(Kdcb) in Kerala State, India

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Unclaimed September 2018

SL NO ACCOUNT HOLDER NAME ADDRESS LINE 1 ADDRESS LINE 2 CITY NAME 1 RAMACHANDRAN NAIR C S/O VAYYOKKIL KAKKUR KAKKUR KAKKUR 2 THE LIQUIDATOR S/O KOYILANDY AUTORIKSHA DRIVERS CO-OP SOCIE KOLLAM KOYILANDY KOYILANDY 3 ACHAYI P K D/OGEORGE P K PADANNA ARAYIDATH PALAM PUTHIYARA CALICUT 4 THAMU K S/O G.R.S.MAVOOR MAVOOR MAVOOR KOZHIKODE 5 PRAMOD O K S/OBALAKRISHNAN NAIR OZHAKKARI KANDY HOUSE THIRUVALLUR THIRUVALLUR KOZHIKODE 6 VANITHA PRABHA E S/O EDAKKOTH HOUSE PANTHEERANKAVU PANTHEERANKAVU PANTHEERAN 7 PRADEEPAN K K S/O KOTTAKKUNNUMMAL HOUSE MEPPAYUR MEPPAYUR KOZHIKODE 8 SHAMEER P S/O KALTHUKANDI CHELEMBRA PULLIPARAMBA MALAPPURAM 9 MOHAMMED KOYA K V S/O KATTILAVALAPPIL KEERADATHU PARAMBU KEERADATHU PARAMBU OTHERS 10 SALU AUGUSTINE S/O KULATHNGAL KOODATHAI BAZAR THAMARASSERY THAMARASSE 11 GIRIJA NAIR W/OKUNHIRAMAN NAIR KRISHADARSAN PONMERI PARAMBIL PONMERI PARAMBIL PONMERI PA 12 ANTSON MATHEW K S/O KANGIRATHINKAV HOUSE PERAMBRA PERUVANNAMUZHI PERUVANNAM 13 PRIYA S MANON S/O PUNNAMKANDY KOLLAM KOLLAM KOZHIKODE 14 SAJEESH K S/ORAJAN 9 9 KOTTAMPARA KURUVATTOOR KONOTT KURUVATTUR 15 GIRIJA NAIR W/OKUNHIRAMAN NAIR KRISHADARSAN PONMERI PARAMBIL PONMERI PARAMBIL PONMERI PA 16 RAJEEVAN M K S/OKANNAN MEETHALE KIZHEKKAYIL PERODE THUNERI PERODE 17 VINODKUMAR P K S/O SATHYABHAVAN CHEVAYOOR MARRIKKUNNU CHEVAYUR 18 CHANDRAN M K S/O KATHALLUR PUNNASSERY PUNNASSERY OTHERS 19 BALAKRISHNAN NAIR K S/O M.C.C.BANK LTD KALLAI ROAD KALLAI ROAD KALLAI ROA 20 NAJEEB P S/O ZUHARA MANZIL ERANHIPALAM ERANHIPALAM ERANHIPALA 21 PADMANABHAN T S/O KALLIKOODAM PARAMBA PERUMUGHAM -

Decisions of Regional Transport Authority, Kozhikode in Themeeting Held on 4-3-2017 at Collectorate Conference Hall, Kozhikode

1 Decisions of Regional Transport Authority, Kozhikode in themeeting held on 4-3-2017 at Collectorate Conference Hall, Kozhikode. PRESENT: 1. SRI.U.V. JOSE, IAS, DISTRICT COLLECTOR AND CHAIRMAN, REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. 2. Dr.P.M.MOHAMMED NAJEEB, DEPUTY TRANSPORT COMMISSIONER AND MEMBER OF REGIONAL TRANSPORT AUTHORITY, KOZHIKODE. Item No. 1 Heard. Granted concurrence for renewal of regular stage carriage permit in respect of KL 10 P 4599 as LSOS without prejudice to the right of the primary authority to fix the class of service according to the length of route and subject to verification of scheme violation if any by the original authority. Item No. 2 Heard. Granted concurrence for renewal of regular stage carriage permit in respect of KL 05 AB 3666 as LSOS without prejudice to the right of the primary authority to fix the class of service according to the length of route and subject to verification of scheme violation if any by the original authority. Item No. 3 Heard. Granted concurrence for renewal of regular stage carriage permit in respect of KL 05 AE 1825 and KL 05 AH 4972 as LSOS without prejudice to the right of the primary authority to fix the class of service according to the length of route and subject to verification of scheme violation if any by the original authority Item No. 4 Heard, the class/Type of service and distance covered in this jurisdiction are not mentioned in the agenda. Hence, decision on the application is 1 2 2 adjourned with direction to Secretary to place the matter in the ensuing meeting with all details. -

Agenda for the Rta Meeting Held on 24.01.2017 at Collectorate Conference Hall, Kozhikode

AGENDA FOR THE RTA MEETING HELD ON 24.01.2017 AT COLLECTORATE CONFERENCE HALL, KOZHIKODE. Present: 1. Sri. N. Prasanth, IAS, District Collector and Chairman, Regional Transport Authority, Vatakara. 2. Sri. M.K.Pushkaran, IPS, Superintendent of Police Kozhikode (Rural) and Member, RTA, Vatakara. 3. Dr.P.M.Muhammed Najeeb, Deputy Transport Commissioner, North Zone, Kozhikode and Member, RTA, Vatakara Item No.1 No G1/4588/2016 AGENDA: - To consider the request for permission for a Bus stand at Kuttiady Town. Applicant:- The Secretary, Kuttiady Grama Panchayath , Kuttiady Item No: 2 G/436342016V Agenda:- To reconsider adjourned item No. 03 dt. 23.06.2016 ie the application for fresh regular stage carriage permit to operate on the route Kattilpeedika - Thoovappara – Koyilandy - Ulloorkadav (via) Vengalam, Kannankandy mukk, Kappad, Pookkad beach, Poyilkav beach, Cheriya mangad, Harbour and Market road with the following set of timings (vehicle number not furnished). Proposed timings. Ulloorkadav Koyilandy Kattilpeedika Start 7.15 7.35 7.40 8.10 8.30 9.00 9.30 10.00 10.10 1 10.40 10.55 11.25 11.50 12.20 12.40 1.10 1.20 1.50 3.00 3.30 3.45 4.15 4.30 5.00 5.10 5.40 5.50 6.20 6.30 7.25 Halt 7.00 7.05 Applicant: Smt. Girija, Nambidikandi. H, Kavumthara. PO, Koyilandy. Hence the RTA may peruse the records and take a decision. Item No:3 G/10425/2016V Agenda:- To reconsider adjourned item No. 06 dt. 23.06.2016 ie the application for fresh regular stage carriage permit in respect of S/C KL 58 G 7115 to operate on the route Kurumpoyil – Koottalida – Balussery - Kozhikode (via) Kannadipoyil, Arapeedika, Manhapalam, Nanmanda, Eranhipalam, Baby Memorial hospital with the following set of timings. -

Report of Rapid Impact Assessment of Flood/ Landslides on Biodiversity Focus on Community Perspectives of the Affect on Biodiversity and Ecosystems

IMPACT OF FLOOD/ LANDSLIDES ON BIODIVERSITY COMMUNITY PERSPECTIVES AUGUST 2018 KERALA state BIODIVERSITY board 1 IMPACT OF FLOOD/LANDSLIDES ON BIODIVERSITY - COMMUnity Perspectives August 2018 Editor in Chief Dr S.C. Joshi IFS (Retd) Chairman, Kerala State Biodiversity Board, Thiruvananthapuram Editorial team Dr. V. Balakrishnan Member Secretary, Kerala State Biodiversity Board Dr. Preetha N. Mrs. Mithrambika N. B. Dr. Baiju Lal B. Dr .Pradeep S. Dr . Suresh T. Mrs. Sunitha Menon Typography : Mrs. Ajmi U.R. Design: Shinelal Published by Kerala State Biodiversity Board, Thiruvananthapuram 2 FOREWORD Kerala is the only state in India where Biodiversity Management Committees (BMC) has been constituted in all Panchayats, Municipalities and Corporation way back in 2012. The BMCs of Kerala has also been declared as Environmental watch groups by the Government of Kerala vide GO No 04/13/Envt dated 13.05.2013. In Kerala after the devastating natural disasters of August 2018 Post Disaster Needs Assessment ( PDNA) has been conducted officially by international organizations. The present report of Rapid Impact Assessment of flood/ landslides on Biodiversity focus on community perspectives of the affect on Biodiversity and Ecosystems. It is for the first time in India that such an assessment of impact of natural disasters on Biodiversity was conducted at LSG level and it is a collaborative effort of BMC and Kerala State Biodiversity Board (KSBB). More importantly each of the 187 BMCs who were involved had also outlined the major causes for such an impact as perceived by them and suggested strategies for biodiversity conservation at local level. Being a study conducted by local community all efforts has been made to incorporate practical approaches for prioritizing areas for biodiversity conservation which can be implemented at local level. -

GI Journal No. 52 1 October 30, 2013

October 30, 2013 GOVERNMENT OF INDIA GEOGRAPHICAL INDICATIONS JOURNAL NO. 52 OCTOBER 30, 2013 / KARTIKA 07, SAKA 1935 2 October 30, 2013 INDEX S.No. Particulars Page No. 1. Official Notices 4 2. New G.I Application Details 5 3. Public Notice 7 4. GI Applications Kaipad Rice – GI Application No. 242 Kullu Shawl (Logo) – GI Application No. 383 Muga Silk of Assam (Logo) – GI Application No. 384 5. GI Authorised User Applications Bastar Dhokra – GI Application No. 83 6. General Information 7. Registration Process 3 October 30, 2013 OFFICIAL NOTICES Sub: Notice is given under Rule 41(1) of Geographical Indications of Goods (Registration & Protection) Rules, 2002. 1. As per the requirement of Rule 41(1) it is informed that the issue of Journal 52 of the Geographical Indications Journal dated 30th October 2013 / Kartika 07th, Saka 1935 has been made available to the public from 30th October 2013. 4 October 30, 2013 NEW G.I APPLICATION DETAILS App.No. Geographical Indications Class Goods 405 Makrana Marble 19 Natural Goods 406 Salem Mango 31 Horticulture 407 Hosur Rose 31 Agricultural 408 Payyanur Pavithra Mothiram 14 Handicraft 409 Kodali Karuppur Saree 24 & 25 Textile 410 Thammampatti Wood Carvings 20 Handicraft 411 Rajapalayam Lock 6 Manufactured 412 Chamba Painting 16 Handicraft 413 Kangra Paintings 16 Handicraft 414 Punjabi Jutti 25 Handicraft 415 Aipan 16 Handicraft 416 Lahaul & Spiti Wool Weaving 23 Handicraft 417 Lacquer Ware Furniture 20 Handicraft 418 Jhajjar Pottery 21 Handicraft 419 Tamta Copperware Craft 6 Handicraft 420 Rewari Jutti -

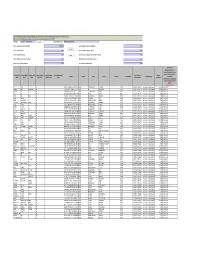

FCL Form IEPF-1

Note: This sheet is applicable for uploading the particulars related to the amount credited to Investor Education and Protection Fund. Make sure that the details are in accordance with the information already provided in e-form IEPF-1 CIN/BCIN L31300MH1967PLC016531 Prefill Company/Bank Name FINOLEX CABLES LIMITED Sum of unpaid and unclaimed dividend 591435.00 Sum of interest on matured debentures 0.00 Validate Sum of matured deposit 0.00 Sum of interest on matured deposit 0.00 Sum of matured debentures 0.00 Clear Sum of interest on application money due for refund 0.00 Sum of application money due for refund 0.00 Redemption amount of preference shares 0.00 Sales proceed for fractional shares 0.00 Sum of Other Investment Types 0.00 Date of event (date of declaration of dividend/redemption date of preference shares/date of Investor First Investor Middle Investor Last Father/Husband Father/Husband Father/Husband Last DP Id-Client Id- Amount Address Country State District Pin Code Folio Number Investment Type maturity of Name Name Name First Name Middle Name Name Account Number transferred bonds/debentures/application money refundable/interest thereon (DD-MON-YYYY) UMA SINGH NA B 30/25 59 MADHAV MARKET LANKAINDIA VARANASI UTTAR PRADESH VARANASI 221005 IN301127-IN301127-15114982Amount for unclaimed and unpaid dividend180.00 09-AUG-2010 SANWAR MAL AGGARWAL NA 15 B D ESTATE TIMARPUR DELHI DELHIINDIA DELHI NEW DELHI 110054 IN301127-IN301127-15118713Amount for unclaimed and unpaid dividend300.00 09-AUG-2010 SANGAM LAL GUPTA NA 23 B ANAND PURI KANPUR, -

Bosch Small Appliance Dealer List.Xlsx

Bosch Home Appliances Stores - India Name Location State Zipcode Telephone NIKSHAN ELECTRONICS ,KNR KANNUR Kerala 670001 9895448669 PLASTA HOME GALARY, KNR KANNUR Kerala 670001 9495895670 HOMZ CENTRE,KNR KANNUR Kerala 670001 9188128098 VASULAL, KNR KANNUR Kerala 670001 9895339669 NANO ELECTRICALS ;THAZHE CHOWA KANNUR Kerala 670001 9847595491 MODERN STEELS, THAZHE CHOWA ,KANNUR KANNUR Kerala 670001 9946229810 CM ASSOCIATES,THAZHE CHOWA ,KANNUR KANNUR Kerala 670001 8606131105 SMART HOMES,MELE CHOWA ,KANNUR KANNUR Kerala 670001 9745227800 OMEGA SALES CORPORATION,THANA, KANNUR KANNUR Kerala 670001 4972706583 NANTIONAL RADIO ELECTRONICS,THANA ,KANNUR KANNUR Kerala 670001 9745233233 PRIMER HOME SHOPPE, KNR KANNUR Kerala 670001 9847215501 YESODHA PLUMBING,CALTEX ,KANNUR KANNUR Kerala 670001 4972703112 POWER HOUSE ,CALTEX,KANNUR KANNUR Kerala 670001 9995884028 BONA AGENCY ,CALTEX,KANNUR KANNUR Kerala 670001 9744006777 YESHOSHA ELECTRICALS,CALTEX ,KANNUR KANNUR Kerala 670001 9895386999 POWER AND SHOWER,THEKKI BAZAR,KANNUR KANNUR Kerala 670001 9447051045 SHAH ELECTRICALS,THEKKI BAZAR,KANNUR KANNUR Kerala 670001 8893512221 ASIAN ELECTRICALS,THEKKI BAZAR,KANNUR KANNUR Kerala 670001 4972767084 RAYZON ,THEKKI BAZAR ,KANNUR KANNUR Kerala 670001 9847155035 MAMATHA ELECTRONICS,THALAP,KANNUR KANNUR Kerala 670001 9995027594 FAAS ELECTRICALS,THALAP,KAANNUR KANNUR Kerala 670001 4972760005 HILIGHT ELECTRICAL KANNUR Kerala 670001 9895678072 FRIENDS ELECTRICALS,OLD BUS STAND ,KANNUR KANNUR Kerala 670001 9447449356 ELECTRIC WORLD,OLD BUS STAND,KANNUR KANNUR Kerala -

District Wise IT@School Master District School Code School Name Thiruvananthapuram 42006 Govt

District wise IT@School Master District School Code School Name Thiruvananthapuram 42006 Govt. Model HSS For Boys Attingal Thiruvananthapuram 42007 Govt V H S S Alamcode Thiruvananthapuram 42008 Govt H S S For Girls Attingal Thiruvananthapuram 42010 Navabharath E M H S S Attingal Thiruvananthapuram 42011 Govt. H S S Elampa Thiruvananthapuram 42012 Sr.Elizabeth Joel C S I E M H S S Attingal Thiruvananthapuram 42013 S C V B H S Chirayinkeezhu Thiruvananthapuram 42014 S S V G H S S Chirayinkeezhu Thiruvananthapuram 42015 P N M G H S S Koonthalloor Thiruvananthapuram 42021 Govt H S Avanavancheri Thiruvananthapuram 42023 Govt H S S Kavalayoor Thiruvananthapuram 42035 Govt V H S S Njekkad Thiruvananthapuram 42051 Govt H S S Venjaramood Thiruvananthapuram 42070 Janatha H S S Thempammood Thiruvananthapuram 42072 Govt. H S S Azhoor Thiruvananthapuram 42077 S S M E M H S Mudapuram Thiruvananthapuram 42078 Vidhyadhiraja E M H S S Attingal Thiruvananthapuram 42301 L M S L P S Attingal Thiruvananthapuram 42302 Govt. L P S Keezhattingal Thiruvananthapuram 42303 Govt. L P S Andoor Thiruvananthapuram 42304 Govt. L P S Attingal Thiruvananthapuram 42305 Govt. L P S Melattingal Thiruvananthapuram 42306 Govt. L P S Melkadakkavur Thiruvananthapuram 42307 Govt.L P S Elampa Thiruvananthapuram 42308 Govt. L P S Alamcode Thiruvananthapuram 42309 Govt. L P S Madathuvathukkal Thiruvananthapuram 42310 P T M L P S Kumpalathumpara Thiruvananthapuram 42311 Govt. L P S Njekkad Thiruvananthapuram 42312 Govt. L P S Mullaramcode Thiruvananthapuram 42313 Govt. L P S Ottoor Thiruvananthapuram 42314 R M L P S Mananakku Thiruvananthapuram 42315 A M L P S Perumkulam Thiruvananthapuram 42316 Govt. -

Kozhikode District Disaster Management Plan

District Disaster Management Plan, 2015 Kozhikode District Disaster Management Plan Published under Section 30 (2) (i) of the Disaster Management Act, 2005 (Central Act 53 of 2005) District Disaster Management Plan 2015 30th July 2016; Pages: 178 This document is for official purposes only. All reasonable precautions have been taken by the District Disaster Management Authority to verify the information and ensure stakeholder consultation and inputs prior to publication of this document. The publisher welcomes suggestions for improved future editions. DISTRICT DISASTER MANAGEMENT PLAN – KOZHIKODE 2015 CONTENTS INTRODUCTION ......................................................................................................................................................................... 4 1.1 VISION .................................................................................................................................................................................4 1.2 MISSION..............................................................................................................................................................................4 1.3 POLICY.................................................................................................................................................................................4 1.4 OBJECTIVES OF THE PLAN ..............................................................................................................................................4 1.5 SCOPE OF THE PLAN -

Kozhikode District 2012-13

List of NGC schools of Kozhikode District 2013-14 Sl.N Head of Name of the School o Institution 1 Headmaster A.S.V.U.P.School, Edakkara P.O, Chellannur (via) Kozhikode 673 616 2 Principal MES Raja Residential School, Kallanthode, NIT Campus PO, Kozhikode 673601 3 Principal Govt. Model H.S.School, Kozhikode- 673 001 4 Headmaster Avalakuttooth Govt. High School, Kottoth, Meppayoor, Kozhikode- 673524 5 Headmaster Azad Memorial U.P. School, P.O. Kumaranellur, Mukkam, Kozhikode-673 602 6 Principal Bharathiya Vidyabhavan School, Ponnyankodekunnu, Chevayur, Kozhikode 7 Principal Sri Guruji Vidhyalaya, Beach Road, Kozhikode 673 032 8 Headmaster Govt. U.P. School Padinjattumuri, P.O. Kizhakkumuri, Kozhikode - 673 611 9 Principal Calicut H.S.School for the Handicapped, Snehanagar, Kolathara, Kozhikode- 10 Headmaster Chennamangallur H.S.School, Chennamangallur P.O, Mukkam, Kozhikode- 11 Headmaster Naduvallur A.U.P.S, Kakkur P.O, Kozhikode-673619 12 Headmaster Chinmaya Vidhyalaya,Nellokode 673016 13 Headmistress NGO Quarters Govt. High School, Merikkunnu P.O, Kozhikode-673012 14 Headmistress Maniyoor U.P.School, P.O.Maniyoor Kozhikode-673523 15 Headmaster Achuthan Girls H.S, Chalappuram, Kozhikode-673002 16 Headmaster G.M.U.P School, Poonoor, Unnikulam P.O, Kozhikode-673 574 17 Headmaster Gov: H.S.S, Kokkallur, Kokkallur P.O, Balussery, Kozhikode-673 612 18 Headmaster G.H.S.S, Puduppady, P.O. Puduppady, Kozhikode -673586 19 Headmaster G.U.P.School, Trikuttissery, Vakayad P.O, Naduvannur (Via), Kozhikode-673614 20 Headmaster Govt: M.U.P.School, Nallalam, Kozhikode-673027 21 Principal G.V.H.S.School for Boys, Quilandy, Kozhikode-673 305 22 Principal G.V.H.S.School, Atholy (P.O), Kozhikode-673 315 23 Principal G.V.H.S School, Kuttichira, Kozhikode-673001 24 Principal G.V.H.S.School, Meenchantha, Kozhikode-673018 25 Principal G.V.H.S School, Meppayoor, Meppayoor P.O, Kozhikode-673524 26 Headmaster Kuttamboor H.S Punnassery P.O, Narikkuni (Via) Kozhikode-673585 27 Principal G.V.H.S School, Payyoli, P.O. -

Regional Transport Authority, Vatakara Agenda for the Rta Meeting to Be Held on 10.07.2019 at Collectorate Conference Hall, Kozhikode

REGIONAL TRANSPORT AUTHORITY, VATAKARA AGENDA FOR THE RTA MEETING TO BE HELD ON 10.07.2019 AT COLLECTORATE CONFERENCE HALL, KOZHIKODE. Present:- 1. Sri.Seeram Sambasiva Rao, IAS, District Collector and Chairman, Regional Transport Authority, Vatakara. 2. Sri.K.G.Simon District Police Chief Kozhikode (Rural) and Member, RTA, Vatakara. 3. Sri.T.C.Vinesh Deputy Transport Commissioner, North Zone, Kozhikode and Member, RTA, Vatakara. Item No: 1 G/10425/2016V Agenda:- 1) To peruse the judgment of Hon’ble STAT in MVAA No. 304/2018 Dtd. 20.12.20 18 and MVARP No.35/2019 dt. 15.06.2019. 2) To consider the modified application for fresh regular stage carriage permit in view of Hon’ble STAT in MVAA No. 304/2018 Dtd. 20.12.2018 MVARP No.35/2019 dt. 15.06.2019 in respect of S/C KL 58 G 7115 to operate on the route Kurumpoyil – Koottalida – Balussery – Kozhikode--Kozhikode Medical College (via) Kannadipoyil, Arapeedika, Manhapalam, Nanmanda, Eranhipalam, Baby Memorial hospital with the following set of timings. Proposed timings. Kurumpoyil Koottalida Balussery Kozhikode Medical College A D A D A D A D A D Start 5.15 05.35 05.40 06.40 08.07 07.42 07.45 06.42 08.25 08.47 08.54 09.54 Pass 10.12 12.14 11.54 Pass 10.31 10.54 10.13 12.45 01.10 01.16 02.16 02.16 02.34 04.25 04.03 Pass 02.53 03.03 02.35 04.30 04.52 04.59 05.59 07.52 07.26 07.30 06.26 08.00 08.16 08.36 halt 08.20 Poonath, Kannadipoil Applicant: Sri. -

National Service Scheme Higher Secondary Education

NATIONAL SERVICE SCHEME HIGHER SECONDARY EDUCATION SPECIAL CAMP 2013-14 THIRUVANANTHAPURAM Name of Name of Principal Sl Programme Officer with Date & Venue of Camp Travel Route Name of School No with Phone No Phone No. P.R.William HSS, Kattakkada, Anupama Stanlo John D 21.12.13 to 27.12.13 1 Kattakada - Neyyardam Thiruvananthapuram 9496818170 9495493045 Govt.LPS, Thottampara Govt.V&HSS, Parassala, Shinju Nath P.R T.R.Sundaresan 22.12.13 to 28.12.13 Parassala to Chenkkavila 2 Thiruvananthapuram 9447089562 9495746981 Govt.K.V.H.S Ayira (Via Poovar) - Ayira 22.12.13 to 28.12.13 Govt.HSS, Venjaranmoodu, Ramani.S.S Hari Kumar.G 3 Govt.UPS Alanthara, From Alanthara – 0.5Km Thiruvananthapuram 0472 2871423 9447586654 Venjaramood 22.12.13 to 28.12.13 The Neyyatinkara – St.Johns HSS, Undancode, Biju Kumar.J Sadanandan T Swiss Central School Karakkonam – 4 Trivandrum 9946312266 9495407253 Elluvila P.O, Nilamammood- Karakkonam viamkulam- Swiss school 22.12.13 to 28.12.13 Baiju S Usha.S Kilimanoor – Paripally 5 Govt.HSS, Kilimanoor, Trivandrum RRV Girls HSS 9656646242 9446751850 route Kilimanoor Govt.V&HSS For Girls, Manacaud, M.R. Helan Rajam Satheesh Chandran 22.12.13 to 28.12.13 Manacaud – Palayam- 6 Trivandrum 9497692824 9447653975 Govt. Model Girls PMG - Pattom H.S.S.Pattom Nedumangadu – Iqbal HSS, Peringamala, Leena Raseena.A 21.12.13 to 27.12.13 Vembayam- 7 Thiruvanathapuram 9846682887 9446965937 Govt.HSS Neduveli Kanniakulangara- Neduveli 22.12.13 to 28.12.13 Govt.HSS, Kamaleswaram, Sindhu G Nair P.Muraleedharan Govt.Girls HSS, 8 East Fort - Peroorkada Manacaud, Thiruvananthapuram 9495729039 Nair 9447964587 Peroorkada, Ambalamukku St.Johns Model HSS, Nalanchira, Shiju.T T.K.Sunny 21.12.13 to 27.12.13 Kesavadasapuram - 9 Thiruvananthapuram 9400620804 9447107390 St.Mary’s HSS, Pattom Pattom 21.12.13 to 27.12.13 Leju P Thomas Fr.Dr.Varkey A.V., Nalanchira Main gate – 10 St.