210310 AC Item 5

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Irish Football Association Annual Report 2018-2019

IRISH FOOTBALL ASSOCIATION ANNUAL REPORT 2018-2019 WWW.IRISHFA.COM 2018-19 CONTENTS President’s Introduction 3 Chief Executive’s Report 6 Stadium Report 9 Irish FA Annual Report Irish FA International Senior Men’s Team 13 International Men’s U21 19 2 International Men’s U19 And U17 20 International Senior Women’s Team 23 International Women’s U19 And U17 26 Girls’ Regional Excellence Programme 29 Elite Performance Programme - Club NI 30 The International Football Association Board (IFAB) 32 Domestic Football Irish Cup 33 Domestic Football 35 Domestic Football Club Licensing And Facilities 36 Refereeing 39 Grassroots Programmes 40 Disability Football Special Education 42 Disability Football Activities 43 Grassroots Football In Schools 44 Domestic Football Women’s Club Football 46 Grassroots Club And Volunteer Development 48 Grassroots Futsal 50 Community Relations 51 Northern Ireland Boys’ Football Association 52 Northern Ireland Schools’ Football Association 54 Communications 56 Finance 57 The Irish Football Association’s Annual Report 2018-19 was compiled, edited and written by Nigel Tilson PRESIDENT’S Annual Report Irish FA INTRODUCTION The depth and breadth of the work we as an association undertake never ceases to amaze me. 2018-19 Initiatives such as our Ahead of the Game mental The U19 men’s side narrowly missed out on health programme and our extensive work with VIEGLMRKERIPMXIVSYRHMR9)YVSWUYEPMƤIVW8LI disabled players are just some of the excellent U17s did manage it, however they found the going things that we do. tough in an elite round mini tournament staged in the Netherlands. And it was great that we received a Royal seal of 3 approval when the Duke and Duchess of Cambridge The senior women’s team bounced back following visited the National Football Stadium at Windsor ETSSV;SVPH'YTUYEPMƤGEXMSRGEQTEMKRF] Park, and our headquarters, back in February. -

Annual Financial Statements for the Year Ended 31St March 2019 Causeway Coast and Glens Borough Council Year Ended 31 March 2019

Annual Financial Statements for the year ended 31st March 2019 Causeway Coast and Glens Borough Council Year ended 31 March 2019 Table of Contents Page No Narrative Report 1 Financial Performance 5 Statement of the Council’s and Chief Financial Officer’s Responsibilities for the Statement of Accounts 10 Annual Governance Statement 11 Significant Governance Issues 23 Certificate of the Chief Financial Officer 24 Remuneration Report For The Year Ended 31 March 2019 25 Independent Auditor’s Report to the Members of the Council 29 The Movement in Reserves Statement 31 The Comprehensive Income and Expenditure Statement 32 The Balance Sheet 33 The Cashflow Statement 34 Notes to the Financial Statements 35 1 Expenditure and Funding Analysis 35 a Summary Adjustments 36 b Analysed Adjustments Current Year 36 c Analysed Adjustments Prior Year 36 2 a Transfers to and from Earmarked Reserves (General Fund Appropriations) and Reconciliation to General Fund 37 b Detailed Summary of Unusable Reserves - Current Year and Reconciliation to Adjustments 37 c Detailed Summary of Unusable Reserves - Prior Year and Reconciliation to Adjustments 38 3 Income and Expenditure by Nature - Current Year 40 a Current Year 40 b Prior Year 41 c Revenue from contracts with service recipients 41 4 Cost of services on continuing operations 42 a Miscellaneous powers to make payments 42 b External audit fees 42 5 Operating and Finance Leases 43 a Finance Leases (Council as lessor) 43 b Operating Lease (Council as lessor) 43 c Finance Leases (Council as lessee) 44 d Operating -

Causeway Coast and Glens What’S on Guide 2019 Contents

Causeway Coast and Glens What’s On Guide 2019 Contents 04 - 11 April 12 - 19 May 20 - 27 June 28 - 37 July 38 - 47 August 48 - 51 September 52 - 55 October 56 - 59 November 60 - 61 December 62 - 63 Exhibitions 64 - 65 Local Markets 66 - 69 Walking Tours 70 Driving Tours 71 Game of Thrones Tours 72 - 73 Food Tours 74 - 75 Water Based Tours & Experiences 76 Doggie Tours 77 Horse Riding 78 - 79 Traditional Music & The Craic What’s On Guide 2019 02 What’s On Guide 2019 03 Little Shop of Horrors Ballymoney Vintage & Classic Car Show Saturday 6th & Tuesday 9th – Saturday 13th April Saturday 13th April 8pm. Riverside Theatre, Ulster University, 10am – 4pm. Cromore Road, Coleraine BT52 1SA Joey Dunlop Leisure Centre, Garryduff Road, Ballymoney BT53 7DB Ballywillan Drama Group presents Little Shop of Horrors. Two months after their sell-out Ballymoney Old Vehicle Club Classic & smash hit Chitty Chitty Bang Bang this award- Vintage Car show & cavalcade. winning group are back at the Riverside with a brand new production of the charming, kooky t. 07960 130 030 and hilarious musical comedy Little Shop of e. [email protected] Horrors. A must see for the entire family this w. www.ballymoneyoldvehicleclub.co.uk deviously delicious musical has devoured the hearts of theatre goers for over thirty years and is a classic musical of sublime ridiculousness. April Tickets from £16. t. 028 7012 3123 w. www.ulster.ac.uk/riverside The Illegals with Niamh Kavanagh Saturday 13th April 8pm. Roe Valley Arts & Cultural Centre, Limavady Fronted by the fabulous Niamh Kavanagh, the Illegals will take you on a journey of soulful harmonies, exciting riffs, blistering guitars and unforgettable songs. -

Title of Report: Impact of Covid- 19 on Both Applicants to Tourism Events Funding Programme 2020 / 2021 and Council Supported Events

Title of Report: Impact of Covid- 19 on both Applicants to Tourism Events Funding Programme 2020 / 2021 and Council Supported Events. Committee Council Report Submitted To: Date of Meeting: 2nd June 2020 For Decision or For Decision For Information Linkage to Council Strategy (2019-23) Strategic Theme Promote our tourist offer locally and internationally Outcome Improve prosperity To provide a balanced portfolio for major events across the Borough and facilitate partnership with other event promoters Lead Officer Head of Tourism and Recreation Budgetary Considerations Cost of Proposal TBC Included in Current Year Estimates YES Capital/Revenue Revenue Code Staffing Costs Screening Required for new or revised Policies, Plans, Strategies or Service Requirements Delivery Proposals. Section 75 Screening Completed: n/a Date: Screening EQIA Required and n/a Date: Completed: Rural Needs Screening Completed n/a Date: Assessment (RNA) RNA Required and n/a Date: Completed: Data Protection Screening Completed: n/a Date: Impact Assessment DPIA Required and n/a Date: (DPIA) Completed: 200602– TEFP Page 1 of 6 1.0 Purpose of Report The purpose of this report is to outline the process by which successful Tourism Events Funding Programme (TEFP) applicants can avail of the funding allocated by Council to support their events. This is in view of the special circumstances created by COVID 19. 2.0 Background At the Council’s Leisure and Development meeting in March 2020 Officers presented the Tourism Evens Funding Programme for April 2020 to March 2021. This report was not ratified and in the interim the COVID 19 pandemic has caused major disruption. -

COUNCIL MEETING TUESDAY 24 JULY 2018 Table of Adoptions No

COUNCIL MEETING TUESDAY 24 JULY 2018 Table of Adoptions No Item Summary of key Adoptions 2 Apologies Councillors Hunter, Knight-McQuillan, McCandless, McCaw and Quigley 3 Declarations of Interests None 4 Minutes of Council Meeting held Tuesday 26 Confirmed subject to June 2018 correction on Page 6 5 Minutes of Planning Committee Meeting held Noted Wednesday 27 June 2018 6 Matters for Reporting to the Partnership Panel None – Local Government Side 7 Conferences La Touche Legacy Seminar, 5 Festival of Noted History 21st-22nd September 2018 8 Correspondence Department for Communities – Historic Noted Environment Fund for 2018/19 The Electoral Office for Northern Ireland – Noted Local Council Polling Scheme Review 9 Consultation Schedule Classification of Registered Housing Noted Associations in Northern Ireland: Consultation Two – The Future of the House Sale Schemes CM_180724_EMC Page 1 of 8 10 Seal Documents 10.1 Grave Registry Certificates, Coleraine, Seal affixed Ballywillan, Agherton and Portstewart Portstewart (No’s 4659 – 4666 inclusive) 10.2 Grave Registry Certificates, Ballymoney Cemetery (No’s 2934 – 2936 inclusive) 10.3 Grave Registry Certificates, Enagh Cemetery, Limavady (No’s 478, 483 – 485 inclusive) 10.4 Licence Agreement Works Compound, Ramore Tennis Courts between CC&GBC and FP McCann Ltd (ref CM 171128) 10.5 Indenture between the Assignors of first part and Assignores of second part with CC&GBC for 3 Berne Road, Portstewart (ref CM 180522) 10.6 Licence Agreement between CC&GBC and Ulster Bank Limited for Car Park Space -

Mid and East Antrim Set for Festival of Football As Supercupni Kicks Off

For the very latest on this year’s SuperCupNI, please visit: supercupni.com Jul 26, 2019 15:21 BST Mid and East Antrim set for festival of football as SuperCupNI kicks off The best young players on the planet are arriving in Mid and East Antrim for a week-long festival of football during this year’s STATSports SuperCupNI. This year’s competition will see some of Europe’s most prestigious young players from teams including Valencia, Arsenal, Manchester United and Newcastle United take on some of Northern Ireland’s finest across four age categories, U13, U15, U17 and U21. Manchester United legend Nicky Butt will open the STATSports SuperCupNI international youth tournament in Coleraine on Sunday 28 July with Ballymena United welcoming Manchester United to the Ballymena Showgrounds on Monday 29 July at 7.30pm. Mayor of Mid and East Antrim, Councillor Maureen Morrow, said: “SuperCupNI continues to be one of the biggest events in the sporting calendar and we are honoured to be hosting several matches as well as having the privilege of staging the finals at Ballymena Showgrounds. “This event puts Mid and East Antrim in the spotlight, showcasing some of the superb sports facilities we have on offer within the Borough. “The competition is great for the local economy and tourism, and demonstrates our capability for hosting major events. “We would also like to welcome all of the fantastic teams, families and fans from across the world to our borough.” A total of 61 teams will take part in this year’s SuperCupNI competition. Matches will take place at Ballymena and Coleraine Showgrounds, Ahoghill, Broughshane, Clough, Scroggy Road (Limavady), Riada Stadium (Ballymoney), Seahaven (Portstewart) and Anderson Park (Coleraine). -

BBC Group Annual Report and Accounts 2018/19

BBC Group Annual Report and Accounts 2018/19 BBC Group Annual Report and Accounts 2018/19 Laid before the National Assembly for Wales by the Welsh Government Return to contents © BBC Copyright 2019 The text of this document (this excludes, where present, the Royal Arms and all departmental or agency logos) may be reproduced free of charge in any format or medium provided that it is reproduced accurately and not in a misleading context. The material must be acknowledged as BBC copyright and the document title specified. Photographs are used ©BBC or used under the terms of the PACT agreement except where otherwise identified. Permission from copyright holders must be sought before any photographs are reproduced. You can download this publication from bbc.co.uk/annualreport Designed by Emperor emperor.works Prepared pursuant to the BBC Royal Charter 2016 (Article 37) Return to contents OVERVIEW Contents About the BBC 2 Inform, Educate, Entertain 4 Highlights from the year p.2 6 Award-winning content Strategic report 8 A message from the Chairman About the BBC 10 Director-General’s statement 16 Delivering our creative remit Highlights from the year and 18 – Impartial news and information award-winning content 22 – Learning for people of all ages 26 – Creative, distinctive, quality output 34 – Reflecting the UK’s diverse communities 48 – Reflecting the UK to the world 55 Audiences and external context 56 – Audience performance and market context 58 – Performance by Service 61 – Public Service Broadcasting expenditure p.8 62 – Charitable work -

Ballymena Rugby Football Club SENIOR SQUAD

Contents Welcome Letter: Galgorm Resort & Spa .......................................................... 5 From the Club President .................................................................................... 7 From the Club Chairman .................................................................................... 9 Message from the Mayor ................................................................................. 13 Message from the President I.R.F.U. ............................................................... 15 Message from the President I.R.F.U. (Ulster Branch) .................................... 19 Message from the Club Captain ...................................................................... 25 Message from the Director of Senior Rugby - by Jamie Smith ....................... 27 Saul Cobing ....................................................................................................... 31 Coaching Ballymena - by Tony Darcy ................................................................. 39 Senior Squad Profiles ....................................................................................... 47 Our Representative Players .............................................................................. 55 Fixtures .............................................................................................................. 61 Ladies Rugby - by Mark Hermin .......................................................................... 71 What is a Charitable Trust ? .......................................................................... -

1 MINUTES of the PROCEEDINGS of the MEETING of the COUNCIL HELD in MOSSLEY MILL on MONDAY 27 JANUARY 2020 at 6.30 PM in the Chai

MINUTES OF THE PROCEEDINGS OF THE MEETING OF THE COUNCIL HELD IN MOSSLEY MILL ON MONDAY 27 JANUARY 2020 AT 6.30 PM In the Chair : The Mayor (Alderman J Smyth) Members Present : Aldermen – F Agnew, P Brett, T Burns, T Campbell, L Clarke, M Cosgrove, M Girvan and D Kinahan Councillors – J Archibald, A Bennington, M Cooper, H Cushinan, P Dunlop, S Flanagan, R Foster, J Gilmour, M Goodman, P Hamill, N Kelly, R Kinnear, A Logue, R Lynch, M Magill, P Michael, J Montgomery, V McAuley, N McClelland, D McCullough, T McGrann, V McWilliam, V Robinson, S Ross, M Stewart, L Smyth, R Swann, B Webb and R Wilson Officers Present : Chief Executive – J Dixon Deputy Chief Executive – M McAlister Director of Organisation Development – A McCooke Director of Operations – G Girvan Director of Finance and Governance – S Cole Director of Community Planning – N Harkness Borough Lawyer and Head of Legal Services – P Casey ICT Change Officer – A Cole Media and Marketing Officer – J McIntyre Member Services Officer – S Boyd Member Services Manager – V Lisk 1 BIBLE READING, PRAYER AND WELCOME The Mayor welcomed everyone to the meeting and advised Members of the audio recording procedures. The meeting opened with a Bible reading and prayer by the Reverend Michael Gregory. Councillors Cushinan, Goodman, Kelly, Kinnear, Logue, McAuley and McGrann joined the meeting at this point. 1 MAYOR’S REMARKS The Mayor paid tribute to staff member Wendy Brolly who had passed away suddenly and led a silence in her honour. He reminded Members that it was Holocaust Memorial Day marking the 75th anniversary since the liberation of Auschwitz and encouraged Members to watch the Council’s specially produced video. -

Awards2018.Pdf

Welcome to the Ballymena Business Excellence Awards Ballymena Area Chamber of Commerce and Industry is delighted to present the 2018 Ballymena Business Excellence Awards. The awards seek to give recognition to the hard work and dedication of businesses in the Ballymena area and enable us all to celebrate their success. Ballymena is widely renowned as the premier shopping town in Northern Ireland, but it is sometimes overlooked that Ballymena has a vibrant and successful industrial and agricultural base as well. These awards help to celebrate the huge contribution made by our business community. The economic environment has been very tough in the last year, and these awards demonstrate the commitment of individuals and the business excellence that exists in Ballymena and the local villages. There are 21 awards this year so there is a category to suit everyone – large or small Robin Cherry MBE businesses, retail, hospitality or industrial and individual awards as well. President Ballymena Area Chamber of I would like to thank Mid and East Antrim Borough Council for agreeing to be our principal Commerce and Industry sponsor once again this year. Chamber has an excellent working relationship with Mid and East Antrim Borough Council and I look forward to continuing and indeed building upon this relationship. I would like to thank all other businesses who have sponsored awards or taken an advertisement in the awards brochure. The judging this year will again be carried out by Insight Mystery Shopping – it is entirely independent of Chamber thereby ensuring the integrity of the awards. The Gala Awards Evening this year takes place on Thursday 18th October in Tullyglass House Hotel. -

Council Agenda

Mid and East Antrim Borough Council uses Livescribe Echo Smartpen technology in order to support minute taking of meetings. This meeting will therefore be audio recorded, but following ratification of the minutes, the recording will be destroyed. Due to COVID-19, there is currently no physical public access to meetings, therefore all open business will be streamed live on Council’s website. December 4th, 2020 To Each Member of Council NOTICE OF MEETING You are requested to attend a Meeting of the Mid and East Antrim Borough Council to be held on Monday, 7th December 2020 at 6:30 pm in The Council Chamber, The Braid, 1-29 Bridge Street, Ballymena and Remote Access. Agenda 1 NOTICE OF MEETING 2 APOLOGIES 3 DECLARATIONS OF INTEREST Members and Officers are invited to declare any pecuniary and non-pecuniary interests, including gifts and hospitality, they may have in respect of items on this Agenda. 4 MINUTES OF PREVIOUS COUNCIL AND COMMITTEE MEETINGS 4.1 Minutes of Council Meeting held on 2 November 2020 - Circulated Full Council - 02 Nov 20.pdf Not included 4.2 Minutes of Policy & Resources Committee held on 9 November 2020 - circulated PR November 2020.docx.pdf Not included 4.3 Minutes of Direct Services Committee held on 10 November 2020 - Circulated DS Committee Minutes 11.20.pdf Not included 4.4 Minutes of Borough Growth Committee held on 16 November 2020 - Circulated Borough Growth Minutes 16.11.20.pdf Not included 5 MINISTERIAL VISITS/DEPARTMENTAL MEETINGS/DEPUTATIONS 5.1 Meeting with Junior Minister, Gordon Lyons MLA - Verbal report -

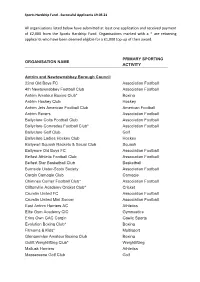

Organisations Listed Below Have Submitted at Least One Application and Received Payment of £2,000 from the Sports Hardship Fund

Sports Hardship Fund - Successful Applicants 19.03.21 All organisations listed below have submitted at least one application and received payment of £2,000 from the Sports Hardship Fund. Organisations marked with a * are returning applicants who have been deemed eligible for a £1,000 top-up of their award. PRIMARY SPORTING ORGANISATION NAME ACTIVITY Antrim and Newtownabbey Borough Council 22nd Old Boys FC Association Football 4th Newtownabbey Football Club Association Football Antrim Amateur Boxing Club* Boxing Antrim Hockey Club Hockey Antrim Jets American Football Club American Football Antrim Rovers Association Football Ballyclare Colts Football Club Association Football Ballyclare Comrades Football Club* Association Football Ballyclare Golf Club Golf Ballyclare Ladies Hockey Club Hockey Ballyearl Squash Rackets & Social Club Squash Ballynure Old Boys FC Association Football Belfast Athletic Football Club Association Football Belfast Star Basketball Club Basketball Burnside Ulster-Scots Society Association Football Cargin Camogie Club Camogie Chimney Corner Football Club* Association Football Cliftonville Academy Cricket Club* Cricket Crumlin United FC Association Football Crumlin United Mini Soccer Association Football East Antrim Harriers AC Athletics Elite Gym Academy CIC Gymnastics Erins Own GAC Cargin Gaelic Sports Evolution Boxing Club* Boxing Fitmoms & Kids* Multisport Glengormley Amateur Boxing Club Boxing Golift Weightlifting Club* Weightlifting Mallusk Harriers Athletics Massereene Golf Club Golf Sports Hardship Fund - Successful