SIMPLOT, DECEASED, JOHN EDWARD SIMPLOT, PERSONAL REPRESENTATIVE, Petitioner V

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Simplot's IT and Business Teams Partner up to Improve Data Management, Traceability, Efficiency and Response Time

AgGateway Case Studies Simplot’s IT and Business Teams Partner Up To Improve Data Management, Traceability, Efficiency and Response Time Background Key Points The J.R. Simplot Company is one of the largest privately held food and Thousands of hours a year agribusiness companies in the saved in staff time to nation. It pioneers innovations in communicate quantity, plant nutrition and food processing, confirming pricing and terms, researches new ways to feed animals etc. This time is now devoted to and sustain ecosystems, and strives other innovative solutions for the to feed a growing global population. company. The company is headquartered in 50% reduction in response time Boise, Idaho, but does business in sending purchase orders to around the globe. There are major vendors. operations in the U.S., Canada, Mexico, Australia, New Zealand and China, with products marketed in more than 40 countries worldwide. Significant reduction in restocking fees or charges for Challenges wrong items. While corporate-wide Simplot has automated many of its business processes with trading partners (such as ordering, ship notices and Reduced overall cost of doing business with partners. invoicing) the agri-business area is more complex; about 20 vendors are now connected with the company but dozens more will be brought on Reduced paper usage by 25%, electronically in the future. by eliminating 1,700 pieces of As these connections are made, it is essential for the IT and business paper a year and the cost to fax departments to work together so that the solution works for the /email each in the distribution of business; in the past the IT department was almost solely responsible purchasing information. -

Steam System Efficiency Optimized After J.R. Simplot Fertilizer Plant Receives Energy Assessment; Industrial Technologies Progra

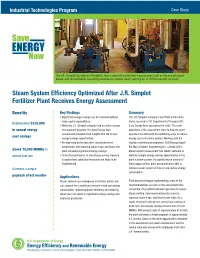

Industrial Technologies Program Case Study The J.R. Simplot Don plant in Pocatello, Idaho, repaired boiler feed water pumps such as the one pictured above, and revised boiler operating practices to reduce steam venting by 17 million pounds annually. Steam System Efficiency Optimized After J.R. Simplot Fertilizer Plant Receives Energy Assessment Benefits Key Findings Summary • Significant energy savings can be achieved without The J.R. Simplot company’s Don Plant in Pocatello, large capital expenditures. Idaho, received a U.S. Department of Energy (DOE) Implemented $335,000 • While the J.R. Simplot company had an active energy Save Energy Now assessment in 2006. The main in annual energy management program, the Save Energy Now objectives of the assessment were to help the plant assessment provided fresh insights that led to new operate more efficiently by identifying ways to reduce cost savings energy savings opportunities. energy use in its steam system. Working with the • By improving boiler operation, recovering more facility’s maintenance engineers, DOE Energy Expert condensate, and repairing steam traps and leaks, the Bill Moir of Steam Engineering Inc., utilized DOE’s Saved 75,000 MMBtu in plant achieved significant energy savings. Steam System Assessment Tool (SSAT) software to annual fuel use • Once the significance of one energy-saving measure identify multiple energy savings opportunities in the is understood, additional measures are likely to be plant’s steam system. By capitalizing on several of implemented. these opportunities, plant personnel were able to Achieved a simple improve steam system efficiency and reduce energy consumption. payback of 6.5 months Applications Steam systems are widespread in fertilizer plants and Plant personnel began implementing some of the can account for a significant amount of end use energy recommendations as soon as the assessment was consumption. -

Fries, Bakers, Tots, and Seed: Genetic Engineering and Varietal Selection

Fries, Bakers, Tots, and Seed: Genetic Engineering and Varietal Selection Kate Binzen Fuller Dept. of Ag Econ and Econ Montana State University [email protected] 406-994-5603 Gary Brester Dept. of Ag Econ and Econ Montana State University Michael Boland Food Industry Center Applied Economics University of Minnesota Paper prepared for presentation at the Agricultural & Applied Economics Association’s 2017 AAEA Annual Meeting, Chicago, Illinois, July 30-August 1, 2017 Copyright 2017 by Kate Binzen Fuller, Gary Brester, and Michael Boland.. All rights reserved. Readers may make verbatim copies of this document for non-commercial purposes by any means, provided that this copyright notice appears on all such copies. Fries, Bakers, Tots, and Seed: Genetic Engineering and Varietal Selection Genetic engineering, or the direct manipulation of an organism’s genome, has been a source of debate ever since the 1970s when scientists developed the first genetically modified organisms. More recently, Danny Hakim’s (2016) New York Times article “Doubts About the Promised Bounty of Genetically Modified Crops,” was followed by heated debate (e.g. Senapathy 2016). In particular, genetically engineered (GE) potato seed provides continued discussions with its pace of development and the introduction of new processes such as gene editing (Chang 2017). In March of 2017, commercial use of three new GE potato varieties was approved by the U.S. Department of Agriculture (USDA). The new varieties have potential human health benefits over other potato varieties, resist browning and bruising, and also resist Late Blight, the disease that caused the Irish Potato Famine. If these new potato varieties are adopted, they would represent the first GE crop primarily consumed in a low-processed form in the United States. -

Genetic Engineering and Risk in Varietal Selection Of

GENETIC ENGINEERING AND RISK IN VARIETAL SELECTION OF POTATOES Downloaded from https://academic.oup.com/ajae/article-abstract/100/2/600/4840830 by Montana State University Library user on 04 September 2018 KATE BINZEN FULLER,GARY W. BRESTER, AND MICHAEL A. BOLAND The objective of this case study is to examine the farm management decision of whether to adopt a new, genetically engineered potato variety. We describe the potato supply chain from seed produc- tion to final consumer products and explore how price and production risk interact to influence deci- sion making at each link in that chain. We provide extensive supplemental material as well, including a teaching note with assignment and/or discussion questions, an introduction to and application of stakeholder theory, and a tool that assists students in calculating expected and simulated actual returns from their choice of potato variety. Key words: Agricultural pests and diseases, farm management decisions, genetic engineering, potatoes, risk analysis, seed production. JEL codes: Q12, Q13, Q16. Genetic engineering, or the direct manipula- engineered (GE) potato seed has fueled con- tion of an organism’s genome, has been a tinued discussions (Chang 2017). In March of source of debate ever since the 1970s when 2017, commercial use of three new GE potato scientists developed the first genetically mod- varieties was approved by the USDA. The ified organisms. More recently, Danny new varieties have potential human health Hakim’s (2016) New York Times article benefits over other potato varieties, resist “Doubts about the Promised Bounty of browning and bruising, and also resist Late Genetically Modified Crops,” was followed Blight, the disease that caused the Irish Potato by heated debate (e.g., Senapathy 2016; Famine. -

How a Few Simple Things Changed History

How a Few Simple Things Changed History Class 4 William A. Reader E-mail: [email protected] 1 What We Will Cover Today • The Impact of Tobacco (continued) – Industrialization & Cigarette Smoking – Tobacco, the Roaring 20s & the World Wars – Cigarettes & Cancer • The Impact of the Potato – Some Notes About the Potato – Consequences of the Potato – The Irish Potato Famine – French Fries, Fast Food & McDonald’s 2 The Industrialization of Smoking • Cigarette smoking did not take off until the creation of brand-name advertising and the invention of the Bonsack cigarette-manufacturing machine • Prior to the Bonsack machine, cigarettes were made by hand – This made them very expensive since a skilled cigarette roller could make no more than 5 cigarettes per minute • Motivated by a $75,000 prize, James Bonsack patented a cigarette-manufacturing machine that could roll 212 cigarettes a minute 3 Growth of Cigarette Smoking • The Bonsack Machine greatly reduced the cost of manufacturing cigarettes and hence the cost of smoking them • In the Industrial world, cigarettes were the most convenient means of smoking – Pipes took time to fill and longer to smoke – Chewing tobacco was seen as a health hazard – Cigarettes were portable and sociable 4 Tobacco & World War I - 1 • Smoking proved very popular in the trenches of World War I due to – Its relaxing properties – Its ability to suppress hunger – It constituted the one bit of civilian normality in the trenches – Its sociability aspects • The militaries of all nations involved approved of smoking and issued -

USDA National School Lunch Product Fact Sheet

J.R. Simplot Company Technical Center P.O. Box 1059, Caldwell, Idaho 83606-1059 Business: 208 454 4611 USDA National School Lunch Product Fact Sheet PRODUCT POTATOES / FRENCH FRIES, FROZEN: 10071179036289 Simplot Infinity® Crinkle Cut Deep-V French Fries, 6/5 LB. Product packed to US Grade A, ⅜" deep-v CC. Processed in Non-Hydrogenated Vegetable Oil; Labeled 0g Trans Fat per serving. Low SPECIFICATION: moisture; Oven-ready or quick deep fry time. SERVING INFORMATION Serving Size (as purchased) Contribution Equivalent Equivalent Servings Per Bag Equivalent Servings Per Case 2.06 oz. ½ cup cooked vegetable 38.83 233.00 PRODUCT FORMULATION CREDITS Food Buying Guide Description of Creditable Oz. / Raw Portion of FBG Yield / Creditable Amt. FBG Subgroup Mult. Ingredient Creditable Ingredient Purchase Unit (quarter cup) Potatoes, French Fries, frozen Crinkle Cut Low Starchy 1.98 x 16.20 / 16 2.00 Moisture Ovenable Includes USDA Foods Each 2.06 ounce serving of the product above contains ½ cup Starchy vegetable. INGREDIENT STATEMENT NUTRITION INFORMATION Potatoes, Vegetable Oil (Soybean, Canola, Cottonseed, and/or Sunflower), Food Starch-Modified, Contains less than 2% of Beta Carotene Color, Cornstarch, Dextrin, Dextrose, Leavening (Sodium Acid Pyrophosphate, Sodium Bicarbonate), Rice Flour, Salt, Xanthan Gum, To Maintain Natural Color (Tetrasodium Pyrophosphate and Disodium Dihydrogen Pyrophosphate). ALLERGENS PRESENT ☒ None ☐ Milk ☐ Egg ☐ Wheat ☐ Soy ☐ Peanuts ☐ Tree Nuts ☐ Fish ☐ Molluscan Shellfish ADDITIONAL INFORMATION ☒ Gluten Free ☐ Lacto-Ovo Vegetarian ☒ Vegan ☐ Kosher ☒ Halal ☒ Smart Snacks Compliant COOKING INSTRUCTIONS Deep Fryer: Preheat fryer to 345°F. Fill fryer basket half full. Fry for 2 ½ - 3 minutes. Convection Oven: Preheat oven to 400°F. -

COMPLAINT for PATENT INFRINGEMENT, TRADE DRESS INFRINGEMENT, and UNFAIR COMPETITION - 1 Case 1:16-Cv-00449-BLW Document 1 Filed 10/07/16 Page 2 of 15

Case 1:16-cv-00449-BLW Document 1 Filed 10/07/16 Page 1 of 15 Dana M. Herberholz, ISB No. 7440 Christopher Cuneo, ISB No. 8557 Andrew Wake, ISB No. 9486 Margaret N. McGann (pro hac vice pending) PARSONS BEHLE & LATIMER 800 W. Main Street, Suite 1300 Boise, ID 83702 Telephone: (208) 562-4900 Facsimile: (208) 562-4901 Email: [email protected] [email protected] [email protected] [email protected] Attorneys for Plaintiff J.R. Simplot Company UNITED STATES DISTRICT COURT DISTRICT OF IDAHO J.R. SIMPLOT COMPANY, Case No. 1:16-cv-449 Plaintiff, COMPLAINT FOR PATENT v. INFRINGEMENT, TRADE DRESS INFRINGEMENT, AND UNFAIR MCCAIN FOODS USA, INC. COMPETITION Defendant. JURY TRIAL DEMANDED Plaintiff J.R. Simplot Company (“Simplot”), by way of complaint against Defendant McCain Foods USA, Inc. (“Defendant” or “McCain”), hereby alleges and avers as follows: COMPLAINT FOR PATENT INFRINGEMENT, TRADE DRESS INFRINGEMENT, AND UNFAIR COMPETITION - 1 Case 1:16-cv-00449-BLW Document 1 Filed 10/07/16 Page 2 of 15 NATURE OF THE ACTION 1. In 1929, J.R. “Jack” Simplot started the company that now bears his name in Declo, Idaho. Mr. Simplot grew the company from a one-man farming operation into one of the world’s largest and most successful privately owned, family-run food and agribusiness companies. Today, with its innovative spirit and more than 80 years of experience, Simplot is one of the most established and respected companies in the food and agribusiness industry in the United States and abroad. 2. Simplot’s unprecedented growth and success is linked to its proud history of innovation. -

2012 | J.R. Simplot Company Sustainability Summary

2012 | J.R. Simplot Company Sustainability Summary CONTENTS 3 What We Stand For 12 Natural Resource Leadership 4 A Message from the President and CEO 15 Energy and Technology 5 Company Profile 16 Safety & Statistics 17 Educating Youth 6 Simplot Around the World 18 Social Responsibility 8 Three Pillars 20 Simplot Family Message 9 Oversight and Strategy As a privately held company, 10 History with Simplot is uniquely positioned to Sustainability make sustainability a priority. Sustainability Task Force created to monitor and advocate for progress company-wide The changes required to meet sustainability goals over the long term are only and report progress toward those goals; and consistently and proactively obtained through rigorous and ongoing communication, measurement and communicate results with company leadership. This process takes time and feedback. effort, and the Sustainability Task Force is in place to do that work. This is why the J.R. Simplot Company has created a Sustainability Task The Sustainability Task Force is responsible for reporting quarterly on the Force, a company-wide effort that seeks to continually gather information, set Company’s progress toward its sustainability goals, including areas such as and revise targets for improvement, and engage the entire company in the environmental, community, health & safety, security, and energy. sustainability conversation. Among the goals of the Sustainability Task Force are to identify and monitor potential areas of improvement; create measurements for success, then track 2 What We Stand For: a Generational Culture Tellingly, this report begins and ends with family. The Company has Sustainability takes many forms, for example: always been privately held, which really means family held. -

Simplot Company Sustainability Report

2014 | J.R. Simplot Company Sustainability Summary What we stand for: a passion for unearthing new possibilities For over eight decades, the Simplot Company has been green energy resources from potato waste; developing new built on family ideals and values. Even in the beginning safety methods and policies for a better workplace; and as J.R. Simplot embraced innovations, he was driven and restoring old mining land to help wildlife thrive. passionate about cultivating a philosophy where new ideas have a chance to grow and flourish. At Simplot, we’re dedicated to Bringing Earth’s Resources to Life. We consider ourselves to be true stewards of the That spirit continues today as we seek new, smarter ways of land, and are driven to provide more plentiful, healthier managing resources to feed the needs of a growing world. food—and do so with fewer resources, less energy, and smarter practices. It’s more than our goal. It’s our passion. Today, sustainability touches every corner of our company: It’s our legacy. It will be for generations to come. building facilities that reduce energy consumption; creating 2 | 2014 J.R. Simplot Company Sustainability Summary CEO J.R. Simplot had a knack for spotting trends. He had the inherent ability to message see possibilities nobody else could see, and the resolve to act on them—helping him turn a one-man farming operation into today’s global food and agribusiness enterprise. His spirit of embracing innovation remains the foundation of our Company. It’s the sense of curiosity that continues to drive us to unearth new, sustainable ways of producing food for a growing world. -

For Determination of Non-Regulated Status for Innate™ Potatoes With

J.R. Simplot Company Petition (13-022-01p) for Determination of Non-Regulated Status for Innate™ Potatoes with Low Acrylamide Potential and Reduced Black Spot Bruise: Events E12 and E24 (Russet Burbank); F10 and F37 (Ranger Russet); J3, J55, and J78 (Atlantic); G11 (G); H37 and H50 (H) OECD Unique Identifiers: SPS-00F10-7; SPS-00F37-7; SPS-0E12-8; SPS-00E24-2; SPS-000J3-4; SPS-00J55-2; SPS-00J78-7; SPS-00G11-9; SPS-00H37-9; SPS-00H50-4 Draft Environmental Assessment March 2014 Agency Contact Cindy Eck Biotechnology Regulatory Services 4700 River Road USDA, APHIS Riverdale, MD 20737 Fax: (301) 734-8669 The U.S. Department of Agriculture (USDA) prohibits discrimination in all its programs and activities on the basis of race, color, national origin, sex, religion, age, disability, political beliefs, sexual orientation, or marital or family status. (Not all prohibited bases apply to all programs.) Persons with disabilities who require alternative means for communication of program information (Braille, large print, audiotape, etc.) should contact USDA’S TARGET Center at (202) 720–2600 (voice and TDD). To file a complaint of discrimination, write USDA, Director, Office of Civil Rights, Room 326–W, Whitten Building, 1400 Independence Avenue, SW, Washington, DC 20250–9410 or call (202) 720–5964 (voice and TDD). USDA is an equal opportunity provider and employer. Mention of companies or commercial products in this report does not imply recommendation or endorsement by the U.S. Department of Agriculture over others not mentioned. USDA neither guarantees nor warrants the standard of any product mentioned. Product names are mentioned solely to report factually on available data and to provide specific information. -

Congressional Record—Senate S5827

June 19, 2008 CONGRESSIONAL RECORD — SENATE S5827 State constitution. Two hundred years commitment to education and commu- standing what this elementary school of subjugation and oppression, of bond- nity outreach expands to the home represents to its community, the age and tyranny, serve as a reminder with June’s famous cooking. June school’s motto is fitting: Ku lokahi ka to all of us now of the importance of warms the homes and lives of others ‘ohana ‘o Wahiawa! Stand in unison the freedom and equality. with her legendary apple strudel which family of Wahiawa!∑ Although Maryland was a slave she has shared through cooking les- f State, it did not secede from the Union. sons. She continues to inspire with her IN HONOR OF ALFREDO NU´ N˜ EZ Marylanders’ contributions to the dedication to continual learning and Union cause and the abolitionist move- improvement. ∑ Mr. KERRY. Mr. President, I would ment did much to secure the abolition June Salander inspires with her en- like to take a moment to celebrate the of slavery. Harriet Tubman, who was ergy and enthusiasm within the reli- life and work of a dedicated educator. born Araminta Ross in Dorchester gious community as well. The Rutland This month, Alfredo Nu´ n˜ ez will retire County, freed countless slaves from Jewish Center has remained an inte- as principal of the Agassiz Elementary bondage and was the first woman to gral part of her social and cultural life. School of Jamaica Plain, MA, and as he lead an armed assault in the Civil War. June’s daughter, Menasha, accurately prepares to do so I am proud to join Frederick Douglass, who was born describes the center as June’s living with his colleagues, friends, and family Frederick Augustus Bailey in Talbot room, kitchen, dining room, and back- in celebrating more than 30 years of County, escaped slavery and went on to yard. -

Case Study: Simplot Relies on Airbus to Deliver Valuable Agronomy to Their Farmers

DEFENCE AND SPACE Intelligence Simplot Relies on Airbus to Deliver Valuable Agronomy to Their Farmers Case Study Challenge Solution and Results Benefits To provide agronomic A fully automated, scalable A reliable system that insights and value through and integrated imagery allows Simplot to grow the use of satellite imagery processing engine for delivery their business and support and mobile technology. of data driven agronomy into farmers in the field. Simplot Advisor™ portal. Satellite imagery is the backbone of our SmartFarm® Precision Agriculture platform. The high resolution, high frequency imagery we receive from Airbus enables our crop advisors to quickly respond with more agronomic insight to issues occuring in the growing season. Allan Fetters, Director of Technology J.R. Simplot Company Challenge resolutions of 50cm to 6m and up to weekly enrolment to tasking to processing and temporal resolution. This imagery process display of imagery, each step became Satellite imagery has been used since the has enabled Simplot’s SmartFarm® Precision integrated and seamless. The digitisation 1970s to provide insight on crop health to Agriculture team and agronomists to gain of imagery also enabled Simplot to overlay farmers and agronomists. However, it has insight on their farmers’ fields, such as: other digital agronomic data layers (soil type, been viewed as nothing more than static, • Infrared – Radiation reflectance from the management zones, yield, etc.) and begin tricolored maps with minimal value for plants surface in the Infrared spectrum. determining correlations within the data to farmers. As GPS-enabled mobile devices facilitate agronomic decisions. The digital • Plant Health – Infrared imagery converted grew in use and satellite imagery started to format also allows Simplot agronomists to to a standard vegetative index.