Liqudity in Cryptocurrency Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Peer Co-Movement in Crypto Markets

Peer Co-Movement in Crypto Markets G. Schwenkler and H. Zheng∗ February 4, 2021y Abstract We show that peer linkages induce significant price co-movement in crypto markets in excess of common risk factors and correlated demand shocks. When large abnormal return shocks hit one crypto, its peers experience unusually large abnormal returns of the opposite sign. These effects are primarily concentrated among smaller peers and revert after several weeks, resulting in predictable returns. We develop trading strategies that exploit this rever- sal, and show that they are profitable even after accounting for trading fees and frictions. We establish our results by identifying crypto peers through co-mentions in online news using novel natural language processing technologies. Keywords: Cryptocurrencies, peers, co-movement, competition, natural language pro- cessing. JEL codes: G12, G14, C82. ∗Schwenkler is at the Department of Finance, Santa Clara University Leavey School of Business. Zheng is at the Department of Finance, Boston University Questrom School of Business. Schwenkler is corresponding author. Email: [email protected], web: http://www.gustavo-schwenkler.com. yThis is a revision of a previous paper by the two authors called \Competition or Contagion: Evidence from Cryptocurrency Markets." We are grateful to Jawad Addoum (discussant), Daniele Bianchi (discussant), Will Cong, Tony Cookson, Sanjiv Das, Seoyoung Kim, Andreas Neuhierl, Farzad Saidi, and Antoinette Schoar, seminar participants at Boston University and the Society for Financial Econometrics, and the participants at the 2020 Finance in the Cloud III Virtual Conference, the 2020 MFA Annual Meeting, the 3rd UWA Blockchain, Cryptocurrency and FinTech Conference, and the 2020 INFORMS Annual Meeting for useful comments and suggestions. -

Linking Wallets and Deanonymizing Transactions in the Ripple Network

Proceedings on Privacy Enhancing Technologies ; 2016 (4):436–453 Pedro Moreno-Sanchez*, Muhammad Bilal Zafar, and Aniket Kate* Listening to Whispers of Ripple: Linking Wallets and Deanonymizing Transactions in the Ripple Network Abstract: The decentralized I owe you (IOU) transac- 1 Introduction tion network Ripple is gaining prominence as a fast, low- cost and efficient method for performing same and cross- In recent years, we have observed a rather unexpected currency payments. Ripple keeps track of IOU credit its growth of IOU transaction networks such as Ripple [36, users have granted to their business partners or friends, 40]. Its pseudonymous nature, ability to perform multi- and settles transactions between two connected Ripple currency transactions across the globe in a matter of wallets by appropriately changing credit values on the seconds, and potential to monetize everything [15] re- connecting paths. Similar to cryptocurrencies such as gardless of jurisdiction have been pivotal to their suc- Bitcoin, while the ownership of the wallets is implicitly cess so far. In a transaction network [54, 55, 59] such as pseudonymous in Ripple, IOU credit links and transac- Ripple [10], users express trust in each other in terms tion flows between wallets are publicly available in an on- of I Owe You (IOU) credit they are willing to extend line ledger. In this paper, we present the first thorough each other. This online approach allows transactions in study that analyzes this globally visible log and charac- fiat money, cryptocurrencies (e.g., bitcoin1) and user- terizes the privacy issues with the current Ripple net- defined currencies, and improves on some of the cur- work. -

User Manual Ledger Nano S

User Manual Ledger Nano S Version control 4 Check if device is genuine 6 Buy from an official Ledger reseller 6 Check the box contents 6 Check the Recovery sheet came blank 7 Check the device is not preconfigured 8 Check authenticity with Ledger applications 9 Summary 9 Learn more 9 Initialize your device 10 Before you start 10 Start initialization 10 Choose a PIN code 10 Save your recovery phrase 11 Next steps 11 Update the Ledger Nano S firmware 12 Before you start 12 Step by step instructions 12 Restore a configuration 18 Before you start 19 Start restoration 19 Choose a PIN code 19 Enter recovery phrase 20 If your recovery phrase is not valid 20 Next steps 21 Optimize your account security 21 Secure your PIN code 21 Secure your 24-word recovery phrase 21 Learn more 22 Discover our security layers 22 Send and receive crypto assets 24 List of supported applications 26 Applications on your Nano S 26 Ledger Applications on your computer 27 Third-Party applications on your computer 27 If a transaction has two outputs 29 Receive mining proceeds 29 Receiving a large amount of small transactions is troublesome 29 In case you received a large amount of small payments 30 Prevent problems by batching small transactions 30 Set up and use Electrum 30 Set up your device with EtherDelta 34 Connect with Radar Relay 36 Check the firmware version 37 A new Ledger Nano S 37 A Ledger Nano S in use 38 Update the firmware 38 Change the PIN code 39 Hide accounts with a passphrase 40 Advanced Passphrase options 42 How to best use the passphrase feature 43 -

On the Relationship of Cryptocurrency Price with US Stock and Gold Price Using Copula Models

mathematics Article On the Relationship of Cryptocurrency Price with US Stock and Gold Price Using Copula Models Jong-Min Kim 1 , Seong-Tae Kim 2 and Sangjin Kim 3,* 1 Statistics Discipline, University of Minnesota at Morris, Morris, MN 56267, USA; [email protected] 2 Department of Mathematics, North Carolina A&T State University, Greensboro, NC 27411, USA; [email protected] 3 Department of Management and Information Systems, Dong-A University, Busan 49236, Korea * Correspondence: [email protected] Received: 15 September 2020; Accepted: 20 October 2020; Published: 23 October 2020 Abstract: This paper examines the relationship of the leading financial assets, Bitcoin, Gold, and S&P 500 with GARCH-Dynamic Conditional Correlation (DCC), Nonlinear Asymmetric GARCH DCC (NA-DCC), Gaussian copula-based GARCH-DCC (GC-DCC), and Gaussian copula-based Nonlinear Asymmetric-DCC (GCNA-DCC). Under the high volatility financial situation such as the COVID-19 pandemic occurrence, there exist a computation difficulty to use the traditional DCC method to the selected cryptocurrencies. To solve this limitation, GC-DCC and GCNA-DCC are applied to investigate the time-varying relationship among Bitcoin, Gold, and S&P 500. In terms of log-likelihood, we show that GC-DCC and GCNA-DCC are better models than DCC and NA-DCC to show relationship of Bitcoin with Gold and S&P 500. We also consider the relationships among time-varying conditional correlation with Bitcoin volatility, and S&P 500 volatility by a Gaussian Copula Marginal Regression (GCMR) model. The empirical findings show that S&P 500 and Gold price are statistically significant to Bitcoin in terms of log-return and volatility. -

Vulnerability of Blockchain Technologies to Quantum Attacks

Vulnerability of Blockchain Technologies to Quantum Attacks Joseph J. Kearneya, Carlos A. Perez-Delgado a,∗ aSchool of Computing, University of Kent, Canterbury, Kent CT2 7NF United Kingdom Abstract Quantum computation represents a threat to many cryptographic protocols in operation today. It has been estimated that by 2035, there will exist a quantum computer capable of breaking the vital cryptographic scheme RSA2048. Blockchain technologies rely on cryptographic protocols for many of their essential sub- routines. Some of these protocols, but not all, are open to quantum attacks. Here we analyze the major blockchain-based cryptocurrencies deployed today—including Bitcoin, Ethereum, Litecoin and ZCash, and determine their risk exposure to quantum attacks. We finish with a comparative analysis of the studied cryptocurrencies and their underlying blockchain technologies and their relative levels of vulnerability to quantum attacks. Introduction exist to allow the legitimate owner to recover this account. Blockchain systems are unlike other cryptosys- tems in that they are not just meant to protect an By contrast, in a blockchain system, there is no information asset. A blockchain is a ledger, and as central authority to manage users’ access keys. The such it is the asset. owner of a resource is by definition the one hold- A blockchain is secured through the use of cryp- ing the private encryption keys. There are no of- tographic techniques. Notably, asymmetric encryp- fline backups. The blockchain, an always online tion schemes such as RSA or Elliptic Curve (EC) cryptographic system, is considered the resource— cryptography are used to generate private/public or at least the authoritative description of it. -

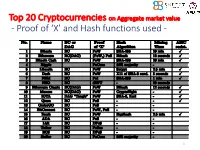

Proof of 'X' and Hash Functions Used

Top 20 Cryptocurrencies on Aggregate market value - Proof of ‘X’ and Hash functions used - 1 ISI Kolkata BlockChain Workshop, Nov 30th, 2017 CRYPTOGRAPHY with BlockChain - Hash Functions, Signatures and Anonymization - Hiroaki ANADA*1, Kouichi SAKURAI*2 *1: University of Nagasaki, *2: Kyushu University Acknowledgements: This work is supported by: Grants-in-Aid for Scientific Research of Japan Society for the Promotion of Science; Research Project Number: JP15H02711 Top 20 Cryptocurrencies on Aggregate market value - Proof of ‘X’ and Hash functions used - 3 Table of Contents 1. Cryptographic Primitives in Blockchains 2. Hash Functions a. Roles b. Various Hash functions used for Proof of ‘X’ 3. Signatures a. Standard Signatures (ECDSA) b. Ring Signatures c. One-Time Signatures (Winternitz) 4. Anonymization Techniques a. Mixing (CoinJoin) b. Zero-Knowledge proofs (zk-SNARK) 5. Conclusion 4 Brief History of Proof of ‘X’ 1992: “Pricing via Processing or Combatting Junk Mail” Dwork, C. and Naor, M., CRYPTO ’92 Pricing Functions 2003: “Moderately Hard Functions: From Complexity to Spam Fighting” Naor, M., Foundations of Soft. Tech. and Theoretical Comp. Sci. 2008: “Bitcoin: A peer-to-peer electronic cash system” Nakamoto, S. Proof of Work 5 Brief History of Proof of ‘X’ 2008: “Bitcoin: A peer-to-peer electronic cash system” Nakamoto, S. Proof of Work 2012: “Peercoin” Proof of Stake (& Proof of Work) ~ : Delegated Proof of Stake, Proof of Storage, Proof of Importance, Proof of Reserves, Proof of Consensus, ... 6 Proofs of ‘X’ 1. Proof of Work 2. Proof of Stake Hash-based Proof of ‘X’ 3. Delegated Proof of Stake 4. Proof of Importance 5. -

Using Blockchain Technology to Secure the Internet of Things

Using Blockchain Technology to Secure the Internet of Things Presented by the Blockchain/ Distributed Ledger Working Group © 2018 Cloud Security Alliance – All Rights Reserved. You may download, store, display on your computer, view, print, and link to Using Blockchain Technology to Secure the Internet of Things subject to the following: (a) the Document may be used solely for your personal, informational, non- commercial use; (b) the Report may not be modified or altered in any way; (c) the Document may not be redistributed; and (d) the trademark, copyright or other notices may not be removed. You may quote portions of the Document as permitted by the Fair Use provisions of the United States Copyright Act, provided that you attribute the portions to the Using Blockchain Technology to Secure the Internet of Things paper. Blockchain/Distributed Ledger Technology Working Group | Using Blockchain Technology to Secure the Internet of Things 2 © Copyright 2018, Cloud Security Alliance. All rights reserved. ABOUT CSA The Cloud Security Alliance is a not-for-profit organization with a mission to promote the use of best practices for providing security assurance within Cloud Computing, and to provide education on the uses of Cloud Computing to help secure all other forms of computing. The Cloud Security Alliance is led by a broad coalition of industry practitioners, corporations, associations and other key stakeholders. For further information, visit us at www.cloudsecurityalliance.org and follow us on Twitter @cloudsa. Blockchain/Distributed Ledger Technology Working Group | Using Blockchain Technology to Secure the Internet of Things 3 © Copyright 2018, Cloud Security Alliance. All rights reserved. -

![Can Ethereum Classic Reach 1000 Dollars Update [06-07-2021] 42 Loss in the Last 24 Hours](https://docslib.b-cdn.net/cover/0683/can-ethereum-classic-reach-1000-dollars-update-06-07-2021-42-loss-in-the-last-24-hours-490683.webp)

Can Ethereum Classic Reach 1000 Dollars Update [06-07-2021] 42 Loss in the Last 24 Hours

1 Can Ethereum Classic Reach 1000 Dollars Update [06-07-2021] 42 loss in the last 24 hours. At that time Bitcoin reached its all-time high of 20,000 and so did Ethereum ETH which surpassed 1,000. 000 to reach 1; Tezos XTZ is priced at 2. In the unlikely event of a significant change for the worst, we expect the Bitcoin price to continue appreciating. ERC-721 started as a EIP draft written by dete and first came to life in the CryptoKitties project by Axiom Zen. ERC-721 A CLASS OF UNIQUE TOKENS. It does not mandate a standard for token metadata or restrict adding supplemental functions. Think of them like rare, one-of-a-kind collectables. The Standard. Institutions are mandating that they invest in clean green technologies and that s what ethereum is becoming, she said. Unlike bitcoin s so-called proof of work, which rewards miners who are competing against each other to use computers and energy to record and confirm transactions on its blockchain, ethereum plans to adopt the more efficient proof of stake model, which chooses a block validator at random based on how much ether it controls. Kaspar explained her thesis Friday on Yahoo Finance Live, citing new updates coming to the cryptocurrency s network later this year. 42 loss in the last 24 hours. At that time Bitcoin reached its all-time high of 20,000 and so did Ethereum ETH which surpassed 1,000. 000 to reach 1; Tezos XTZ is priced at 2. In the unlikely event of a significant change for the worst, we expect the Bitcoin price to continue appreciating. -

A Survey on Volatility Fluctuations in the Decentralized Cryptocurrency Financial Assets

Journal of Risk and Financial Management Review A Survey on Volatility Fluctuations in the Decentralized Cryptocurrency Financial Assets Nikolaos A. Kyriazis Department of Economics, University of Thessaly, 38333 Volos, Greece; [email protected] Abstract: This study is an integrated survey of GARCH methodologies applications on 67 empirical papers that focus on cryptocurrencies. More sophisticated GARCH models are found to better explain the fluctuations in the volatility of cryptocurrencies. The main characteristics and the optimal approaches for modeling returns and volatility of cryptocurrencies are under scrutiny. Moreover, emphasis is placed on interconnectedness and hedging and/or diversifying abilities, measurement of profit-making and risk, efficiency and herding behavior. This leads to fruitful results and sheds light on a broad spectrum of aspects. In-depth analysis is provided of the speculative character of digital currencies and the possibility of improvement of the risk–return trade-off in investors’ portfolios. Overall, it is found that the inclusion of Bitcoin in portfolios with conventional assets could significantly improve the risk–return trade-off of investors’ decisions. Results on whether Bitcoin resembles gold are split. The same is true about whether Bitcoins volatility presents larger reactions to positive or negative shocks. Cryptocurrency markets are found not to be efficient. This study provides a roadmap for researchers and investors as well as authorities. Keywords: decentralized cryptocurrency; Bitcoin; survey; volatility modelling Citation: Kyriazis, Nikolaos A. 2021. A Survey on Volatility Fluctuations in the Decentralized Cryptocurrency Financial Assets. Journal of Risk and 1. Introduction Financial Management 14: 293. The continuing evolution of cryptocurrency markets and exchanges during the last few https://doi.org/10.3390/jrfm years has aroused sparkling interest amid academic researchers, monetary policymakers, 14070293 regulators, investors and the financial press. -

Ethereum Classic Price Prediction 2030

1 Ethereum Classic Price Prediction 2030 Update [06-08-2021] There are various cryptocurrencies out now in the bitcoin market, and people worldwide and mostly in the countries like United States , are investing in these digital currencies. 00000001 Ethereum max 7d low Emax 7d high- 0. And this particular blockchain allows to grants investors security and also control for all of their digital assets. Firstly, we have to be sure about the amount of ETH in our wallet to cover our transaction fees. Once OKExChain supports EVM, developers can use the development tools and languages of Ethereum to develop smart contracts on OKExChain. The contract launched the Beacon Chain, the first stage in the ETH 2. Most are confident that Ethereum 2. Ethereum s Growing Transaction Fees Shouldn t Stop Users. Is Cardano or Ethereum a Better Investment. It was developed in 2017 by Charles Hoskinson, who was previously involved in creating Ethereum itself. In other words, we have defined proof, in the per-coin values of both Bitcoin and Ethereum, that increases of 500 , 1,000 and more are not unprecedented or wildly unreasonable in this market , especially for coins that started out at a few cents. And this has given the latter a significant advantage over the former. At the same time, it is also going to take many other alts with it to new highs. A 10k price is definitely on the cards with so many Decentralized finance apps shifting to their protocols. If Ethereum could hit 10k by the end of 2021 then it would cross the 1 trillion market cap and might become the 2nd cryptocurrency to do so. -

Blockchain Security

CO 445H BLOCKCHAIN SECURITY Dr. Benjamin Livshits Apps Stealing Your Data 2 What are they doing with this data? We don’t know what is happening with this data once it is collected. It’s conceivable that this information could be analysed alongside other collections of data to provide insights into a person’s identity, online activity, or even political beliefs. Cambridge Analytica and other dodgy behavioural modification companies taught us this. The fact is we don’t know what is happening to the data that is being exfiltrated in this way. And in most cases we are not even aware this is taking place. The only reason we know about this collection of data-stealing apps is because security researcher, Patrick Wardle told us. Sudo Security Group’s GuardianApp claims another set of dodgy privacy eroding iOS apps, while Malwarebytes has yet another list of bad actors. http://www.applemust.com/how-to-stop-mac-and-ios-apps-stealing-your-data/ From Malwarebytes 3 https://objective-see.com/blog/blog_0x37.html Did You Just Steal My Browser History!? 4 Adware Doctor Stealing Browsing History 5 https://vimeo.com/288626963 Blockchain without the Hype 6 Distributed ledgers and blockchain specifically are about establishing distributed trust How can a community of individuals agree on the state of the world – or just the state of a database – without the risk of outside control or censorship Doing this with open-source code and cryptography turns out to be a difficult problem Distributed Trust 7 A blockchain is a decentralized, distributed and public -

Exploring the Interconnectedness of Cryptocurrencies Using Correlation Networks

Exploring the Interconnectedness of Cryptocurrencies using Correlation Networks Andrew Burnie UCL Computer Science Doctoral Student at The Alan Turing Institute [email protected] Conference Paper presented at The Cryptocurrency Research Conference 2018, 24 May 2018, Anglia Ruskin University Lord Ashcroft International Business School Centre for Financial Research, Cambridge, UK. Abstract Correlation networks were used to detect characteristics which, although fixed over time, have an important influence on the evolution of prices over time. Potentially important features were identified using the websites and whitepapers of cryptocurrencies with the largest userbases. These were assessed using two datasets to enhance robustness: one with fourteen cryptocurrencies beginning from 9 November 2017, and a subset with nine cryptocurrencies starting 9 September 2016, both ending 6 March 2018. Separately analysing the subset of cryptocurrencies raised the number of data points from 115 to 537, and improved robustness to changes in relationships over time. Excluding USD Tether, the results showed a positive association between different cryptocurrencies that was statistically significant. Robust, strong positive associations were observed for six cryptocurrencies where one was a fork of the other; Bitcoin / Bitcoin Cash was an exception. There was evidence for the existence of a group of cryptocurrencies particularly associated with Cardano, and a separate group correlated with Ethereum. The data was not consistent with a token’s functionality or creation mechanism being the dominant determinants of the evolution of prices over time but did suggest that factors other than speculation contributed to the price. Keywords: Correlation Networks; Interconnectedness; Contagion; Speculation 1 1. Introduction The year 2017 saw the start of a rapid diversification in cryptocurrencies.