Unassigned Fund Balance Is the Residual Classification for the Government‘S General Fund and Includes All Spendable Amounts Not Contained in the Other Classifications

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WHY ACCOUNTING and FINANCIAL REPORTING for GOVERNMENTS IS DIFFERENT THAN BUSINESSES by Jeffrey Winter

WHY ACCOUNTING AND FINANCIAL REPORTING FOR GOVERNMENTS IS DIFFERENT THAN BUSINESSES by Jeffrey Winter here are more than 80,000 user groups differ so too does the revenues through taxes on sales, governmental entities purpose of financial reporting. income, property and other activities. in the United States Governments are created to These types of revenues consisting of counties, provide their citizens with public are referred to as “nonexchange” municipalities,T townships, independent services that businesses are not transactions because they do not school districts and special districts. incentivized to provide. This includes result from a voluntary exchange Each government must adhere a wide variety of services from law between willing participants. In fact, to accounting and financial reporting enforcement to recreational activities the parties who provide the funding standards set by the Governmental to road repair. under nonexchange transactions are Accounting Standards Board (GASB). The users of these services are often not the same parties receiving These standards and the resulting interested in the government’s ability to the services funded – or at least they do financial statements are similar to those sustain the services and their ability to not benefit in direct correlation to the of businesses, but maintain a number do so efficiently. Further, they want to amount of funding provided. of key differences that often prompt know if the burden of paying for current As a result, the nature of individuals with business backgrounds services has already been funded or nonexchange transactions requires to ask the question: Why are the shifted to taxpayers in future years. different accounting considerations standards different for governments? Accordingly, governmental than exchange based revenues. -

David Bean David R

Speaker Biographies David Bean David R. Bean is the director of research and technical activities for the Governmental Accounting Standards Board. He assigns and provides oversight to the GASB’s research, technical, and administrative activities. Prior to joining the GASB in 1990, David worked in public accounting and government. He also has served as Deputy Chairman of the International Public Sector Accounting Standards Board (IPSASB). He was the lead author on the 1988 Governmental Accounting, Auditing and Financial Reporting and was the founder of the GAAFR Review. He was the last director of the National Council on Governmental Accounting before the formation of the GASB in 1984. David is a member of the Government Finance Officers Association, the Connecticut and Illinois Government Finance Officers Associations, the American Institute of Certified Public Accountants, the Illinois CPA Society, the Association of Government Accountants, the National Federation of Municipal Analysts, and the Municipal Analysts Group of New York. Lisa Parker Lisa Parker is a senior project manager with the Governmental Accounting Standards Board (GASB). Prior to joining the GASB in 2008, Lisa worked for Runyon Kersteen Ouellette CPAs for 10 years, the town of Old Orchard Beach, Maine as finance director and interim town manager for 2 years, and the city of Saco, Maine as finance director for 8 years. Lisa is a certified public accountant and a chartered global management accountant. She also is a member of the Association of Governmental Accountants, the American Institute of Certified Public Accountants, and the Maine Society of Certified Public Accountants, where she served as president. -

Governmental Accounting

SECTION I--GOVERNMENTAL ACCOUNTING MEASUREMENT FOCUS BASIS OF ACCOUNTING (MFBA) Traditionally, governments have used essentially the same accounting as private-sector businesses for their proprietary funds (enterprise and internal service funds) and similar trust funds (nonexpendable and pension trust funds). In both cases, the measurement focus of the operating statement has been on the changes in economic resources (changes in total net position). Such changes have been recognized as soon as the underlying event or transaction has occurred, regardless of the timing of the related cash flow – the accrual basis of accounting. Thus, under GASB 34, proprietary funds (enterprise and internal service funds) and fiduciary funds recognize revenues as soon as they are earned and expenses as soon as a liability is incurred, just like private-sector businesses. Governments have always taken a very different approach, however, in accounting for their governmental funds and expendable trust funds. The measurement focus here has been on changes in current financial resources. Additionally, changes in current financial resources have only been recognized to the extent that they normally are expected to have an impact upon near-term cash flows (modified accrual basis of accounting). Therefore, in addition to being earned, the inflows of expendable financial resources must also be available to pay for current period liabilities before it can be recognized as revenue. Likewise, in several cases (interest payable, compensated absences) no expenditure is recognized in a governmental fund for future outflows of financial resources that does not represent a use of current financial resources. This unique MFBA for governmental funds is reminiscent of fund accounting’s historical link with checkbook accounting (funds originally developed out of separate checking accounts) and is consistent with the near-term financing focus that typically characterizes a government’s operating budget. -

Governmental Accounting

SECTION I--GOVERNMENTAL ACCOUNTING GOVERNMENTAL ACCOUNTING Fund Accounting Statute indicates resources which a school is permitted to receive and expressly and/or implicitly states the purposes for which those resources may be used. The accounting system used by a school should provide for legal compliance; that is, resources are received and spent according to law. For this reason, schools have evolved a means of indicating legal compliance by use of “fund accounting.” The Governmental Accounting Standards Board has defined the term “fund” as follows: A fund is a fiscal and accounting entity with a self-balancing set of accounts recording cash and other financial resources, together with all related liabilities and residual equities or balances, and changes therein, which are segregated for the purpose of carrying on specific activities or attaining certain objectives in accordance with special regulations, restrictions, or limitations. The diverse nature of a school’s operations and the necessity of determining legal compliance preclude a single set of accounts for recording and summarizing all the financial transactions. Instead, the required accounts are organized on the basis of funds, each of which is completely independent of any other. Each fund must be so accounted for that the identity of its resources, obligations, revenues, expenditures, and fund equities is continually maintained. These purposes are accomplished by providing a complete self-balancing set of accounts for each fund which shows its assets, liabilities, fund balances or net position, revenues and expenditures/expenses. An account is defined as a formal record of a particular type of transaction. A group of accounts comprises a ledger. -

Governmental Accounting

SECTION I--GOVERNMENTAL ACCOUNTING MEASUREMENT FOCUS BASIS OF ACCOUNTING (MFBA) Traditionally, governments have used essentially the same accounting as private-sector businesses for their proprietary funds (enterprise and internal service funds) and similar trust funds (nonexpendable and pension trust funds). In both cases, the measurement focus of the operating statement has been on the changes in economic resources (changes in total net position). Such changes have been recognized as soon as the underlying event or transaction has occurred, regardless of the timing of the related cash flow – the accrual basis of accounting. Thus, under GASB 34, proprietary funds (enterprise and internal service funds) and fiduciary funds recognize revenues as soon as they are earned and expenses as soon as a liability is incurred, just like private-sector businesses. Governments have always taken a very different approach, however, in accounting for their governmental funds and expendable trust funds. The measurement focus here has been on changes in current financial resources. Additionally, changes in current financial resources have only been recognized to the extent that they normally are expected to have an impact upon near-term cash flows (modified accrual basis of accounting). Therefore, in addition to being earned, the inflows of expendable financial resources must also be available to pay for current period liabilities before it can be recognized as revenue. Likewise, in several cases (interest payable, compensated absences) no expenditure is recognized in a governmental fund for future outflows of financial resources that does not represent a use of current financial resources. This unique MFBA for governmental funds is reminiscent of fund accounting’s historical link with checkbook accounting (funds originally developed out of separate checking accounts) and is consistent with the near-term financing focus that typically characterizes a government’s operating budget. -

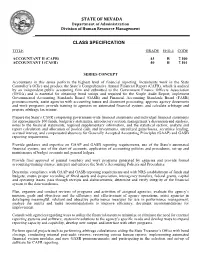

Accountant 07.100 Class Specification

STATE OF NEVADA Department of Administration Division of Human Resource Management CLASS SPECIFICATION TITLE GRADE EEO-4 CODE ACCOUNTANT II (CAFR) 43 B 7.100 ACCOUNTANT I (CAFR) 40 B 7.101 SERIES CONCEPT Accountants in this series perform the highest level of financial reporting. Incumbents work in the State Controller’s Office and produce the State’s Comprehensive Annual Financial Report (CAFR), which is audited by an independent public accounting firm and submitted to the Government Finance Officers Association (GFOA) and is essential for obtaining bond ratings and required for the Single Audit Report; implement Governmental Accounting Standards Board (GASB) and Financial Accounting Standards Board (FASB) pronouncements; assist agencies with accounting issues and document processing; approve agency documents and work programs; provide training to agencies on automated financial system; and calculate arbitrage and prepare arbitrage tax returns. Prepare the State’s CAFR comprising government-wide financial statements and individual financial statements for approximately 100 funds, budgetary statements, introductory section, management’s discussion and analysis, notes to the financial statements, required supplementary information, and the statistical section; analyze and report calculation and allocation of pooled cash and investments, unrealized gains/losses, securities lending, accrued interest, and compensated absences for Generally Accepted Accounting Principles (GAAP) and GASB reporting requirements. Provide guidance and expertise on GAAP and GASB reporting requirements, use of the State’s automated financial system, use of the chart of accounts, application of accounting policies and procedures, set-up and maintenance of budget accounts and general ledgers. Provide final approval of journal vouchers and work programs generated by agencies and provide formal accounting training classes; interpret and enforce the State’s Accounting Policies and Procedures. -

Basic Accounting Terminology: • Event: a Happening Or Consequence

GOVERNMENTAL ACCOUNTING All those involved in the oversight or management of government operations, and those whose livelihood and interest rely on the finances of local governments, need to have a clear understanding of governmental accounting, auditing, and financial reporting which are based on a sound set of principles and interrelated practices and procedures. Accounting, financial reporting, and the financial statement audit provide the informational infrastructure of public finance. Accountability: Term used by GASB to describe a government’s duty to justify the raising and spending of public resources. The GASB has identified accountability as the “paramount objective” of financial reporting “from which all other objectives must flow”. Accounting and financial reporting (primarily the responsibility of management) are complementary rather than identical. Accounting: The process of assembling, analyzing, classifying, and recording data relevant to a government’s finances. Financial reporting: “Accounting” and “financial reporting” are similar but distinctly different terms that are often used together. The process of taking the information thus assembled, analyzed, classified, and recorded and providing it in usable form to those who need it. Financial reporting can take one of three forms: internal financial reporting (management reports), special purpose financial reporting (outside parties), and general purpose external financial reporting (GPEFR). The nationally recognized standards that govern GPEFR are known as generally accepted accounting principles (GAAP). 1 Display: The display method of communication provides that items are reported as dollar amounts on the face of the financial statements if they both 1) meet the definition of one of the seven financial statement elements and 2) can be reliably measured. -

How to Read Governmental Financial Statements, Part 1

FOCUS: FINANCE AND BUDGETING How to Read Governmental Financial Statements, Part 1 Gregory S. Allison anagement and elected to-actual financial statements (that officials of governmen- is, statements comparing budgeted Mtal entities receive an of- amounts with actual results); brief ten overwhelming supply of finan- analyses of tax billings and collec- cial data. This information takes tions, as well as general revenue various forms—budgetary re- collections; and investment sum- ports, internally generated finan- maries—these are a few examples cial statements, schedules and of the internal information that summaries, and audited annual should be available to manage- financial statements. Usually, in- ment and elected officials on a ternally generated information continuing basis. In most cases the comes in a format that is com- format of these presentations is left prehensible to accountants and to the discretion of management, nonaccountants alike. Compre- elected officials, and staff respon- hending the audited financial sible for preparing the informa- statements, however, requires at tion. Some governing bodies may least a minimal understanding of desire a summary of revenues by the principles of governmental category (property taxes, utility financial reporting. This article, billings and collections, other the first of two parts, is designed taxes, and so forth). Others may to make the audited financial focus on key ratios on a monthly statements more user-friendly and basis (for example, tax collection to provide a key to unlocking the rates and expenditures to date basic information they contain. compared with budget projec- The article focuses on current tions). reporting requirements. Part 2, Governments typically operate scheduled for a future issue of purely from a cash perspective: rev- Popular Government, will intro- enue is recognized when cash duce readers to new governmental is collected, and expenditures are financial reporting requirements that paring financial statements for external recognized as cash is disbursed. -

Beginning Governmental Accounting

Beginning Governmental 0011 0010 1010 1101 0001 0100Accounting 1011 Presented by: Elizabeth Alba, Instructor Yakima Valley Community College 0011 0010 1010 1101 0001 0100 1011 WMCA Workshop 1 March 19, 2014 2 45 0011 0010 1010 1101 0001 0100 1011 Please turn your cell phone to vibrate mode…. Thank you 12 45 Agenda • Basic Accounting Theory – Understanding the basic accounting equation – Identify asset and liability accounts • Double Entry Accounting – Record transactions using debits and credits – Understand how debits and credits affect accounts • Accounting System and Records – Understand the difference between journals and ledgers – Relate the journals and ledgers to computerized records – Learn the value and purpose of a trial balance • The Basis of Accounting – Define the basis of accounting – Contrast the three common bases of accounting – Understand when to recognize a revenue or expense under the modified accrual basis of accounting. • Budgets – Why are they important – Analysis of the budget Basic Accounting Theory Why Use Accounting? Generally Accepted Accounting Principles (GAAP) is a set of rules for businesses and governments to follow so their financial statements/reports can easily be compared to other businesses. Without GAAP, businesses could record and report data in any manner – making comparison difficult. Government vs. Private Business 0011 0010• Providing 1010 1101 0001services 0100 1011 • Profit driven • Fiscal and operational • Value for the owner or accountability shareholder is a major • Must comply with focus finance related legal • Income is expect to be and contractual issues more than the1 cost • Sometimes Revenues (Revenues must will not cover the cost exceed expenses to be of governmental profitable) 2 activites 45 Understanding the Accounting Equation • The basic accounting equation is the cornerstone of the accounting process. -

Part 1: a Basic Background & Overview of SLG Accounting

GAQC Web Event: A Basic Background & Overview February 6, 2018 of State and Local Government Accounting A Basic Background & Overview of State and Local Government Accounting Part 1 of a 2-Part Series A Governmental Audit Quality Center Web Event February 6, 2018 Presenters Corey Arvizu, CPA Frank Crawford, CPA HeinfeldMeech Crawford & Associates 2 1 GAQC Web Event: A Basic Background & Overview February 6, 2018 of State and Local Government Accounting What We Will Cover State and Local Government Reporting Principles Financial Reporting Entity Basic Financial Statements 3 Terminology & Abbreviations (for reference) SLG State and Local Government GAAP Generally Accepted Accounting Principles BFS Basic Financial Statements MD&A Management Discussion & Analysis RSI Required Supplementary Information PG Primary Government CAFR Comprehensive Annual Financial Report 4 2 GAQC Web Event: A Basic Background & Overview February 6, 2018 of State and Local Government Accounting Panel Discussion What benefits have your experienced in your career by specializing in governmental accounting and auditing? 5 SLG Reporting Principles History of the Governmental Accounting Standards Board Objectives of SLG Financial Reporting GAAP 3 GAQC Web Event: A Basic Background & Overview February 6, 2018 of State and Local Government Accounting History of the GASB Financial Accounting Foundation (FAF) Financial Accounting Governmental Standards Board Accounting Standards (FASB) Board (GASB) 7 GASB GAAP AICPA recognizes GASB as the standard-setting authority for GAAP for state and local governments. Definition of a Government: • GASB Codification 1000.801 & 1000 fn 4 • Factors that are irrelevant for determining appropriate GAAP – Incorporation as a not for profit organization – Exempt from federal income taxation (e.g., Internal Revenue Code section 501) 8 4 GAQC Web Event: A Basic Background & Overview February 6, 2018 of State and Local Government Accounting Objectives of Governmental Financial Reporting 1. -

GAAFR Appendix A: Illustrative Journal Entries

Appendix A Illustrative Journal Entries Illustrative journal entries This appendix provides information to support the fund financial statements presented in the illustrative CAFR found in Appendix D. This appendix relies exclusively on journal entries to illustrate how activity is recorded.1 A complete set of journal entries is provided for each fund type used in the illustrative financial statements,2 with the exception of the special revenue fund type (which reports the same basic types of transactions as the general fund). When the illustrative financial statements include more than one fund of a given fund type, sample journal entries are provided for only one of the individual funds. The sample journal entries are presented by fund type in the following order, with the page numbers for each fund’s entries in parenthesis: General fund (A-2 – A-30) Debt service fund (A-30 – A-36) Capital projects fund (A-37 – A-46) Permanent fund (A-46 – A-47) Enterprise fund (A-48 – A-55) Internal service fund (A-56 – A-59) Pension (and other employee benefit) trust fund (A-60 – A-63) Private purpose trust fund (A-63 – A-64) Investment trust fund (A-64 – A-67) Custodial fund (A-67 – A-68) Journal entries have been numbered sequentially throughout this appendix for journal entries of all fund types. Also, amounts throughout are expressed in whole 1. In practice, other techniques often are used for the initial recording of certain types of transactions during the fiscal year. 2. The illustrative financial statements do not include agency funds as that fund type has been replaced with custodial funds. -

Managing and Accounting for Fixed Assets

FOCUS: FINANCE AND BUDGETING Managing and Accounting for Fixed Assets William C. Rivenbark ixed assets represent a signifi- at their original historical cost and cant investment of public dol- remain at that value throughout Flars for local governments and their life. Fixed assets purchased by public authorities. Items that consti- “proprietary funds” (business-like tute fixed assets are tangible in na- funds, such as public utilities) are ture and normally have a useful life capitalized at their original histori- of at least two years. Commonly cal cost and depreciated over their used classifications of fixed assets are useful life. Items of insignificant land, buildings, equipment, and ve- value are simply expensed in their hicles. year of purchase. Maintaining control of fixed assets is Localities tend to capi- a function of the entire organization, talize assets at dollar values not just the accounting department. To much lower than needed, maintain financial control of fixed as- ✓ setting policy primarily to sets from an accounting perspective, a satisfy the internal control locality must properly report their value FIXED function rather than the fi- on its annual financial statements. To portant to staff, managers, ASSET nancial reporting function.2 They maintain internal control from a man- council members, investors, and should set the dollar value for capi- agement perspective (that is, to ensure creditors. External auditors issue a talization of assets with the objective of use of the assets for authorized pur- “qualified audit opinion” if they find accurately reporting the value of fixed poses and to prevent their misuse or that the financial statements are inad- assets on their annual financial state- theft), the locality must assign custodial equate in a material respect.