town (UCT) in terms of the non-exclusive license granted to UCT by the author. University of Cape Town Town Cape of University Mass Murder and Motivation: The Rwandan Genocide ASMUND AAMAAS (amsasmOOl) A dissertation submitted in fulfilment of the requirements for the award of the degree of Master of Arts in Jewish Studies Faculty of the Humanities Department of Hebrew and Jewish Studies University of Cape Town 2007 Supervisors: Professor Milton Shain and Professor Mohamed Adhikari University of Cape Town Declaration: This work has not been previously submitted in whole, or in part, for the award of any degree. It is my own work. Each significant contribution to, and quotation in, this dissertation from the work, or works, of other people has been attributed, and has been cited and referenced. Acknowledgment The motivation for writing this thesis has its roots in a highly interesting course on Holocaust and mass murder convened and led by Professor Milton Shain at the University of Cape Town in 2003. The seminar was the main reason why I choose to write this thesis. I am truly grateful to my supervisor Professor Shain for letting me do this project and for valuable comments along the process of writing it. Thank you also to my co supervisor Professor Mohamed Adhikari for helpful comments on the thesis. -

O C E a N O C E a N C T I C P a C I F I C O C E a N a T L a N T I C O C E a N P a C I F I C N O R T H a T L a N T I C a T L

Nagurskoye Thule (Qanaq) Longyearbyen AR CTIC OCE AN Thule Air Base LAPTEV GR EENLA ND SEA EAST Resolute KARA BAFFIN BAY Dikson SIBERIAN BARENTS SEA SEA SEA Barrow SEA BEAUFORT Tiksi Prudhoe Bay Vardo Vadso Tromso Kirbey Mys Shmidta Tuktoyaktuk Narvik Murmansk Norilsk Ivalo Verkhoyansk Bodo Vorkuta Srednekolymsk Kiruna NORWEGIAN Urengoy Salekhard SEA Alaska Oulu ICELA Anadyr Fairbanks ND Arkhangelsk Pechora Cape Dorset Godthab Tura Kitchan Umea Severodvinsk Reykjavik Trondheim SW EDEN Vaasa Kuopio Yellowknife Alesund Lieksa FINLAND Plesetsk Torshavn R U S S Yakutsk BERING Anchorage Surgut I A NORWAY Podkamennaya Tungusk Whitehorse HUDSON Nurssarssuaq Bergen Turku Khanty-Mansiysk Apuka Helsinki Olekminsk Oslo Leningrad Magadan Yurya Churchill Tallin Stockholm Okhotsk SEA Juneau Kirkwall ESTONIA Perm Labrador Sea Goteborg Yedrovo Kostroma Kirov Verkhnaya Salda Aldan BAY UNITED KINGDOM Aluksne Yaroslavl Nizhniy Tagil Aberdeen Alborg Riga Ivanovo SEA Kalinin Izhevsk Sverdlovsk Itatka Yoshkar Ola Tyumen NORTH LATVIA Teykovo Gladkaya Edinburgh DENMARK Shadrinsk Tomsk Copenhagen Moscow Gorky Kazan OF BALTIC SEA Cheboksary Krasnoyarsk Bratsk Glasgow LITHUANIA Uzhur SEA Esbjerg Malmo Kaunas Smolensk Kaliningrad Kurgan Novosibirsk Kemerovo Belfast Vilnius Chelyabinsk OKHOTSK Kolobrzeg RUSSIA Ulyanovsk Omsk Douglas Tula Ufa C AN Leeds Minsk Kozelsk Ryazan AD A Gdansk Novokuznetsk Manchester Hamburg Tolyatti Magnitogorsk Magdagachi Dublin Groningen Penza Barnaul Shefeld Bremen POLAND Edmonton Liverpool BELARU S Goose Bay NORTH Norwich Assen Berlin -

Gorilla Trekking Safari

BEST OF KENYA “12 – Day Wildlife Safari” UNE J 4 – 15, 2021 $4950 per person plus international airfare Single Supplement - $2250 Kenya is renowned for its unparalleled wildlife, habitat diversity and fascinating cultural heritage. A wide range of ecological zones, semi-arid plains and vast savannahs, tropical montane forests, rugged wilderness, acacia woodlands, and rugged wilderness, provide for a tremendous array of fauna and flora. Under a limitless sapphire sky thrives an animal population, staggering in both diversity and number. Here, elephant, zebra, leopard, lion, rhinoceros, giraffe, cheetah and baboon have lived and adapted for eons in this ancient landscape, alongside more than a thousand colorful bird species and a multitude of butterflies and other insects. Our safari combines superlative wildlife viewing with luxurious comfort and attentive service, while staying in some of Kenya’s finest safari lodges and tented camps, as we explore in depth, this magical land known as the “Gem of Africa.” SAFARI ITINERARY DAY 1 – JUNE 4 - DEPART USA DAY 2 – JUNE 5 - ARRIVE NAIROBI (NBO) Upon arrival at the Jomo Kenyatta International Airport, you will be met by Safari Legacy and transferred to your hotel for check in. Overnight Crown Plaza Hotel. (meals in-flight) https://www.ihg.com/crowneplaza/hotels/us/en/nairobi/nbocp/hoteldetail DAY 3 – JUNE 6 - NAIROBI / TRAIN TO VOI / TSAVO WEST NATIONAL PARK & TAITA HILLS CONSERVANCY After breakfast, board your train and enjoy a scenic 4-hour train excursion to Voi Station where you will be met by your Safari Legacy Safari guides. Continue to the Taita Hills Conservancy arriving at Salt Lick Safari Lodge in time for lunch. -

Membership of the Board of Governors

Membership of the Board of Governors As of 15 February 2021 Chair of the Board Mr Robin Hayes Chief Executive Ocer JETBLUE AIRWAYS Members Mr Mikhail Pluboyarinov General Director and Chief Executive Ocer AEROFLOT Ms María José Hidalgo Gutiérrez Chief Executive Ocer AIR EUROPA Mr Benjamin Smith Chief Executive Ocer AIR FRANCE / KLM (representing Air France) Mr Yuji Hirako President and Chief Executive Ocer ALL NIPPON AIRWAYS Mr Douglas Parker Chairman and Chief Executive Ocer AMERICAN AIRLINES Mr Anco van der Wer Chief Executive Ocer AVIANCA Mr Tang Kin Wing Augustus Chief Executive Ocer CATHAY PACIFIC AIRWAYS LIMITED Mr Liu Shaoyong Chairman CHINA EASTERN AIRLINES Mr Wang Changshun Chairman CHINA SOUTHERN AIRLINES Mr Pedro Heilbron Executive President and Chief Executive Ocer COPA AIRLINES Mr Mohamed Roshdy Zakaria Chairman and Chief Executive Ocer Egyptair Holding Co (representing EGYPTAIR) Mr Tewolde GebreMariam Group Chief Executive Ocer ETHIOPIAN AIRLINES Mr Donald F. Colleran President and Chief Executive Ocer FEDEX EXPRESS Mr Luis Gallego MartÍn Chief Executive Ocer IAG (representing IBERIA) Mr Ronojoy Dutta Chief Executive Ocer INDIGO AIRLINES Mr Pieter Elbers President & CEO KLM ROYAL DUTCH AIRLINES Mr Walter Cho Chairman and CEO KOREAN AIR Mr Roberto Alvo Chief Executive Ocer LATAM Airlines Group Mr Carsten Spohr Chairman and Chief Executive Ocer LUFTHANSA Mr Mohamad El-Hout Chairman and Director General MIDDLE EAST AIRLINES Mr Mehmet Tevk Nane Chief Executive Ocer PEGASUS AIRLINES Mr Alan Joyce Chief Executive Ocer QANTAS Mr Akbar Al Baker Chief Executive Oce QATAR AIRWAYS Ms Yvonne Manzi Makolo CEO RWANDAIR Mr Rickard Gustafson President and Chief Executive Ocer SAS Mr Ibrahim Al-Omar Director General SAUDI ARABIAN AIRLINES Mr Goh Choon Phong Chief Executive Ocer SINGAPORE AIRLINES Mr Ajay Singh Chairman and Managing Director SPICEJET Mr Oscar Munoz Chairman UNITED AIRLINES ----- Mr Alexandre de Juniac Director General IATA. -

Analyzing the Case of Kenya Airways by Anette Mogaka

GLOBALIZATION AND THE DEVELOPMENT OF THE AIRLINE INDUSTRY: ANALYZING THE CASE OF KENYA AIRWAYS BY ANETTE MOGAKA UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA SPRING 2018 GLOBALIZATION AND THE DEVELOPMENT OF THE AIRLINE INDUSTRY: ANALYZING THE CASE OF KENYA AIRWAYS BY ANETTE MOGAKA A THESIS SUBMITTED TO THE SCHOOL OF HUMANITIES AND SOCIAL STUDIES (SHSS) IN PARTIAL FULFILMENT OF THE REQUIREMENT FOR THE AWARD OF MASTER OF ARTS DEGREE IN INTERNATIONAL RELATIONS UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA SUMMER 2018 STUDENT DECLARATION I declare that this is my original work and has not been presented to any other college, university or other institution of higher learning other than United States International University Africa Signature: ……………………… Date: ………………………… Anette Mogaka (651006) This thesis has been submitted for examination with my approval as the appointed supervisor Signature: …………………. Date: ……………………… Maurice Mashiwa Signature: …………………. Date: ……………………… Prof. Angelina Kioko Dean, School of Humanities and Social Sciences Signature: …………………. Date: ……………………… Amb. Prof. Ruthie C. Rono, HSC Deputy Vice Chancellor Academic and Student Affairs. ii COPYRIGHT This thesis is protected by copyright. Reproduction, reprinting or photocopying in physical or electronic form are prohibited without permission from the author © Anette Mogaka, 2018 iii ABSTRACT The main objective of this study was to examine how globalization had affected the development of the airline industry by using Kenya Airways as a case study. The specific objectives included the following: To examine the positive impact of globalization on the development of Kenya Airways; To examine the negative impact of globalization on the development of Kenya Airways; To examine the effect of globalization on Kenya Airways market expansion strategies. -

Nowhere to Go : Informal Settlement Eradication in Kigali, Rwanda

University of Louisville ThinkIR: The University of Louisville's Institutional Repository College of Arts & Sciences Senior Honors Theses College of Arts & Sciences 5-2017 Nowhere to go : informal settlement eradication in Kigali, Rwanda. Emily E Benken University of Louisville Follow this and additional works at: https://ir.library.louisville.edu/honors Part of the Social and Cultural Anthropology Commons Recommended Citation Benken, Emily E, "Nowhere to go : informal settlement eradication in Kigali, Rwanda." (2017). College of Arts & Sciences Senior Honors Theses. Paper 127. http://doi.org/10.18297/honors/127 This Senior Honors Thesis is brought to you for free and open access by the College of Arts & Sciences at ThinkIR: The University of Louisville's Institutional Repository. It has been accepted for inclusion in College of Arts & Sciences Senior Honors Theses by an authorized administrator of ThinkIR: The University of Louisville's Institutional Repository. This title appears here courtesy of the author, who has retained all other copyrights. For more information, please contact [email protected]. NOWHERE TO GO: INFORMAL SETTLEMENT ERADICATION IN KIGALI, RWANDA By Emily Elizabeth Benken Submitted in partial fulfillment of the requirements for Graduation summa cum laude and for Graduation with Honors from the Department of Anthropology University of Louisville May 2017 i ii NOWHERE TO GO: INFORMAL SETTLEMENT ERADICATION IN KIGALI, RWANDA By Emily Elizabeth Benken A Thesis Approved on March 27th, 2017 by the following Thesis Committee: Thesis Advisor Thesis Committee Member Thesis Committee Member iii DEDICATION This thesis is dedicated to my grandmother Mrs. Joyce Graeter Whose unending support made this thesis possible. -

Statement of Outcomes of the 6Th Africa Initiative Meeting 1St March 2019, Kigali, Rwanda

Statement of outcomes of the 6th Africa Initiative meeting 1st March 2019, Kigali, Rwanda 1. On 28 February – 1st March 2019, 68 delegates from 22 African countries and 11 Africa Initiative partners came together in Kigali, Rwanda, for the 6th meeting of the Africa Initiative (see annex 1). 2. The Africa Initiative was launched for a period of three years by the OECD hosted Global Forum in 2014 along with its African members and development partners (see annex 2). The Initiative aims to ensure that African countries can realise the full potential of progress made by the global community in implementing tax transparency and in international tax cooperation. With encouraging first results, its mandate was renewed for a further period of three years (2018-2020) in Yaoundé in November 2017. Countries participating in the Africa Initiative have committed to meeting specific and measurable targets in implementing and using the international tax transparency standards. 3. The delegates welcomed the attendance and support of the Economic Community of West African States (ECOWAS), the Central Africa Monetary and Economic Community (CEMAC), the East Africa Community (EAC), the Organisation for the harmonisation of business law in Africa (Organisation pour l’Harmonisation en Afrique du Droit des Affaires – OHADA) and the European Union for the first time at an Africa Initiative meeting. 4. Emphasising the increasing political focus on tackling illicit financial flows (IFFs) from Africa, delegates discussed how to convert political attention into tangible deliverables. They acknowledged that enhanced tax transparency is an important part of the solution to fighting tax evasion which in turn is a major component of IFFs. -

Occupational Health Impacts of Climate Change Across Different Climate Zones and Elevations in Sub-Saharan East Africa

Vol. 15(6), pp. 243-251, June 2021 DOI: 10.5897/AJEST2021.2976 Article Number: 71E736F67065 ISSN: 1996-0786 Copyright ©2021 African Journal of Environmental Science and Author(s) retain the copyright of this article http://www.academicjournals.org/AJEST Technology Full Length Research Paper Occupational health impacts of climate change across different climate zones and elevations in sub-Saharan East Africa Samuel Kruse1*, Odilichi Ezenwanne2, Matthias Otto3, Tord Kjellstrom4, Patrick Remington5, Bruno Lemke3, Belay Simane6 and Jonathan A Patz7 1Department of Computer Sciences, School of Computer, Data & Information Sciences, University of Wisconsin - Madison, United States. 2Aaron E. Henry Community Health Services Center Inc. United States. 3Nelson Marlborough Institute of Technology, New Zealand. 4Health and Environment International Trust, New Zealand. 5School of Medicine and Public Health, University of Wisconsin - Madison, United States. 6Center for Environment and Sustainable Development College of Development Studies Addis Ababa University, Ethiopia. 7Global Health Institute of University of Wisconsin-Madison, United States. Received 3 January, 2021; Accepted 25 May, 2021 Climate change will cause Sub-Saharan tropical countries to experience a disproportionate increase in the number of extremely hot days when compared to Western countries with more temperate climates. We use the High Occupational Temperature Health and Productivity Suppression (HOTHAPS) model to estimate the potential impact of rising temperatures on worker productivity in different climate regions within Ethiopia, Uganda, Rwanda, and Kenya under varying future climate change scenarios. Using population data obtained from the International Labor Organization, we also estimate productivity losses at a country-wide level. We project large inter-country and intra-country disparities in productivity losses due to varying climatic conditions and local geography.