August 2017 Investor Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Would You Like to Write ''The Formation of Perhydrophenalenes and Polyalkyladamantanes by Lsomerization of Tricyclic Perhydroaromatics ?''

would you like to write ''The Formation of Perhydrophenalenes and Polyalkyladamantanes by lsomerization of Tricyclic Perhydroaromatics ?'' How's that again? Well, never mind Athabasca oil sands project in North ings in Exploration, Production, -Bob Warren, Ed Janoski, and Abe ern Alberta to multiply the world's Manufacturing, Research, Engineer Schneider already wrote it. They're petroleum resources; plan a new $125 ing, Sales, Accounting, Economics, chemists in Sun Oil Company's Re million processing facility in Puerto and Computer Operation. Locations search and Development Department. Rico; expand the Toledo Refinery to - Philadelphia, Toledo and Dallas Their paper is just one of many re the tune of $50 million; sponsor the areas. sulting from imaginative and origi "Sunoco Special" and the racing team You may write us for an appoint nal basic research conducted at Sun of Roger Penske and Mark Donohue ment, write for our book "Sunoco Oil. in big league sports car racing to Career Opportunities Guide," or con Maybe basic research and technical competition-prove and improve Sun tact your College Placement Director papers aren't your cup of tea. But oco products for the public; pursue a to see Sun's representative when on isn't the kind of company that in continuing program for air and water campus. SUN OIL COMPANY, Indus vests in and encourages such projects pollution control; beautify Sunoco trial Relations Dept. CED, 1608 Wal the kind of company you'd like to service stations everywhere. nut Street, Philadelphia, Pa.19103 or work for? Sunoco is geared for growth. We P . O. Box 2880, Dallas, Texas 75221. -

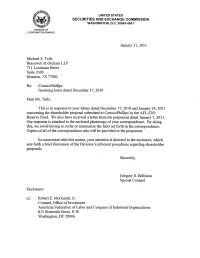

Conocophillips: Rule 14A-8 No-Action Letter

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549-4561 Januar 31, 2011 Michael S. Telle Bracewell & Giuliani LLP 711 Louisiana Street Suite 2300 Houston, TX 77002 Re: ConocoPhillps . Incoming letter dated December 17, 2010 Dear Mr. Telle: Ths is in response to your letters dated December 17, 2010 and Janua 24,2011 concernng the shareholder proposal submitted to ConocoPhillps by the AFL-CIO Reserve Fund. We also have received a lttter from the proponent dated Januar 7, 201l. our response is attached to the enclosed photocopy of your correspondence. By doing this, we avoid having to recite or sumarze the facts set forth in the correspondence. Copies of all of the correspondence also will be provided to the proponent. In connection with this matter, your attention is directed to the enclosure, which sets forth a brief discussion ofthe Division's informal procedures regarding shareholder proposals. Sincerely, Gregory S. Bellston Special Counsel Enclosures cc: Robert E. McGarrah, Jr. Counsel, Office of Investment American Federation of Labor and Congress of Industrial Organizations 815 Sixteenth Street, N.W. Washington, DC 20006 Januar 31, 2011 Response of the Office of Chief Counsel Division of Corporation Finance Re: ConocoPhilips Incoming letter dated December 17, 2010 The proposal requests that the board prepare a report on the steps the company has taen to reduce the risk of accidents. The proposal fuher specifies that the report should describe the board's oversight of process safety management, staffing levels, inspection and maintenance of refineries and other equipment. Weare unable to concur in your view that ConocoPhilips may exclude the proposal under rule 14a-8(i)(10). -

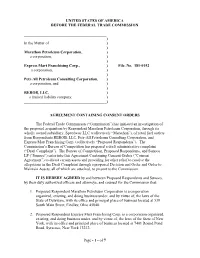

Marathon Agreement

UNITED STATES OF AMERICA BEFORE THE FEDERAL TRADE COMMISSION __________________________________________ ) In the Matter of ) ) Marathon Petroleum Corporation, ) a corporation, ) ) Express Mart Franchising Corp., ) File. No. 181-0152 a corporation, ) ) Petr-All Petroleum Consulting Corporation, ) a corporation, and ) ) REROB, LLC, ) a limited liability company. ) __________________________________________) AGREEMENT CONTAINING CONSENT ORDERS The Federal Trade Commission (“Commission”) has initiated an investigation of the proposed acquisition by Respondent Marathon Petroleum Corporation, through its wholly owned subsidiary, Speedway LLC (collectively “Marathon”), of retail fuel outlets from Respondents REROB, LLC, Petr-All Petroleum Consulting Corporation, and Express Mart Franchising Corp. (collectively “Proposed Respondents”). The Commission’s Bureau of Competition has prepared a draft administrative complaint (“Draft Complaint”). The Bureau of Competition, Proposed Respondents, and Sunoco LP (“Sunoco”) enter into this Agreement Containing Consent Orders (“Consent Agreement”) to divest certain assets and providing for other relief to resolve the allegations in the Draft Complaint through a proposed Decision and Order and Order to Maintain Assets, all of which are attached, to present to the Commission. IT IS HEREBY AGREED by and between Proposed Respondents and Sunoco, by their duly authorized officers and attorneys, and counsel for the Commission that: 1. Proposed Respondent Marathon Petroleum Corporation is a corporation organized, existing, and doing business under, and by virtue of, the laws of the State of Delaware, with its office and principal place of business located at 539 South Main Street, Findlay, Ohio 45840. 2. Proposed Respondent Express Mart Franchising Corp. is a corporation organized, existing, and doing business under, and by virtue of, the laws of the State of New York, with its office and principal place of business located at 7401 Round Pond Road, Syracuse, New York 13212. -

Sunoco Pipeline L.P

Sunoco Pipeline L.P. 1300 Main St. Houston, TX 77002 Phone: (713) 989-7000 Website: www.energytransfer.com Energy Transfer Partners, a Texas-based energy company founded in 1995 as EMERGENCY CONTACT: a small intrastate natural gas pipeline 1-800-786-7440 or 877-839-7473 company, is now one of the largest and most diversified master limited PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: partnerships in the United States. Butane 1011 115 Light Cycle Oil 1993 128 Strategically positioned in all of the major Ethane 1035 115 Propane 1075 115 U.S. production basins, the company Fuel Oil 1993 128 Diesel owns and operates a geographically Fuel, Aviation, (Ultra Low Sulfur) 1993 128 diverse portfolio of energy assets, Turbine Engine Kerosene (Ultra Low Sulfur) 1223 128 including midstream, intrastate and (Jet Fuel or Jet A) 1863 128 interstate transportation and storage Gasoline 1203 128 assets. Energy Transfer operates more than 90,000 miles of natural DELAWARE & PHILADELPHIA COUNTIES ONLY: gas, crude oil, natural gas liquids and PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: refined products pipelines and related Crude Oil 1267 128 Naphtha, Petroleum facilities, including terminalling, storage, Alkylate (Light Alkylate (Gasoline Components) 1255 128 fractionation, blending and various Naphtha and Benzene) 1203 128 Raffinate acquisition and marketing assets in 38 Butane (N-Butane) 1075 115 (Naphtha, solvent) 1256 128 states. Butane-Butylene 1075 115 Reformate Cat. Gasoline 1203 128 (Naphtha petroleum) 1255 128 • Intrastate Transportation and Storage Isobutane 1075 115 Udex Feed Operations – approximately 7,900 (Benzene-rich Reformate) 1255 128 miles of natural gas pipelines and three storage facilities. -

ETP & SXL Project Summary

ENERGY TRANSFER EQUITY & ENERGY TRANSFER PARTNERS DISCLAIMER This presentation relates to a presentation the management of Energy Transfer Equity, L.P. (ETE) and Energy Transfer Partners, L.P. (ETP) will give to investors on September 7, 2016. At this meeting, members of the Partnerships’ management may make statements about future events, outlook and expectations related to Energy Transfer Partners, L.P. (ETP), Sunoco Logistics Partners L.P. (SXL), Panhandle Eastern Pipe Line Company, LP (PEPL), Sunoco LP (SUN), and ETE (collectively, the Partnerships), and their subsidiaries and this presentation may contain statements about future events, outlook and expectations related to the Partnerships and their subsidiaries all of which statements are forward-looking statements. Any statement made by a member of management of the Partnerships at this meeting and any statement in this presentation that is not a historical fact will be deemed to be a forward-looking statement. These forward-looking statements rely on a number of assumptions concerning future events that members of management of the Partnerships believe to be reasonable, but these statements are subject to a number of risks, uncertainties and other factors, many of which are outside the control of the Partnerships. While the Partnerships believe that the assumptions concerning these future events are reasonable, we caution that there are inherent risks and uncertainties in predicting these future events that could cause the actual results, performance or achievements of the Partnerships and their subsidiaries to be materially different. These risks and uncertainties are discussed in more detail in the filings made by the Partnerships with the Securities and Exchange Commission, copies of which are available to the public. -

PES Holdings, LLC Enters Into Restructuring Support Agreement to Create Sustainable Financial Foundation

1735 Market Street Philadelphia, PA 19103 | 215 339 1200 www.pes-companies.com PES Holdings, LLC Enters Into Restructuring Support Agreement to Create Sustainable Financial Foundation Agreement Provides $260 Million in New Financing From Term B Lenders and Owners PES Expects to Complete Recapitalization Through Prepackaged Court Process While Continuing Operations Without Interruption Employee Pay and Benefits to Continue as Usual and Vendors to be Paid in Ordinary Course of Business Before and During Court Process Philadelphia, PA. (January 22, 2018) – PES Holdings, LLC (“PES Holdings” or the “Company”), a subsidiary of Philadelphia Energy Solutions LLC (“PES LLC”), announced today that it has entered into a Restructuring Support Agreement (“RSA” or the “Agreement”) with the holders of 100% of the Company’s outstanding Term A debt and more than 90% of the Company’s outstanding Term B debt. In addition to restructuring existing debt and receiving relief from current debt service obligations, the Company has secured access to $260 million in new financing comprising $120 million in debtor-in-possession and exit financing, $75 million in additional capital from Sunoco Logistics Partners Operations L.P. (“Sunoco Logistics”) and a $65 million equity investment from existing equity holders, led by The Carlyle Group along with management and other partners. The recapitalized Company will have a stronger financial foundation to support operations amid continuing pressure on refining margins and soaring costs for merchant refiners associated with the purchase of Renewable Identification Numbers (“RINs”) to satisfy requirements under the Renewable Fuel Standard (“RFS”) established by the Environmental Protection Agency (“EPA”). The Agreement provides that the recapitalization will be completed pursuant to a proposed prepackaged restructuring (the “Restructuring”) through the filing of a Chapter 11 Plan of Reorganization (the “Plan”) for PES Holdings and affiliated subsidiaries. -

Seven & I Holdings to Purchase Sunoco's Assets for $3.3Bn

Find our latest analyses and trade ideas on bsic.it 7-Eleven Owner Upgrades: Seven & i Holdings to Purchase Sunoco’s Assets for $3.3bn Seven & i Holdings Co Ltd. (TYO: 3382) – market cap as of 07/04/2017: ¥4.11tn ($37.0bn) Sunoco LP (NYSE: SUN) – market cap as of 07/04/2017: $3.38bn Introduction On April 6, 2017, the worldwide Japanese retail-store operator Seven & i Holdings Co. announced that it would acquire more than 1,000 gas stations and convenience stores owned by Sunoco LP in the U.S. for $3.3bn. The owner of the famous 7-Eleven chain’s acquisition of Sunoco was carried out in the light of the large potential which the company identifies in the U.S. market. About Seven & i Holdings Seven & i Holdings is a Japanese holding company founded in 2005 and headquartered in Tokyo. The company operates in the convenience stores, supermarket, and restaurant industries with 60,000 outlets spread out in 17 countries. With the acquisition of Sunoco, the company is now expanding its most famous brand, Seven- Eleven, throughout Japan and the US. The holding’s operating profit mainly derives from Convenience Store (86.3%), Superstore (2.1%), Department Store (1.1%), Food Services (0.3%) and Financial Services (14.1%), whereas the company’s Mail and Other Services and Corporate divisions contributed negatively to the overall EBIT by 2.4% and 3.0% respectively. The operating profitability of the company is clearly skewed towards the Convenience Store segment and this is further stressed by the breakdown of the projected capital investment plan (as of the FY2016 Annual Report): 7-Eleven Japan and - more importantly for the transaction analysed - 7-Eleven Inc. -

Who Is Sunoco Logistics and Sunoco Pipeline?

ABOUT SUNOCO LOGISTICS AND THE MARINER EAST PROJECT Q: Who is Sunoco Logistics and Sunoco Pipeline? A: Sunoco Logistics Partners L.P. (SXL) is a publicly traded partnership that owns pipelines, terminals and other assets used in the purchase, transfer and sale of: • crude oil; • refined products such as gasoline, diesel and jet fuel; • natural gas liquids, such as propane, ethane and butane. Sunoco Logistics has approximately 8,000 miles of pipelines throughout the United States. Sunoco Pipeline L.P. is a wholly owned subsidiary of Sunoco Logistics Partners L.P. with more than seven decades’ experience. Q: What is Mariner East? A: Mariner East is a pipeline infrastructure project in Pennsylvania, Delaware, Ohio and West Virginia to transport Marcellus/Utica shale natural gas liquids (NGLs) such as propane, ethane and butane, to the Marcus Hook Industrial Complex in Southeastern Pennsylvania and other access points for distribution to destinations in Pennsylvania and other domestic and international markets. The project has two phases: • Mariner East 1 is an underground pipeline project to transport 70,000 barrels a day of liquid propane and ethane from the Marcellus Shale region in Western Pennsylvania approximately 300 miles east to the Marcus Hook Industrial Complex in Marcus Hook, Pa. and Claymont, Del., where the products will be processed, stored, and sold to the local, regional, and international markets. Mariner East 1 utilizes mostly existing 8-inch diameter steel pipeline, except for 51 miles of new 12-inch diameter steel pipe between Washington County and Westmoreland County. • Mariner East 2 is a planned, approximately $2.5 billion new underground pipeline system, consisting of up to two pipelines approximately 350 miles in length, with origins in Ohio, West Virginia and Pennsylvania. -

Enbridge's Energy Infrastructure Assets

Enbridge’s Energy Infrastructure Assets Last Updated: Aug. 4, 2021 Energy Infrastructure Assets Table of Contents Crude Oil and Liquids Pipelines .................................................................................................... 3 Natural Gas Transmission Pipelines ........................................................................................... 64 Natural Gas Gathering Pipelines ................................................................................................ 86 Gas Processing Plants ................................................................................................................ 91 Natural Gas Distribution .............................................................................................................. 93 Crude Oil Tank Terminals ........................................................................................................... 96 Natural Gas Liquids Pipelines ................................................................................................... 110 NGL Fractionation ..................................................................................................................... 111 Natural Gas Storage ................................................................................................................. 112 NGL Storage ............................................................................................................................. 119 LNG Storage ............................................................................................................................ -

Sunoco Pipeline L.P

Sunoco Pipeline L.P. ORDER ON PETITION FOR DECLARATORY ORDER 137 FERC ~ 61,107 (2011} In this case, Sunoco Pipeline L.P. (Sunoco) filed a petition for a declaratory order seeking a decision by the Commission approving, among other things, a rate and priority of service structure for its Mariner West pipeline project that would move ethane from the Marcellus Shale formation production area to various markets. After a widely-publicized open season for all potential shippers, those shippers who executed transportation service agreements in which they committed to ship or pay a minimum amount of ethane (5,000 barrels per day) for a term extending through June 30, 2020, and who paid a premium that was at least $0.01 more than the rate charged uncommitted shippers, would not have their volumes subject to prorationing under normal operating conditions. Sunoco reserved 90 percent of capacity on the expansion for committed shippers and the balance, 10 percent for uncommitted shippers. The Commission granted the petition for declaratory order. ~V..&...&...I...&.V-:1: ..JV V V · · ~.&.'\.\,.,. ~ £-J· · \ V.&..&.V.L.L..&.'- ..&. U...&. } ..&...&.J V~j ~V..&...&. 137 FERC ~ 61,107 UNITED STATES OF AMERICA FEDERAL ENERGY REGULATORY COMMISSION Before Commissioners: Jon Wellinghoff, Chairman; Philip D. Moeller, John R. Norris, and Cheryl A. LaFleur. Sunoco Pipeline L.P. Docket No. OR11-22-000 ORDER ON PETITION FOR DECLARATORY ORDER (Issued November 4, 2011) 1. On September 2, 2011, Sunoco Pipeline L.P. (Sunoco) filed a petition for a declaratory order approving: (1) priority service for Sunoco's proposed Mariner West ethane pipeline (Project); and (2) the overall tariff and rate structure for the Project. -

Sunoco Pipeline L.P

Sunoco Pipeline L.P. 1300 Main St. Houston, TX 77002 Phone: (713) 989-7000 Website: www.energytransfer.com Energy Transfer Partners, a Texas-based Sunoco Pipeline operates a energy company founded in 1995 as a geographically diverse portfolio of energy EMERGENCY CONTACT: small intrastate natural gas pipeline assets including, pipelines, terminalling For crude oil: 1-800-753-5531 company, is now one of the largest and marketing assets. Crude oil, For refined products + LPG:1-800-786-7440 and most diversified master limited refined products and natural gas liquids PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: partnerships in the United States. are transported through a 12,000-mile Butane/Propane 1075 115 Strategically positioned in all of the major pipeline system that traverses 21 states. Crude Oil 1297 128 U.S. production basins, the company For more information about local Gasoline/ owns and operates a geographically operations of Sunoco Pipeline, please Refined Products 1203 128 diverse portfolio of energy assets, contact us at: including midstream, intrastate and TEXAS Angelina, Bell, Brazoria, Brazos, interstate transportation and storage COUNTIES OF OPERATION: Brown, Chambers, Cherokee, Coke, assets. Energy Transfer operates more Coleman, Coryell, Falls, Glasscock, than 90,000 miles of natural gas, crude oil, Anderson Grimes Nacogdoches Gregg, Grimes, Hamilton, Hardin, Andrews Hall Navarro natural gas liquids and refined products Harris, Harrison, Houston, Jasper, Angelina Hamilton Nolan pipelines and related facilities, including Jefferson, Lampasas, Leon, Liberty, Bell Hardin Orange terminalling, storage, fractionation, McLennan, Milam, Mills, Montgomery, Borden Harris Panola blending and various acquisition and Nacogdoches, Orange, Panola, Polk, Bosque Harrison Polk marketing assets in 38 states. -

Storm Report-Irma-PM-FL GA.XLS

Brand Name Site Name Street Address City State Zip Phone# EXXONMOB BOB'S FUEL 16091 NW US HWY 441 ALACHUA FL 32615 (386) 462-5590 BP BP 8997157 15980 NW HWY 441 ALACHUA FL 326150000 (386) 462-0539 CHVRNWF CHEVRON 0042065 15000 NW US HWY 441 ALACHUA FL 326155666 (000) 000-0000 SHELL CIRCLE K STORE 27239 16070 NW US HIGHWAY ALACHUA FL 326154890 (000) 000-0000 EXXONMOB CK 2721202 14411 N.W. US HIGHWA ALACHUA FL 32615 (386) 462-2880 RACEWAY RACEWAY 6953 16171 NW US HWY 441 ALACHUA FL 32616 (770) 431-7600 SUNOCO SUNOCO SRVC STATION11921 NW US HWY ALACHUA FL 326530000 (386) 462-1301 RACETRAC RACETRAC 629 484 SOUTH & SR434 ALTAMONTE SP FL 32714 (407) 862-2242 SHELL CIRCLE K STORES INC 91 W STATE ROUTE 436 ALTAMONTE SPG FL 327144206 (407) 788-8186 SUNOCO SUNOCO SRVC STATION1395 E. ALTAMONT ALTAMONTE SPG FL 329010000 (407) 834-1018 WAWA WAWA 5179 919 WEST SR 436 ALTAMONTE SPRING FL 327142931 (610) 358-8000 7-ELEVEN 7-ELEVEN 10060 401 WEST HWY 436 ALTAMONTE SPRINGS FL 32714 (407) 862-5671 7-ELEVEN 7-ELEVEN 23348 340 DOUGLAS AVE ALTAMONTE SPRINGS FL 32714 (407) 788-1947 7-ELEVEN 7-ELEVEN 30059 898 SR 434 NORTH ALTAMONTE SPRINGS FL 32714 (407) 869-1291 EXXONMOB 7-ELEVEN 34767 901 W HWY #436 ALTAMONTE SPRINGS FL 327142901 (407) 682-5912 EXXONMOB 7-ELEVEN 34780 501 E ALTAMONTE DR ALTAMONTE SPRINGS FL 327014702 (407) 331-4366 BP BP 9493347 109 E ALTAMONTE DR ALTAMONTE SPRINGS FL 327014310 (407) 260-0144 UNBRANDED CASSELBERRY 66 FOOD1681 S RONALD REAGANALTAMONTE SPRINGS FL 32701 (407) 831-5844 CHVRNWF CHEVRON 0301815 201 W.