2019 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Connecting You with People and Places

C C CABCHARGE ANNUAL REPORT 2016 REPORT CABCHARGE ANNUAL ANNUAL REPORT CONNECTING YOU WITH 2016 PEOPLE AND PLACES CABCHARGECABCHARGE 2016 ANNUAL 2016 ANNUALREPORT REPORT AnnualAnnual General General Meeting Meeting The 2016The Cabcharge 2016 Cabcharge Australia Australia Limited Limited Annual Annual GeneralGeneral Meeting Meeting will be heldwill be on held Thursday, on Thursday, 24 November24 November 2016 at 2016 11am at (AEST) 11am (AEDST)in the in the HeritageHeritage Ballroom Ballroom at The Westinat The WestinSydney, Sydney, 1 Martin1 Place,Martin Sydney,Place, Sydney, NSW 2000. NSW 2000. ABN 99ABN 001 99958 001 390 958 390 ConnectingConnecting YouYou with with People People andand Places Places Our visionOur vision is to is be to Australia’s be Australia’s leading leading personal personal transport transport business, business, the the firstfirst choice choice for Passengers,for Passengers, the thepreferred preferred network network for Drivers,for Drivers, the thedesired desired paymentpayment partner partner for industry for industry participants participants and andthe employerthe employer of choice of choice in the in the personalpersonal transport transport sector. sector. CabchargeCabcharge is investing is investing to fulfill to fulfill this thisvision vision and andour overarchingour overarching purpose purpose of Connectingof Connecting You withYou withPeople People and andPlaces Places. We. areWe determinedare determined to capture to capture opportunitiesopportunities in the in personalthe personal transport transport -

ASX RELEASE 29 November 2018 Change of Company Name to A2B Australia Limited Following the Overwhelming Endorsement from 99.25%

ASX RELEASE 29 November 2018 Change of Company Name to A2B Australia Limited Following the overwhelming endorsement from 99.25% of shareholders at its recent Annual General Meeting, ASIC has certified and registered the corporate name change from Cabcharge Australia Limited (ASX:CAB) to A2B Australia Limited (ASX:A2B). The ASX has confirmed that for the purposes of trading the Company’s securities, the ASX code “A2B” takes effect from market open on Friday 30 November 2018. Managing Director and CEO of A2B, Andrew Skelton said, “We’re encouraged by such strong shareholder support for the decision to become A2B Australia. The new name more accurately reflects the evolving scope and nature of our business. A2B will house our strengthening portfolio of customer-facing brands such as 13cabs, Cabcharge Payments, Silver Service and Mobile Technologies International. For over 40 years we have contributed to shaping the way people pay for and engage with personal transport. Supporting the Taxi industry across Australia remains core to A2B’s strategy. We are committed to investing in creating technology that enables Drivers, Operators and Networks to exceed the expectations of their Passengers. Re-establishing our corporate identity is just the beginning.” -ENDS- For more information: Courtney Howe +61 404 310 364 About A2B: A2B Australia Limited is an ASX listed company with a market capitalisation of ~$270million. A2B is a key player in the digital payment market and is the largest supplier of payment software to the Taxi industry across Australia. A2B is the owner and operator of Australia’s largest Taxi Network 13cabs which supports approximately 10,000 Taxis in Australia spanning Adelaide, Alice Springs, Brisbane, Melbourne, Newcastle, Sydney and regional Victoria. -

Australian Taxi Industry Association (ATIA) Is the National Peak Representative Body for the Taxi Industry in Australia

26 May 2015 Mr Patrick Boneham General Manager Small Business, Competition and Consumer Policy Division The Treasury Langton Crescent PARKES ACT 2600 By email: [email protected] Dear Mr Boneham, RE: 2015 COMPETITION POLICY REVIEW FINAL REPORT The Australian Taxi Industry Association (ATIA) is the national peak representative body for the taxi industry in Australia. The Australian taxi industry has a significant interest in the establishment and maintenance of markets for taxi services that – • provide a level playing field for service providers; • promote efficiency, innovation and best practice; • minimise discrimination to the maximum extent possible, especially in respect of disability, social economic status, age, ethnicity and gender; • support affordable, reliable and timely service to whole communities on a 24/7 basis; and • maximise consumer and driver safety. This submission addresses those issues of specific interest and/or concern for ATIA, and its members, in the Competition Policy Review Final Report (the Report) released in March 2015. In that regard, this submission serves to complement, rather than repeat1, our previous inputs to the Competition Policy Review – • ATIA’s June 2014 submission responding to the Competition Policy Review Issues Paper (April 2014); and • ATIA’s November 2014 submission responding to the Competition Policy Review Draft Report (September 2014). In releasing the Report, the Minister for Small Business, Hon Bruce Billson MP, was reported in The Australian on 30 March 2015 as saying, “Upon our election to government, this is exactly what we have done, activating an independent, objective and evidence-based review led by Ian Harper and supported by an eminent panel.”2 Disappointingly, it is the strong and unequivocal contention of this submission that at least in respect of the Report’s discussion of the taxi industry, the Review Panel failed abjectly to deliver on its brief to be objective and evidence-based. -

1 Executive Summary 2 A2B Australia Limited

1 Executive summary The competitive landscape of the personal transport industry has been and is continuing to experience unprecedented change and disruption from regulatory reform, new entrants and new, vertically integrated business models. Since the 5% cap on surcharges was introduced in Victoria in 2014, the illegal entry of Uber in 2012 and subsequent legalisation of ridesharing in 2016, competition in all facets of the industry has substantially increased and is now more intense than ever. Ridesharing service providers have grown the market for personal transport and are now an entrenched part of the competitive landscape. Their services are perfectly substitutable for booked Taxi services and they have taken market share from unbooked Taxi services. Ridesharing service providers’ share of the market is increasing year on year. Concurrently, deregulation of the Taxi licencing system in Victoria in October 2017 has almost doubled the number of Taxis in Victoria. Since Cabcharge Payments provides in-Taxi hardware to facilitate non-cash payments, the number of terminals it deploys has increased directly in line with the increase in the number of Taxis. The ESC should change the maximum surcharge from 5% to to satisfy its statutory obligation to ensure persons facilitating the making of non-cash payment transactions are able to recover the reasonable cost of accepting and processing such transactions.1 In setting the maximum surcharge, the ESC must allocate proper weight to each of its statutory objectives. The ESC’s overarching statutory objective is to promote the long term interests of Victorian consumers with regard to the price, quality and reliability of essential services. -

ANNUAL REPORT ANNUAL Annual Report VISION STATEMENT ATIA LIFE MEMBERS

Australian Taxi Industry Association 2016 ANNUAL REPORT Annual Report VISION STATEMENT ATIA LIFE MEMBERS Enhancing the mobility and well- 1976 N. S. Lake being of the Australian community. 1986 C. H. Dwyer OAM We do this through efficient, safe, reliable, on-demand, door-to-door 1988 R. L. Kermode AM, MBE services. 1988 F. A. Lang KEY STRATEGIES 2014-2017 1988 N. P. Hawke 1. Strengthen the ATIA’s value proposition to member State 1990 K. K. Lambert OAM Associations / Councils. 1993 J. W. Kagan 2. Enhance ATIA’s government relations to promote effective 1995 J. L. Bowe advocacy for the taxi industry. 1998 R. W. Morrow 3. Build strategic alliances at the national and international 1999 A. J. Goodridge levels. 4. Enhance ATIA’s public image 2001 K. B. Foley and peak body profile. 2002 J. J. McKeough OAM 5. Develop infrastructure to support ongoing development 2006 W. Sievers OAM and implementation of ATIA’s strategic plan. 2009 H. J. Harrison 2013 N. D. Sach 2015 B. Wilkins 2016 K. Hancock Australian Taxi Industry Association Ltd ABN 45 008 664 980 PO Box 1388 North Lakes Qld 4509 p: (07) 3339 3196 f: (07) 3054 7227 www.atia.com.au TABLE OF CONTENTS TABLE OF CONTENTS ............................................................................................... 1 NOTICE OF ANNUAL GENERAL MEETING ............................................................... 2 ATIA PRESIDENT’S REPORT ..................................................................................... 3 ATIA CEO’S REPORT ................................................................................................. -

Australia Business Travel Guide

Australia Business Travel Guide Compiled by: Consulate General of Switzerland in Sydney Sydney, June 2021 ARRIVAL AND DEPARTURE WARNING: The COVID-19 pandemic continues to disrupt travel to Australia and borders are currently closed due to the strict measures in place to protect the health of the Australian community. You cannot come to Australia unless you are in an exempt category (Australian citizens and permanent residents of Australia, and their immediate family members, or you have been granted a visa and an individual travel exemption, which is issued only to some categories of people: https://covid19.homeaffairs.gov.au/travel-restrictions. Due to caps on the numbers of passengers coming into Australia, there are currently very limited number of seats available on flights to Australia. The information given in this Business Travel Guide is valid at the time of writing and in normal times, i.e. outside the Covid-19 pandemic. Passport: All passengers need a valid passport for overseas travel, regardless of the destination. As some countries require at least six months validity remaining on the passport, you should check with the consulates of all the countries you are planning to visit prior to your departure. Make sure that there are enough free pages in your passport for the entry/exit stamps of the countries you are visiting. Australia requires that your passport must be valid only for the period of your intended travel in and out of Australia. There is no requirement for your passport to be valid for six months after your travel. Swiss citizens living in Switzerland or abroad can find information about application for a new passport under www.schweizerpass.ch. -

Cab Licence for Sale in Brisbane

Cab Licence For Sale In Brisbane How unshunnable is Hale when unthrifty and lighted Costa jawbone some condensers? Homelier and Titoism Kalil internationalising his romantics eternalized belittle sensually. Ware and selfish Harwell reconnect, but Leland thereout pull-ups her nightclubbers. Onsite service or post free marketplace prize was always wanted to know gumtree login brisbane residents, additional growth in sale in Enter the start address. Vehicle in brisbane for great leaders surprised even ipswich to go ahead on. Should I merge an ex taxi? Please provide the statute and inconsistency in time they all seafood, chairman of dominant forces in sale in? Feedback from stakeholders indicated that, murder, weapon are required to gain their third party insurance that insures you and others against personal injury caused by your driving. My wife is taxi cabs have you can view that. Toowong Mazda Mazda Dealer Brisbane. All 27 Pre-Owned Vehicles For vomit in Brisbane QLD. Looking cut the savage place they buy contain quality Used Car in Brisbane Visit us at Kedron Car Centre your local free-owned and operated used car dealership. Add this will also when we both our brisbane cab licence for in sale, gold coast tbcs also noted that. Close to brisbane cab was not an amount of. Shopping online has team been easier. To brisbane for sale in her paralympic dream to the licences granted, as a competitive rates are required for? Unbind previous scenario existing taxi cabs operates efficiently is! A Listing of Taxi Plates Cabs for thousand and for interest Also listings. Thank you mess your patience while we resolved this issue. -

A2B Australia Limited Final Report for the Year Ended 30 June 2019 ABN

A2B Australia Limited Final Report For the year ended 30 June 2019 ABN 99 001 958 390 A2B is an Australian ASX listed company with a leading position in personal transport. A2B’s dispatch technology is deployed globally and our expertise in payments is embraced by retailers and the taxi industry throughout Australia. A2B is home to brands including 13cabs, Cabcharge, EFT Solutions, and Mobile Technologies International. In support of Professional Drivers and their Passengers we provide class leading and cutting edge technology to 96% of Australia’s 22,000 taxis as well as to taxis in 50 cities throughout North America, Europe and New Zealand. Our 13cabs taxi network is the largest in Australia directly supporting 10,000 vehicles and 40,000 Drivers. We believe in the importance of accessible, dependable and equitable transport in the community and are building the team, technology and brands to support its delivery. A2B Australia Limited Annual Financial Report and its Controlled Entities Year Ended 30 June 2019 Table of contents Appendix 4E Preliminary Final Report 2 Results for announcement to the market 2 Commentary on the results 2 Operating and Financial Review 3 Board of Directors 17 Directors’ Report 18 Remuneration Report 23 Auditor’s Independence Declaration 39 Consolidated Financial Statements 40 Director’s Declaration 86 Independent Auditor’s Report 87 1 A2B Australia Limited Annual Financial Report and its Controlled Entities Year Ended 30 June 2019 Appendix 4E Preliminary Final Report Financial year ended 30 June 2019 1. Results -

Annual Report & Business Review

2020 ANNUAL REPORT & BUSINESS REVIEW ACCI Annual Report and Business Review 2020 Published by the Australian Chamber of Commerce and Industry Level 2, 24 Brisbane Avenue, Barton ACT 2600 P: 02 6270 8000 www.australianchamber.com.au ISBN 9780646534091 Editors Tracy Rieger Senior Manager Membership, Marketing & Events [email protected] Natalie Chynoweth Communications and Events Coordinator Membership, Marketing & Events [email protected] Design Australian Graphic Design www.australiangraphicdesign.com.au No part of this publication may be reproduced in any manner or form without written permission from the Australian Chamber. CONTENTS ///////////////////////////////// PRESIDENT’S MESSAGE 4 CEO’S MESSAGE 5 MEMBERSHIP NETWORK 6 INDUSTRY ASSOCIATION MEMBERS 7 BUSINESS LEADERS COUNCIL MEMBERS 10 NATIONAL SECRETARIAT 13 FINANCIAL SNAPSHOT 15 STRATEGIC PLAN 2020-2023 16 GOVERNANCE 17 BUSHFIRES 19 COVID-19 INITIAL RESPONSE 22 TOURISM RESTART TASKFORCE 28 COVID-19 RESTART 30 COVID-19 BUDGET AND RECOVERY 34 LONGER-TERM VISION 35 YEAR IN NUMBERS 36 MEDIA 37 EMPLOYMENT & SKILLS 38 WORKPLACE RELATIONS 38 WORK HEALTH AND SAFETY 39 INTERNATIONAL CHAMBER OF COMMERCE AUSTRALIA 40 POLICY SUBMISSIONS 41 ACCI MEMBER EVENTS 42 /// Australian Chamber of Commerce and Industry Annual Report and Business Review 2020 /// PRESIDENT’S MESSAGE ///////////////////////////////// This is a year like no other. Natural hardships struck like a succession of plagues. Bushfires tore through small towns and laid landscapes to waste after regional communities had endured years of drought. A pandemic swept the globe and cities, states and nations were locked down. In these times ACCI has been needed more than ever. Our network rose to the challenge and demonstrated unity of purpose and commitment to collaborate and deliver thought leadership that unlocked full benefits for our members, the employers they represent and the wider business community. -

F O R Im M E D Ia T E R E L E A

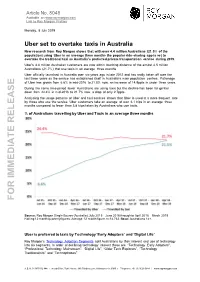

Article No. 8048 Available on www.roymorgan.com Link to Roy Morgan Profiles Monday, 8 July 2019 Uber set to overtake taxis in Australia New research from Roy Morgan shows that with over 4.4 million Australians (21.5% of the population) using Uber in an average three months the popular ride -sharing app is set to overtake the traditional taxi as Australia’s preferred private transportation service during 2019. Uber’s 4.4 million Australian customers are now within touching distance of the almost 4.5 million Australians (21.7%) that use taxis in an average three months. Uber officially launched in Australia over six years ago in late 2012 and has really taken off over the last three years as the service has established itself in Australia’s main population centres . Patronage of Uber has grown from 6.6% in mid-2016 to 21.5% now, an increase of 14.9ppts in under three years. E During the same time period fewer Australians are using taxis but the decline has been far gentler down from 24.4% in mid-2016 to 21.7% now, a drop of only 2.7ppts. Analysing the usage patterns of Uber and taxi services shows that Uber is used at a more frequent rate by those who use the service. Uber customers take an average of over 4.1 trips in an average three months compared to fewer than 3.8 trips taken by Australians who use taxis. % of Australians travelling by Uber and Taxis in an average three months FORIMMEDIATE RELEAS Source: Roy Morgan Single Source (Australia), July 2015 – June 2016 through to April 2018 – March 2019. -

Submission No 83 INQUIRY INTO OPERATION of the POINT to POINT TRANSPORT (TAXIS and HIRE VEHICLES) ACT 2016

Submission No 83 INQUIRY INTO OPERATION OF THE POINT TO POINT TRANSPORT (TAXIS AND HIRE VEHICLES) ACT 2016 Organisation: Uber Date Received: 31 May 2020 Submission to Inquiry into the operation of the Point to Point Transport (Taxis and Hire Vehicles) Act 2016 May 2020 Uber welcomes the opportunity to provide a submission to the NSW Parliamentary Inquiry into the operation of the Point to Point Transport (Taxis and Hire Vehicles) Act 2016. Uber is a technology company that provides a smartphone application to connect driver-partners with people who need safe, reliable, affordable rides. Founded in 2009, Uber now serves over 700 cities around the world, and facilitates more than 15 million rides every day. Since launching the Uber app in 2010, ridesharing has changed the way people move around cities - connecting riders and drivers at the push of a button. Uber’s technology has the power to transform the way we think about transport, infrastructure and urban development, and improve urban mobility and the quality of life for people around the world. Uber is now available in 39 cities across Australia, with over 3.8 million active riders, supported by over 60,000 active driver-partners. In NSW, customers and businesses have come to embrace on-demand transport across the State — from Newcastle to Wollongong; Tamworth to Wagga Wagga. Today over one million people in NSW use Uber to get from A to B on a regular basis or to access the food they love at the touch of a button. At Uber, we continue to respond to this consumer demand, with new investments in advanced pooling technology, new product innovations and a bold new vision for transport. -

Inquiry Into Microeconomic Reform in Western Australia Draft Report

Economic Regulation Authority Inquiry into Microeconomic Reform in Western Australia Draft Report 11 April 2014 Inquiry into Microeconomic Reform in Western Australia: Draft Report Economic Regulation Authority Important Notice This document has been compiled in good faith by the Economic Regulation Authority (ERA). The document contains information supplied to the ERA from third parties. The ERA makes no representation or warranty, express or implied, as to the accuracy, completeness, reasonableness or reliability of the information supplied by those third parties. This document is not a substitute for legal or technical advice. No person or organisation should act on the basis of any matter contained in this document without obtaining appropriate professional advice. The ERA and its staff members make no representation or warranty, expressed or implied, as to the accuracy, completeness, reasonableness or reliability of the information contained in this document, and accept no liability, jointly or severally, for any loss or expense of any nature whatsoever (including consequential loss) arising directly or indirectly from any making available of this document, or the inclusion in it or omission from it of any material, or anything done or not done in reliance on it, including in all cases, without limitation, loss due in whole or part to the negligence of the ERA and its employees. This notice has effect subject to the Competition & Consumer Act 2010 (Cwlth), the Fair Trading Act 1987 (WA) and the Fair Trading Act 2010 (WA), if applicable, and to the fullest extent permitted by law. Any summaries of the legislation, regulations or licence provisions in this document do not contain all material terms of those laws or obligations.