Non-Tax Revenue

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Om Cement Products

+91-8048372668 Om Cement Products https://www.indiamart.com/om-cement-products-nagpur/ Established in 2009, Om Cement Products is manufacturing a comprehensive range of Cement Windows Frames, Cement Grills, Cement Poles, Cement Pipes and much more. About Us With ultramodern infrastructural abilities coupled with brilliant technical knowledge, we, “Om Cement Products”, came into existence in the year 2009, at Nagpur, (Maharashtra, India). Our company is a partnership firm, specializing in manufacturing a comprehensive range of Cement Windows, Cement Grills, Cement Poles and Cement Pipes. Moreover, clients appreciate our products for their outstanding features such as smooth finish, sturdy construction, abrasion resistant, user friendliness and many more. Under the astute guidance and visionary direction of our honorable mentor, “Mr. Mangesh Duddalwar (Partner)”, we are moving from strength to strength and have become the reckoned name in the industry. For more information, please visit https://www.indiamart.com/om-cement-products-nagpur/about-us.html CEMENT PIPES O u r P r o d u c t s Concrete Drainage Cement Joint Cement Pipe Pipes RCC Joint Cement Pipe Socket RCC Cement Pipe CEMENT POLES O u r P r o d u c t s Cement Pole Y Shape Cement Poles Fencing Cement Pole Concrete Cement Pole O u r OTHER PRODUCTS: P r o d u c t s RCC Cement Pipe RCC Cement Fencing Pole Cement Grill Concrete Cement Window Grill OTHER PRODUCTS: O u r P r o d u c t s Cement Jali Cement Septic Tank Cement Half Round F a c t s h e e t Year of Establishment : 2009 Nature of Business : Manufacturer Total Number of Employees : Upto 10 People CONTACT US Om Cement Products Contact Person: Mr. -

Maharashtra State Legislative Council Electoral Roll - 2020

Maharashtra State Legislative Council Electoral Roll - 2020 Nagpur Division Graduates' Constituency Qualify Date : 1-11-19 Date of publication of final Voter list prepared till 12-11-2020 voter list : 30-12-19 DISTRICT-:Nagpur PART NO -:131 Sr. Name Of Relative Qualific Gend Elector Address Occupation Age EPIC No. No. Elector Name ation er Photo 1 2 3 4 5 6 7 8 9 10 Sonarwahi Kuhi 1 Rahul Badge Iswar Badge 441210 M.A. Service 32 M SPR1506807 Sonarwahi Kuhi 2 Jitendra Badge Iswar Badge 441210 B.A. Service 30 M SPR6287163 Navegaon Sirsi 3 Kalpana Bante Vijay Bante Kuhi 441210 B.A. House Wife 30 F Vrushketu Sadashivrao 4 Wadegaon Kuhi M.A. RTD. 71 M Bhabulkar Bhabulkar 441210 Tarachand 5 Ashwini Bhoyar Gothangaon Kuhi B.A. Educetion 37 F Bhoyar 441210 Sahadeo 6 Upasrao Bhute Mandhal Kuhi B.A. Farmer 45 M Bhute 441210 Purushottam Anandrao 7 Mandhal Kuhi B.A. L.I.C. A. 41 M Chacherkar Chacherkar 441210 Sima Shekhar 8 Mandhal Kuhi B.A. House Wife 30 F Chacherkar Chacherkar 441210 Yashwant M.A.B.e 9 Vijay Chakole Mandhal Kuhi Principal 46 M Chakole 441210 d Suryabhan 10 Mohan Chakole Bori Kuhi 441210 B.A. Teacher 38 M Chakole Yadavrao 11 Sarika Chamat Bothali Kuhi B.A. Teacher 40 F Chamat 441210 Rajhans Vasant 12 Mandhal Kuhi B.A. Farmer 43 M Chaudhari Chaudhari 441210 Mangal 13 Dilip Chavhan Mandhal Kuhi B.A. Teacher 43 M Chavhan 441210 Page No.: 1 of 30 Maharashtra State Legislative Council Electoral Roll - 2020 Nagpur Division Graduates' Constituency Qualify Date : 1-11-19 Date of publication of final Voter list prepared till 12-11-2020 voter list : 30-12-19 DISTRICT-:Nagpur PART NO -:131 Sr. -

Identifying Market for Dry Waste -A Case of Maharashtra

Identifying Market for Dry Waste A Case of Maharashtra Regional Centre for Urban & Environmental Studies All India Insititute of Local Self-Government, Mumbai Supported by Ministry of Housing and Urban Affairs, Government of India MARCH 2018 Identifying Market for Dry Waste A Case of Maharashtra Regional Centre for Urban & Environmental Studies All India Insititute of Local Self-Government, Mumbai Supported by Ministry of Housing and Urban Affairs, Government of India MARCH 2018 Identifying Market Potential for Recyclable Solid Waste in Maharashtra The Regional Centre for Urban and Environmental Studies (RCUES), All India Institute of Local Self-Government (AIILSG), Mumbai The Regional Centre for Urban & Environmental Studies (RCUES) at AIILSG, Mumbai was established by the Ministry of Housing and Urban Affairs (MoHUA), Government of India (GoI) to undertake urban policy research, technical advisory services and strengthening work capabilities of municipal officials and elected members from the States of Goa, Gujarat, Maharashtra, Rajasthan and UT's of Diu, Daman, Dadra & Nagar Haveli and Lakshadweep in the Western Region and States of Assam and Tripura in the North East Region. RCUES, Mumbai is recognized as a National Training Institute (NTI) and is fully supported by the MoHUA, GoI. The Principal Secretary, Urban Development Department of Government of Maharashtra (GoM) is the ex- officio Chairperson of the Advisory Committee of the RCUES, Mumbai, which is constituted by the MoHUA, GoI. AIILSG, Mumbai houses the Solid Waste Management (SWM) Cell backed by the GoM for capacity building of municipal bodies and provide technical advisory services to ULBs in the State. Ministry of Urban Employment and Poverty Alleviation (MoUE&PA), GoI and UNDP have set up the `National Resource Centre on Urban Poverty' (NRCUP), which is anchored by RCUES at AIILSG, Mumbai. -

District Census Handbook, Nagpur

·CENSUS OF INDIA 1961 DISTRICT CENSUS HANDBOOK NAGPUR Compiled by THE MAHARASHTRA CENSUS OFFICE BOMBAY Printed in India by the Manager, Government Press and Book Depot, Nagpur, and Published by the Director, Government Printing and Stationery, Maharashtra State, Bombay-,. 1965 rPrice - Rs. Ei~ht] CENSUS OF INDIA 196 t Central Government Publications Census Report, Volume X-Maharashtra, is published in the folk>wing Parts I-A and B General Report I-C Subsidiary Tables II-A General Popuiation Tables JI-B (i) General Economic Tables-Industrial Classification II-]} (ii) General Economic Tables-Occupational Classification II-C (i) Social and Cultural Tables II-C (ii) Migration Tables III Household Economic Tables IV Report on Housing and Establishments V-A Scheduled Castes and Scheduled Tribes in Maharashtra-Tables V·B ... Scheduled Castes and Scheduled Tribes i.n Maharashtra-Ethnographic Notes VI (1-35) Village Surveys (35 monographs on 35 selected villages) VII·A Handicrafts in Maharashtra VII-B Fairs and Festivals in Maharashtra VIII-A Administration Report-Enumeration (For official use only) VIII·B Administration Report-Tabulation (For official use only) IX Census Atlas of Maharashtra X (1-12) Cities of Maharashtra (15 Volumes-Four volumes on Greater Bombay and One each on other eleven Cities) State Government Publications 25 Volumes of District Census Handbooks in English 25 Volumes of District Census Handbooks in Marathi Alphabetical List of Villages in Maharashtra J-1977-i.3-(Nagpur.} ' . .. : « Drs ~ A r I? I l (r.. 0 D l c .. O c t- % I ~ " 0 III , It! 0 0 l- I- " ' ~ \ c:r . '" .(, ... ~'" ,..~ • A,lIAr q. -

For 1977-78 and 1978-79

GOVEilNMENl' OP MAHAUSHTRA ' . OUTLINE OF ACTIVITIES for 1977-78 and 1978-79 URBAN DEVELOPMENT AND PUIJLIC ' HEALTH DEPARTMENT OUTLINE OF ACTIVITIES 1977•78 AND 1978-79 URBAN DEVELOPMENT AND PUBLIC HEALTH DEPARTMENT CONTENTS (A) URBAN DEVELOPMENT Chapter-1-Town Planning and Valuation Department 1 Cbapter-2-Municipal Administration and Fmaocial Assistance to Municipal 7 Corporations and Municipal Councils. Chapter-3-<:ity and Industrial Development Corporation of Maharashtra 21 Ltd. (ClDCO). Chl!pter-4--Bombay Metropolitan Region Development Authority 36 Chapter-S-Fire Protection and Control 42 Chapler-6-Maharashtra Prevention of Water and Air Pollution Board 44 Chapter-7-Reclamation Schemes in Greater Bombay 49 Cbapter-8-Urban Water Supply and Sanitation 51 (B) PUBUC HEALTH Chapter-1-Directorate of Health Services 59. Chapter-2-DiJ"e9torate of Medical Education and Research 106 Chapter-3--Employees• State Jnsnrance Scheme 110 Chaptcr-4--Ayurvedic Department 113 Chapter-5-Haffkine Biopharmaceutical Corporation Ltd. IIi Chapter-6-Food and Drus Administration 119 Chapter-7-Family Welfare Pro!'ranune i!! Mahar!lshlll! ~tat~ t;!~ (A) URBAN DEVELOPMENT CHAPTER-I TOWN PLANNING AND VALUATION DEPARTMENT . 1.1. Organisation and Strength The Town Planning and Valuation Department endeavours to plan the growth of the fast growing towns in Maharashtra and acts as principal adviser to Government in matters of land valu ation and estate management. The Director of Town Planning · is the Head of Department, which has its Head Office at Pun!! and has branch Offices located at all the district headquarters in the State. The Department has been offering the services of its experien ced officers to other agencies also. -

Notice for Appointment of Regular / Rural Retail Outlet Dealership HPC Proposes to Appoint Retail Outlet Dealers in Maharashtra, As Per Following Details

Notice for appointment of Regular / Rural Retail Outlet Dealership HPC proposes to appoint Retail Outlet Dealers in Maharashtra, as per following details: Estimate Fixed Security Finance to be d Category Type of Minimum Dimensions (in M) / Mode of Fee / Deposit ( Sl No Name Of Location Revenue District Type of RO arranged by the monthly Site * Area of the site (in Sq. M.).* selection Minimu Rs in Applicant Sales m Bid Lakhs) 1 2 3 4 5 6 7 8 9(a) 9(b) 10 11 12 SC Estimat SC CC 1 Estimate ed SC PH d fund working ST required capital ST CC 1 for require ST PH develop Draw of (Regular/Rural MS+HSD CC / DC Fronta ment OBC Depth Area ment of Lots/Biddi ) in Kls /CFS ge for OBC CC 1 infrastru ng operati OBC PH cture at on of OPEN RO (Rs RO (Rs OPEN CC 1 in Lakhs in OPEN CC 2 ) Lakhs) OPEN PH FROM JAFRABAD PHATA IN CHIKHLI CITY TOWARDS JAFRABAD UP TO 5 DRAW OF 1 BULDHANA Regular 150 SC CFS 40 50 2000 0 0 0 3 KM ON SH-228 LOTS WITHIN 3 KM FROM SHELU BAZAR JUNCTION, LHS ON SHELUBAZAR DRAW OF 2 WASHIM Regular 152 SC CFS 40 50 2000 0 0 0 3 KARANJA ROAD TOWARDS KARANJA LOTS WITHIN 4 KM OF KHEMANAND ENGLISH SCHOOL TOWARDS BHOOM DRAW OF 3 AHMEDNAGAR Regular 150 ST CFS 40 50 2000 0 0 0 3 ON AHMEDNAGAR BHOOM ROAD SH-157 LOTS UPTO 4 KM FROM KRISHI UTPANNA BAZAR SAMITI GATE, LONI KHURD DRAW OF 4 AHMEDNAGAR Regular 150 ST CFS 40 50 2000 0 0 0 3 TOWARDS SINNAR ON SH 31 LOTS 5 VILLAGE KADRABAD, ON KADRABAD-KACHNER ROAD AURANGABAD Regular 150 SC CFS 40 50 2000 0 0 DRAW OF 0 3 DRAW OF 6 VILLAGE BHATKUDGAON ON SH- 44 ON NEWASA–SHEVGAON ROAD AHMEDNAGAR Regular -

Rashtrasant Tukadoji Maharaj Nagpur

RASHTRASANT TUKADOJI MAHARAJ NAGPUR UNIVERSITY,NAGPUR PRELIMINARY ELECTORAL ROLL FOR THE ELECTION OF SIX HEADS OF DEPARTMENTS OF AFFILIATED & CONDUCTED COLLEGES TO THE BOARD OF STUDIES-2015 UNDER SECTION 37(2)(b) OF MAHARASHTRA UNIVERSITIES ACT, 1994. Name of Faculty : ( 1) ARTS DATE:10/07/2015 Page : 1 Board of Studies: ( 101) ENGLISH ------------------------------------------------------------------------- ------------------------------------------------------------ Sr. Subject Name of Head of the Department Teaching Exp. Town College Name & Address of the College No. code Year Month code code ------------------------------------------------------------------------- ------------------------------------------------------------ 1 101 ABDUL SHAMIM LATIF 02 - 06 4 192 RENUKA MAHAVIDYALAYA MANEWADA RING ROAD City: NAGPUR,District: NAGPUR 2 101 AGLAWE SHASHANK JANARDAN 18 - 10 259 834 SHRI. KRISHNARAO ZOTING PATIL ARTS & COMMERCE COLLEGE City: SAMUDRAPUR,,District: WARDHA 3 101 AGRAWAL RAMESHCHANDRA FULCHAND 15 - 10 204 714 RAJIV GANDHI ARTS, COMMERCE & SCIENCE COLLEGE City: SADAK-ARJUNI,,District: GONDIA 4 101 AGRAWAL VIBHA BALRAMPRASAD 07 - 10 206 716 C.J. PATEL ARTS & COMMERCE COLLEGE City: TIRORA,,District: GONDIA 5 101 ALI FARZANA SHAKIR 21 - 01 4 168 DR. PANJABRAO DESHMUKH COLLEGE OF COMMERCE (EVENING) COTTON MARKET, City: NAGPUR,District: NAGPUR 6 101 ALONE SUNIL DATTATRAYA 02 - 01 28 344 SHRI. LIMDEO PATIL ARTS & COMMERCE COLLEGE City: MANDHAL,District: NAGPUR 7 101 AMBADE DHIRAJ BHAGWANJI 08 - 06 1 8 ANNASAHEB GUNDEWAR COLLEGE OF ARTS & COMMERCE KATOL ROAD, City: NAGPUR,District: NAGPUR 8 101 AMBADKAR MANGLA VISHVASRAO 15 - 05 20 329 NAGAR PARISHAD SHIVAJI MAHAVIDYALAYA City: MOWAD,District: NAGPUR 9 101 BHAGDIKAR VANDANA VIJAY 17 - 03 4 176 MAHILA MAHAVIDYALAYA NANDANWAN, NEAR GANESHNAGAR, City: NAGPUR,District: NAGPUR 10 101 BHAIRAM RAJKUMAR BHAIYALAL 17 - 03 202 712 JAGAT KALA VANIJYA & INDIRABEN H. -

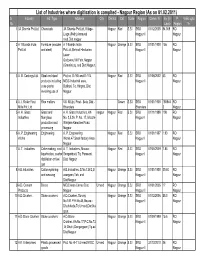

List of Industries Where Digitisation Is Complted - Nagpur Region (As on 01.02.2011) Sr

List of Industries where digitisation is complted - Nagpur Region (As on 01.02.2011) Sr. Industry Ind. Type Address City District Cat. Scale Region Comm. Yr. Inv.(In P. Valid upto No. Lacs) Region Yr. 1 3A Chemie Pvt.Ltd. Chemicals 3A Chemie Pvt.Ltd.,Village- Nagpur Red S.S.I SRO 01/12/2005 84.069 RO Linga (Peth),Amravati Nagpur II Nagpur road,Dist.nagpur 2 A 1 Boards India Furniture (wooden A 1 Boards India Nagpur Orange S.S.I SRO 01/01/1900 156 RO Pvt.Ltd and steel) Pvt.Ltd.,Behind Hindustan Nagpur II Nagpur Lever Godowns,Vill.Fetri,Nagpur (Gramin),tq. and Dist.Nagpur. 3 A. B. Castings Ltd. Steel and steel Plot no. B-165 and B-174, Nagpur Red S.S.I SRO 01/06/2002 53 RO products including MIDC Industrial area, Nagpur II Nagpur coke plants Butibori, Tq. Hingna, Dist. involving use of Nagpur 4 A. I. Roller Flout Rice mullors Vill- MUjbi, Post - Bela, Dist - Green S.S.I SRO 01/01/1900 188944 RO Mills Pvt. Ltd Bhandara Bhandara 3 Nagpur 5 A. K. Glass Glass and A. K. Glass Industries, Kh nagpur Nagpur Red S.S.I SRO 01/11/1998 108 RO Industries fiberglass No. 3,5,26, P. No. 17, Mouza- Nagpur I Nagpur production and Wanjara Kamptee Road, processing Nagpur 6 A. P. Engineering Engineering A. P. Engineering Nagpur Red S.S.I SRO 01/01/1997 1.93 RO Works Works,47,Small factory Area Nagpur I Nagpur Nagpur 7 A. T. Industries Coke making, coal A. -

Nagpur Division Teachers Constituency Election 2017 Teachers Part No

Nagpur Division Teachers Constituency Election 2017 Teachers Part No. 1 to 43 (Area Details) Sr. Part No.of Name of Polling Station. Location o Polling Station Polling area P.S. No All Voters of Village Bharsingi, Jalalkheda, Lohari-Sawanga, Ramthi, zilla parishad primary 1 Bharsingi 1 Thaturwada, Tinkheda, Rohana, Mendhala, Mayawadi, Bhishnur, Thadipauni, School building bharshingi Datewadi, Wadvihara of Previous Part No 1/219 Loksatta Rotary primary All Voters of Village Mowad, Khairgaon, Thugaondeo, Belona, Madna, 2 Mowad School Nagar parishad 2 Dindargaon, Bopapur, Deoli, of Previous Part No 2/219 Mowad Tahsil Office building All Voters of Narkhed taluka in Previous part No 3/219 except voters shown at 3 Narkhed 3 Narkhed P.S. No 1 Bharsingi and P.S. No 2 Mowad bhimrao bapu Deshmukh 4 Kalod 4 All Voters of Saoner Taluka included in Previous Part No 4/219 Adarsha vidyalaya Kelod Tahsil Office building All Voters of Ramtek Taluka in Previous Part No. 10/219 and 11/219 except 5 Ramtek 5 Ramtek Voters attached to P.S. No. 6 Pawani Voters o fPrevious Part No 11/219 of Village Deolapar, Bothia Palora, Karwai, zilla parishad primary 6 Pauni 6 Bandra,Pawani, Dahoda, Hiwara Bazar, Pathrai, Moudi except Voters attacher School pawani to P.S. No 5 Ramtek Tahsil Office building All Voters of Parsioni in Previous part No 8/219 and 9/219 except voters 7 Parshivni 7 parseoni shown at P.S. No 17 Kanhan Muncipal council building 8 Khapa 8 All Voters of Saoner Taluka included in Previous Part No 5/219 Khapa Nagar parishad Subhash 9 Saoner 9 All Voters of Saoner Taluka in Previous Part NO 6/219 primary School Saoner Muncipal council Office 10 Mohpa 10 All Voters of Kalmeshwar Taluka in Previous Part No12/219 building Mohpa Tahsil Office building 11 Katol 11 All Voters of Katol Taluka in Previous Part No 14/219 Koatol zilla parishad primary All Voters of Village Kondhali Jamgad, Kachari-Sawanga, Dhula, Masod in 12 Kondhali School building No. -

Gazetteer of India Maharashtra State Nagpur

GAZETTEER OF INDIA MAHARASHTRA STATE NAGPUR DISTRICT SUPPLEMENTARY Contents NAGPUR DISTRICT GAZETTEER SUPPLEMENTARY Contents Price-Rs. 3·80 Obtainable from the Government Book Depots at Bombay, Nagpur, Pune and Aurangabad or through any recognized Book-seller. Contents MAHARASHTRA STATE GAZETTEERS GOVERNMENT OF MAHARASHTRA NAGPUR DISTRICT SUPPLEMENTARY BOMBAY GAZETTEERS DEPARTMENT, GOVERNMENT OF MAHARASHTRA Contents GAZETTEER OF INDIA MAHARASHTRA STATE GAZETTEERS NAGPUR DISTRICT SUPPLEMENTARY FIRSTEDITION PUBLISHED BY THE EXECUTIVE EDITOR AND SECRETARY, GAZETTEERS DEPARTMENT, GOVERNMENT OF MAHARASHTRA, BOMBAY AND PRINTED IN INDIA BY THE MANAGER, GOVERNMENT CENTRAL PRESS, BOMBAY. Contents Contents PREFACE .............................................................................................................................................................. 9 CHAPTER 1 : Genral— ..................................................................................................................................... 10 ADMINISTRATIVE SUB-DIVISIONS OF NAGPUR DISTRICT, 1971 .................................................. 10 AVERAGE RAINFALL AND RAINY DAYS IN NAGPUR DISTRICT SINCE 1956-57 ...................... 10 SPECIAL WEATHER PHENOMENA IN NAGPUR DISTRICT ............................................................. 11 MONTHWISE SPECIAL WEATHER PHENOMENA IN NAGPUR DISTRICT IN 1974 ................... 11 MEAN WIND SPEED IN KILOMETERS PER HOUR IN NAGPUR DISTRICT .................................. 12 CHAPTER 2 : History— ................................................................................................................................... -

Village Map Taluka: Umred

Nagpur (Urban) Kamptee Village Map Taluka: Umred Surgaon District: Nagpur Khapri Raja Pachgaon !( Kuhi Salaimendha Undari Hingna Chimanazari Dawalimet Majri Wadadh Sukli Mangli Khapri (Ku) Champa Kalandri Khairi Pendhari µ Matkazari Kolarmet 3 1.5 0 3 6 9 Kachhimet Bhiwapur Haladgaon Uti Nirwa Barvha Salai Sonpuri km Umra Tikhadi Pusagondi Wadegaon Mhasepathar (r) Pipla Dudha Aptur Nagpur (Rural) Masalkund Bramhi (ri) Fukeshwar Virli Ukadwadi Akola Kumbhapur (ri) Bendoli Thara Location Index Marajghat (r1) Wagholi (ri) Saiki Paradgaon Bramhni Khairi (Ka) Gaosut Welsakra Rajulwadi Khapri Davha District Index Bothali Thombra Sukli (ri) Udasa Nandurbar Heoti Kotgaon Dahegaon Bhandara Dhule Amravati Nagpur Gondiya Jalgaon Sindi Vihari Amboli Piti Chuwha Ghoturli Akola Wardha Kinhala (de) Jamgad Hatkawada (ri)Khapri (ri) Buldana Jamhalapani Bopeshwar (ri) Nashik Washim Chandrapur Maramzari (ri) Wayagaon (rt) Pavni Yavatmal Garamsur (ri) Ganpawli (ri) Piraya Wanoda Makardhokada Pimpalkhut (ri) Palghar Aurangabad Umred (Rural) Deni Jalna Gadchiroli Katara Gangapur Hingoli Thane Umri (ri) Ahmednagar Parbhani Ridhora Bareja (ri) Mumbai Suburban Nanded Khairi Bk Tambekhani (ri) Seo Mumbai Bid Kanwha Chargaon Pune Shirpur Raigarh Bidar Umred (M Cl) Tirkhura Latur MurzadiTambekhani (m) Narsala (ri) Bhapsi Borgaon (kari) Surajpur (ri) !( Osmanabad Surabardi UMRED Amgaon Karandla Solapur Dhamangaon (ri) Satara Bhivgad Kalamana Boribhatari (ri) Khedi (r1) Ratnagiri Pipardol Wagholi Sangli Dewli Belgaon Nawegaon (S) Salairani Parsodi Maharashtra State Pandhartal Wadandra Muradpur Lohara Salaimahalgaon Panjrepar Kolhapur Mendhepathar Thana Sindhudurg Panjrepar (ri) Kumbhari Khursapar Dharwad Nishanghat Junoni Godhani Kawadapur Telkawadsi Mohpa Dhurkheda Fattepur Taluka Index Kohla Mhasala Ramtek Bela Borgaon Metmangrud (ri) Rakhi Bidmohna (ri) Narkhed Savner Parseoni Dighori Bori Majara Menkhat (ri) Sawangi (bk) Chikhaldhokda Pendkapur Amghat Pethmahmadpur (ri) Kalameshwar Gowari Forest Katol Nagpur (Rural) Mauda Jaitapur Salai Kh. -

NAGPUR (RURAL) 1.Xlsx

Allotment Incentive Waiver OTSBalance OTSProvisional Disbursed FullName GramPanchayat BankName BranchName Category Amount Amount Payable Waiver Amount Amount Umesh Bharat Patle ALAGONDI Bhandara DCCB LAKHANI Waiver 0.00 18500.00 0.00 0.00 0.00 Samita Umesh Patale ALAGONDI Waiver 0.00 0.00 0.00 0.00 0.00 Sarita Ravbaji Sonwane ALAGONDI State Bank of India GIRAD Waiver 0.00 40634.41 0.00 0.00 40634.41 Ravaba Tanbaji Sonvane ALAGONDI Waiver 0.00 0.00 0.00 0.00 0.00 Uttam Pandurangji Makhare ALAGONDI Gondiya DCCB ARJUNI MORGAON Incentive 15000.00 0.00 0.00 0.00 15000.00 Manisha Uttam Makhare ALAGONDI Incentive 0.00 0.00 0.00 0.00 0.00 Rajendra Sadashiv Awdhut ALAGONDI Allahbad Bank Waiver 0.00 150000.00 0.00 0.00 107115.00 Rekha Rajendra Avadhut ALAGONDI Waiver 0.00 0.00 0.00 0.00 0.00 Rambhau Ramchndra Nagpure ALAGONDI Nagpur DCCB BELA OTS 0.00 0.00 4053.00 150000.00 0.00 Anusaya Rambhau Nagpure ALAGONDI OTS 0.00 0.00 0.00 0.00 0.00 Pradip Narayan Mungale ALAGONDI Allahbad Bank BORI Incentive 15000.00 0.00 0.00 0.00 15000.00 Mala Pradip Mungale ALAGONDI Incentive 0.00 0.00 0.00 0.00 0.00 Kalpana Bhimrao Lokhande ALAGONDI Allahbad Bank BORI OTS 0.00 0.00 105307.00 150000.00 150000.00 Dadarav Daulat Kukude ALAGONDI NA 0.00 0.00 0.00 0.00 0.00 Vimalbai Dadarao Kukudde ALAGONDI NA 0.00 0.00 0.00 0.00 0.00 Dilip Haridas Godaghate ALAGONDI Bank of India Waiver 0.00 64523.00 0.00 0.00 64523.00 Sandip Gajanan Shambharkar ALAGONDI Bank of India BUTIBORI Waiver 0.00 120160.00 0.00 0.00 120160.00 Santosh Nilkanth Aglawe ALAGONDI Nagpur DCCB BELA OTS