Rating Action: Moody's Upgrades the Holding Company Debt Ratings of Eight European Insurance Groups Following a Change in Methodology

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Premium Thresholds for Equity Options Traded at Euronext Amsterdam Premium Based Tick Size

Premium Based Tick Size Premium thresholds for equity options traded at Euronext Amsterdam Trading Trading Premium Company symbol symbol threshold Underlying American European €0.50 €5.00 1 Aalberts AAI x 2 ABN AMRO Bank ABN x 3 Accell Group ACC x 4 Adidas ADQ x 5 Adyen (contract size 10) ADY x 6 Aegon AGN x 7 Ageas AGA x 8 Ahold Delhaize, koninklijke AH AH9 x 9 Air France-KLM AFA x 10 Akzo Nobel AKZ x 11 Allianz AZQ x 12 Altice Europe ATC x 13 AMG AMG x 14 Aperam AP x 15 Arcadis ARC x 16 ArcelorMittal MT MT9 x 17 ASM International ASM x 18 ASML Holding ASL AS9 x 19 ASR Nederland ASR x 20 BAM Groep, koninklijke BAM x 21 Basf BFQ x 22 Bayer REG BYQ x 23 Bayerische Motoren Werke BWQ x 24 BE Semiconductor Industries BES x 25 BinckBank BCK x 26 Boskalis Westminster, koninklijke BOS x 27 Brunel International BI x 28 Coca-Cola European Partners CCE x 29 CSM CSM x 30 Daimler REGISTERED SHARES DMQ x 31 Deutsche Bank DBQ x 32 Deutsche Lufthansa AG LUQ x 33 Deutsche Post REG DPQ x 34 Deutsche Telekom REG TKQ x 35 DSM, koninklijke DSM x 36 E.ON EOQ x 37 Euronext ENX x 38 Flow Traders FLW x 39 Fresenius SE & CO KGAA FSQ x 40 Fugro FUR x 41 Grandvision GVN x 42 Heijmans HEY x 43 Heineken HEI x 44 IMCD IMD x 45 Infineon Technologies NTQ x 46 ING Groep ING IN9 x 47 Intertrust ITR x 48 K+S KSQ x 49 Kiadis Pharma KDS x 50 Klépierre CIO x 51 KPN, koninklijke KPN x 52 Marel MAR x 53 Muenchener Rueckver REG MRQ x 54 NIBC Holding NIB x 55 NN Group NN x 56 NSI NSI x 57 OCI OCI x 58 Ordina ORD x 59 Pharming Group PHA x 60 Philips Electronics, koninklijke PHI -

Trade Credit Insurance

Trade Credit Insurance Peter M. Jones PRIMER SERIES ON INSURANCE ISSUE 15, FEBRUARY 2010 NON-BANK FINANCIAL INSTITUTIONS GROUP GLOBAL CAPITAL MARKETS DEVELOPMENT DEPARTMENT FINANCIAL AND PRIVATE SECTOR DEVELOPMENT VICE PRESIDENCY www.worldbank.org/nbfi Trade Credit Insurance Peter M. Jones primer series on insurance issue 15, february 2010 non-bank financial institutions group global capital markets development department financial and private sector development vice presidency www.worldbank.org/nbfi ii Risk Based Supervision THIS ISSUE Author Peter M. Jones was the Chief Executive Officer of the African Trade Insurance Agency (ATI) from 1 February, 2006 up until 31 July, 2009 when he retired. During his time as CEO of ATI, Peter successfully implemented a legal and capital restructuring, including the expansion of the Agency’s product offering to ensure that it meets the full needs of the private and public sector in Africa. Prior to joining ATI, Peter held various positions at the Multilateral Investment Guarantee Agency (MIGA). He was also a Vice-President at Export Development Canada (EDC), where he was responsible for all of EDC’s business operations in the Transportation sector, as well as for the establishment, development and management of its equity investment program. This experience, together with his senior positions at the Canadian Imperial Bank of Commerce (CIBC) and ANZ/Grindlays Bank, has provided him with wide ranging skills and experience in identification of viable equity opportunities, including successful exits. Peter is a Fellow of the Institute of Chartered Secretaries and Administrators. Series editor Rodolfo Wehrhahn is a senior insurance specialist at the World Bank. -

Prospectus Dated 23 June 2020

Prospectus dated 23 June 2020 Bupa Finance plc (Incorporated with limited liability in England and Wales with Registered no. 02779134, legal entity identifier ZIMCVQHUFZ8GVHENP290) £350,000,000 4.125 per cent. Fixed Rate Subordinated Notes due 2035 Issue price: 99.383 per cent. The £350,000,000 4.125 per cent. Fixed Rate Subordinated Notes due 2035 (the “Notes”) will be issued by Bupa Finance plc (the “Issuer”) and will be constituted by a trust deed (as amended or supplemented from time to time, the “Trust Deed”) to be dated on or about 25 June 2020 (the “Issue Date”) between the Issuer, and the Trustee (as defined in “Terms and Conditions of the Notes” (the “Conditions”, and references herein to a numbered “Condition” shall be construed accordingly)). Application has been made to the United Kingdom Financial Conduct Authority (the “FCA”) under Part VI of the Financial Services and Markets Act 2000, as amended (the “FSMA”) for the Notes to be admitted to the official list of the FCA (the “Official List”) and to the London Stock Exchange plc (the “London Stock Exchange”) for the Notes to be admitted to trading on the London Stock Exchange’s Regulated Market (the “Market”). References in this Prospectus to the Notes being “listed” (and all related references) shall mean that the Notes have been admitted to the Official List and have been admitted to trading on the Market. The Market is a regulated market for the purposes of Directive 2014/65/EU, as amended (“MIFID II”). This Prospectus has been approved by the FCA, which is the United Kingdom (“UK”) competent authority, under Regulation (EU) 2017/1129 (the “Prospectus Regulation”). -

Part VII Transfers Pursuant to the UK Financial Services and Markets Act 2000

PART VII TRANSFERS EFFECTED PURSUANT TO THE UK FINANCIAL SERVICES AND MARKETS ACT 2000 www.sidley.com/partvii Sidley Austin LLP, London is able to provide legal advice in relation to insurance business transfer schemes under Part VII of the UK Financial Services and Markets Act 2000 (“FSMA”). This service extends to advising upon the applicability of FSMA to particular transfers (including transfers involving insurance business domiciled outside the UK), advising parties to transfers as well as those affected by them including reinsurers, liaising with the FSA and policyholders, and obtaining sanction of the transfer in the English High Court. For more information on Part VII transfers, please contact: Martin Membery at [email protected] or telephone + 44 (0) 20 7360 3614. If you would like details of a Part VII transfer added to this website, please email Martin Membery at the address above. Disclaimer for Part VII Transfers Web Page The information contained in the following tables contained in this webpage (the “Information”) has been collated by Sidley Austin LLP, London (together with Sidley Austin LLP, the “Firm”) using publicly-available sources. The Information is not intended to be, and does not constitute, legal advice. The posting of the Information onto the Firm's website is not intended by the Firm as an offer to provide legal advice or any other services to any person accessing the Firm's website; nor does it constitute an offer by the Firm to enter into any contractual relationship. The accessing of the Information by any person will not give rise to any lawyer-client relationship, or any contractual relationship, between that person and the Firm. -

Report International Conference on Inclusive Insurance 2020 Digital Edition

Report International Conference on Inclusive Insurance 2020 Digital Edition Edited by Zahid Qureshi and Dirk Reinhard Report International Conference on Inclusive Insurance 2020 — Digital Edition Conference documents and This report is the summary of the Inter- presentations are available online: national Conference on Inclusive Insur- ance — Digital Edition, which took place from 2 to 6 November 2020. Individual summaries, in various styles, were contributed by a team of international www.inclusiveinsurance.org rapporteurs. Readers, authors and organisers might not share all opinions expressed or agree with the recommen- dations given. These, however, reflect the rich diversity of the discussions. Over 70 speakers participated in the conference. Report International Conference on Inclusive Insurance 2020 — Digital Edition 1 Contents 1 Contents 31 Agenda 61 Agenda 2 Foreword Day 3—4 November 2020 Day 5—6 November 2020 3 Acknowledgements How to reach scale and develop Lessons learnt and next steps 4 Participant overview inclusive insurance markets 62 Session 16 5 Agenda 32 Session 8 Technology driving Day 1—2 November 2020 Integrated risk inclusive insurance Inclusive insurance management solutions amidst a pandemic 65 Session 17 36 Session 9 The ups and downs of 6 Session 1 How digitisation can inclusive insurance: Opening of the conference — spur market growth Learning from experience The landscape of inclusive insurance 2020 39 Session 10 68 Session 18 Lessons learnt from Outlook: What will be the next 9 Keynote national strategies milestones -

Successful NLII Business Loan Fund Continues to Grow

Successful NLII business loan fund continues to grow Another € 480 million available for Dutch SMEs through institutional investors Amsterdam/Rotterdam, 8 March 2017 – Dutch investment institution Nederlandse Investeringsinstelling N.V. (NLII) and Robeco today announce that the SME corporate lending fund Bedrijfsleningenfonds (BLF), created by NLII with Robeco acting as fund manager, has raised € 480 million in the second funding round, bringing the fund total to € 960 million. This will make extra funding from institutional investors available to larger Dutch SMEs. An amount of € 195 million has already been lent to Dutch SMEs since the fund was established. The parties participating in this second round of funding are NN Group, Pensioenfonds Metaal & Techniek (PMT), Pensioenfonds van de Metalektro (PME), a.s.r. and the European Investment Fund (EIF). Most of these parties also participated in the first funding round. NLII CEO Loek Sibbing: “The success of the BLF is clearly highlighted by this second round of funding. Our objective is to enable institutional investors such as pension funds and insurers to invest directly in the Dutch economy and that is exactly what the BLF offers investors. The fund has already enabled a number of Dutch companies to continue to grow. Expanding the fund increases the lending opportunities for SMEs significantly.” Robeco BLF fund manager Erik Hylarides: “The BLF was established to bring about a change in the funding landscape by offering companies access to multiple sources of finance. The current expansion of the fund and the pipeline of transactions we are working on prove that this has been a success. -

Annual Report and Accounts 2010

bupa Registered office the British united Provident Bupa House Association Limited is a company 15-19 Bloomsbury Way limited by guarantee. London WC1A 2BA registered in england No. 432511. a For further copies of this document nnual report 2010 ‘Bupa’ and the Heartbeat logo are +44 (0)20 7656 2300 registered service marks. Press office +44 (0)20 7656 2454 bupa annual report 2010 W i t H yo u t H r o u g H L i f e rA / 2010 www.bupa.com 2 0 1 0 H i g hl i g H t s Group revenues 5 year record Group underlying 5 year record (up 9%) surplus before tax 06 £3,827.2m 06 £359.1m £7.58bn 07 £4,250.1m £464.9m 07 £374.2m 2009: £6.94bn 08 £5,923.9m 2009: £428.2m 08 £413.4m 09 £6,941.4m 09 £428.2m 10 £7,576.0m 10 £464.9m Group revenues by segment Surplus by segment* Care services £1,182.9m Care services £139.7m europe and North America £2,999.5m europe and North America £116.7m international Markets £3,394.0m international Markets £208.9m throughout the annual report and accounts: equity 5 year record underlying surplus before taxation expense excludes non-recurring items (mainly adjustments relating to amortisation of other intangible assets attributable arising on business combinations, impairment of goodwill and other to bupa 06 £1,917.1m intangible assets, profit / (loss) on sale of businesses and assets, the impact 07 £3,347.4m of property revaluations, realised and unrealised foreign exchange gains and losses and the absolute return on return seeking assets). -

Blue Cross Blue Shield Companies, Bupa Join to Create Largest Global Healthcare Network, Covering 190 Countries

Blue Cross Blue Shield Companies, Bupa Join to Create Largest Global Healthcare Network, Covering 190 Countries GeoBlue, an international health insurance product offered in the U.S. via the BCBS network, to be expanded CHICAGO and LONDON, Jan. 9, 2014 – The Blue Cross Blue Shield Association (BCBSA) and Bupa today announced a strategic global partnership that will create the largest healthcare provider network in the world for international health insurance customers. The U.K.-headquartered international healthcare company Bupa, and the largest U.S.-based health insurance group the Blue Cross and Blue Shield (BCBS) system, are teaming up to expand GeoBlue, the global health insurance product offered in the U.S. under the Blue Cross Blue Shield brand. The partnership includes Bupa’s purchase of a 49 percent stake in Highway to Health, Inc. (HTH)*, which sells and administers the GeoBlue international health insurance products. BCBSA and a group of BCBS companies continue to own the remaining 51 percent. Launching later this year, the partnership will create the largest global health care provider network, combining the BCBS network in the U.S., and GeoBlue’s and Bupa’s global networks, totaling more than 11,500 hospitals and approximately 750,000 medical professionals in more than 190 countries. Bupa and BCBS companies will also develop new insurance products offered through GeoBlue, which will be available to customers and employers for coverage in 2015. “I’m delighted Bupa has joined forces with Blue Cross and Blue Shield organizations – this is the biggest partnership the international health insurance market has ever seen,” said Robert Lang, managing director of the Bupa Global Market Unit. -

Abn Amro Bank Nv

7 MAY 2020 ABN AMRO ABN AMRO BANK N.V. REGISTRATION DOCUMENT constituting part of any base prospectus of the Issuer consisting of separate documents within the meaning of Article 8(6) of Regulation (EU) 2017/1129 (the "Prospectus Regulation") 250249-4-270-v18.0 55-40738204 CONTENTS Page 1. RISK FACTORS ...................................................................................................................................... 1 2. INTRODUCTION .................................................................................................................................. 26 3. DOCUMENTS INCORPORATED BY REFERENCE ......................................................................... 28 4. SELECTED DEFINITIONS AND ABBREVIATIONS ........................................................................ 30 5. PRESENTATION OF FINANCIAL INFORMATION ......................................................................... 35 6. THE ISSUER ......................................................................................................................................... 36 1.1 History and recent developments ............................................................................................. 36 1.2 Business description ................................................................................................................ 37 1.3 Regulation ............................................................................................................................... 40 1.4 Legal and arbitration proceedings .......................................................................................... -

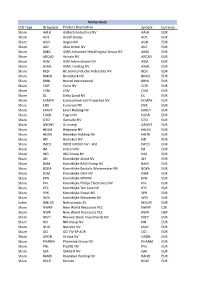

CFD Type IB Symbol Product Description Symbol Currency Share

Netherlands CFD Type IB Symbol Product Description Symbol Currency Share AALB Aalberts Industries NV AALB EUR Share AO1 Accell Group AO1 EUR Share AGN Aegon NV AGN EUR Share AKZ Akzo Nobel NV AKZ EUR Share AMG AMG Advanced Metallurgical Group NV AMG EUR Share ARCAD Arcadis NV ARCAD EUR Share ASM ASM International NV ASM EUR Share ASML ASML Holding NV ASML EUR Share BESI BE Semiconductor Industries NV BESI EUR Share BINCK BinckBank NV BINCK EUR Share BRNL Brunel International BRNL EUR Share COR Corio NV COR EUR Share CSM CSM CSM EUR Share DL Delta Lloyd NV DL EUR Share ECMPA Eurocommercial Properties NV ECMPA EUR Share ENX Euronext NV ENX EUR Share EXACT Exact Holding NV EXACT EUR Share FUGR Fugro NV FUGR EUR Share GTO Gemalto NV GTO EUR Share GRONT Grontmij GRONT EUR Share HEIJM Heijmans NV HEIJM EUR Share HEHN Heineken Holding NV HEHN EUR Share HEI Heineken NV HEI EUR Share IMCD IMCD GROUP NV - W/I IMCD EUR Share IM Imtech NV IM EUR Share ING ING Groep NV ING EUR Share AH Koninklijke Ahold NV AH EUR Share BAM Koninklijke BAM Groep NV BAM EUR Share BOKA Koninklijke Boskalis Westminster NV BOKA EUR Share DSM Koninklijke DSM NV DSM EUR Share KPN Koninklijke KPN NV KPN EUR Share PHI Koninklijke Philips Electronics NV PHI EUR Share KTC Koninklijke Ten Cate NV KTC EUR Share VPK Koninklijke Vopak NV VPK EUR Share WES Koninklijke Wessanen NV WES EUR Index IBNL25 Netherlands 25 IBNL25 EUR Share NWRP New World Resources PLC NWRP CZK Share NWR New World Resources PLC NWR GBP Share NISTI Nieuwe Steen Investments NV NISTI EUR Share NN NN Group NV -

Aegon Fixed Income

Executing our strategy April 2014 Fixed income presentation aegon.com Key messages . Focus on executing our strategy is delivering clear results ► Strategic transformation to become a truly customer-centric company is well underway ► Solid business growth is driving increase in profitability ► Risk profile significantly improved . Executing on balanced capital deployment strategy, supporting a sustainable dividend . Making progress towards 2015 targets . Intention to remain on track to be within leverage target ranges by the end of 2014 2 Over 150 Life insurance, pensions years of & asset management history AA- financial Present in more than 25 strength rating markets throughout the Americas, Europe and Asia Underlying earnings before tax Revenue-generating investments Paid out in claims and benefits in 2013 in 2013 Over EUR 1.9 EUR 20 26,500 billion billion EMPLOYEES1 EUR 475 billion1 Aegon at a glance 1) As per December 31, 2013 3 Building on leading market positions United States United Kingdom The Netherlands China of America # 7 Individual pensions # 1 Group pensions # 11 of foreign-owned life # 5 Individual life # 3 Group pensions # 6 Individual life insurers in China # 8 Variable Annuities # 10 Individual protection # 6 Accident & health # 12 Pensions # 10 Annuities # 10 Property & casualty Japan Canada Central & Spain # 1 Variable annuities # 5 Universal life Eastern Europe Historic positions do not reflect # 6 Term life # 1 Household in Hungary current business India # 6 Life in Hungary Start up # 3 Pensions Romania1 Brazil # -

Controversial Arms Trade

Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Case study: Controversial Arms Trade A case study prepared for the Fair Insurance Guide Anniek Herder Alex van der Meulen Michel Riemersma Barbara Kuepper 18 June 2015, embargoed until 18 June 2015, 00:00 CET Naritaweg 10 1043 BX Amsterdam The Netherlands Tel: +31-20-8208320 E-mail: [email protected] Website: www.profundo.nl Contents Summary ..................................................................................................................... i Samenvatting .......................................................................................................... viii Introduction ................................................................................................................ 1 Chapter 1 Background ...................................................................................... 2 1.1 What is at stake? ....................................................................................... 2 1.2 Trends in international arms trade .......................................................... 3 1.3 International standards............................................................................. 4 1.3.1 Arms embargoes ......................................................................................... 4 1.3.2 EU arms export policy ................................................................................. 4 1.3.3 Arms Trade Treaty .....................................................................................