Rwanda Cross-Border Agricultural Trade Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

STATEMENT by H.E. Yoweri Kaguta Museveni President of the Republic

STATEMENT by H.E. Yoweri Kaguta Museveni President of the Republic of Uganda At The Annual Budget Conference - Financial Year 2016/17 For Ministers, Ministers of State, Head of Public Agencies and Representatives of Local Governments November11, 2015 - UICC Serena 1 H.E. Vice President Edward Ssekandi, Prime Minister, Rt. Hon. Ruhakana Rugunda, I was informed that there is a Budgeting Conference going on in Kampala. My campaign schedule does not permit me to attend that conference. I will, instead, put my views on paper regarding the next cycle of budgeting. As you know, I always emphasize prioritization in budgeting. Since 2006, when the Statistics House Conference by the Cabinet and the NRM Caucus agreed on prioritization, you have seen the impact. Using the Uganda Government money, since 2006, we have either partially or wholly funded the reconstruction, rehabilitation of the following roads: Matugga-Semuto-Kapeeka (41kms); Gayaza-Zirobwe (30km); Kabale-Kisoro-Bunagana/Kyanika (101 km); Fort Portal- Bundibugyo-Lamia (103km); Busega-Mityana (57km); Kampala –Kalerwe (1.5km); Kalerwe-Gayaza (13km); Bugiri- Malaba/Busia (82km); Kampala-Masaka-Mbarara (416km); Mbarara-Ntungamo-Katuna (124km); Gulu-Atiak (74km); Hoima-Kaiso-Tonya (92km); Jinja-Mukono (52km); Jinja- Kamuli (58km); Kawempe-Kafu (166km); Mbarara-Kikagati- Murongo Bridge (74km); Nyakahita-Kazo-Ibanda-Kamwenge (143km); Tororo-Mbale-Soroti (152km); Vurra-Arua-Koboko- Oraba (92km). 2 We are also, either planning or are in the process of constructing, re-constructing or rehabilitating -

Speech to Parliament by H.E. Yoweri Kaguta Museveni President of The

Speech to Parliament By H.E. Yoweri Kaguta Museveni President of the Republic of Uganda Parliamentary Buildings - 13th December, 2012 1 Rt. Hon. Speaker, I have decided to use the rights of the President, under Article 101 (2) of the 1995 Constitution of the Republic of Uganda, to address Parliament. I am exercising this right in order to counter the nefarious and mendacious campaign of the foreign interests, using NGOs and some Members of Parliament, to try and cripple or disorient the development of the Oil sector. If the Ugandans may remember, this is not the first time these interests try to distort the development of our history. When we were fighting the Sudanese-sponsored terrorism of Kony or when we were fighting the armed cattle- rustlers in Karamoja, you remember, there were groups, including some religious leaders, Opposition Members of Parliament as well as NGOs, which would spend all the 2 time denouncing us, the Freedom Fighters. They were denouncing those who were fighting to defend the lives and properties of the people, rather than denouncing the terrorists, the cattle-rustlers and their external-backers (in the case of Kony) as well as their internal collaborators. It would appear as if the wrong-doer was the Government, the NRM, rather than the criminals. We, patiently, put up with that malignment at the same time as we fought, got injured or killed, against the enemy until we achieved victory. Eventually, we won, supported by the ordinary people and the different people’s militias. There is total peace in the whole country and yet the misleaders of those years have not apologized to the Ugandans for their mendacity. -

Esoko Corporate Strategy

Agribusiness developments in Ghana: Japan-Ghana partnerships opportunities GIPC Japan Investment Seminar Daniel Asare-Kyei, PhD July 2021 Esoko 2021 | Private & Confidential Africa’s population boom, a challenge and an opportunity • Currently 70% of Africa’s population are engaged in Agriculture • Many of whom are smallholder farmers cultivating less than 2 hectares • These smallholders produce 80% of food consumption • Africa’s food market is now estimated at $300B, projected to rise to $1trillion by 2030 • Demand for food is expected to double by 2050 • At the same time, Africa’s food import bill ranges between $30B to $50B per annum • Ghana’s population is projected to grow to between 52M to 65M by 2050 according to GSS Esoko 2021 | Private & Confidential That means, in just 29 growing seasons, Ghana’s 4 million small farms must learn to feed about 30M more people while facing: Demographic shift; Rapid changes in Increased Weather Variability/ Information Gap lack of adequate Lack of Field-Level insight to prevent Climate Changes rendering farm populations, shits from data across the value chain making it risk and improve production traditional practices non attractive to financial agriculture to services & industry ineffective and increasing institutions, the youth and investors sectors and rural-urban migration risk in farming Esoko 2021 | Private & Confidential Ghana Agriculture overview ✓ ✓ ✓ ✓ ✓ Esoko 2021 | Private & Confidential Areas of significant investment opportunities for Ghana & Japan partnerships Esoko 2021 | Private & Confidential Opportunities abound in both the input and output segments Credit disbursement Value addition and Cold chain storage, transport especially through processing and associated logistics digital channels Underpin by digital technologies powered by Agritech & Fintech companies Esoko 2021 | Private & Confidential Commodity value chains presents the best low hanging fruits… Ghana spends about US$2 billion each year on food imports. -

Land Use Change and Soil Degradation in the Southwestern Highlands of Uganda

LAND USE CHANGE AND SOIL DEGRADATION IN THE SOUTHWESTERN HIGHLANDS OF UGANDA Simon Bolwig A Contribution to the Strategic Criteria for Rural Investments in Productivity (SCRIP) Program of the USAID Uganda Mission The International Food Policy Research Institute 2033 K Street, N.W. Washington, D.C. 20006 September 2002 Strategic Criteria for Rural Investments in Productivity (SCRIP) is a USAID-funded program in Uganda implemented by the International Food Policy Research Institute (IFPRI) in collaboration with Makerere University Faculty of Agriculture and Institute for Environment and Natural Resources. The key objective is to provide spatially-explicit strategic assessments of sustainable rural livelihood and land use options for Uganda, taking account of geographical and household factors such as asset endowments, human capacity, institutions, infrastructure, technology, markets & trade, and natural resources (ecosystem goods and services). It is the hope that this information will help improve the quality of policies and investment programs for the sustainable development of rural areas in Uganda. SCRIP builds in part on the IFPRI project Policies for Improved Land Management in Uganda (1999-2002). SCRIP started in March 2001 and is scheduled to run until 2006. The origin of SCRIP lies in a challenge that the USAID Uganda Mission set itself in designing a new strategic objective (SO) targeted at increasing rural incomes. The Expanded Sustainable Economic Opportunities for Rural Sector Growth strategic objective will be implemented over the period 2002-2007. This new SO is a combination of previously separate strategies and country programs on enhancing agricultural productivity, market and trade development, and improved environmental management. Contact in Kampala Contact in Washington, D.C. -

First Laboratory-Confirmed Outbreak of Human and Animal Rift Valley

Am. J. Trop. Med. Hyg., 100(3), 2019, pp. 659–671 doi:10.4269/ajtmh.18-0732 Copyright © 2019 by The American Society of Tropical Medicine and Hygiene First Laboratory-Confirmed Outbreak of Human and Animal Rift Valley Fever Virus in Uganda in 48 Years Trevor R. Shoemaker,1,2* Luke Nyakarahuka,3,4 Stephen Balinandi,1 Joseph Ojwang,5 Alex Tumusiime,1 Sophia Mulei,3 Jackson Kyondo,4 Bernard Lubwama,6 Musa Sekamatte,6 Annemarion Namutebi,7 Patrick Tusiime,8 Fred Monje,9 Martin Mayanja,3 Steven Ssendagire,6 Melissa Dahlke,10 Simon Kyazze,10 Milton Wetaka,10 Issa Makumbi,10 Jeff Borchert,5 Sara Zufan,2 Ketan Patel,2 Shannon Whitmer,2 Shelley Brown,2 William G. Davis,2 John D. Klena,2 Stuart T. Nichol,2 Pierre E. Rollin,2 and Julius Lutwama3 1Viral Special Pathogens Branch, Centers for Disease Control and Prevention-Uganda, Entebbe, Uganda; 2Viral Special Pathogens Branch, Centers for Disease Control and Prevention, Atlanta, Georgia; 3Department of Arbovirology, Emerging and Reemerging Infectious Diseases, Uganda Virus Research Institute, Entebbe, Uganda; 4Department of Biosecurity, Ecosystems and Veterinary Public Health, College of Veterinary Medicine, Animal Resources and Biosecurity, Makerere University, Kampala, Uganda; 5Global Health Security Unit, Centers for Disease Control and Prevention-Uganda, Kampala, Uganda; 6Ministry of Health, Kampala, Uganda; 7Kabale Regional Referral Hospital, Kabale, Uganda; 8Kabale District Health Office, Kabale, Uganda; 9Ministry of Agriculture, Animal Industry and Fisheries, Kampala, Uganda; 10Public Health Emergency Operations Centre, Ministry of Health, Kampala, Uganda Abstract. In March 2016, an outbreak of Rift Valley fever (RVF) was identified in Kabale district, southwestern Uganda. -

Kabale District HRV Profile.Pdf

Kabale District Hazard, Risk and Vulnerability Profi le 2016 KABALE DISTRICT HAZARD, RISK AND VULNERABILITY PROFILE a Acknowledgement On behalf of Office of the Prime Minister, I wish to express my sincere appreciation to all of the key stakeholders who provided their valuable inputs and support to this Multi-Hazard, Risk and Vulnerability mapping exercise that led to the production of comprehensive district Hazard, Risk and Vulnerability (HRV) profiles. I extend my sincere thanks to the Department of Relief, Disaster Preparedness and Management, under the leadership of the Commissioner, Mr. Martin Owor, for the oversight and management of the entire exercise. The HRV assessment team was led by Ms. Ahimbisibwe Catherine, Senior Disaster Preparedness Officer supported by Ogwang Jimmy, Disaster Preparednes Officer and the team of consultants (GIS/DRR specialists); Dr. Bernard Barasa, and Mr. Nsiimire Peter, who provided technical support. Our gratitude goes to UNDP for providing funds to support the Hazard, Risk and Vulnerability Mapping. The team comprised of Mr. Steven Goldfinch – Disaster Risk Management Advisor, Mr. Gilbert Anguyo - Disaster Risk Reduction Analyst, and Mr. Ongom Alfred- Early Warning system Database programmer. My appreciation also goes to Kabale District Team. The entire body of stakeholders who in one way or another yielded valuable ideas and time to support the completion of this exercise. Hon. Hilary O. Onek Minister for Relief, Disaster Preparedness and Refugees KABALE DISTRICT HAZARD, RISK AND VULNERABILITY PROFILE i EXECUTIVE SUMMARY The multi-hazard vulnerability profile outputs from this assessment was a combination of spatial modeling using socio-ecological spatial layers (i.e. DEM, Slope, Aspect, Flow Accumulation, Land use, vegetation cover, hydrology, soil types and soil moisture content, population, socio-economic, health facilities, accessibility, and meteorological data) and information captured from District Key Informant interviews and sub-county FGDs using a participatory approach. -

Supporting Affordable and Green Buildings in Kigali/Rwanda

Kafunzo Merama Kagitumba Lake Mutanda Lake Bunyonyi Rwempasha Lubirizi Rutshuru Kisoro Nyagatare Cyanika Kabale a K b ag BIRUNGA m era u Butaro t NAT'L PARK Muvumba i g Kidaho Lac a Katuna K Lac Burera Rwanyakizinga Ruhengeri Mulindi Gatunda Lac Kirambo Cyamba Busogo Ruhondo Gabiro AKAGERA Byumba Ngarama Lac Kora NORRE NATIONAL Mikindi Mutura NORD PARK Lake Kagali Kinihira Lac Hago Mujunju Goma Nemba Gisenyi Rushashi Kinyami EST Muhura Nyundo Kabaya N Lac y Rutare Ngaru a Mbogo Murambi Kivumba ba Lac Rukara GISHWATI ro ng Shyorongi Muhazi NATURAL Ngororero Lac Ile Ihema Bugarura RESERVE Kiyumba KIGALI OUEST Kigali Rwamagana Ile Wahu Runda Gikoro Bulinga Kayonza Lac Lac Kicukiro Bicumbi Nasho Kivu Mabanza Lac SUPPORTING AFFORDABLE AND Gitarama Butamwa Kigarama Mugesera Lac Lake Ile Kibuye Mpanga Bisongou Birambo Lac Idjwi Mugesera Kibungo Cyambwe Gishyita Bwakira SUD Rilima Rukira Rwamatamu Masango Ruhango Sake Gashora Rusumo Gatagara Bare Nemba Kirehe Kaduha K Nyanza Ngenda ag Ile er Gombo Rwesero a Karaba Lac Lac Rusatira Cyohoha Rweru Kamembe Gisakura Gikongoro Sud Karama Bukavu Cyangugu Rwumba Kitabi Cyimbogo Karengera GREEN BUILDINGS IN KIGALI/RWANDA NYUNGWE Nyakabuye Bugumya NAT'L PARK Butare Ruramba Gisagara u r Busoro a y Bugarama n Munini ka A The boundaries and names shown and the designations used Runyombyi on this map do not imply official endorsement or acceptance by the United Nations. Map No. 3717 Rev. 11 UNITED NATIONS Department of Field Support July 2015 Geospatial Information Section (formerly Cartographic Section) Rwanda’s housing challenge Building materials and their environmental Impact analysis by building material type Rwanda’s National Housing Policy which was rolled out in impacts The impacts of exterior wall construction using nine locally available materials were compared and assessed relative to their share March 2015 aims at fast-tracking affordable housing projects The choice of building materials during the upgrading of of the city-wide flows in 2015. -

The Ict Market in Ivory Coast 2015

THE ICT MARKET IN IVORY COAST 2015 I - MARKET OVERVIEW The Ivory Coast is the second largest economy in Africa and the largest economy in the West African Economic and Monetary Union (UEMOA). Since 2011 the Ivory Coast has registered remarkable growth. Indeed, GDP growth was at 8.8% in 2013 and 9.2% in the third quarter of 2014. This positive performance comes after years of sluggish performance and was facilitated by many factors mainly the devaluation of the CFA franc, higher cocoa and coffee prices, growth in non-traditional primary exports such as pineapples and rubber, debt relief and rescheduling, as well as the discovery of oil and gas reserves. The Ivory Coast records the 4th highest growth rate amongst African countries, with an average annual FDI growth rate of 43.1%, between 2007-2012. Lebanon is Ivory Coast’s leading investor. Capital Yamoussoukro Largest city Abidjan Government Presidential Republic Currency West African CFA franc (XOF) Official language French Area 322,463 km2 Population 22,848,945 (July 2014 est.) Calling code +225 Economic snapshot 2009 2010 2011 2012 2013 2014 GDP (% annual growth rate) 3.7 2.4 -4.7 9.5 9.5 9.9(Q3) Exports of goods and services (% of GDP) 50.7 50.5 53.8 48.4 48.4 - Imports of goods and services (% of GDP) 39.8 43.2 37.3 44.2 44.2 - ICT goods imports (% total goods imports) 3.9 3.3 3.1 2.5 2.5 - CONTENT Inflation (annual %) 1.0 1.7 4.9 1.3 1.3 - Exchange rate (per USD) 472.2 495.3 471.9 510.5 510.5 494.4 I. -

Review of Agricultural Market Information Systems in Sub-Saharan Africa

Review of agricultural market information systems in sub-Saharan Africa Maryben Chiatoh, Amos Gyau Review of agricultural market information systems in sub-Saharan Africa Maryben Chiatoh, Amos Gyau LIMITED CIRCULATION Correct citation: Chiatoh M, Gyau A. 2016. Review of agricultural market information systems in sub-Saharan Africa. ICRAF Working Paper no. 235. Nairobi, World Agroforestry Centre. DOI: http://dx.doi.org/10.5716/WP16110.PDF Titles in the working paper series aim to disseminate interim results on agroforestry research and practices and stimulate feedback from the scientific community. Other publication series from the World Agroforestry Centre include: Technical Manuals, Occasional Papers and the Trees for Change series. Published by the World Agroforestry Centre United Nations Avenue PO BOX 30677, GPO 00100 Nairobi, Kenya Tel: +254(0) 20 722 4000, via USA +1650 8336645 Fax: Tel: +254(0) 20 722 4001, via USA +1650 833 6646 Email: [email protected] Working Paper no. 235 The views expressed in this publication are those of the authors and not necessarily those of the World Agroforestry Centre. Articles appearing in the working paper series may be quoted or reproduced without charge, provided their source is acknowledged. iii About the authors Maryben World Agroforestry Centre [email protected] Chiatoh West and Central Africa Regional Programme Yaounde, Cameroon Amos Gyau World Agroforestry Centre [email protected] (corresponding United Nations Avenue author) Box 30677 – 00100 Nairobi, Kenya iv Table of contents About -

Open Data Intermediaries in the Agricultural Sector in Ghana

OPEN DATA INTERMEDIARIES IN THE AGRICULTURAL SECTOR IN GHANA RESEARCH PAPER TABLE OF CONTENTS 1 Introduction 3 Background 3 The knowledge lacuna 4 Research question(s), research scope and research method 4 2 Theoretical framework 5 3 Findings 6 Farmerline 7 Esoko 8 CocoaLink 10 4 Discussion 12 Emergence: opportune niches 12 Capital 13 Effects on the ecosystem 17 Data sources 18 5 Conclusion 19 References 20 Authors Alex Adrason and François van Schalkwyk September 2016 Publication date World Wide Web Foundation Published by Licence Published under a Creative Commons Attribution International 4.0 Licence Andrason A & Van Schalkwyk F (2016) Open data intermediaries in the agricultural sector in Suggested citation Ghana: A research paper. Washington DC: World Wide Web Foundation Cover photo credit Esoko.com This work was supported by the World Wide Web Foundation as part of the Open Data for Development (OD4D) network and carried out with financial support from the UK Government's Department for International Development (DfID) and the International Development Research Centre (IDRC), Canada. The views expressed in this work are those of the creators and do not necessarily represent those of the Web Foundation, the DfID and the IDRC or its Board of Governors. 2 • Open data intermediaries in the agricultural sector in Ghana 1 Introduction 2016: 6). Open data intermediaries are thus bridging agents. They link two (or more) other agents to facilitate the use of open data at some point(s) in the chain. In other BACKGROUND words, if there is an open dataset at the beginning, in the middle or at the end of a data chain – but not necessarily Africa loses billions of dollars due to its inability to produce in the entire chain – a connecting actor who enables and/ enough food and process its agricultural commodities. -

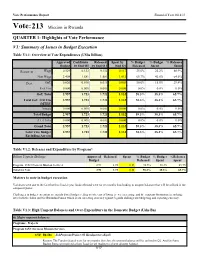

Vote:213 Mission in Rwanda

Vote Performance Report Financial Year 2018/19 Vote:213 Mission in Rwanda QUARTER 1: Highlights of Vote Performance V1: Summary of Issues in Budget Execution Table V1.1: Overview of Vote Expenditures (UShs Billion) Approved Cashlimits Released Spent by % Budget % Budget % Releases Budget by End Q1 by End Q 1 End Q1 Released Spent Spent Recurrent Wage 0.529 0.132 0.132 0.117 25.0% 22.2% 88.9% Non Wage 2.408 1.581 1.581 1.012 65.7% 42.0% 64.0% Devt. GoU 0.020 0.010 0.010 0.003 50.0% 15.0% 29.4% Ext. Fin. 0.000 0.000 0.000 0.000 0.0% 0.0% 0.0% GoU Total 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% Total GoU+Ext Fin 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% (MTEF) Arrears 0.000 0.000 0.000 0.000 0.0% 0.0% 0.0% Total Budget 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% A.I.A Total 0.000 0.000 0.000 0.000 0.0% 0.0% 0.0% Grand Total 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% Total Vote Budget 2.957 1.723 1.723 1.132 58.3% 38.3% 65.7% Excluding Arrears Table V1.2: Releases and Expenditure by Program* Billion Uganda Shillings Approved Released Spent % Budget % Budget %Releases Budget Released Spent Spent Program: 1652 Overseas Mission Services 2.96 1.72 1.13 58.3% 38.3% 65.7% Total for Vote 2.96 1.72 1.13 58.3% 38.3% 65.7% Matters to note in budget execution Variances were due to the fact that this finacial year funds released were for six months thus leading to unspent balances that will be utilised in the subquent Quater. -

Uganda Road Fund Annual Report FY 2011-12

ANNUAL REPORT 2011-12 Telephone : 256 41 4707 000 Ministry of Finance, Planning : 256 41 4232 095 & Economic Development Fax : 256 41 4230 163 Plot 2-12, Apollo Kaggwa Road : 256 41 4343 023 P.O. Box 8147 : 256 41 4341 286 Kampala Email : [email protected] Uganda. Website : www.finance.go.ug THE REPUBLIC OF UGANDA In any correspondence on this subject please quote No. ISS 140/255/01 16 Dec 2013 The Clerk to Parliament The Parliament of the Republic of Uganda KAMPALA. SUBMISSION OF UGANDA ROAD FUND ANNUAL REPORT FOR FY 2010/11 In accordance with Section 39 of the Uganda Road Act 2008, this is to submit the Uganda Road Fund Annual performance report for FY 2011/12. The report contains: a) The Audited accounts of the Fund and Auditor General’s report on the accounts of the Fund for FY 2011/12; b) The report on operations of the Fund including achievements and challenges met during the period of reporting. It’s my sincere hope that future reports shall be submitted in time as the organization is now up and running. Maria Kiwanuka MINISTER OF FINANCE, PLANNING AND ECONOMIC DEVELOPMENT cc: The Honourable Minister of Works and Transport cc: The Honourable Minister of Local Government cc: Permanent Secretary/ Secretary to the Treasury cc: Permanent Secretary, Ministry of Works and Transport cc: Permanent Secretary Ministry of Local Government cc: Permanent Secretary Office of the Prime Minister cc: Permanent Secretary Office of the President cc: Chairman Uganda Road Fund Board TABLE OF CONTENTS Abbreviations and Acronyms iii our vision iv