Tennessee's Equine Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Joseph Battell and the Morgan Horse

Story by Amanda Kay Gustin Photos courtesy of the Vermont Historical Society VERMONT HISTORY Joseph Battell and the Morgan Horse Joseph Battell held forth that the Morgan horse-not the Standardbred-was the true trotting racehorse of America. EW VERMONTERS HAVE HAD AS VARIED AN number of business ventures including real estate investment, impact on the history of the state as Joseph Batte!!. As a publishing the Middlebury Register, and operating the Bread Fbusinessman, philanthropist, author, innkeeper, newspa Loaf Inn in Ripton. per publisher, and finally horse breeder, his life touched Joseph had been a horseman all his life, and he viewed nearly every aspect oflife in Vermont in the 19th the coming age of the automobile- a "murdering and 20th centuries. monster destroying the peace of the fo rest with Born in Middlebury in July 1839, Jo its thunder and bringing in crowds of peo seph was the son of Philip Battell and ple" -with concern and no small amount ·; Emma Seymour, both themselves of disdain. His Middlebury Register of scions of well-connected families. ten carried page after page of notices Emma's father was Horatio Sey of gruesome accidents collected from mour, who had served as one papers across the country, and he of Vermont's earliest United tried to have legislation passed fo r States senators, and she was bidding automobiles from using among Middlebury's most public roads in Middlebury. He eligible young women. Philip did not allow any automobiles at came to Vermont as part of the Bread Loaf Inn. He preferred the Middlebury College class the pace and aesthetic benefits of of 1826. -

School of Rack

By Elizabeth Graves, ©2007 Feeling a little bored? Nothing really that gives you that pizzazz these days? Looking for the new horsy adventure? I may just have the answer for you! © Liz Graves Yankee, a Rocky Mountain Horse, owned and ridden by John Koomar performs one of the racking gaits. Ah, but which one? A Racking horse just may be the What They Have in ing effect of the fore legs. The hind answer to zipping up your life. Common hooves work with more up-and- They come in every color, shape, EACHVARIATION IS EVEN IN TIMING; down action, creating a bobbing of size, can be found in a variety of you can hear an even 1-2-3-4, four- the hindquarters and tail head. The head is carried still, or with just breeds, and are common in the beat timing as each hoof hits the ground. However, even though they a slight poll-based bob, but no up- new designer horses - those are even in set-down, racking gaits and-down headshake or side-to-side crosses of two or more gaited are often called lateral gaits because motion of the head will exist. breeds. There’s something for the hooves on the same side (later- Each gait is smooth to ride with everyone, from a slower, al) of the horse pick up almost in just a slight side-to-side vibration in steady-Eddy kind of horse to unison. An exception is the fox the pelvis and tailbone of the rider. one that gets up and covers lots rack, which is diagonal in pick-up There is a rolling transfer of weight from one hoof to another in the of ground fast, for the thrill you and even in set-down. -

List of Horse Breeds 1 List of Horse Breeds

List of horse breeds 1 List of horse breeds This page is a list of horse and pony breeds, and also includes terms used to describe types of horse that are not breeds but are commonly mistaken for breeds. While there is no scientifically accepted definition of the term "breed,"[1] a breed is defined generally as having distinct true-breeding characteristics over a number of generations; its members may be called "purebred". In most cases, bloodlines of horse breeds are recorded with a breed registry. However, in horses, the concept is somewhat flexible, as open stud books are created for developing horse breeds that are not yet fully true-breeding. Registries also are considered the authority as to whether a given breed is listed as Light or saddle horse breeds a "horse" or a "pony". There are also a number of "color breed", sport horse, and gaited horse registries for horses with various phenotypes or other traits, which admit any animal fitting a given set of physical characteristics, even if there is little or no evidence of the trait being a true-breeding characteristic. Other recording entities or specialty organizations may recognize horses from multiple breeds, thus, for the purposes of this article, such animals are classified as a "type" rather than a "breed". The breeds and types listed here are those that already have a Wikipedia article. For a more extensive list, see the List of all horse breeds in DAD-IS. Heavy or draft horse breeds For additional information, see horse breed, horse breeding and the individual articles listed below. -

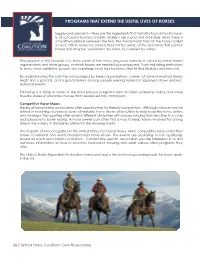

Programs That Extend the Useful Lives of Horses

PROGRAMS THAT EXTEND THE USEFUL LIVES OF HORSES: Supply and demand — they are the ingredients that form the foundation for near- ly all successful business models. Markets are sound and profitable when there is a healthy balance between the two. The theory holds true for the horse market as well. Often, however, owners may not be aware of the demands that exist for horses that may be “unwanted” by some, but desired by others. The purpose of this chapter is to show some of the many programs already in place by horse breed organizations and other groups, in which horses are needed by participants. From trail riding enthusiasts to horse show exhibitors, people are searching every day for horses that fit their lifestyles and interests. By understanding the activities encouraged by breed organizations, owners of some unwanted horses might find a good fit, and a good market, among people seeking horses for organized shows and rec- reational events. Following is a listing of some of the most popular programs and activities underway today and some true-life stories of unwanted horses that developed into champions. Competitive Horse Shows: Nearly all horse breed associations offer opportunities for friendly competition. Although a horse may be retired or reaching advanced years of maturity, horse shows offer outlets to help keep the horse active and involved. The registries offer several different disciplines with classes ranging from leadline to saddle seat pleasure to barrel racing. A horse owner can often find a way to keep horses involved for a long time in the variety of disciplines offered in the showing world. -

Electronic Supplementary Material - Appendices

1 Electronic Supplementary Material - Appendices 2 Appendix 1. Full breed list, listed alphabetically. Breeds searched (* denotes those identified with inherited disorders) # Breed # Breed # Breed # Breed 1 Ab Abyssinian 31 BF Black Forest 61 Dul Dülmen Pony 91 HP Highland Pony* 2 Ak Akhal Teke 32 Boe Boer 62 DD Dutch Draft 92 Hok Hokkaido 3 Al Albanian 33 Bre Breton* 63 DW Dutch Warmblood 93 Hol Holsteiner* 4 Alt Altai 34 Buc Buckskin 64 EB East Bulgarian 94 Huc Hucul 5 ACD American Cream Draft 35 Bud Budyonny 65 Egy Egyptian 95 HW Hungarian Warmblood 6 ACW American Creme and White 36 By Byelorussian Harness 66 EP Eriskay Pony 96 Ice Icelandic* 7 AWP American Walking Pony 37 Cam Camargue* 67 EN Estonian Native 97 Io Iomud 8 And Andalusian* 38 Camp Campolina 68 ExP Exmoor Pony 98 ID Irish Draught 9 Anv Andravida 39 Can Canadian 69 Fae Faeroes Pony 99 Jin Jinzhou 10 A-K Anglo-Kabarda 40 Car Carthusian 70 Fa Falabella* 100 Jut Jutland 11 Ap Appaloosa* 41 Cas Caspian 71 FP Fell Pony* 101 Kab Kabarda 12 Arp Araappaloosa 42 Cay Cayuse 72 Fin Finnhorse* 102 Kar Karabair 13 A Arabian / Arab* 43 Ch Cheju 73 Fl Fleuve 103 Kara Karabakh 14 Ard Ardennes 44 CC Chilean Corralero 74 Fo Fouta 104 Kaz Kazakh 15 AC Argentine Criollo 45 CP Chincoteague Pony 75 Fr Frederiksborg 105 KPB Kerry Bog Pony 16 Ast Asturian 46 CB Cleveland Bay 76 Fb Freiberger* 106 KM Kiger Mustang 17 AB Australian Brumby 47 Cly Clydesdale* 77 FS French Saddlebred 107 KP Kirdi Pony 18 ASH Australian Stock Horse 48 CN Cob Normand* 78 FT French Trotter 108 KF Kisber Felver 19 Az Azteca -

Parts of the Horse Poll Crest Forehead Face Bridge Withers Point of Hip of Nose Loin Croup Nostril Neck Back

American Paint Horse Association Parts of the Horse Poll Crest Forehead Face Bridge Withers Point of Hip of Nose Loin Croup Nostril Neck Back Muzzle Jaw Throat Latch Shoulder Point of Shoulder Barrel Flank Chest Girth Stifle Elbow Abdomen Gaskin Forearm Chestnut Knee Hock Cannon Fetlock Hoof Coronet Pastern Abdomen (belly)—area between the ribs Crest —top part of the neck, from the ears Gaskin —muscle above the hock Pastern —located between the fetlock and and the stifle, contains the digestive system to the withers; where the mane grows Girth —just behind the front leg where the the hoof Back —upper portion of the barrel, Croup —upper part of the hindquarters girth of a saddle is situated Point of Hip —bone projecting on both between the withers and the loins between the loin and the tail Hock —joint between the gaskin and the sides of the hindquarters, located Barrel —trunk of the horse Elbow —projected joint above the forearm hind cannon bone between the loin and the croup Point of Shoulder —bone protruding from Bridge of Nose —bony portion of the face and in front of the girth Hoof —horny growth that protects the the shoulder, toward the chest between the forehead and the muzzle Face —part of the head from the forehead lower limb/foot to the muzzle Poll —part of the head, at the top of the Cannon —bone that lies between the knee Jaw —large rounded area under the eye and the fetlock on the front leg, and the Fetlock —joint where the cannon bone neck and between the ears Knee —joint located between the forearm hock and the fetlock on -

Show Logo Goes Here

RALEIGH INVITATIONAL HORSE SHOW 4601 Trinity Road Raleigh, North Carolina 27607 INDOOR ARENA APRIL 9 – 11, 2020 AFFILIATED WITH: Carolina Summer Circuit American Saddlebred Horse Association Star Show American Saddlebred Assoc. of the Carolinas American Saddlebred Association of Virginia East Tennessee Saddlebred Association Judge - Sarah Russell Entry Closing Date without penalty March 23, 2020 www.RaleighInvitational.com Hampton Inn & Suites Raleigh/Cary Raleigh Invitational Horse Show Hotel is only 2 miles from the Hunt Horse Complex and NC State Fairgrounds Ask for the Hunt Horse Complex Rates 1 King Bed with Sleeper Sofa - $97.00 + Tax 2 Queen Beds - $97.00 + Tax King Suites - $122.00 + Tax All rooms equipped with a Refrigerator and Microwave High Speed Wireless Internet Complimentary On the House Breakfast Buffet Served Daily from 6 am -10 am Coin Operated Laundry Facility Outdoor Salt Water Swimming Pool Surrounded by Lush Landscaping Two Gas Barbecue Grills Pet Friendly with no extra deposit required Pet Exercise Area 111 Hampton Woods Lane Raleigh, NC 27607 919.233.1798 www.carysuites.hamptoninn.com 1520 Blue Ridge Rd. Raleigh NC 27607 Phone: 919.832.4100 fax: 919.828.1796 www.ramadaraleigh.com Raleigh Invitational Horse Show $79.00 plus tax per night King or Double Queen* The Ramada is centrally located near the intersection of Wade Avenue and Blue Ridge Road, making major businesses and attractions just moments away. The RBC Center, State Fairgrounds & Hunter Horse Complex, Carter Finley Stadium, NC Museum of Art, NC State Veterinary School and NCSU are less than a minutes’ drive. If you are in the mood to shop, Crabtree Valley Mall offers a huge selection of choices from over 220 stores and is less than five miles away. -

Morgan Horses

The 12th Annual NATIONAL MORGAN HORSE SHOW Sponsored by: Saturday Evening Friday Evening 7:00 P. M. 7:00 P. M. Sunday Saturday Afternoon Afternoon 1:00 P. M. 1:00 P. M. PERFORMANCE BREED CLASSES CLASSES For Stallions and Saddle, Harness, Mares: Colts and Pleasure. Utility Fillies and Equitation THE MORGAN HORSE CLUB Watch The Foundation Breed of America Perform. TRI-COUNTY FAIR GROUNDS NORTHAMPTON, MASS. July 30, 31 and August 1, 1954 Adults $1.00 Children - under 12 - 50' A LAW FOR IT . by 1939 Vermont Legislature "There oughta be a law agin it," is a favorite expresion of Vermonters. Sometimes they reverse themselves and make a law "for it" as they did in 1939 when the legislature passed the following resolution: "Whereas, this is the year recognized as the 150th anniversa y of the famous horse 'Justin Morgan,' which horse not only established a recognized breed of horses named for a single individual, but brought fame th•tzugh his descendants to Vermont and thousands of dollars to Vermonters. "The name Morgan has come to mean beauty, spirit, and action to all lovers of the horse; and the Morgan horses fo• many years held the world's record for trotting horses, and "Whereas the Morgan blood is recognized as foundation stock for the American Saddle Horse, for the American Trotting Horse, and for the Tennessee Walking Horse. In each of these three breeds, the Morgan horse is recognized as a foundation, and therefore, with the recognition of its value to the horse b seeders of the nation, and recognition that it was in Vermont that Morgan -

AHC PAST Act Frequently Asked Questions

PREVENT ALL SORING TACTICS ACT OF 2013 (H.R. 1518) Frequently Asked Questions What is the Horse Protection Act and why was it enacted? The Horse Protection Act (HPA or Act) is a federal law that was passed in 1970 to stop the cruel practice of “soring” horses that was occurring in sectors of the horse show industry, primarily the Tennessee Walking Horse and Racking Horse industry. In the 1950s, some horse owners and trainers who wanted to improve their horses’ chances of winning began to sore their horses as a shortcut in place of longer and more conventional training methods. As this practice spread, public concern over the practice led to the passage of the federal law. What activities does it prohibit? The federal law prohibits the showing, sale, auction, exhibition, or transport of horses that have been “sored.” The HPA was passed in 1970 in response to the growing practice of soring of horses to cultivate an accentuated gait on some horses for showing or sale. The Act and its enforcement have traditionally been aimed at those sectors of the walking horse show industry that push for a particularly accentuated gait, known as the “big lick” or “performance” gait, while showing. What is soring? According to the U.S. Department of Agriculture, Animal and Plant Health Inspection Service (USDA or the Department) the agency that enforces the HPA: “Soring is a cruel and inhumane practice used to accentuate a horse’s gait. Soring may be accomplished by irritating or blistering a horse’s forelegs through the injection or application of chemicals or mechanical devices that cause irritation. -

Now, That's a Walking Horse!

Now, That’s a Walking Horse! 2018 Grant and Recognition Program Rewarding Amateur Owners and Riders using Tennessee Walking Horses in new/non-traditional ways and multi-breed environments Encouraging and supporting therapeutic and natural horsemanship programs and clinics and public promotion of the breed APPLICATION COVER SHEET Please type or print legibly Name of Rider/Applicant Gender: M/F____ Age range: Youth (18 or under) ____ 19-30____31-45____46-65____ 66- 80____81+____ Name of Horse Owner (if different) Applicant Street Address: City: State: Zip: Home Phone: Cell: E-Mail: Name of Horse Used in this Activity (use separate sheet to list multiple horses used in therapeutic horsemanship or public promotion programs): Registration #: Gender: G/S/M Birthdate: ___/___/____ Check One. 1. I am applying for a recognition award in the following category (use separate applications for multiple categories): _____Dressage (incl. Western or Cowboy Dressage) _____ Jumping _____Gymkhana events (i.e. barrel racing, pole bending) _____Reining _____Driving _____Endurance or Distance Riding _____Competitive Trail Riding/ Judged Trail Rides _____Trail Obstacle Competitions _____Natural Horsemanship Competitions _____Cowboy Mounted Shooting _____Vaulting _____Agility Training/Competition 2. I am applying for a grant in the following category: Equipment or sponsorship for riders or upkeep of horses in a non-profit therapeutic horsemanship program at (name of center or establishment) Hosting or organizing a natural horsemanship clinic with (name of clinician) -

Rulebook21.Pdf

APPALOOSA A HORSE FOR ALL REASONS 2 0 2 Share your reasons with us at [email protected] 1 RIDE WITH US into the NEW DECADE ApHC DIRECTORY The Appaloosa Horse Club is on Pacific Time, three hours behind New York, two hours behind Texas, one hour behind Colorado, in the same time zone as California. Business hours are 8 a.m. to 5 p.m., Monday through Friday. Administration Member Services Executive Secretary— Membership information ext. 500 Lynette Thompson ext. 249 [email protected] [email protected] Administrative Assistant— Museum [email protected] www. appaloosamuseum.org [email protected] Director— Crystal White ext. 279 Accounting [email protected] Treasurer— Keith Ranisate ext. 234 Racing Coordinator— Keri Minden-LeForce ext. 248 Appaloosa Journal [email protected] [email protected] Editor— Registration Dana Russell ext. 237 General information ext. 300 [email protected] Registry Services— Advertising Director— [email protected] Hannah Cassara ext. 256 [email protected] Performance General Information ext. 400 Art/Production Director— Barbara Lawrie Performance Department Supervisor— [email protected] Keri Minden-LeForce ext. 248 [email protected] Graphic Designer & Circulation Manager— Judge Coordinator and Show Secretary— Jonathan Gradin ext. 258 Debra Schnitzmeier ext. 244 (circulation & subscriptions, address [email protected] changes, missing & damaged issues, Appaloosa Journal Online) [email protected] [email protected] Show Results/Show Approvals— [email protected] Deb Swenson ext. 265 [email protected] Information Technnology ACAAP— Information Technology Supervisor— Amber Alsterlund ext. 264 Dave O’ Keefe ext. 251 [email protected] [email protected] Trail & Distance Coordinator— [email protected] ext. 221 Marketing Marketing/Public Relations Director— Youth Programs Hannah Cassara ext. -

The Ambling Influence.Pdf

THE AMBLING INFLUENCE end up in the ASB PART 1 The American Saddlebred Horse is famous for his Cave drawings from the Steppes of Asia (http://www.spanishjennet.org/history.shtml). gaits, but where do these gaits come from? Gaited horses have been around for many years, but how did they end up in the American Saddlebred? This series of articles will take you from the dawn of the gaited horse through to the modern day Saddlebred, look at the genetics behind the ambling gait and give you some pointers as to the physique of the gaited horse. What is a gaited horse anyway? Every pace of the horse, be it walk, trot or canter, is called a “gait”. For the gaited enthusiast, any horse can do these gaits, what they are interested in is the smooth non-jarring English palfrey, cc 1795 – 1865. lateral gait (the legs on one side moving together). (http://www.1st-art-gallery.com/John- This “gait” comes in many guises and names Frederick-Herring-Snr/My-Ladye's-Palfrey.html). depending on the collection, speed and length of stride of the horse, as well as the individual breed of the horse. It is the specific pattern of footfall and the cadence that defines the gait in each of the gaited breeds. A quiet horse may well have a better gait than his flashy fast-moving counterpart, so look beyond the hype and see exactly what those feet and hindquarters are doing. This smooth-moving gait has been depicted in cave walls and fossilised in footprints dating to over 3½ million years ago – so just how did it get from there Lady Conaway's Spanish Jennet to the American Saddlebred? We know that horses (http://www.spanishjennet.org/registry.shtml) are not native to America, so to answer that question we must travel back in time and place to Europe and Asia.