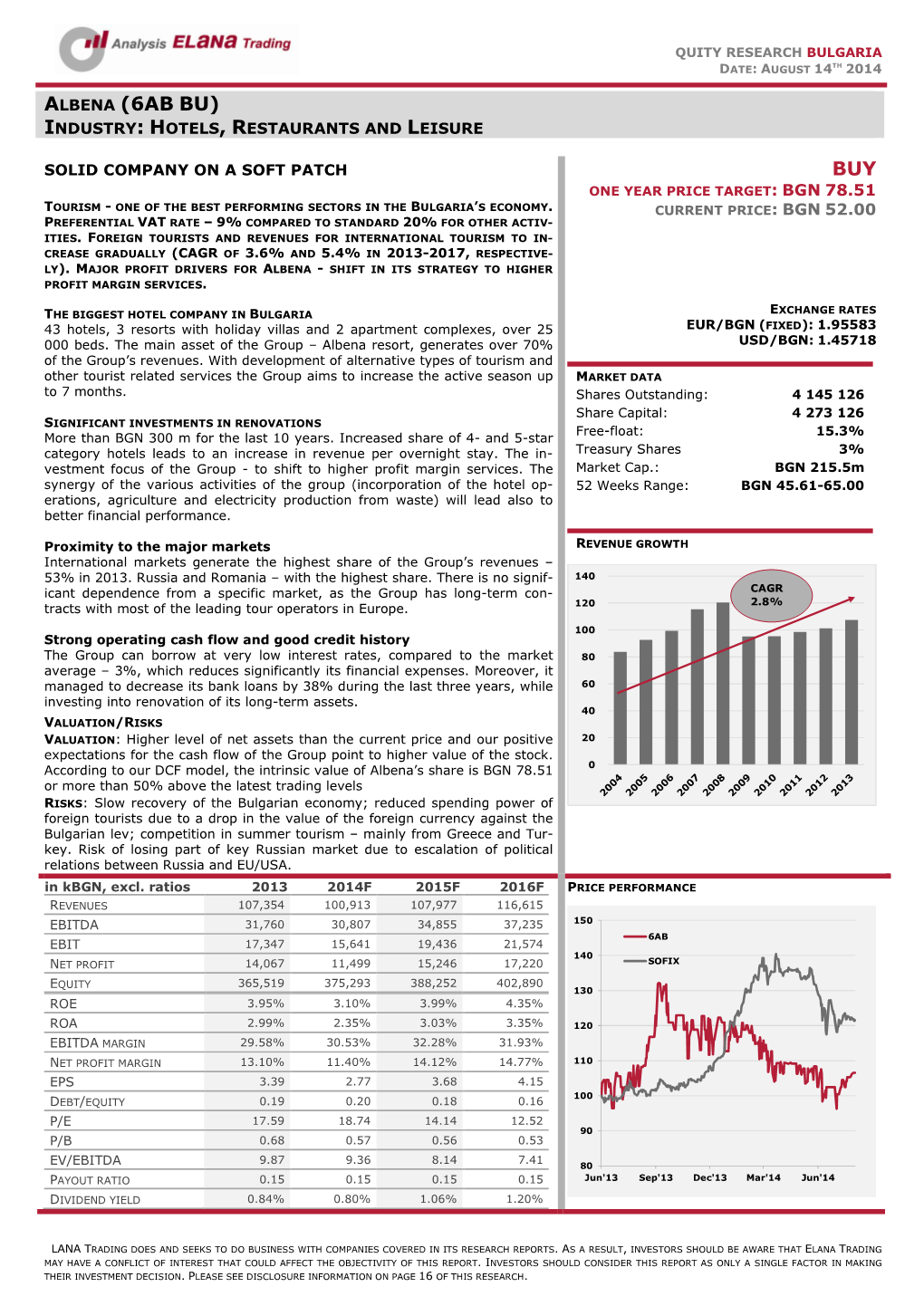

Albena (6Ab Bu) Industry: Hotels, Restaurants and Leisure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

5 Dendrological Diversity in Santa Marina Holiday Village

Silva Balcanica, 19(1)/2018 DENDROLOGICAL DIVERSITY IN SANTA MARINA HOLIDAY VILLAGE - SOZOPOL AS AN EXAMPLE OF CONTEMPORARY LANDSCAPE DESIGN TRENDS IN BULGARIA Svetlana Anisimova Faculty of Ecology and Landscape Architecture, University of Forestry – Sofia Abstract The paper presents dendrofloral characteristics of Santa Marina Holiday Village, situated on the Southern Bulgarian Black Sea coast. The systematic structure and species composition of woody ornamentals, the absolute and relative quantitative participation of each species were analyzed. A total number of 227 woody species, 315 species and intraspecific taxa, respectively of 110 genera, belonging to 54 families, were recorded. Furthermore, 44.4% of the families were represented by only one species. The results indicate a significant tree and shrub diversity, competitive with the one displayed in some Bulgarian historical parks famous for their dendrological collections. Some of them have been rarely cultivated in the green spaces in Bulgaria so far. A trend of a large scale use of alien species and cultivars was established. Consequently, the participation of autochthonous species is insignificant (5.9%). A relatively high percentage of coniferous and evergreen woody species provides the constant ornamental effect of the holiday village green spaces. Key words: urban green spaces, alien species, woody ornamentals, landscape planning INTRODUCTION The ornamental tree and shrub vegetation plays a leading role in the landscape design, creating the volume-spatial composition and enhancing environmental aesthetics and expressiveness. All ecosystem services provided by woody species depend on their adaptability to extreme environmental conditions (Chen, Jim 2008). In recent years, the diversity of ornamental tree and shrub species and cultivated varieties has grown considerably (Knapp, 2010; Chalker-Scott 2015; Sjöman et al., 2016.). -

66 FOLKLORICA 2013, Vol. XVII Mythological Thinking and Archetypes in the Contemporary Bulgarian Nestinarski Ritual Complex

66 Mythological Thinking and Archetypes in the Contemporary Bulgarian Nestinarski Ritual Complex Ana Stefanova Institute of Ethnology and Folklore Studies and Ethnographic Museum (IEFSEM) Bulgaria, Sofia Photographer: Svetlan Stefanov, Bulgaria Abstract The paper examines mythological thinking in the contemporary performance of the ancient ritual complex of nestinarstvo in Bulgaria. As the folk tradition is transformed into freshly “invented” forms in the village of Stomanevo, it has been influenced by “external” factors such as individual cultural elements as well as by globalization, in particular easy access to information and the flow of esoteric literature into Bulgaria in the aftermath of communism. The rite is further molded by distinct psychological factors that constitute fundamental and dynamic conditions necessary for the tradition to be preserved and to evolve. This ritual is a living example of a community phenomenon with roots in the collective unconscious and based on archetypal structure. While its “outer” traits may vary, the “core” remains the same, representing a mosaic of universal values anchored in space and time. The paper examines mythological thinking in a contemporary performance of the ancient ritual complex of nestinarstvo in Bulgaria. (1) As the old tradition has been transformed into newly “invented” forms (2), it has been influenced by “external” factors such as individual cultural elements and globalization, represented by easy access to information and the flow of esoteric literature into Bulgaria in the aftermath of the fall of communism. These trends are further molded by distinct internal psychological determinants, which make up basic dynamic conditions required for a tradition to persist and to evolve. -

Research, Development and Education in Tourism

Research, Development and Education in Tourism Research, Development and Education in Tourism Edited by Sonia Mileva and Nikolina Popova Research, Development and Education in Tourism Edited by Sonia Mileva and Nikolina Popova This book first published 2019 Cambridge Scholars Publishing Lady Stephenson Library, Newcastle upon Tyne, NE6 2PA, UK British Library Cataloguing in Publication Data A catalogue record for this book is available from the British Library Copyright © 2019 by Sonia Mileva, Nikolina Popova and contributors All rights for this book reserved. No part of this book may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the copyright owner. ISBN (10): 1-5275-3719-6 ISBN (13): 978-1-5275-3719-4 TABLE OF CONTENTS Introduction ................................................................................................ 1 Chapter One ................................................................................................ 4 Climate Change and Tourism Adaptation in Bulgaria Maria Vodenska Chapter Two ............................................................................................. 28 Formation of Tourism Policy in Lithuania: Challenges for Image Creation Vita Juknevičienė, Andželika Gumuliauskienė And Rita Toleikienė Chapter Three ........................................................................................... 44 Global and Local Challenges to Plovdiv Destination -

Maritime Spatial Plan for the Cross-Border Area Mangalia

Marine spatial plan for the cross-border area Mangalia Shabla Current situation analysis EUROPEAN COMMISSION Executive Agency for Small and Medium-sized Enterprises (EASME) Department A - COSME, H2020 SME and EMFF Unit A3 - EMFF Call reference No: MARE/2014/22 Project Full Name: Cross border maritime spatial planning in the Black Sea – Romania and Bulgaria (MARSPLAN – BS) Project No: EASME/EMFF/2014/1.2.1.5/2/SI2.707672 MSP LOT 1 /BLACK SEA/MARSPLAN-BS European Maritime and Fisheries Fund (EMFF) Marine spatial plan for the cross-border area Mangalia Shabla Volume 1 Current situation analysis - topic paper DELIVRABLE Page 1 Marine spatial plan for the cross-border area Mangalia Shabla Current situation analysis 1. Introduction to specific problems of the area The marine spatial plan for Mangalia-Shabla area was conceived as a pilot project included in MATSPLAN -BS project in order to test the capacities of the two countries to develop and adopt a concrete instrument for the management of the marine area. This plan takes into consideration the existing data describing the processes of the natural marine areas as well as the human activities developed in this area in order to establish balance between human actions and ecosystems subsistence. The plan is meant also to to put into practice the EU Directive for MSP, creating an institutional framework for MSP implementation in Romania and Bulgaria, enhancing the cross-border cooperation and exchange of information between the two countries. 1.1 Plan area delimitation The spatial plan area is located at the border between Romania and Bulgaria, its delimitation took into consideration two types of zones: the territorial waters (the management area) and coastal area and EEZ (the extended analyse area for the study of interactions). -

Transformations of Rural Areas in Poland and Bulgaria a Case Study

POLSKA AKADEMIA NAUK INSTYTUT GEOGRAFII i PRZESTRZENNEGO ZAGOSPODAROWANIA im. Stanisława Leszczyckiego DOKUMENTACJA GEOGRAFICZNA nr 27 TRANSFORMATIONS OF RURAL AREAS IN POLAND AND BULGARIA A CASE STUDY Editors: BOŻENA GAŁCZYŃSKA MARGARITA ILIEVA WARSZAWA 2002 DOKUMENTACJA GEOGRAFICZNA Komitet Redakcyjny: Krzysztof Błażejczyk (redaktor) Bronisław Górz Andrzej Kowalczyk Teresa Kozłowska-Szczęsna Roman Soja Alojzy Woś Barbara Jaworska (sekretarz) Wydawca: IG i PZ PAN Adres redakcji: 00-818 Warszawa, ul. Twarda 51/55 tel.(48-22) 69 78 851 fax (48-22) 620 62 21 PL-ISSN 0012-5032 ISBN 83-87954-36-5 http://rcin.org.pl POLSKA AKADEMIA NAUK INSTYTUT GEOGRAFII i PRZESTRZENNEGO ZAGOSPODAROWANIA im. Stanisława Leszczyckiego DOKUMENTACJA GEOGRAFICZNA nr 27 TRANSFORMATIONS OF RURAL AREAS IN POLAND AND BULGARIA A CASE STUDY Editors: BOŻENA GAŁCZYŃSKA MARGARITA ILIEVA WARSZAWA 2002 http://rcin.org.pl Recenzent: Prof. dr. hab. Andrzej Stasiak http://rcin.org.pl Table of Contens Introduction Bożena Gałczyńska, Margarita Ilieva 5 Transformation of the rural areas in Poland. The spatial processes and the regional differentiation Bożena Gałczyńska 7 Transformation of the rural areas in Bulgaria (processes, territorial disparities) Margarita Ilieva 21 Transformations in the functional structure of the rural areas in Poland. Selected problems Władysława Stola 35 Problems of rural population in Bulgaria Chavdar Mladenow 51 Changes of Polish agriculture in 1990s and the integration with European Union Roman Kulikowski 59 The underdeveloped rural regions - an -

Contaminants Assessment at the National Level

Contaminants assessment at the national Bulgarian level V. Doncheva, O. Hristova, B. Dzhurova, K. Stefanova, R. Bekova Institute of Oceanology - BAS, Varna, Bulgaria 19 - 20 June 2019, Istanbul, Turkey Overview of the existing contaminants monitoring According to improved monitoring program D8 Assessment areas, Coastal (0-30) monitoring stations network - 37 stations WFD 2000/60/ЕС; - Vromos Bay – to investigate the impact form past radionuclides pollution; - Mussel farms (additional information from own monitoring is required). Shelf (30-200m) - 5 stations at 12 miles zone - Sites for dredging depose (in front of Varna Bay and cape Galata and Burgas Bay) Open Sea (>200m) - At transects Krapets, Galata and Ahtopol 19 - 20 June 2019, Istanbul, Turkey Overview of the existing contaminants monitoring Monitoring program for D9 Assessment areas, Coastal (0-30) in front of 6 “hot spots” monitoring stations network - Varna Bay - Burgas Bay - Krapets (to investigate potential transboundary influence from Danube) river - Kamchia river - Vromos Bay - Mussel farms Shelf (30-200m) - in front of Krapets at 12 miles zone - Sites for dredging depot (in front of Varna Bay and cape Galata and Burgas Bay) Open Sea (>200m) - At transects Krapets, Galata and Ahtopol 19 - 20 June 2019, Istanbul, Turkey Overview of the existing contaminants monitoring Assessment species FISH Other seafood - Sprattus sprattus sulinus - Rapana venosa - Engraulis encrasicholus ponticus - Mytilus galloprovincialis - Trachurus mediterraneus ponticus - Sarda sarda - Belone belone - Scophthalmus maeoticus - Merlangius merlangus euxinus - Squalus acanthias - Neogobius melanostomus 19 - 20 June 2019, Istanbul, Turkey Overview of the existing contaminants monitoring Parameters and Frequency ❑ priority substances in waters: monthly (12 times per year), annually throughout the six-year cycle of implementation of Art. -

Varna, Bulgaria 03.07.2018 – 08.07.2018

INTERNATIONAL FOLK DANCE FESTIVAL “VARNA 2018” – Varna, Bulgaria 03.07.2018 – 08.07.2018 Organizers: MUNICIPALITY OF VARNA FOLKLORE FESTIVAL ASSOCIATION (MAKFOLK & TALIJA Art Co.) The International Folk Dance Festival “Varna 2018” will be held for the 13th time in Varna, Bulgaria from 3rd of July till 8th of July 2018. Varna – the Sea Capital of Bulgaria! Apart from being a beach resort, Varna rivals the great cities of Sofia and Plovdiv, in its offering of cultural attractions and historical buildings, museums and art galleries. Today Varna is the largest city on Bulgaria's Black Sea coast and is the main port for both naval and commercial ship ping. Because it is a close neighbor to the popular coastal resorts of Golden Sands, St. Constantine & Helena, and Albena, Varna has a cosmopolitan atmosphere. Varna is also the host city of numerous prestigious cultural events. Dolphinaruim It is the only dolphinarium on the Balkan Peninsula and it is one of the greatest attractions that Varna can offer to its guests. The show lasts 40 minutes. The visitors will enjoy the incredible intelligence and playfulness of the sea mammals. A curious fact is that in 1992 a baby-dolphin was born in the Dolphinarium in Varna. The event was a sign that the animals feel at home in their surrounding. FESTIVAL CONDITIONS: The International folk dance festival “Varna 2018” is a non-competitive sample of traditional and modern dances and music performed by folkloric groups. On the festival may participate children and youth folklore dance groups, vocal groups, instrumental groups, as well as groups and performers from other art styles with minimum 10 persons on the stage. -

Short Term EVS: Not Just History

ERASMUS + K1: Youth mobility Short-term EVS + training course Short term EVS: Not just History Topic: new skills and knowledge in a field of archeological activities WHEN: 01.09. - 15.10.2014 WHERE: Bulgaria, Veliki Preslav - second capital of Bulgaria In archeological complex old capital Preslav and Archeological museum http://en.wikipedia.org/wiki/Preslav http://www.museum-preslav.com/ PARTICOPANTS: 28 youth (17-29 years old) - 7 countries x 4 people Spain, Hungary, Latvia, Italy, Azerbaijan, Georgia, Turkey and of course Bulgarian team that will work with you PROFILE of 4 youth per country; participants: Working language – English (or 1 of participants have to know English very good); Unemployment youth people, from poor and distance area; 1 of participants may to be person that study Archeology or History; Without experience in youth programs What will you learn in the frame of the project? 1. Specifics for the profession of archaeologists and working in an archeological area: - How to hunt different archaeological sites (movable and immovable); - How to prepare and implement plans (regular) and rescue excavations or underwater research; - How to make a scientific treatment of excavated monuments; - How to use and prepare scientific and reference documentation; - How to work with instrumentation - line calipers, scales, etc..; - In conducting excavations - how to work with different maps, geophysical and building tools, cameras, packaging materials; - How to preserve and store objects and artifacts; - Work in a team or independently. 2. Facts and information about the history of the Balkans and Europe: - Information about material and spiritual culture of the people of the past; - Reconstruct the history of the continent of Europe in ancient times. -

Bulgarian Society of Cardiology

www.cardiobg.com www.12cardiocongress.com Bulgarian Society of Cardiology Bulgarian Society of Cardiology Organizer of the Congress Dear Colleagues, On behalf of the Organizing Committee and myself I am honored to invite you to participate in the XII National Congress of Bulgarian Society of Cardiology Cardiology, which will take place on 7 – 10th www.cardiobg.com October 2010 in Albena Resort, Varna, Bulgaria. The program of the Congress will cover President – Assoc. Prof. Vladimir Pilossoff different plenary sessions presenting innovative Bulgarian scientific achievements, Scientific Secretary – Assoc. Prof. Elina Trendafilova as well as poster sessions. Elected President – Prof. Asen Goudev 65, Konjovitza Str., Sofia 1309 The pharmaceutical industry will be able to market their products at the industry focused e-mail: [email protected] symposia and at the Exhibition which will be an essential aspect of the Cogress. The National Congress of Cardiology is one of the key events on the scientific calendar in Bulgaria bringing together more than 1300 participants from all over the country and eminent foreign specialists. For the first time this year the program Congress Manager of the Congress will include joint session between the European and Bulgarian Societies of Cardiology. Leading international lecturers are invited. The main topics are Acute Coronary Syndrome and Heart Failure. Additional information could be found at the web site of the Congress http://www.12cardiocongress.com Company for International Meetings Ltd. /CIM/ We look forward to welcome you! www.cim.bg Assoc. Prof. Vladimir Pilossoff President of the Bulgarian Society of Cardiology Sofia 1000, 18, Christo Belchev Str. tel. + 359 2 987 74 22 ; fax: + 359 2 980 60 74 е-mail: [email protected] Tzvetana Pankova e-mail: [email protected] Bulgarian Society of Cardiology Bulgarian Society of Cardiology Bulgarian Society of Cardiology Bulgarian Society of Cardiology Organizing Committee Scientific Program Plenary Sessions Chairperson: Poster Sessions Assoc. -

Landslide Hazard Assessment of Bulgarian Black Sea Coast

Landslide Hazard Assessment of Bulgarian Black Sea Coast Valentin Nenov, Husein Jemendjiev, Nikolay Dobrev Burgas University Bulgaria Engineering geological regions in Bulgaria largest LS areas Danube river Bank, Northern Black sea coast, Rodopi mountain Representative profiles of landslides in the territory of Bulgaria Geological structure 1 – loess complex (еоlQp); 2 – limestones of the Karvuna Formation (kvN1s); 3 – aragonite clays with limestone intercalations, Topola Formation (toN1s); 4 – limestones with sand intercalations, Odar Formation (odN1s); 5 – sands, Frangen Formation (frN1s); 6 – diatomaceous clays of the Euxinograd Formation (evN1kg-s); 7 – delapsium; 8 – oldest landslide scarp. Bulgarian Black Sea coast LS • The territory of the Bulgarian Black Sea coast is highly hazardous in respect of LS • In areas along the Black Sea coast more than 120 landslides are active • Most are active landslides in the northern Black Sea coast of Varna to Kavarna (between the resorts of St. St. Constantine and Elena, Zlatni Pyasatsi, Albena, and the Balchik area). • The depth of the main slip surface is usually up to 50-60 m or more (reaching 100 m at some places). Landslide distribution on the Bulgarian Black Sea coast: 1 - landslide zone ; 2 - separate landslide; 3 - landslides triggered in 1996; 4 - landslides triggered in 1997 South Black sea coast examples North Black sea coast Mora & Vahrson Landslide Hazard Assessment Intrinsic Landslide Susceptibility (Susceptibility Indicator: SUSC) Slope Factor Sr : Relative Relief representing the -

Good Practice from Bulgaria

Perpetuum Mobile Albena: Co-digestion of kitchen and agricultural waste Nikolay Sidjimov BAMEE Webinar, Biogas from organic wastes, 15 May 2020 Bulgaria – bio-waste treatment • 50-60% of municipal solid waste is biodegradable municipal waste • In 1995: 2.24 million tons • In 2007: 1,4 million tons (62% of 1995 value) Bio-waste landfill diversion targets: • 2010: 75% • 2013: 50% • 2020: 35% 2 Bulgaria - targets achieved! ▪ 2020 target of 35% achieved in 2016 ▪ OP 2007-2013 ▪ 18 composting plants ▪ 1 anaerobic digestion plant ▪ OP 2014-2020 ▪ 35 composting plants ▪ 3 anaerobic digestion plants ▪ 19 plant for preliminary treatment 3 The Black Sea Resort Albena ▪ Located 30km from Varna and 12km from Balchik ▪ 43 hotels with a total of 20,000 beds ▪ Green Oscar for contribution to environment ▪ Investment in energy efficiency, renewable energy, recycling and waste reduction ▪ In Eco Agro complex, production of own fresh food, including beef from cattle farm and organic wine 4 The Perpetuum Mobile plant 5 The Perpetuum Mobile plant • The Albena daughter company “Perpetuum mobile BG” AD operates the biogas plant • Construction of anaerobic digester for agricultural and kitchen wastes from Albena Resort in 2012 • New installation currently under construction • Co-generation of electricity and heat from biomass • Heat (1MWh) is used for a greenhouse (and district heating) • Digested materials used as liquid fertilizer on agricultural fields of the company and parks & gardens of the resort • Electricity production (1MWe) directly to the grid 6 7 Key challenges • At the beginning, problems using kitchen waste and started using just agricultural residues • Team improves technical processes to use both types of waste but still mainly agricultural • The bacterial flora is very sensible to many external factors: temperature and pH • Process, speed and results depend also on size of the input organic materials, length of stay, good contact of organic material and bacteria • For the better digestion, the inlet material is screened; flotation method is used to separate fats. -

BULGARIA, Friday 4Rd June to Friday 17Th June 2010

Visit to BULGARIA, Friday 4rd June to Friday 17th June 2010. Albena Coastal, the Eastern Rhodopes and Sakar Mountains, and the northern coastal lakes of Shabla and Durankulak, and Cape Kaliakra. Brian & Isabel Eady. It was way back in July 1997 that we made our first visit to Bulgaria. We were not into birding then, but both remember commenting on the number of birds about. Since then, we caught the birding bug, and decided it was time to revisit. We spoke to Dimiter Georgiev, Managing Director and tour leader for Neophron Tours whilst on our visit to the Bird Fair last year 2009, and we were very pleased that his company actually did one and two day birding tours. Inter-mixed with local birding, which we could undertake ourselves around the locality where we would be staying, fitted our criteria perfectly. Our research showed that the two periods which were ideal for Bulgarian birding were, either the autumn, around September time, and the Spring, May to June. As we were also contemplating a holiday in January 2011 to somewhere in climes as yet unknown, which option to choose, was quite easy, so we opted for a spring visit. Researching on the Internet, Travelling Birder.com turned up quite a few reports which were quite encouraging, especially one written by Trond Haugskott who visited Albena on the Black Sea coast between 3rd and 17th June 2005. This happened to be the same time that we were expecting to visit. During his visit, which was a family holiday, he found a good number of species, and that was basically around the Albena area, with a few other trips thrown in, notably Srebarna, Durankulak, Shabla, and Cape Kaliakra.