Winning Policies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pacer CSOP FTSE China A50 ETF Schedule of Investments July 31, 2020 (Unaudited) Shares Value COMMON STOCKS - 98.0% Agriculture - 1.6% Muyuan Foodstuff Co Ltd

Page 1 of 4 Pacer CSOP FTSE China A50 ETF Schedule of Investments July 31, 2020 (Unaudited) Shares Value COMMON STOCKS - 98.0% Agriculture - 1.6% Muyuan Foodstuff Co Ltd. - Class A 9,230 $ 120,977 Wens Foodstuffs Group Co Ltd. - Class A 4,660 15,857 136,834 Auto Manufacturers - 0.7% SAIC Motor Corp Ltd. - Class A 24,600 64,077 Banks - 23.7% Agricultural Bank of China Ltd. - Class H 352,300 163,039 Bank of China Ltd. - Class H 193,900 92,512 Bank of Communications Co Ltd. - Class A 184,100 125,556 China CITIC Bank Corp Ltd. - Class H 24,700 18,261 China Construction Bank Corp. - Class H 81,500 71,464 China Everbright Bank Co Ltd. - Class H 126,400 68,456 China Merchants Bank Co Ltd. - Class A 108,200 539,489 China Minsheng Banking Corp Ltd. - Class A 254,300 201,851 Industrial & Commercial Bank of China Ltd. - Class A 198,400 140,993 Industrial Bank Co Ltd. - Class A 127,400 285,849 Ping An Bank Co Ltd. - Class A 75,000 143,348 Shanghai Pudong Development Bank Co Ltd. - Class A 132,300 196,379 2,047,197 Beverages - 17.9% Jiangsu Yanghe Brewery Joint-Stock Co Ltd. - Class A 4,000 77,398 Kweichow Moutai Co Ltd. - Class A 4,000 961,777 Wuliangye Yibin Co Ltd. - Class A 16,200 504,835 1,544,010 Building Materials - 1.6% Anhui Conch Cement Co Ltd. - Class H 15,900 139,921 Coal - 0.5% China Shenhua Energy Co Ltd. -

Jpmorgan Funds - China A-Share Opportunities Fund

Fund House of the Year Fund Selector Asia Awards - Singapore3) Singapore 2021 - Greater China/China Equity - Platinum4) FOR SINGAPORE INVESTORS ONLY SINGAPORE RECOGNISED SCHEME FACT SHEET | July 31, 2021 JPMorgan Funds - China A-Share Opportunities Fund INVESTMENT OBJECTIVE PERFORMANCE To provide long-term capital growth by investing primarily inCUMULATIVE PERFORMANCE (%) companies of the People's Republic of China (PRC). JPM China A-Share Opportunities A (acc) - USD CSI 300 (Net)1) EXPERTISE 300 200 Fund Manager Howard Wang, Rebecca Jiang 250 150 % CHANGE FUND INFORMATION (JPMorgan Funds - China A-Share Opportunities Fund) 200 100 Fund base currency Launch Date REBASED 150 50 CNH 11/09/15 Total fund size (m) Inception NAV 100 0 USD 8,051.8 USD 15.61 50 -50 ISIN code 08/15 08/16 08/17 08/18 08/19 08/20 08/21 LU1255011170 Since 11/09/15 Current charge Since 1 month 3months 1 year 3 years 5 years Initial : Up to 5.0% of NAV launch Redemption : Currently 0% (Up to 0.5% of NAV) A (acc) - USD (NAV to NAV) -7.9 -4.4 20.8 98.6 143.2 149.4 Management fee : 1.5% p.a. A (acc) - USD (Charges applied)* -12.3 -9.0 15.0 89.2 131.5 137.4 Subscription Channel Benchmark (in USD)1) -6.7 -4.9 12.3 52.4 69.1 59.2 Cash A (acc) - RMB (NAV to NAV) -8.0 -4.5 11.8 88.4 136.4 151.7 SRS(for platforms only) A (acc) - RMB (Charges applied)* -12.4 -9.0 6.4 79.4 125.1 139.7 RATINGS A (acc) - SGD (NAV to NAV) -7.3 -2.6 19.0 97.4 - 105.5 A (acc) - SGD (Charges applied)* -11.8 -7.2 13.3 88.0 - 95.7 Morningstar Analyst Rating Silver Morningstar Rating™ ★★★★★ ANNUALISED -

2020 Annual Report Contents

2020 Annual Report Contents ABOUT US CORPORATE GOVERNANCE i Five-Year Summary 116 Corporate Governance Report 1 Introduction 131 Changes in the Share Capital and ’ 2 Business Performance at a Glance Shareholders Profile Directors, Supervisors, Senior Management 4 Chairman’s Statement 134 and Employees 152 Report of the Board of Directors and MANAGEMENT DISCUSSION AND ANALYSIS Significant Events 170 Report of the Supervisory Committee 8 Customer Development 14 Technology-Powered Business Transformation FINANCIAL STATEMENTS 20 Business Analysis 20 Performance Overview 172 Independent Auditor’s Report 23 Life and Health Insurance Business 179 Consolidated Income Statement 32 Property and Casualty Insurance Business 180 Consolidated Statement of Comprehensive 38 Investment Portfolio of Insurance Funds Income 181 Consolidated Statement of Financial Position 44 Banking Business 183 Consolidated Statement of Changes In Equity 54 Asset Management Business 184 Consolidated Statement of Cash Flows 60 Technology Business 185 Notes to Consolidated Financial Statements 68 Analysis of Embedded Value 79 Liquidity and Capital Resources 85 Risk Management OTHER INFORMATION 100 Sustainability 327 Ping An Milestones 113 Prospects of Future Development 328 Honors and Awards 329 Glossary 332 Corporate Information Cautionary Statements Regarding Forward-Looking Statements To the extent any statements made in this Report contain information that is not historical, these statements are essentially forward- looking. These forward-looking statements include but are not limited to projections, targets, estimates and business plans that the Company expects or anticipates may or may not occur in the future. Words such as “potential”, “estimates”, “expects”, “anticipates”, “objective”, “intends”, “plans”, “believes”, “will”, “may”, “should”, variations of these words and similar expressions are intended to identify forward-looking statements. -

Summary of 2020 Annual Report of Ping an Bank Co., Ltd

Security Code: 000001 Security Name: Ping An Bank Notice No.: 2021-006 Code of preference shares: 140002 Short name of preference shares: PYY01 Summary of 2020 Annual Report of Ping An Bank Co., Ltd. I. Important notes 1. This summary of annual report is extracted from the full text of the annual report. Investors are advised to carefully read the full annual report at the news media designated by the CSRC to have a comprehensive understanding of the business performance, financial position and future development plan of Ping An Bank Co., Ltd. (Hereinafter “Ping An Bank” or the “Bank”). 2. The Board of Directors (hereinafter referred to as the “Board”), the Supervisory Committee, the directors, the supervisors and senior management of the Bank guarantee the authenticity, accuracy and completeness of the contents of the 2020 Annual Report, in which there are no false representations, misleading statements or material omissions, and are severally and jointly take responsibilities for its contents. 3. The 16th meeting of the 11th session of the Board of the Bank deliberated the 2020 Annual Report together with its summary. The meeting required 15 directors to attend, and 15 directors attended the meeting. The Annual Report was approved unanimously at the meeting. 4. The 2020 annual financial reports prepared by the Bank was audited by PricewaterhouseCoopers Zhong Tian LLP (hereinafter referred to as “PwC”) according to the China Standards on Auditing and PwC issued a standard unqualified auditors’ report. 5. Xie Yonglin (the Bank’s Chairman), Hu Yuefei (the President), Xiang Youzhi (the Vice President and the CFO) and Zhu Peiqing (the head of the Finance Department) guarantee the authenticity, accuracy and completeness of the financial reports included in the 2020 Annual Report. -

Foundation. Innovation

Foundation. Innovation. LION-OCBC SECURITIES CHINA LEADERS ETF Seize the opportunity with 80* China leaders. *Based on the underlying Index Securities of the Hang Seng Stock Connect China 80 Index Introduction Investment Objective Today, China is an economic powerhouse that is too The investment objective of the Fund is to replicate as big to ignore. The way China influences the global closely as possible, before expenses, the performance economy is multi-faceted, and China's rise provides an of the Hang Seng Stock Connect China 80 Index using opportunity for investors to ride this wave of growth. a direct investment policy of investing in all, or The Lion-OCBC Securities China Leaders ETF allows substantially all, of the underlying Index Securities. investors to partake in China’s growth as well as The Index is compiled and calculated by Hang Seng diversify their investment portfolio through the inclusion Indexes Company Limited and is designed to measure of Chinese stocks in an easy and affordable way. the overall performance of 80 largest Chinese companies in terms of market capitalisation listed in Hong Kong and/or mainland China that are eligible for Northbound or Southbound trading under the Stock Connect schemes. Seize the opportunity with 80 China market giants Tap into the exciting growth opportunities Diversify your investment portfolio through offered by the second largest economy and ownership of China as a standalone asset class. second largest stock market in the world. China is now too big to be ignored. Gain easy access to the 80 largest Chinese Start investing from as little as SGD 25# in a companies like Ping An Insurance, Kweichow single trade of 10 units. -

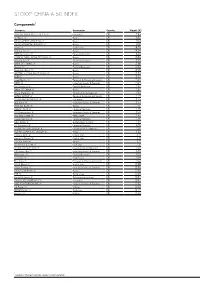

Stoxx® China a 50 Index

STOXX® CHINA A 50 INDEX Components1 Company Supersector Country Weight (%) PING AN INSUR GP CO. OF CN 'A' Insurance CN 7.93 Ind Bank 'A' Banks CN 5.82 CHINA MERCHANTS BANK 'A' Banks CN 5.13 CHINA MINSHENG BANKING 'A' Banks CN 4.91 Vanke 'A' Real Estate CN 4.76 Pudong Dev 'A' Banks CN 4.64 CITIC Securities 'A' Financial Services CN 3.25 AGRICULTURAL BANK OF CHINA 'A' Banks CN 2.84 Haitong Sec 'A' Financial Services CN 2.73 BANK OF COMMS.'A' Banks CN 2.66 Moutai 'A' Food & Beverage CN 2.60 Everbright Bank 'A' Banks CN 2.58 INDSTRL & COML.BK.OF CHINA 'A' Banks CN 2.29 BOB 'A' Banks CN 2.27 Gree Electric 'A' Personal & Household Goods CN 2.04 CRRC 'A' Industrial Goods & Services CN 2.04 Yili Company 'A' Food & Beverage CN 1.92 BANK OF CHINA 'A' Banks CN 1.84 China State Con 'A' Construction & Materials CN 1.83 MIDEA GROUP 'A' Personal & Household Goods CN 1.79 CHINA PAC.IN.(GROUP) 'A' Insurance CN 1.75 BOE Tech 'A' Industrial Goods & Services CN 1.67 PING AN BANK 'A' Banks CN 1.61 ORIENT SECS.'A' Financial Services CN 1.56 CN Shipbuilding 'A' Industrial Goods & Services CN 1.50 Poly Real Estate 'A' Real Estate CN 1.47 Huatai Security 'A' Financial Services CN 1.36 SAIC Motor 'A' Automobiles & Parts CN 1.35 GF Securities 'A' Financial Services CN 1.28 CHINA RAILWAY GROUP 'A' Construction & Materials CN 1.26 SUNING COMMERCE GROUP 'A' Retail CN 1.22 Hengrui Medi 'A' Health Care CN 1.17 Kangmei Pharm 'A' Health Care CN 1.17 Hua Xia Bank 'A' Banks CN 1.17 CHINA PTL.& CHM.'A' Oil & Gas CN 1.11 CHINA RAILWAY CON.'A' Construction & Materials CN 1.07 -

Ping an Insurance Group Co-A 13.41 Jiangsu Hengrui

元大投信海外基金持股明細表 日期:2018/06/30 單位:% 元大上證50基金 元大大中華TMT基金-新台幣 元大中國平衡基金-新台幣 元大巴西指數基金 PING AN INSURANCE GROUP CO-A 13.41 JIANGSU HENGRUI MEDICINE C-A 5.37 CHINA ZHONGWANG HOLDINGS LTD 7.40 VALE SA 12.19 KWEICHOW MOUTAI CO LTD-A 7.77 LEPU MEDICAL TECHNOLOGY-A 4.92 GENSCRIPT BIOTECH CORP 4.95 ITAU UNIBANCO HOLDING S-PREF 10.12 CHINA MERCHANTS BANK-A 5.76 SUNNY OPTICAL TECH 4.69 CHINA DATANG CORP RENEWABL-H 4.85 BANCO BRADESCO SA-PREF 7.02 INDUSTRIAL BANK CO LTD -A 3.79 KWEICHOW MOUTAI CO LTD-A 4.65 GREE ELECTRIC APPLIANCES I-A 3.89 AMBEV SA 6.59 INNER MONGOLIA YILI INDUS-A 3.58 KINGDEE INTERNATIONAL SFTWR 4.58 PING AN INSURANCE GROUP CO-A 3.78 PETROBRAS - PETROLEO BRAS-PR 5.23 JIANGSU HENGRUI MEDICINE C-A 3.54 國巨 4.29 CHINA TAIPING INSURANCE HOLD 3.71 PETROBRAS - PETROLEO BRAS 4.49 CHINA MINSHENG BANKING-A 3.50 AIER EYE HOSPITAL GROUP CO-A 4.02 JIANGSU KING`S LUCK BREWER-A 3.66 B3 SA-BRASIL BOLSA BALCAO 3.27 BANK OF COMMUNICATIONS CO-A 3.33 MIDEA GROUP CO LTD-A 4.00 BY-HEALTH CO LTD-A 3.38 ITAUSA-INVESTIMENTOS ITAU-PR 3.17 AGRICULTURAL BANK OF CHINA-A 2.78 INSPUR ELECTRONIC INFORMAT-A 3.69 INNER MONGOLIA FURUI MEDIC-A 2.49 BANCO DO BRASIL S.A. 1.91 CITIC SECURITIES CO-A 2.76 WANHUA CHEMICAL GROUP CO -A 3.51 SHANDONG GETTOP ACOUSTIC C-A 2.23 BANCO BRADESCO S.A. -

Krane-UBS China a Share Fund

Contact us: +(1) 855 8KRANE8 [email protected] Krane-UBS China A Share Fund Investment Philosophy: Fund Details by Share Class Institutional Investor The Krane-UBS China A Share Fund is driven by the view that the best way to Data as of 06/30/2021 capture the alpha potential of China's A Share market is to identify high quality, industry leading companies in strategic industries. The Fund is concentrated in a Ticker KUAIX KUASX select number of holdings and has a long-term investment horizon. Inception Date 6/15/2021 6/15/2021 Research Process: Gross Expense Ratio 1.55% 1.80% • Strategic Industries: Focus on strategic industries that could benefit from China's structural growth and transition to services-led economy. Net Expense Ratio 1.49%* 1.74%* • Fundamental Research: Sector analysts conduct in-depth industry and Minimum Investment $100,000 $2,500 company research, and the portfolio manager and analysts visit the companies MSCI China A MSCI China A in-person. Benchmark Index Onshore Index (Net) Onshore Index (Net) • Industry Leaders: Identify leading companies with good corporate governance, a proven business model, and solid core operations. • Portfolio Construction: Seek to maximize investment returns through our 20 to Top 10 Holdings as of 06/30/2021 Ticker % 60 "best stock ideas“. Holdings are subject to change. Portfolio Manager: WULIANGYE YIBIN CO LTD-A 000858 C2 9.83 Bin Shi is a member of the Global Emerging Market CHINA MERCHANTS BANK-A 600036 C1 9.65 and Asia Pacific Equities team at UBS Asset Management, the sub-adviser of the Fund, located in PING AN BANK CO LTD-A 000001 C2 9.62 Hong Kong. -

PING an BANK CO., LTD. 2020 THIRD QUARTERLY REPORT Section I Important Notes

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. OVERSEAS REGULATORY ANNOUNCEMENT This announcement is made pursuant to Rules 13.09 and 13.10B of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited. “The Announcement of Ping An Insurance (Group) Company of China, Ltd. in relation to the Disclosure of 2020 Third Quarterly Report of Ping An Bank”, which is published by Ping An Insurance (Group) Company of China, Ltd. on the website of the Shanghai Stock Exchange, is reproduced herein for your reference. By order of the Board Sheng Ruisheng Joint Company Secretary Shenzhen, PRC, October 21, 2020 As at the date of this announcement, the Executive Directors of the Company are Ma Mingzhe, Xie Yonglin, Tan Sin Yin, Yao Jason Bo and Cai Fangfang; the Non-executive Directors are Soopakij Chearavanont, Yang Xiaoping and Wang Yongjian; the Independent Non-executive Directors are Ge Ming, Ouyang Hui, Ng Sing Yip, Chu Yiyun and Liu Hong. Stock Code: 601318 Stock Short Name: Ping An of China Serial No.: Lin 2020-067 THE ANNOUNCEMENT OF PING AN INSURANCE (GROUP) COMPANY OF CHINA, LTD. IN RELATION TO THE DISCLOSURE OF 2020 THIRD QUARTERLY REPORT OF PING AN BANK The board of directors and all directors of Ping An Insurance (Group) Company of China, Ltd. -

March 2021 Overview CSE: PKK Disclaimer OTCQX: PKKFF

CSE: PKK | OTCQX: PKKFF March 2021 Overview CSE: PKK Disclaimer OTCQX: PKKFF FORWARD-LOOKING STATEMENTS Apart from historical data, this document may contain The Corporation is in no way obliged nor does it intend to information and statements concerning the future results update or revise these prospective statements on the basis of Peak Fintech Group (the “Corporation”, the “Peak Group” of new information, future events, etc. or “Peak”) which should be considered as prospective and forward-looking. These statements, when utilized, reflect the current vision of the Corporation concerning future events; they are based on information currently available to the Corporation and on assumptions which are considered reasonable. These prospective statements are subject to risks, uncertainties and other factors likely to influence the results, performance and achievements of the Corporation such that they could differ substantially from the results, performance and achievements prospective statements of this nature might imply. All $ values expressed in this presentation are in Canadian dollars 2 CSE: PKK The Problem OTCQX: PKKFF ? ▪ Over 100M small businesses in China have a hard time getting access to credit ▪ Blindly knocking on bank doors often leads to rejection and frustration 3 CSE: PKK The Lending Hub Ecosystem Solution OTCQX: PKKFF ▪ Access to all data on small business that would be Banks required by any lender to qualify the business for credit ▪ Accounting software ▪ Bank statements ▪ Government ▪ Other ▪ Specific lending criteria -

Beneficial Ownership Disclosure in Asian Publicly Listed Companies

Beneficial Ownership Disclosure in Asian Publicly Listed Companies 2017 This work is published under the responsibility of the Secretary-General of the OECD. The opinions expressed and arguments employed herein do not necessarily reflect the official views of OECD member countries. This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. © OECD 2017 2 Foreword A sound corporate governance infrastructure should combine transparency, accountability and integrity. This requires knowledge of beneficial ownership and ownership and control structures in listed companies. In line with Chapter 5 of the G20/OECD Principles of Corporate Governance concerning the development of frameworks for disclosure and transparency, the OECD Asian Roundtable on Corporate Governance (Asian Roundtable) recognises the need for an adequate regulatory framework for disclosure of beneficial ownership and control in Asian jurisdictions. This report reviews company practices regarding disclosure of beneficial ownership and control in Asia. The report was discussed by representatives from 14 Asian jurisdictions at the 2016 meeting of the Asian Roundtable in Seoul, Korea. Established in 1999, the Asian Roundtable serves as a valuable regional platform for exchanging experiences and advancing the reform agenda on corporate governance while promoting awareness and use of the G20/OECD Principles of Corporate Governance in Asia. It brings together policy makers, practitioners and experts on corporate governance from the Asian region, OECD countries and relevant international organisations. The roundtables are co-organised by the OECD and an Asian host country, in partnership with the Government of Japan. -

Fact Sheet As of June 30, 2019

Fact Sheet as of June 30, 2019 The China Fund Inc. INVESTMENT OBJECTIVE The investment objective of The China Fund, Inc. (the "Fund") is to acheive long -term capital appreciation. The Fund seeks to acheive its objective through investment in the equity securities of companies and other entities with significant assets, investments, production activities, trading or other business intrests in China or which derive a significant part of their revenue from China. The Fund has an operating policy that the Fund will invest at least 80% of its assets in China companies. For this purpose, ‘China companies’ are (i) companies for which the principal securities trading market is in China; (ii) companies for which the principal securities trading market is outside of China or in companies organized outside of China, that in both cases derive at least 50% of their revenues from goods or services sold or produced, or have at least 50% of their assets in China; or (iii) companies organized in China. Under the policy, China means the People’s Republic of China, including Hong Kong, and Taiwan. The Fund will provide its stockholders with at least 60 days’ prior notice of any change to this policy. FUND DATA NET ASSET VALUE (NAV) / MARKET PRICE Listing Date (NYSE) July 10, 1992 NAV / Market Price at Inception $13.15 / $14.26 Total Fund Assets (millions) $243.9 NAV / Market Price at 06/30/2019 Distribution Frequency Annual Benchmark MSCI China All Shares Index* Management Firm Matthews International Capital Management, LLC Portfolio Management Andrew Mattock, CFA HIGH / LOW RANGES (52 weeks) High / Low NAV $24.29 / $18.03 *Benchmark effective Jan 1, 2019.