Mintel Reports Brochure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retail Brochure

1,052 SF, 1,213 SF, 2,646 SF & 4,637 SF FLAGSHIP RETAIL OPPORTUNITIES Opportunity 333 North Michigan Avenue is a timeless and historic piece of prized real estate centrally located on the prime corner of Michigan and Wacker Drive between the Magnificent Mile and Millennium Park. This intersection is an incomparable junction that provides retailers the rare opportunity to serve as the link between luxurious retailers, tourism destinations and the hub of Chicago’s working population. Artist’s Conceptual Rendering Michigan Avenue N DEWITT PL N FAIRBANKS CT N COLUMBUS DR MIES VAN DER ROHE WAY Northwestern Memorial Spa Di La Fronza The Art Institute Hospital Salon of Chicago N STETSON AVE Millenium John Blaze American Craft Stetsons Modern Wildberry Pizza Gyu-Katu 7-Eleven Volare Hyatt Kitchen & Bar Steak & Sushi Pancakes Park Westin Hancock Riverwalk N ST CLAIR ST Cafe & Bar Regency The Tilt Observation Adidas Tavern at the Park The Signature Room Build-A-Bear La Briola The Midway Water Soprafi na Benihana Banana Republic Stan’s Donuts Hotel Club Tower Coach Potbelly Starbucks Ugg Intercontinental Free People GNC Louis Vuitton Chase Bank Place Salvatore Ferragamo Henri Bendel Pandora Chicago Swiss Fine Timing Cop Copine Hanig’s Footwear Forever 21 Apple Lids Coach Michael Store Bvlgari The North Face Tumi Jordan’s Citibank Giordano’s Garrett Popcorn Park Grill Anne Fontaine Pumping The Disney Store Ermenegildo Timberland Steakhouse Tribune Blackhawks Store Stan’s Donuts American Zegna Chase Bank Allen Edmonds Omega Watch Cheesecake Factory Girl Station Neiman Eno Wine Starbucks E WACKER DR TCBY Walgreen’s Marcus Nike Town Burberry Sephora Men’s Wearhouse Starbucks Bar Tower Fannie May Starbucks N MICHIGAN AVE Sweetwater Lens Crafters Nando’s Gucci Verizon Wireless PNC Bank Tavern & Grille CVS Pharmacy Nutella Cafe Mont Blanc H&M Ralph Lauren Saks Zara Starbucks Roastery Grand Lux Cafe MCM MAC Bank of America Purple Pig Walgreen’s Bottega Veneta Fifth Nordstrom Rack Rolex AT&T Store Breitling J. -

2013 Airport Food Review: Denver Tops List for First Time in Decade; Atlanta Remains Grounded for Third Year

2013 Airport Food Review: Denver Tops List for First Time in Decade; Atlanta Remains Grounded for Third Year A Report by the Physicians Committee for Responsible Medicine November 2013 The Physicians Committee’s 13th annual Airport Food Review finds 76 percent of restaurants at 18 of the busiest U.S. airports offer at least one healthful plant-based entrée. The results are consistent with the 2012 report, which finds 76 percent of airport eateries serve at least one high-fiber, cholesterol-free entrée as an option to more than 100 million U.S. travelers who fly during November and December each year. In 2001, the average score in the Airport Food Review was 57 percent. The good news is travelers won’t have to look far this year to find healthful options. Dietitians with the Physicians Committee look for airport restaurants that offer an array of immunity-boosting vegetables, fruits, whole grains, and legumes. Denver International Airport tops the report for the first time since 2003, with 85 percent of its airport eateries offering at least one healthful option, including Colorado Sunshine Wraps at Itza Wrap! Itza Bowl! and barley burgers at Boulder Beer Tap House. Ronald Reagan Washington National Airport makes the biggest gain this year, ascending from 11th to third place, offering healthful bites, including a wide variety of leafy green salads, at more than 80 percent of its restaurants. Hartsfield-Jackson Atlanta International Airport—the world’s busiest airport—remains in last place for the third year in a row, with healthful entrées available at just 50 percent of its restaurants. -

Trendscape Report, Highlighting What Campbell’S Global Team of Chefs and Bakers See As the Most Dynamic Food Trends to Watch

Insights for Innovation and Inspiration from Thomas W. Griffiths, CMC Vice President, Campbell’s Culinary & Baking Institute (CCBI) Last year we published our first-ever Culinary TrendScape report, highlighting what Campbell’s global team of chefs and bakers see as the most dynamic food trends to watch. The response has been exceptional. The conversations that have taken place over the past year amongst our food industry friends and colleagues have been extremely rewarding. It has also been quite a thrill to see this trend-monitoring program take on a life of its own here at Campbell. Staying on the pulse of evolving tastes is inspiring our culinary team’s day-to- day work, driving us to lead innovation across company-wide business platforms. Most importantly, it is helping us translate trends into mealtime solutions that are meaningful for life’s real PICS moments. It’s livening up our lunch break conversations, too! TO OT H These themes are This 2015 Culinary TrendScape report offers a look at the year’s ten most exciting North 15 the driving force 0 American trends we’ve identified, from Filipino Flavors to Chile Peppers. Once again, 2 behind this year’s top trends we’ve developed a report that reflects our unique point of view, drawing on the expertise of our team, engaging culinary influencers and learning from trusted Authenticity industry partners. Changing Marketplace Just like last year, we took a look at overarching themes—hot topics—that are shaping Conscious Connections the ever-changing culinary landscape. The continued cultural transformation of retail Distinctive Flavors markets and restaurants catering to changing consumer tastes is clearly evident Elevated Simplicity throughout this year’s report. -

Building UCC Vegan and Halal Options

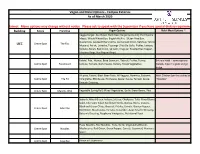

Vegan and Halal Options - Campus Eateries As of March 2020 Disclaimer: Menu options may change without notice. Please ask to speak with the Supervisor if you have special dietary requirements. Building Eatery Franchise Vegan Options Halal Meat Options * Veggie Burger, Southwest Black Bean Burger (excluding the Chipotle Mayo), Whole Wheat Bun, English Muffin, Gluten Free Bun, Guacamole, Sauteed Mushrooms, Carmelized Onion, Ketchup, Yellow Centre Spot The Fixx UCC Mustard, Relish, Sriracha, Toppings ( Pico De Gallo, Pickles, Lettuce, Tomato, Relish, Red Onion, Spinach, Arugular, Roasted Red Pepper, Jalapeno Rings, Hot Pepper Rings) Falafel, Pita, Humus, Baba Ganoush , Tabouli, Pickles, Turnip, Entirely Halal + some options Centre Spot Paramount Lettuce, Tomato, Garlic Sauce, Parsley, Mixed Vegetables (Salads, dips) in a grab and go fridge All pitas, Falafel, Black Bean Patty, All Veggies, Hummus, Balsamic Halal Chicken (can be cooked at Centre Spot Pita Pit Vinaigrette, BBQ Sauce, Hot Sauce, Specail Sauce, Teriyaki Sauce, "Noodles" Fatoush Dressing, Centre Spot Manchu Wok Vegetable Spring Roll, Mixed Vegetables, Garlic Green Beans, Rice Spinach, Mixed Green, Iceberg Lettuce, Chickpeas, Tofu, Mixed Beans Salad, Edamame Salad, Sunflower Seeds, Quinoa, Beets, Craisins, Black and Green Olives, Broccoli, Pickles, Carrots, Greeen Pepper, Centre Spot Salad Bar Red Onion, Mushrooms, Tomato, Cucumber, Asian Sesame Dressing, Balsamic Dressing, Raspberry Vinaigrette, Nutritional Yeast Pasta Noodles, Rice Noodles, Tofu, Garlic, Vegetables (Brocoli, -

P-Card Transparency Report

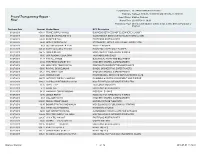

Company Name SC SPARTANBURG SCH DIS 7 Post Date Between 2019-03-28 00:00:00 and 2019-04-27 00:00:00 P-card Transparency Report - Report Owner Blanton, Shannon Final Report Time 2019-07-01 11:39:43 Transaction Type One of: Cash advance or Misc Credit or Misc Debit or Purchase or Payment Purchase Date Amount Vendor Name MCC Description 03/26/2019 451.81 TRANE SUPPLY-115422 BUSINESS SERVICES NOT ELSEWHERE CLASSIFI 03/26/2019 26.00 SLED BACKGROUND CHE GOVERNMENT SERVICES NOT ELSEWHERE CLASSI 03/26/2019 63.25 ZAXBY'S #15801 FAST FOOD RESTAURANTS 03/26/2019 14.43 OFFICE DEPOT #2361 STATIONARY, OFFICE AND SCHOOL SUPPLY STO 03/26/2019 9.63 DOLLAR GENERAL # 11702 VARIETY STORES 03/27/2019 149.38 RAY'S VACUUM & SEWING HOUSEHOLD APPLIANCE STORES 03/27/2019 265.15 LOWES #02548 HOME SUPPLY WAREHOUSE STORES 03/27/2019 10.00 UBR PENDING.UBER.COM TAXICABS/LIMOUSINES 03/27/2019 14.17 8160 ALL PHASE ELECTRICAL PARTS AND EQUIPMENT 03/27/2019 23.52 THE FRESH MARKET 014 GROCERY STORES, SUPERMARKETS 03/27/2019 8.00 NEW YORK TIMES DIGITAL CONTINUITY/SUBSCRIPTION MERCHANTS 03/27/2019 50.00 PAYPAL BRUCEUNLIMI BANDS, ORCHESTRAS, ENTERTAINERS 03/27/2019 67.21 WAL-MART #1281 GROCERY STORES, SUPERMARKETS 03/27/2019 44.00 WEEBLR.COM PROFESSIONAL SERVICES NOT ELSEWHERE CLAS 03/27/2019 199.75 GATEWAY SUPPLY COMPANY PLUMBING & HEATING EQUIPMENT AND SUPPLIE 03/27/2019 138.61 AG PRO SPARTANBURG 010132 MISCELLANEOUS AUTOMOTIVE DEALERS 03/27/2019 35.15 UBER TRIP TAXICABS/LIMOUSINES 03/27/2019 5.17 ARGO TEA FAST FOOD RESTAURANTS 03/27/2019 34.33 WALMART.COM 8009666546 DISCOUNT -

Your Guide to Services and Amenities

Your Guide to Services and Amenities Feinberg Pavilion/Galter Pavilion Security Services Lower concourse, Feinberg Food and Drink 251 E. Huron St./201 E. Huron St. Surgery Waiting Area Fifth and seventh Au Bon Pain Bakery Second floor floors, Feinberg Cosi First floor Retail and Public Services How Do You Roll? Second floor ATM Second floors, Feinberg and Galter LYFE Kitchen First floor Barbara’s Bookstore First floor, Galter Prentice Women’s Hospital 250 E. Superior St. Stan’s Donuts First floor Farmer’s Fridge Second floor, Feinberg Pulse Gift Shop Second floor, Galter Retail and Public Services Patient, Family and Visitor Services U.S. Bank (Coming Summer 2015) Ashland Addison Florist Co. First floor ATM Second floor Second floor, Feinberg ATM Second floor Bridges to Feinberg Pavilion and Parking Garages Walgreens Pharmacy Second floor, Feinberg Zen & Now Gifts First floor Second floor Language Assistance (see Patient Representatives) Food and Drink Food and Drink Mothers’ Room Second floor Au Bon Pain Bakery Second floor, Feinberg Argo Tea First floor Au Bon Pain Bakery First floor, Galter Dunkin Donuts Second floor Other Food and Drink on GRK Greek Kitchen Second floor, Feinberg Farmer’s Fridge First floor the Northwestern Campus Protein Bar Second floor, Feinberg Fresh Market at Fairbanks Second floor 1 Corner Bakery Arkes Family Pavilion, Saigon Sisters Second floor, Galter 676 N. Saint Clair St., First floor Patient, Family and Visitor Services Starbucks First floor, Feinberg The Mathews Chapel Third floor 2 Jazzman’s Café Rehabilitation Institute of Chicago, 345 E. Superior St., Lobby Patient, Family and Visitor Services Financial Counseling Basement Bridges to Parking Garage Second floors, Language Assistance (see Patient Representatives) 3 M Burger Arkes Family Pavilion, Feinberg and Galter Lost and Found (see SecurityDEL Services)AWARE PLACE 161 E. -

Argo Tea Greenhouse at Connors Park Retail Case Study

Argo Tea REF RESHING CONNORS PARK The Argo Tea greenhouse in Connors Park on the Near North Side of Chicago is a little architectural gem in a city of architectural wonder. What makes the tea-osk so clever is that it serves its setting while being an edifice of Argo Tea’s core values. Founded in 2003 by Arsen Avakian (CEO), Simon Simonian and Daniel Lindwasser, Argo Tea does more than serve drinks, it provides people with a one-cup- at-a-time experience. “Sustainability and quality are two of our core platforms, and that reaches beyond our menu to the use of sustainable design elements, landscaping, energy sources and service items.” DANA DIMITRI D IRECTOR OF MARKETING ARGO TEA www.wilsonart.com retail project: Argo Tea Greenhouse at Connors Park location: Chicago, Illinois partners: Argo Tea Chicago Park District lead designer: Mark Cuellar, Argo Tea fabricator: Part of that experience is the story of tea. community. We raise awareness of the health Creative Surfaces, Sioux Falls, S.D. Though it is second only to water in popularity benefits of tea and the cultural benefits of wilsonart products: worldwide, tea still has room to grow in the partnering with responsible suppliers. We Studio Teak High Pressure Laminate United States, where according to The Tea provide a space for people to come and work, Capers Solid Surface Association of the U.S.A, the infusion of leaves or study, or meet with friends in an environment and herbs was a $10.41 billion domestic where they can experience tea and relax.” market in 2013. -

230 West Monroe

w monroe 3,400 SF 2ND GEN RESTAURANT + 687 SF OUTDOOR PATIO AND 3,367 SF RETAIL SPACE FOR LEASE Dunkin Swada Matcha Kinzie Chase Einstein Public Donuts Trump Gilt Bar Chophouse HiVibe PNC Bank Mercadito The Smith Bank RPM Steak Bagels Southern Cut House International Kinzie Hotel & Tower K Station Highline CVS Untitled Blue Barrio Siena Tavern Harry STK Museum of Apartments Mercury Caray’s Brodcast Moe’s Cantina Steakhouse Merchandise Mart Old Crow Tortoise Club Smokehouse Protein Bar Apparel Center Ann Sacks Rohl Subway Katana Cafe The Devon & Devon Waterworks Freshii IV Me Porcelanosa Bentwood 7Eleven Umbria Langham Vicostone Keeler The Westin Hotel Artistic Tile Subzero Woll Kamehachi Chicago Holiday Inn K&B Galleries The Shade Store Nonina Chicago Spin The Chopping Block House of Blues Yolk The Pizzeria Portofino RPM 320 Chicago Cut River Roast Kitchen Dicks Last Smith & On The Water River Bar Resort Wollensky Salesforce Tower (under construction) Wolf Woint West Wacker Prime & Cafe Baci Sidebar Grille Chase McCormick & Catch 35 Provisions Bank Schmick’s Duru’s Custom Corner Shirts & Suits AceBounce Morton’s Steakhouse Bakery Ping Pong Renaissance Associated Starbucks New Line Wow Market Gibsons Goodwin’s Bank Tavern Creations Protein Bar Italia Restaurant Ajida Bao theWit LakeLake Dunkin' Taste 222 Chipotle Potbelly Chic-Fil-A Elephant & Donuts Starbucks Walgreens The Clayton Castle Porter Kitchen & Deck Blackwood BBQ Ronny’s Goodman AT&T Small Chicago Popeyes Cheval Pearl Peet’s Original Theater Coee Theatre Tavern T-Mobile Petterino’s -

Foodinspectionbasic Based on Food Inspections

FoodInspectionBasic Based on Food Inspections DBA Name IPSENTO FLAT GRILL 7- ELEVEN CHICAGO BY NIGHT THE NEW GRACE RESTAURANT FURIOUS SPOON EN PASSANT Beaubien Elementary School UNCOMMON GROUND THE DRAKE HOTEL LIME LEAF Kozminski THIRD RAIL TAVERN MAX'S TAKE OUT SAIGON PHO GOGI NARA SUBWAY Subway ROYALTY ARYA BHAVAN Page 1 of 478 09/27/2021 FoodInspectionBasic Based on Food Inspections AKA Name Risk IPSENTO Risk 2 (Medium) FLAT GRILL Risk 1 (High) 7- ELEVEN Risk 2 (Medium) CHICAGO BY NIGHT Risk 1 (High) THE NEW GRACE RESTAURANT Risk 1 (High) FURIOUS SPOON Risk 1 (High) EN PASSANT Risk 1 (High) Beaubien Elementary School Risk 1 (High) UNCOMMON GROUND Risk 1 (High) THE DRAKE HOTEL Risk 1 (High) LIME LEAF Risk 1 (High) Kozminski Risk 1 (High) THIRD RAIL TAVERN Risk 1 (High) MAX'S TAKE OUT Risk 1 (High) SAIGON PHO Risk 1 (High) GOGI NARA Risk 1 (High) SUBWAY Risk 1 (High) Subway Risk 1 (High) ROYALTY Risk 1 (High) ARYA BHAVAN Risk 1 (High) Page 2 of 478 09/27/2021 FoodInspectionBasic Based on Food Inspections ROSATI'S GRANT PARK MIMI'S TACOS THE ORIGINA GINO'S EAST CHICAGO BUTTERDOUGH KIMBALL MINI MART PRET A MANAGER FLASH FOOD MART SUMMER COQ D OR M & M FOOD DAYGLOW SUBWAY SUBWAY #44541 TRATTORIA ULTIMO MISS SAIGON GRAZE TACO MAYA BIAN BLACK DOG GELATO DUNKIN DONUTS NANDO'S PERI-PERI BROTHER'S SUBMARINE INC Page 3 of 478 09/27/2021 FoodInspectionBasic Based on Food Inspections ROSATI'S Risk 1 (High) MIMI'S TACOS Risk 1 (High) GINO'S EAST Risk 1 (High) BUTTERDOUGH Risk 1 (High) KIMBALL MINI MART Risk 3 (Low) PRET A MANGER Risk 1 (High) FLASH -

Roland Osae-Oppong Internet Marketing

ROLAND OSAE-OPPONG INTERNET MARKETING Teavana was founded in 1997 by former Applebee's manager Andrew Mack and his wife Nancy, after the couple took a trip abroad and observed American tourists' affinity for fine wine and coffee. The specialty retailer sells more than 100 varieties of premium loose-leaf teas, as well as tea pots and other tea-related merchandise. Its mission is to introduce consumers to the global tea lifestyle, which includes the aromas, textures, tastes, and healthful qualities of loose-leaf teas. Teavana Teavana is a specialty tea and tea accessory retailer based in Atlanta, Georgia. Teavana dream began with an idea that people would enjoy fresh, high-quality tea in a place that was part Tea Bar, part Tea Emporium. They introduce people to the aromas, textures, and beneficial qualities of loose leaf teas while enlightening them with the history and variety of teas available. The company went public last July, and today operates 284 company-owned stores in the U.S. and Canada, as well as 18 franchised stores in Mexico. On December 31, 2012, Starbucks acquired Teavana for about $620-million Starbucks licenses its trademark through other channels such as licensed retail stores and, through certain of its licensees and equity investees, Starbucks produces and sells a variety of ready-to-drink beverages Teavana's commitment is for people to enjoy fresh, high-quality tea in a place that was part Tea Bar, part Tea Emporium. STRENGTHS WEAKNESSES Teavana teas area Making their tea always fresh samples misleadingly -

Environmental Health Food Safety Activities Generated 12/14/2017

Environmental Health Food Safety Activities Generated 12/14/2017 VIOLATION TYPES Priority (P): The highest risk violations which are directly related to an increased risk of foodborne illness. Examples include improper handwashing, unsafe food temperatures. Priority foundation (Pf): Violations that can create a high risk (Priority) violation. Examples include lack of soap at a handsink, no calibrated thermometer, no test strips to check sanitizer levels. Core (C): Lower risk violations. Examples include general maintenance of facility (floors, walls, ceilings). Correction Requirements: (P) and (Pf) violations must be corrected immediately when possible. Follow-up inspections occur to ensure all of these violations have been resolved if not corrected during the routine inspection. Open Core (C) violations are verified at the next routine inspection. For a complete description of the violations cited at each licensed establishment click HERE. ROUTINE INSPECTIONS COMPLETED LAST WEEK Unannounced inspections that occur on a set frequency, typically every six months. Activity Date Facility Name Site Address City P Pf C 12/07/2017 BAMBOO EXPRESS 6101 LAKE MICHIGAN DR ALLENDALE 4 7 12 STE B500 12/08/2017 GREAT LAKES ELEMENTARY 3200 152ND AVE HOLLAND 0 0 0 12/08/2017 GRAND HAVEN HIGH SCHOOL 17001 FERRIS ST GRAND HAVEN 0 0 0 12/08/2017 ARBY'S RESTAURANT GROUP DBA 12308 JAMES ST HOLLAND 0 0 0 ARBY'S #5489 12/08/2017 SIRI THAI KITCHEN 301 N RIVER AVE HOLLAND 1 0 2 12/08/2017 COURTYARD BY MARRIOTT 121 E 8TH ST HOLLAND 2 1 2 12/08/2017 SUBWAY 10402 -

Buffalo-Canisius-Selecting a Meal Plan 8-5-15 LG

HOW TO SELECT A MEAL PLAN BUFFALO STATE STUDENTS AT CANISIUS COLLEGE STEP 1: CHOOSING THE RIGHT MEAL PLAN! • Identify how much time you will be spending on Buffalo State’s campus and choose a meal plan which fits with your personal eating habits. EXAMPLE: o I will be attending class 3 days per week. My class schedule is 9am – 6pm on Monday, Wednesday and Friday. With 16 weeks in the Fall 2014 semester, I will be on campus 48 days. I personally like to sit down and have a meal once per day, while I am usually on the go and prefer quick service meals once or twice a day. o The meal plan which fits my lifestyle best is: Flex Plus 50. This meal plan has 50 block meals to use at my discretion over the course of the semester as well as $1,000 in Dining Dollars for me to utilize at the on campus restaurants like Subway, Spot Coffee and Salsarita’s. MEAL PLAN OPTIONS FOR RESIDENT STUDENTS LIVING AT CANISIUS COLLEGE (FOR A DESCRIPTION OF HOW FUNDS WORK PLEASE SEE BACK OF SHEET) MEAL PLANS WITH MEALS SWIPES PLAN NAME NO. OF MEALS DINING DOLLARS BENGAL BUCKS PLAN COST BLOCK 30 30 meals per semester $500 $0 $890 per semester FLEX PLUS 50 50 meals per semester $1000 $75 $1705 per semester BLOCK 75 75 meals per semester $800 $75 $1775 per semester BLOCK 50 50 meals per semester $150 $0 $580 per semester BONUS PACK 20 20 meals per semester $150 $0 $335 per semester MINI PACK 10 10 meals per semester $150 $0 $245 per semester BONUS PACK 20+ 20 meals per semester $100 $100 $380 per semester MINI PACK 10+ 10 meals per semester $100 $100 $300 per semester DECLINING BALANCE MEAL PLANS PLAN NAME DINING DOLLARS BONUS DOLLARS TOTAL DOLLARS PLAN COST MINI DINING DOLLAR $250 $15 $265 $250 MEGA DINING DOLLAR $500 $25 $525 $500 SUPER DINING DOLLAR $1000 $35 $1035 $1000 STEP 2: CHOOSE THE AMOUNT TO TRANSFER TO CANISIUS COLLEGE • Identify how much of the Dining Dollars on your Buffalo State meal plan you would like to have allocated to utilize on your Canisius College ID card.