Global Truck Study 2016, the Truck Industry in Transition

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Weifu High-Technology Group Co., Ltd

无锡威孚高科技集团股份有限公司 2021 年半年度报告全文 WEIFU HIGH-TECHNOLOGY GROUP CO., LTD. SEMI-ANNUAL REPORT 2021 AUGUST 2021 1 无锡威孚高科技集团股份有限公司 2021 年半年度报告全文 Section I. Important Notice, Contents and Interpretation Board of Directors, Supervisory Committee, all directors, supervisors and senior executives of Weifu High-Technology Group Co., Ltd. (hereinafter referred to as the Company) hereby confirm that there are no any fictitious statements, misleading statements, or important omissions carried in this report, and shall take all responsibilities, individual and/or joint, for the reality, accuracy and completion of the whole contents. Wang Xiaodong, Principal of the Company, Ou Jianbin, person in charger of accounting works and Ou Jianbin, person in charge of accounting organ (accounting principal) hereby confirm that the Financial Report of 2021 Semi-Annual Report is authentic, accurate and complete. All directors are attend the Meeting for the Report deliberation. In this report, details of relevant risks and countermeasures in operation have described, found more in relevant content in the Report. Concerning the forward-looking statements with future planning involved in the Report, they do not constitute a substantial commitment for investors. The China Securities Journal, Securities Times, Hong Kong Commercial Daily and Juchao Website (www.cninfo.com.cn)are the information disclosure media appointed by the Company, all information should be prevail on the above mentioned media, investors are advice to pay attention on investment risks. The Company has no plan of cash dividend distributed, no cash bonus and capitalizing of common reserves either carried out. The Report is prepared in Chinese and English respectively. In the event of any discrepancy between the two versions, the Chinese version shall prevail. -

CHINA CORP. 2015 AUTO INDUSTRY on the Wan Li Road

CHINA CORP. 2015 AUTO INDUSTRY On the Wan Li Road Cars – Commercial Vehicles – Electric Vehicles Market Evolution - Regional Overview - Main Chinese Firms DCA Chine-Analyse China’s half-way auto industry CHINA CORP. 2015 Wan Li (ten thousand Li) is the Chinese traditional phrase for is a publication by DCA Chine-Analyse evoking a long way. When considering China’s automotive Tél. : (33) 663 527 781 sector in 2015, one may think that the main part of its Wan Li Email : [email protected] road has been covered. Web : www.chine-analyse.com From a marginal and closed market in 2000, the country has Editor : Jean-François Dufour become the World’s first auto market since 2009, absorbing Contributors : Jeffrey De Lairg, over one quarter of today’s global vehicles output. It is not Du Shangfu only much bigger, but also much more complex and No part of this publication may be sophisticated, with its high-end segment rising fast. reproduced without prior written permission Nevertheless, a closer look reveals China’s auto industry to be of the publisher. © DCA Chine-Analyse only half-way of its long road. Its success today, is mainly that of foreign brands behind joint- ventures. And at the same time, it remains much too fragmented between too many builders. China’s ultimate goal, of having an independant auto industry able to compete on the global market, still has to be reached, through own brands development and restructuring. China’s auto industry is only half-way also because a main technological evolution that may play a decisive role in its future still has to take off. -

Ids-TCV5(9)07 -BIR High Performance All-Rounder Traffic Camera

iDS-TCV5(9)07 -BIR High Performance All-Rounder Traffic Camera 5 MP (2/3” GMOS), 2464 × 2056 @ 50 fps License plate recognition 9 MP (1” GMOS), 4096 × 2160 @ 25 fps Vehicle type recognition Color: 0.001 Lux @ (F1.4, AGC ON) Vehicle color recognition H.265, H.264, MJPEG Vehicle manufacturer recognition 60 dB SNR Supports speed detection with built-in 24 GHz 3D DNR radar Alarm I/O Built-in IR light with 16 beads One RS-485 interface IP65 Two defined streams Over 98% detection sensitivity Built-in Micro SD/TF card, up to 128 GB Over 98% LPR accuracy Supports side mounting with convenient installation and debug Superiority Dedicated camera for ANPR HD resolution Integrated IR Professional shutter speed control Built-in ANPR engine, equipped with deep-learning algorithm Built-in radar, supporting speed detection Multiple detection and recognition Vehicle type recognition Vehicle color recognition Vehicle manufacturer recognition Radar speed detection Driving on lane line detection Illegal lane change detection Wrong-way driving detection Seatbelt status detection Phone call detection Application Vehicle control Traffic monitoring Toll collection Security Speed detection Scenarios Highway Tunnel Toll station Urban road Specification Camera iDS-TCV507-BIR iDS-TCV907-BIR Image Sensor 5 MP (2/3” GMOS) 9 MP (1” GMOS) Min. Illumination Color: 0.001 Lux @ (F1.4, AGC ON), 0.0005 Lux with IR Shutter Speed 50 to 20,000 μs Day & Night IR cut filter Digital Noise Reduction 2D/3D DNR SNR 60 dB Lens Focal Length -

Análisis De Los Materiales Utilizados En La

UNIVERSIDAD TECNOLÓGICA EQUINOCCIAL FACULTAD DE CIENCIAS DE LA INGENIERÍA E INDUSTRIAS CARRERA DE INGENIERÍA AUTOMOTRIZ ANÁLISIS DE LOS MATERIALES UTILIZADOS EN LA CONSTRUCCIÓN DE UN CIGÜEÑAL DE UN VEHÍCULO CHINO MARCA SAIC WULING MODELO MINI VAN PASAJEROS 1000CC MEDIANTE ENSAYOS DESTRUCTIVOS Y NO DESTRUCTIVOS TRABAJO PREVIO A LA OBTENCIÓN DEL TÍTULO DE INGENIERO AUTOMOTRIZ HERNÁN DARÍO VALENCIA RAMÍREZ DIRECTOR: MSC. LENÍN OMAR VALENCIA MÉNDEZ Quito, septiembre 2016 © Universidad Tecnológica Equinoccial. 2016 Reservados todos los derechos de reproducción FORMULARIO DE REGISTRO BIBLIOGRÁFICO PROYECTO DE TITULACIÓN DATOS DE CONTACTO CÉDULA DE 172452804-5 IDENTIDAD: APELLIDOS Y VALENCIA RAMÍREZ HERNÁN DARÍO NOMBRES: SAN CARLOS (PEDRO DE ALVARADO N57 75 Y FERNANDEZ DIRECCIÓN: SALVADOR, BLOQUE HUMABI DEP. 102) EMAIL: [email protected] TELÉFONO FIJO: 2596922 TELÉFONO 0983087331 MOVIL: DATOS DE LA OBRA ANÁLISIS DE LOS MATERIALES UTILIZADOS EN LA CONSTRUCCIÓN DE UN CIGÜEÑAL DE UN VEHÍCULO TITULO: CHINO MARCA SAIC WULING MODELO MINI VAN PASAJEROS 1000CC MEDIANTE ENSAYOS DESTRUCTIVOS Y NO DESTRUCTIVOS AUTOR O AUTORES: VALENCIA RAMÍREZ HERNÁN DARÍO FECHA DE ENTREGA DEL PROYECTO DE 2016-09-12 TITULACIÓN: DIRECTOR DEL PROYECTO DE MSC. LENÍN OMAR VALENCIA MÉNDEZ TITULACIÓN: PREGRADO POSGRADO PROGRAMA X TITULO POR EL QUE INGENIERO AUTOMOTRIZ OPTA: RESUMEN: Mínimo Se realizó el análisis de los materiales utilizados en la 250 palabras construcción de un cigüeñal de un vehículo chino marca Saic Wuling modelo mini van pasajeros 1000cc mediante ensayos destructivos y no destructivos, se utilizó los laboratorios de Metalurgia Extractiva, Metalografía, desgaste y falla, Análisis de Esfuerzos Y vibraciones, y el taller de Mecanizado de la Facultad de Ingeniería Mecánica de la Escuela Politécnica Nacional por medio de probetas normalizadas internacionalmente bajo la Sociedad Americana para Pruebas y Materiales (ASTM) por sus siglas en inglés. -

Promocja Na Filtry Do 31.12.2017

Promocja na filtry do 31.12.2017 cena Nazwa symbol sprzedaży zamiennik zastosowanie netto 81779100017MAN AJ 2014.06.09 / CC4E / A-89240001960 Filtr 64049A 0,97 / AF25951 Filtr AP051/6 18,48 C30138 / SA5176/ WA59431/ E605L/ PA7557 Filtr chłodziwa WF2061 34,78 WF2053/ SW1617 Filtr chłodziwa WF2078 23,94 P551309 Filtr chłodziwa WF2083 22,38 Filtr chłodziwa WF2091 30,25 WE2091/ SW1641 Filtr Cieczy H34WF 31,96 WF2142/ WA923/2/ B5089/ WF2142/ FT5459/ WFC20 Filtr hudrauliczny ST1953 70,08 HY15132 Filtr hydraulczny HF7703 111,97 SH51000V/ PT9293/ PT23233 Filtr hydrauliczny 4400367 103,08 6250257442 Filtr hydrauliczny 4656608 123,07 HF7679 / SH60328 Hitachi, Filtr hydrauliczny 417090251 72,53 HY9968 Filtr hydrauliczny FH0421 22,40 HF7999 / 4139298936 / HZO-008 / 0002701098 Filtr hydrauliczny H060D20H 75,01 ST1037/ SH75007 Filtr hydrauliczny H160D25W 129,23 ST1061/ SH75067 Filtr hydrauliczny H240D20N 74,56 SH75038 / HF6873 Filtr hydrauliczny H962 53,05 SH62203 / HX89/ HX89/ E834H Filtr hydrauliczny HEK0240239 93,04 HHC01426 / SH63331 Filtr hydrauliczny HF28812 72,73 SH51026/ 51821/ B7026/ W1019 Massey-Ferguson, Filtr hydrauliczny HF28866 23,42 CR60/6 / P171523 Filtr hydrauliczny HF28891 101,87 SH66032/ 51853/ PT509-MPG/KIT Case, Filtr hydrauliczny HF28894 178,41 SH60007/ BT9377/ P550615 Komatsu, Filtr hydrauliczny HF28900 28,97 SO1684/ HY9757/ 51089/ PT8350/ P551753 Caterpillar, Filtr hydrauliczny HF28912 26,93 SH63018 / HY9169/ 92082E/ PT9477/ WH22-25 Case, Fiat, Fiatagri, New Holland, Dennis Eagle, cena Nazwa symbol sprzedaży zamiennik zastosowanie -

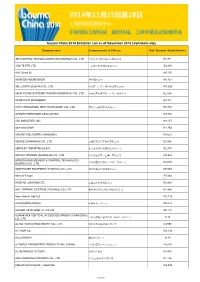

11-20 Baumachina2014 Preliminary Exhibitor List.Xlsx

bauma China 2014 Exhibitor List as of November 2014 (alphabetically) Company name Company name in Chinese Hall / Outdoor / Booth Number 3B6 CONTROL TECHNOLOGIES (GUANGZHOU) CO., LTD. 广州市惠毕斯控制技术有限公司 E4.771 3-ELITE PTE LTD. 三易电子科技股份有限公司 E4.270 A.M. Gears Srl N5.170 AB BRUZAHOLMS BRUK 瑞典BZH公司 N3.321 ABL LIGHTS (DALIAN) CO., LTD. 阿波罗(大连)照明制品有限公司 W3.560 ABUS CRANE SYSTEMS TRADING (SHANGHAI) CO., LTD. 安博起重设备贸易(上海)有限公司 E2.636 ACME PACK ENGINEERS E3.131 ACP (CHANGZHOU) HEAT EXCHANGER CO., LTD. 常州爱克普换热器有限公司 E5.739 ACROW FORMWORK ASIA LIMITED W3.701 ADL INSULFLEX, INC. N3.117 ad-media GmbH N1.752 ADVANTAGE AUSTRIA SHANGHAI N3.621 AEGISE (SHANGHAI) CO., LTD. 上海得锡乐汽车配件有限公司 E2.586 AEROLIFT INDUSTRIALS B.V. 保定安瑞利特机械制造有限公司 E2.735 AFFINIA TRADING (SHANGHAI) CO., LTD. 阿菲尼亚贸易(上海)有限公司 W4.624 AFRISO MEASUREMENT & CONTROL TECHNOLOGY 菲索测量控制技术(苏州)有限公司 N4.574 (SUZHOU) CO., LTD. AGG POWER EQUIPMENT (FUZHOU) CO., LTD. 福州德塔动力设备有限公司 N5.589 Aircrete Europe E7.460 AIRSTAR LIGHTING LTD. 上海辰驻贸易有限公司 E4.289 AKG THERMAL SYSTEMS (TAICANG) CO., LTD. 爱克奇换热技术(太仓)有限公司 N1.468 Akon Hidrolik Valf A.S. W1.116 ALFAGOMMA NINGO 阿法格玛宁波公司 W5.228 ALFRED HEYD GMBH U. CO. KG N5.131 ALIMAK HEK VERTICAL ACCESS EQUIPMENT (CHANGSHU) 安利马赫垂直输送设备(常熟)有限公司 A.14 CO., LTD. AL-KO (YANTAI) MACHINERY CO., LTD. 烟台爱科机械设备有限公司 E3.568 ALL-KOR CO. W4.134 ALLU GROUP ALLU集团公司 A.19 ALTAIRAC ENGINEERED PRODUCTS INC.(CHINA) 上海阿泰瑞克重工有限公司 E6.638 ALTO PRODUCTS CORP. 翱图汽车配件 N3.415 AMA (SHANGHAI) TRADING CO., LTD. 埃马(上海)商贸有限公司 N1.126 AMERICAN AUGERS / TRENCOR W2.650 1 von 97 bauma China 2014 Exhibitor List as of November 2014 (alphabetically) Company name Company name in Chinese Hall / Outdoor / Booth Number AMETEK VEHICULAR INSTRUMENTATION SYSTEMS (VIS) N5.738 Ammann Construction Machinery Shanghai Co., LTD. -

Ids-TCV500-BE/Ids-TCV900-BE High Performance ANPR Capture Unit

iDS-TCV500-BE/iDS-TCV900-BE High Performance ANPR Capture Unit 5 MP (2/3” GMOS), 2464 × 2056 @ 50 fps Two defined streams 9 MP (1” GMOS), 4096 × 2160 @ 25 fps Built-in micro SD/TF card, up to 128 GB Color: 0.001 Lux@(F1.4, AGC ON) License plate recognition (LPR) H.265, H.264, MJPEG Vehicle type recognition 60 dB SNR Vehicle color recognition 3D DNR Vehicle manufacturer recognition Alarm I/O Detection sensitivity: > 98% LPR accuracy: > 98% Superiority Dedicated camera for ANPR HD resolution Professional shutter speed control Built-in ANPR engine, equipped with deep learning algorithm Capable of recognizing multiple features and detecting multiple violations Vehicle type recognition Vehicle color recognition Vehicle manufacturer recognition Radar speed detection Driving on lane line detection Illegal lane change detection Wrong-way driving detection Seatbelt detection Phone call detection Application Vehicle control Traffic monitoring Toll collection Security Scenarios Highway Tunnel Toll station Urban road Specification Camera iDS-TCV500-BE iDS-TCV900-BE Image Sensor 5 MP (2/3'' GMOS) 9 MP (1'' GMOS) Min. Illumination Color: 0.001 Lux@(F1.4, AGC ON) Shutter Speed 50 μs to 20,000 μs Day & Night IR cut filter Digital Noise Reduction 2D/3D DNR SNR 60 dB Lens Focal Length 15 to 50 mm 11 to 40 mm 25 mm Aperture F1.4-C F1.6-25 F1.4 Focus Manual CS-Mount CS-Mount CS-Mount Horizontal: 62° to Horizontal: 31°, FOV Horizontal: 42.7° to 13.7° 23.6° Vertical: 16.9° Vertical: 23.4° to 7.6° Vertical: 32.2° to 12.2° -

Support List : for Instrument Series Brand Model Year/Chip

Support list : For instrument Series Brand Model Year/Chip Single chip DongFeng 81118(1;570) ATMEGA32 instrument Single chip DongFeng 90318(1;570) ATMEGA32 instrument Single chip DongFeng 90408(1;615) ATMEGA32 instrument Single chip DongFeng 90820(1;570) ATMEGA32 instrument Single chip DongFeng 90923(1;570) ATMEGA32 instrument Single chip DongFeng 91007(1;615) ATMEGA32 instrument Single chip DongFeng 100123(1;570) ATMEGA16 instrument Single chip DongFeng 100305(1;495) ATMEGA32 instrument Single chip DongFeng 100512(1;495) ATMEGA32 instrument Single chip DongFeng P100719 ATMEGA32 instrument Single chip DongFeng P110303 ATMEGA32 instrument Single chip DongFeng P3820070(1;615) ATMEGA32 instrument Single chip DongFeng XTD70802 ATMEGA16 instrument Single chip DongFeng XTD70808 ATMEGA16 instrument Single chip DongFeng XTD70830 ATMEGA16 instrument Single chip DongFeng XTD71028 ATMEGA16 instrument Single chip DongFeng XTD71105 ATMEGA32 instrument Single chip DongFeng XTD80516 ATMEGA32 instrument Single chip DongFeng XTD90818 ATMEGA32 V1 instrument Single chip DongFeng XTD91126 ATMEGA32 instrument Single chip DongFeng XTD120814 ATMEGA32 instrument Single chip FOTON Auman ATMEGA32 instrument Single chip FuDi ZB157J1D1 ATMEGA16 instrument Single chip HaFei Zhongyi ATMEGA169 instrument Single chip Geely ZB156A ATMEGA169 V1 instrument Single chip Geely ZB127LS ATMEGA169 V1 instrument Single chip Geely ZB137LZ ATMEGA169 instrument Single chip Geely ZB118TYJ ATMEGA16 instrument Single chip Geely ZB106 ATMEGA16 instrument Single chip Geely ZB118 ATMEGA16 -

Make Code Make Description Model Code Model

MAKE CODE MAKE DESCRIPTION MODEL CODE MODEL DESCRIPTION TOYO TOYOTA CORON_STATI Corona Station Wagon TOYO TOYOTA CREST_DIES Cresta/Cressida (Diesel) TOYO TOYOTA CREST_PET Cresta/Cressida (Petrol) TOYO TOYOTA CROWN_DIES Crown (Diesel) TOYO TOYOTA CROWN_PET Crown (Petrol) TOYO TOYOTA CROWN Crown TOYO TOYOTA CROWN_JZS Crown, model JZS TOYO TOYOTA CYNOS_COUPE Cynos Coupe TOYO TOYOTA DUET_M100A Duet, model M100A TOYO TOYOTA DUET_M101A Duet, model M101A TOYO TOYOTA DYNA_CAB Dyna Cab Over TOYO TOYOTA DYNA_DUMP Dyna Dump Truck TOYO TOYOTA ESTIM_EMINA Estima Emina (Diesel) TOYO TOYOTA ESTIM_LUCID Estima Lucida (Petrol) TOYO TOYOTA ESTIM Estima TOYO TOYOTA FORTU_2WD27 Fortuner 2.7, 2WD TOYO TOYOTA FORTU_4WD27 Fortuner 2.7, 4WD TOYO TOYOTA FORTU_2WD30 Fortuner 3.0, 2WD TOYO TOYOTA FORTU_4WD30 Fortuner 3.0, 4WD TOYO TOYOTA FUN_CARGO Fun cargo Hatchback TOYO TOYOTA GAIA_ACM10 Gaia, model ACM10 TOYO TOYOTA GAIA_ACM15 Gaia, model ACM15 TOYO TOYOTA GAIA_SXM10 Gaia, model SXM10 TOYO TOYOTA GAIA_SXM15 Gaia, model SXM15 TOYO TOYOTA GRANV_WAGON Granvia Wagon TOYO TOYOTA HARRI_PET Harrier (Petrol) TOYO TOYOTA HARRI_DBA Harrier, Model DBA-GSU30W TOYO TOYOTA HIACE_MINI Hiace Mini - TOYO TOYOTA HIACE_MINI_BUS Hiace Mini Bus TOYO TOYOTA HIACE_SUPER Hiace Super Custom TOYO TOYOTA HIACE_VAN_PET Hiace Van (Petrol) TOYO TOYOTA HIACE_VAN Hiace Van TOYO TOYOTA HILUX_DIES Hilux (Diesel) TOYO TOYOTA HILUX_4WD Hilux 4WD Station TOYO TOYOTA HILUX_2WD Hilux D/Cabin 2WD TOYO TOYOTA HILUX_4WD1 Hilux D/Cabin 4WD TOYO TOYOTA HILUX_DBL Hilux Double Cabin TOYO TOYOTA HILUX_LONG -

Gaining Momentum: Recent Trends in China's Automobile Parts Market

Gaining momentum: Recent trends in China's automobile parts market National Industry Program Contents 1 Executive summary 2 Overview of regulatory environment 4 Market size and key players' trends' analysis 10 Market segments outlook 17 Market opportunities and Deloitte's suggestions 20 Contacts Executive summary 2011 is the first year of China’s “12th Five-Year Plan”, which will witness economic transition from policy- stimulated rapid growth to stable growth amid structural adjustment, during which, the development of the auto industry in China is shifting from scale expansion to strength growth. “Proprietary brand”, “M&A and restructuring” and “new-energy auto” are three key words in the draft of the “12th Five-Year Plan” for the auto industry. During April to May 2011, National Development and Reform Commission (NDRC) and Ministry of Commerce jointly amended Catalogue for the Guidance of Foreign Investment Industries, specifying for the first time that the percentage of foreign equity shall not exceed 50 percent in enterprises of key new-energy auto parts. This provision may have far-reaching impact on the overall layout of multinational companies in the parts industry in China. As a key link in the global production and supply system of autos and parts, China now houses almost all the world-leading auto parts manufacturers and is itself a huge exporter of home-made auto tires, glasses and audio products. The scale of China’s auto parts and accessories industry approached RMB1.5 trillion in 2010, with the CAGR of 30 percent in the past five years. Percentage of the total output of the parts sector in the total output of the auto industry has increased steadily to above 40 percent. -

ZF-TRW - Global Headquarters Chassis, Transmission, Driveline Systems

ZF-TRW - Global Headquarters Chassis, transmission, driveline systems ZF Friedrichshafen AG ZF Friedrichshafen is a global leader in driveline and chassis technology as well as active Graf-von-Soden-Platz 1 and passive safety technology. In 2014, the company generated 56% of its sales from Friedrichshafen Europe. 88046 Germany The company, which acquired TRW Automotive in May 2015, is now present in about 230 locations in some 40 countries. ZF is one of the top three automotive suppliers worldwide. ZF completed acquisition of TRW Automotive for Tel: +49 7541 770 USD12.4 billion. Subsequent to the acquisition, TRW’s business is incorporated into ZF as a new division called Fax: +49 7541 77 908 000 Active & Passive Safety. TRW is being managed as the fifth division within the ZF Group. The company expects the Web: http://www.zf.com integration to conclude in three to five years. Latitude: 47.66757 The combined company is a one of the major players in automotive technologies, ranging from driver assistance and Longitude: 9.49342 occupant safety systems, to drivelines and transmissions, and braking and steering systems. This combination of advanced technologies comprehensively addresses the growing, industry-wide trends of safety, fuel efficiency and Company Type: Public autonomous driving. Also, in February 2015, ZF divested its 50% share in steering systems joint-venture ZF Lenksysteme (ZFLS) to Bosch in order to smooth its TRW acquisition. Had ZF not divested its stake in ZFLS, the Senior Officers combined ZF-TRW would have gained a large share in the global steering systems market. Dr. Stefan Sommer, CEO, Head, Steering Post reorganization and TRW acquisition, ZF operates its business in five divisions: Car Powertrain Technology, Car Systems, ZF Services, Corporate Research Chassis Technology, Commercial Vehicle Technology, Industrial Technology, and Active and Passive Safety and Development Technology. -

Western Arms Exports to China

SIPRI Policy Paper WESTERN 43 ARMS EXPORTS January 2015 TO CHINA oliver bräuner, mark bromley and mathieu duchâtel STOCKHOLM INTERNATIONAL PEACE RESEARCH INSTITUTE SIPRI is an independent international institute dedicated to research into conflict, armaments, arms control and disarmament. Established in 1966, SIPRI provides data, analysis and recommendations, based on open sources, to policymakers, researchers, media and the interested public. The Governing Board is not responsible for the views expressed in the publications of the Institute. GOVERNING BOARD Sven-Olof Petersson, Chairman (Sweden) Dr Dewi Fortuna Anwar (Indonesia) Dr Vladimir Baranovsky (Russia) Ambassador Lakhdar Brahimi (Algeria) Jayantha Dhanapala (Sri Lanka) Ambassador Wolfgang Ischinger (Germany) Professor Mary Kaldor (United Kingdom) The Director DIRECTOR Dr Ian Anthony (United Kingdom) Signalistgatan 9 SE-169 70 Solna, Sweden Telephone: +46 8 655 97 00 Fax: +46 8 655 97 33 Email: [email protected] Internet: www.sipri.org Western Arms Exports to China SIPRI Policy Paper No. 43 OLIVER BRÄUNER, MARK BROMLEY AND MATHIEU DUCHÂTEL January 2015 © SIPRI 2015 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, without the prior permission in writing of SIPRI or as expressly permitted by law. Printed in Sweden ISSN 1652–0432 (print) ISSN 1653–7548 (online) ISBN 978–91–85114–87–0 Contents Preface iv Acknowledgements v Summary vi Abbreviations ix 1. Introduction 1 2. The United States’ export controls on transfers to China 5 The US national export control system 5 US national controls on exports to China 7 Application of national export controls on transfers to China 9 What has the USA licensed and exported to China? 13 Box 2.1.