Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. 20554 ) in the Matter of ) IB

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Outside the Cage: the Political Campaign to Destroy Mixed Martial Arts

University of Central Florida STARS Electronic Theses and Dissertations, 2004-2019 2013 Outside The Cage: The Political Campaign To Destroy Mixed Martial Arts Andrew Doeg University of Central Florida Part of the History Commons Find similar works at: https://stars.library.ucf.edu/etd University of Central Florida Libraries http://library.ucf.edu This Masters Thesis (Open Access) is brought to you for free and open access by STARS. It has been accepted for inclusion in Electronic Theses and Dissertations, 2004-2019 by an authorized administrator of STARS. For more information, please contact [email protected]. STARS Citation Doeg, Andrew, "Outside The Cage: The Political Campaign To Destroy Mixed Martial Arts" (2013). Electronic Theses and Dissertations, 2004-2019. 2530. https://stars.library.ucf.edu/etd/2530 OUTSIDE THE CAGE: THE CAMPAIGN TO DESTROY MIXED MARTIAL ARTS By ANDREW DOEG B.A. University of Central Florida, 2010 A thesis submitted in partial fulfillment of the requirements for the degree of Master of Arts in the Department of History in the College of Arts and Humanities at the University of Central Florida Orlando, Florida Spring Term 2013 © 2013 Andrew Doeg ii ABSTRACT This is an early history of Mixed Martial Arts in America. It focuses primarily on the political campaign to ban the sport in the 1990s and the repercussions that campaign had on MMA itself. Furthermore, it examines the censorship of music and video games in the 1990s. The central argument of this work is that the political campaign to ban Mixed Martial Arts was part of a larger political movement to censor violent entertainment. -

PSUAC) Friday April 27Th, 2018

PETE SUAZO UTAH ATHELETIC COMMISSION (PSUAC) Friday April 27th, 2018 Attending Commissioners: Taylor Leavitt (Commission Chair), Commissioner Bruce R. Baird in attendance with Commissioner Leslie Reberg via teleconference. Director Scott Bowler facilitated the call from the Bryce Canyon Conference Room #369. Also in attendance; Referee Bobby Wombacher, Judge Dan Furse and Contestant Francisco Alcantara. Commission Chairman Leavitt called the meeting to order at 12:09pm at the Governor’s Office of Economic Development in the “Bryce Canyon Conference Room.” Sign Per Diem Sheet Director Bowler signed for Commissioners Leslie Reberg as she attended via teleconference. Approval of Meeting Minutes Commission Chairman Taylor Leavitt made a motion to “Table” the approval of Meeting Minutes to the next meeting as a quorum of attendee’s within the Commission was not available to vote. Contestant Francisco Alcantara petition to be granted a License after 10 straight MMA & Boxing Losses: Director Bowler explained to the Commission members that in accordance with the “Non-Performing Contestant Protocol” adopted 4-26-2011 which reads; Protocol for Administrative Suspension of Non-Performing Contestants: Any contestant who has lost their last eight bouts by submission, technical knockout or knockout shall not be approved to compete in the State of Utah. Any contestant who has lost nine of their last ten bouts by submission, technical knockout or knockout shall not be approved to compete in the State of Utah. Any contestant who has lost their last ten bouts by decision, submission, technical knockout or knockout shall not be approved to compete in the State of Utah. Any contestant who has lost thirteen of their last fifteen bouts by any means shall not be approved to compete in the State of Utah. -

PSUAC) Friday May 18Th, 2018

PETE SUAZO UTAH ATHELETIC COMMISSION (PSUAC) Friday May 18th, 2018 Attending Commissioners: Taylor Leavitt (Commission Chair), Commissioner Bruce R. Baird in attendance with Commissioner Leslie Reberg via teleconference. Director Scott Bowler facilitated the call from the Bryce Canyon Conference Room #369. Also in attendance; Referee Bobby Wombacher, Judge Dan Furse and Contestant Francisco Alcantara. Commission Chairman Leavitt called the meeting to order at 12:09pm at the Governor’s Office of Economic Development in the “Bryce Canyon Conference Room.” Sign Per Diem Sheet Director Bowler signed for Commissioners Leslie Reberg as she attended via teleconference. Approval of Meeting Minutes Commission Chairman Taylor Leavitt made a motion to “Table” the approval of Meeting Minutes to the next meeting as a quorum of attendee’s within the Commission was not available to vote. Contestant Francisco Alcantara petition to be granted a License after 10 straight MMA & Boxing Losses: Director Bowler explained to the Commission members that in accordance with the “Non-Performing Contestant Protocol” adopted 4-26-2011 which reads; Protocol for Administrative Suspension of Non-Performing Contestants: Any contestant who has lost their last eight bouts by submission, technical knockout or knockout shall not be approved to compete in the State of Utah. Any contestant who has lost nine of their last ten bouts by submission, technical knockout or knockout shall not be approved to compete in the State of Utah. Any contestant who has lost their last ten bouts by decision, submission, technical knockout or knockout shall not be approved to compete in the State of Utah. Any contestant who has lost thirteen of their last fifteen bouts by any means shall not be approved to compete in the State of Utah. -

Master Instructor of Krav Maga Elite & Diamond Mixed Martial Arts

Master Instructor of Krav Maga Elite & Diamond Mixed Martial Arts: Joseph Diamond Joe Diamond is the Master Instructor of Krav Maga Elite and Diamond Mixed Martial Arts located in Northfield, NJ and Philadelphia, PA. Master Diamond is a licensed Real Estate salesperson currently working at Long and Foster in Ocean City, NJ. He is currently studying for the NJ Real Estate Broker’s exam. Master Diamond’s first experience with martial arts began when he trained at the Veteran’s Stadium with Kung Fu Expert and Phillies head trainer, Gus Hefling, alongside Phillies players: Mike Schmidt, Steve Carlton, Tug McGraw and John Vukovich, Master Diamond’s uncle. He continued his martial art training at the age of 12. He loved the workout and the confidence it gave him for protecting himself, family and friends. Upon achieving his Black Belt, he knew that Martial Arts would help develop a healthy lifestyle that made him stronger and confident. It became his passion to make it an essential part of his life. Master Diamond is a Level 3 US Army Combatives Instructor, and has taught Combatives and Brazilian Jiujitsu to enlisted and reserve soldiers for several years at Ft. Dix, NJ, Ft. Benning, GA, The Burlington Armory, NJ and ROTC Programs at local universities. Master Diamond is also a Level 5 Certified Instructor in Commando Krav Maga under Moni Aizik, world renowned Krav Maga expert. Master Diamond has taught law enforcement officers and military personnel from the following: New Jersey State Police, US Air Marshalls, FBI, US Army, US Marines, US Navy Seals and several local law enforcement agencies. -

Matt Humehume Godfather of Pankration Marcelo Alonso

NW FIGHTSCENE MAGAZINE SUMMER 2006 THE NORTHWEST’S PREMIER FIGHTLIFE & NIGHTLIFE MAGAZINE MATTMATT HUMEHUME GODFATHER OF PANKRATION MARCELO ALONSO EVENTSEVENTS SPORTFIGHTSPORTFIGHT 1515 AMATEURAMATEUR PRIDEPRIDE FCFC X-FIGHTINGX-FIGHTING CHAMPIONSHIPSCHAMPIONSHIPS DESERTDESERT BRAWLBRAWL XVIIXVII AXAX FIGHTINGFIGHTING CHAMPIONSHIPSCHAMPIONSHIPS NWNW NIGHTNIGHT LIFELIFE DRAGSTRIPDRAGSTRIP RIOTRIOT RINGRING GIRLSGIRLS DESERTDESERT BRAWLBRAWL RINGRING GIRLSGIRLS $5.00 USD $7.00 CAN LLOCALOCAL SPOSPOTLIGHTTLIGHT 74589 0157490 ZERO ISSUE SUMMER 2006 EDED “SHORT“SHORT FUSE”FUSE” HERMAN HERMAN nwfightscene.com CAMICAMI “HOSTILE”“HOSTILE” HOSTETLER HOSTETLER ONON THETHE RECORDRECORD Summer 2006 Welcome to the next generation of pop culture. We couldn’t be more Editors: Mike Hoernlein, Mike Renouard, excited as we embark on this new journey called NW FightScene Shelli Hoernlein Magazine (NWFS). For decades, local bands have had publications that covered their events and took an inside look at stand out performers. A Creative Director: Tripp Sherr good portion of our staff has a long history working with these publica- tions as advertisers and contributors. We’ve also been long time fans of Graphic Design: Tripp, Mike Hoernlein local pankration and kickboxing events held in the Northwest. Seeing Contributing Writers: Mike Hoernlein, fights on TV is great, but nothing compares to the spectacle of seeing these warriors compete in person, with the crowd so pumped you can Marc Forsyth, Chris Hoernlein, Steve feel the energy. “Spaniard” Roberts, Aeryn As the sport of Mixed Martial Arts (MMA) grows, the new & novice Contributors: Kink Clothing, fans need to be educated to get the most enjoyment out of it. Luckily, Charlie's Combat Club, there are a few great MMA mags distributed nationally, but we don’t get Freedumbimages.com to read about our local fighters in them too often. -

RFP Request List

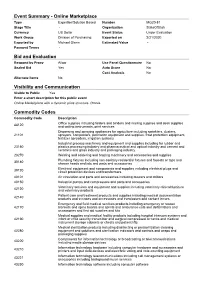

Event Summary - Online Marketplace Type Expertise/Solution Based Number MG20-81 Stage Title - Organization StateOfUtah Currency US Dollar Event Status Under Evaluation Work Group Division of Purchasing Exported on 2/21/2020 Exported by Michael Glenn Estimated Value - Payment Terms - Bid and Evaluation Respond by Proxy Allow Use Panel Questionnaire No Sealed Bid Yes Auto Score No Cost Analysis No Alternate Items No Visibility and Communication Visible to Public Yes Enter a short description for this public event Online Marketplace with a dynamic price structure. Omnia. Commodity Codes Commodity Code Description Office supplies including folders and binders and mailing supplies and desk supplies 44120 and writing instruments, print services Dispersing and spraying appliances for agriculture including sprinklers, dusters, 21101 sprayers, composters, pollination equipment and supplies, frost protection equipment, fertilizer spreaders, irrigation systems Industrial process machinery and equipment and supplies including for rubber and 23150 plastics processing industry and pharmaceutical and optical industry and cement and ceramics and glass industry and packaging industry 23270 Welding and soldering and brazing machinery and accessories and supplies Plumbing fixtures including non-sanitary residential fixtures and faucets or taps and 30180 shower heads and jets and parts and accessories Electrical equipment and components and supplies including electrical plugs and 39120 circuit protection devices and transformers 40101 Air circulation and -

The BG News October 4, 1985

Bowling Green State University ScholarWorks@BGSU BG News (Student Newspaper) University Publications 10-4-1985 The BG News October 4, 1985 Bowling Green State University Follow this and additional works at: https://scholarworks.bgsu.edu/bg-news Recommended Citation Bowling Green State University, "The BG News October 4, 1985" (1985). BG News (Student Newspaper). 4430. https://scholarworks.bgsu.edu/bg-news/4430 This work is licensed under a Creative Commons Attribution-Noncommercial-No Derivative Works 4.0 License. This Article is brought to you for free and open access by the University Publications at ScholarWorks@BGSU. It has been accepted for inclusion in BG News (Student Newspaper) by an authorized administrator of ScholarWorks@BGSU. Pwtly cloudy. Hl0h 65 Vol. 68 Issue 24 THE BG NEWS Friday, October 4,1985 Leaders quit CIAO posts by Valeric Qptak school," she said. staff reporter She often neglected class work because of time commitments in Tlie University Activities Or- UAO, she said. "In a few in- ganization is undergoing some stances I found I hadn't learned activity of its own as the organi- something from my classes that zation faces turnover of its two I should have." she said. highest offices. Pearson held her resignation The president and vice presi- off until after Fall Fest, which dent that were elected last she coordinated. spring have decided to resign "(My resignation) was some- from their offices for personal thing I saw coming," she ad- reasons. mitted. President Lori Wolfinger has CLASSWORK AND job hunt- said she will officially resign ing are Pearson's priorities now next Wednesday, when the that she is out of office. -

University of San Diego / Spring 2010 a D V E N T U R O

56318U_BC-3.indd 2 W H I L E T H E R E A R E M A N Y W A Y S T O B E A D V E N T U R O U S O P E N I N G A D O O R I S T H E F I R S T S T E P . US UNIVERSITY D MAGAZINE OF SA N DI EGO / S P R I N G 2 0 1 0 2/2/10 10:53 AM EDITORIAL LICENSE USD MAGAZINE MAGAZINE S T A F F [ e d i t o r / s e n i o r d i r e c t o r ] Julene Snyder [reinvention] [email protected] [ s e n i o r c r e a t i v e d i r e c t o r ] Barbara Ferguson BE KIND, REWIND [email protected] Who among us hasn’t wished for a do-over? CONTRIBUTORS was flying. Legs pumping, hair a wild whipping nimbus, going faster than I ever [ w r i t e r s ] had. A moment earlier, when I’d finally reached the top of the hill, a bit out of Ryan T. Blystone, Carol Cujec, Nathan Dinsdale, Liz Harman, Kelly Knufken, breath, I’d barely paused before I took a deep breath, pointed the front wheel I Trisha J. Ratledge, Anthony Shallot ’10 of my beloved gold Schwinn in a downward direction, leaned forward and let [ p h o t o g r a p h e r s ] gravity do the rest. -

MMA Encyclopedia / Jonathan Snowden and Kendall Shields

00MMAEncycl_i-iv__ 02/09/10 3:54 PM Page i ECW Press 00MMAEncycl_i-iv__ 02/09/10 3:54 PM Page ii Copyright © Jonathan Snowden and Kendall Shields, 2010 Published by ECW Press 2120 Queen Street East, Suite 200, Toronto, Ontario, Canada m4e 1e2 416-694-3348 [email protected] All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form by any process — electronic, mechanical, photocopying, recording, or other- wise — without the prior written permission of the copyright owners and ECW Press. The scanning, uploading, and distribution of this book via the Internet or via any other means without the permission of the publisher is illegal and punishable by law. Please purchase only authorized electronic editions, and do not participate in or encourage electronic piracy of copyrighted materials. Your support of the authors’ rights is appreciated. library and archives canada cataloguing in publication Snowden, Jonathan, 1975- The MMA encyclopedia / Jonathan Snowden and Kendall Shields. Includes bibliographical references. isbn 978-1-55022-923-3 1. Mixed martial arts--Encyclopedias. i. Shields, Kendall ii. Title. gv1102.7.m59s65 2010 796.81503 c2010-901256-9 Developing Editor: Michael Holmes Cover Design: Dave Gee Text Design: Tania Craan Color Section Design: Rachel Ironstone Typesetting: Gail Nina Photos copyright © Peter Lockley, 2010 Printing: Solisco Tri-Graphic 1 2 3 4 5 The publication of The MMA Encyclopedia has been generously supported by the Government of Ontario through Ontario Book Publishing Tax Credit, by the OMDC Book Fund, an initiative of the Ontario Media Development Corporation, and by the Government of Canada through the Canada Book Fund. -

Commencement Book 2021

2021 Commencement Convocation “We are extending a distinguished tradition— one where we come together, as a community, to recognize our students and celebrate their tremendous academic growth and accomplishments.” Chancellor Patrick Gallagher #PittGrad21 @PittTweet @pittofficial A Message from Chancellor Patrick Gallagher Thank you for joining us in celebrating the University of Pittsburgh’s 2021 Commencement. We are extending a distinguished tradition—one where we come together, as a community, to recognize our students and celebrate their tremendous academic growth and accomplishments. This tradition persists—even during a pandemic—because a diverse group of family, friends, faculty and staff has once again challenged our students and championed their success. To those of you who have offered such vital support: Thank you. This year’s graduates will soon join an even bigger Pitt community—one that is more than 340,000 alumni strong and is defined by individuals who are living out our university’s mission of leveraging knowledge for society’s gain. To the members of our Class of 2021 who are making this transition: Congratulations! You are part of an elite group with a noble mission, and I am excited to watch you continue to lead lives of impact for years to come. Hail to Pitt! Patrick Gallagher Chancellor iii A Message from the Pitt Alumni Association Dear graduates, Congratulations! You’ve made it through a difficult and unusual year—one none of us will soon forget—and now you’re ready to step out into the world as newly minted graduates of the University of Pittsburgh. Today, you also become official members of the Pitt alumni family, one of more than 342,000 graduates living around the globe. -

093481 Iub 2008 Commence

ONE HUNDRED SEVENTY-NINTH ANNUAL COMMENCEMENT Dear Friends: Welcome to Indiana University’s 2008 Commencement. Together, on this great day of celebration, we pause to honor the tremendous accomplishments of our graduates. This is their shining moment. Coming from across the state of Indiana, throughout the nation, and around the world, they have become a part of the fabric of excellence woven at Indiana University over the course of nearly two centuries. In subjects ranging from accounting to zoology, they have drawn on their intelligence, talents, and tenacity to achieve mastery and prepare for the challenges of tomorrow. We honor their achievements today and recognize the challenges they have already faced, and overcome, as they have pursued their dreams. This day has been years in the making: years of study and years of support. Our graduates have reached this wonderful day propelled by the love, encouragement, and faith of their families and friends. The strength of that support helps each of us achieve our highest aspirations and deserves our deepest gratitude. Today is as much a day to share that gratitude as to celebrate. Indiana University’s class of 2008 will always be a part of IU’s rich and living history. Having dedicated themselves to the pursuit of academic excellence, driven by curiosity and intellectual passion, our graduates are now poised on the cusp of ever greater accomplishments. We will remember and celebrate them always, wishing them the greatest success in the future. Most sincerely, Michael A. McRobbie President Glimpses of Commencements Past “The Commencement of 1833 was held in the “Society, through government, through “If someone were to ask me casually about life, I new chapel, the orchestra composed of two philanthropy, and through the sacrifices of would simply say, ‘Play it like you feel it, baby, flutes, & one of them cracked—imagine the individual families, has supported higher and live it up, kid. -

2018 Fighter Roster 05.22.18 Vnbc

2018 FIGHTER ROSTER MAY | 2018 1 FEATHERWEIGHT 145lbs ALEXANDRE ALMEIDA 2018 FEATHERWEIGHT DIVISION 18-7-0 NICKNAME: “CAPITÃO” SPECIALTY/FOUNDATION: JIU JITSU WEIGHT: 145 LBS. HEIGHT | REACH: 5’11” | 71” FIGHTING OUT OF: MANAUS, BRAZIL ASSOCIATION: XTREME COUTURE AGE | BORN: 29 | 08/21/1988 2018 PFL PAY: N/A CAREER HIGHLIGHTS ˗ Started MMA career fighting for Brazilian regional promotions, most notably for Jungle Fights ˗ Defeated Rafael Miranda to capture the Jungle Fights Featherweight title at Jungle Fight 62 ˗ Made his WSOF debut at WSOF24 by defeating fellow Brazilian Saul Almeida via submission ˗ Went 1-1 against perennial title contender Lance Palmer for the WSOF Featherweight belt BEYOND THE CAGE ˗ Began fighting professionally at age 18 ˗ Was selected to appear on TUF Brazil Season 4 before pre-fight medical exams kept him out ˗ Cleared to compete once updated tests proved his records were mixed up with someone else 3 ANDRE HARRISON 2018 FEATHERWEIGHT DIVISION 17-0-0 NICKNAME: “THE BULL” SPECIALTY/FOUNDATION: WRESTLING WEIGHT: 145 LBS. HEIGHT | REACH: 5’8” | 69” FIGHTING OUT OF: LONG ISLAND, NY ASSOCIATION: BELLMORE KICKBOXING MMA AGE | BORN: 29 | 05/16/1988 2018 PFL PAY: N/A CAREER HIGHLIGHTS ˗ Went 7-0 under the Ring of Combat banner earning the Featherweight title via 1st round TKO ˗ Former Titan FC Featherweight Champion who defended his belt 4-times ˗ Won the WSOF Featherweight title in his 2nd appearance defeating Lance Palmer at WSOF35 ˗ Considered one of the top non-UFC Featherweight prospects in the world ˗ Notable wins: Lance Palmer, Alexandre Bezerra, Cody Bollinger, Desmond Green and Steven Siler BEYOND THE CAGE ˗ Was an All-American wrestler at Nassau Community College & Fort Hays State University ˗ Although currently living in New York, Harrison is originally from Trinidad & Tobago ˗ Everlast has created a custom gloves for Harrison ˗ His MMA idol is Anderson Silva 4 BEKBULAT MAGOMEDOV 2018 FEATHERWEIGHT DIVISION 19-1-0 NICKNAME: N/A SPECIALTY/FOUNDATION: SAMBO WEIGHT: 145 LBS.