In Re: Foundry Networks, Inc. Securities Litigation 00-CV-4823

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brocade Communications Systems Inc

BROCADE COMMUNICATIONS SYSTEMS INC FORM 10-K (Annual Report) Filed 12/16/13 for the Period Ending 10/26/13 Address 130 HOLGER WAY SAN JOSE, CA 95134-1376 Telephone (408) 333-8000 CIK 0001009626 Symbol BRCD SIC Code 3577 - Computer Peripheral Equipment, Not Elsewhere Classified Industry Computer Storage Devices Sector Technology Fiscal Year 10/25 http://www.edgar-online.com © Copyright 2013, EDGAR Online, Inc. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use. Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended October 26, 2013 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number: 000-25601 Brocade Communications Systems, Inc. (Exact name of registrant as specified in its charter) Delaware 77-0409517 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 130 Holger Way, San Jose, CA 95134-1376 (Address of registrant’s principal executive offices) (Zip code) Registrant’s telephone number, including area code: (408) 333-8000 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common stock, $0.001 par value The NASDAQ Stock Market LLC Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Dell Software & Peripherals Manufacturer's List

Dell Software & Peripherals Manufacturer’s List 01 Communique Adept Computer Solutions Amd 16p Invoice Test Adesso Amdek Corp. 1873 Adi Systems, Inc. American Computer Optics 2 Adi Tech American Ink Jet 20th Century Fox Adic American Institute For Financial Re 2xstream.Com Adler / Royal American Map Corporation 3com Adobe Academic American Megatrends 3com Academic Adobe Commercial Fonts American Power Conversion 3com Oem Adobe Government Licensing American Press,Inc 3com Palm Program American Small Business Computers 3dfx Adobe Systems American Tombow 3dlabs Ads Technologies Ami2000 Corporation 3m Ads Technologies Academic Ampad Corporation 47th Street Photo Adtran Amplivox 7th Level, Inc. Advanced Applications Amrep 8607 Advanced Digital Systems Ams 8x8, Inc Advanced Recognition Technologies Anacomp Ab Dick Advansys Anchor Pad International, Inc. Abacus Software, Inc. Advantage Memory Andover Advanced Technologies Abl Electronics Corporation Advantus Corp. - Grip-A-Strip Andrea Electronics Corporation Abler Usa, Inc Aec Software Andrew Corporation Ablesoft, Inc. Aegis Systems Angel Lake Multimedia Inc Absolute Battery Company Aesp Anle Paper - Sealed Air Corporation Absolute Software, Inc. Agfa Antec Accelgraphics, Inc. Agson Antec Oem Accent Software Ahead Systems, Inc. Anthro Corporation Accent Software Academic Aiptek Inc Aoc International Access Beyond Aironet Aopen Components Access Softek/Results Mkt Aitech Apex Data, Inc. Access Software Aitech Academic Apex Pc Solutions Acclaim Entertainment Aitech International Apexx Technology Inc Acco Aiwa Computer Systems Div Apg Accpac Aladdin Academic Apgcd Accpac International Aladdin Systems Aplio, Inc. Accton Technology Alcatel Internetworking Apollo Accupa Aldus Appian Graphics Ace Office Products Alien Skin Software Llc Apple Computer Acer America Alive.Com Applied Learning Sys/Mastery Point Aci Allaire Apricorn Acme United Corporation Allied Telesyn Apw Zero Cases Inc Acoustic Communications Systems Allied Telesyn Government Aqcess Technologies Inc Acroprint Time Recorder Co. -

Reportlinker Adds World Routers Market Report

Reportlinker Adds World Routers Market Report. NEW YORK New York, state, United States New York, Middle Atlantic state of the United States. It is bordered by Vermont, Massachusetts, Connecticut, and the Atlantic Ocean (E), New Jersey and Pennsylvania (S), Lakes Erie and Ontario and the Canadian province of -- Reportlinker.com announces that a new market research report is available in its catalogue. World Routers Market http://www.reportlinker.com/p0109904/World-Routers-Market.html This report analyzes the worldwide markets for Routers in US$ Millions. The major End use markets analyzed are Service Providers, Enterprises, and Research/Education & Other Markets. The report provides separate comprehensive analytics for North America North America, third largest continent (1990 est. pop. 365,000,000), c.9,400,000 sq mi (24,346,000 sq km), the northern of the two continents of the Western Hemisphere., Europe, Asia-Pacific, and Rest of World. Annual forecasts are provided for each region for the period of 2006 through 2015. A five-year historic analysis is also provided for these markets. The report profiles 189 companies including many key and niche players worldwide such as 2Wire, 3Com Corporation, ADTRAN Inc., Alcatel-Lucent, Allied Telesis Allied Telesis is a telecommunications company, formerly Allied Telesyn. Headquartered in Japan, their North American headquarters are in Bothell, Washington, a suburb of Seattle. Inc., ASUSTeK Computer Inc., Belkin International Inc., Buffalo Technology (USA), Inc., Ciena Corporation Ciena Corporation NASDAQ: CIEN develops and markets communications network platforms and software, and offers professional services. The Company's broadband access, data and optical networking platforms, software tools, and global network services support worldwide telecom, Cisco Systems “Cisco” redirects here. -

Seagate Crystal Reports

PERSONAL PROPERTY MANUFACTURER NAME & CODE Run Date: Friday, January 27, 2012 MANUFACTURE NAME MANUFACTURE CODE 3COM 100010 3M CORPORATION 100020 ACE COMPUTERS 101010 ACER 101020 ADAPTEC 101030 ADC 101040 ADT 101050 AEROHIVE NETWORKS 101060 AIPHONE 101070 ALCATEL 101080 ALLIED TELESIS 101090 AMER NETWORKS 101100 APC (AMERICAN PWR CONVERSION) 101110 APPLE 101120 APP-TECHS 101130 ARUBA NETWORKS 101140 ASANTE 101150 ASTARO 101160 ASUS COMPUTER INTERNATIONAL 101170 AUDIO ENHANCEMENT 101180 AVAYA 101190 AVERMEDIA INFORMATION 101200 AVOCENT 101210 AVROVER 101220 AXIS COMMUNICATIONS 101230 BALT 102010 BANG & OLUFSEN 102020 BARRACUDA 102030 BELKIN 102040 BELTRONICS 102050 BLUECOAT SYSTEMS 102060 BOGEN 102070 BOSCH 102080 BOXLIGHT 102090 BRADFORD NETWORKS 102100 BRETFORD MANUFACTURING 102110 BRITE COMPUTERS 102120 BROCADE COMMUNICATIONS 102130 BROTHER 102140 BYTESPEED COMPUTERS 102150 CABLEXPRESS 103010 CALIFONE INTERNATIONAL 103020 CALYPSO SYSTEMS 103030 CANON 103040 CASIO 103050 CHANNEL VISION TECHNOLOGY 103060 CHECKPOINT 103070 CHIEF MANUFACTURING 103080 CISCO 103090 CITADEL 103100 COMMSCOPE 103110 COMPAQ 103120 Prepared by John Cacciola, SAU Page 1 of 5 PERSONAL PROPERTY MANUFACTURER NAME & CODE Run Date: Friday, January 27, 2012 MANUFACTURE NAME MANUFACTURE CODE COMPELLENT 103130 CONTINENTAL ACCESS 103140 CRESTRON 103150 DAEWOO 104010 DAKTECH 104020 DA-LITE 104030 DELL 104040 DEMCO 104050 D-LINK 104060 DUKANE 104070 EARTHWALK 105010 EATON 105020 EIKI 105030 ELMO MANUFACTURING 105040 E-MACHINES 105050 EMC CORPORATION 105060 EMERSON 105070 ENTERASYS -

Insight Manufacturers, Publishers and Suppliers by Product Category

Manufacturers, Publishers and Suppliers by Product Category 2/15/2021 10/100 Hubs & Switch ASANTE TECHNOLOGIES CHECKPOINT SYSTEMS, INC. DYNEX PRODUCTS HAWKING TECHNOLOGY MILESTONE SYSTEMS A/S ASUS CIENA EATON HEWLETT PACKARD ENTERPRISE 1VISION SOFTWARE ATEN TECHNOLOGY CISCO PRESS EDGECORE HIKVISION DIGITAL TECHNOLOGY CO. LT 3COM ATLAS SOUND CISCO SYSTEMS EDGEWATER NETWORKS INC Hirschmann 4XEM CORP. ATLONA CITRIX EDIMAX HITACHI AB DISTRIBUTING AUDIOCODES, INC. CLEAR CUBE EKTRON HITACHI DATA SYSTEMS ABLENET INC AUDIOVOX CNET TECHNOLOGY EMTEC HOWARD MEDICAL ACCELL AUTOMAP CODE GREEN NETWORKS ENDACE USA HP ACCELLION AUTOMATION INTEGRATED LLC CODI INC ENET COMPONENTS HP INC ACTI CORPORATION AVAGOTECH TECHNOLOGIES COMMAND COMMUNICATIONS ENET SOLUTIONS INC HYPERCOM ADAPTEC AVAYA COMMUNICATION DEVICES INC. ENGENIUS IBM ADC TELECOMMUNICATIONS AVOCENT‐EMERSON COMNET ENTERASYS NETWORKS IMC NETWORKS ADDERTECHNOLOGY AXIOM MEMORY COMPREHENSIVE CABLE EQUINOX SYSTEMS IMS‐DELL ADDON NETWORKS AXIS COMMUNICATIONS COMPU‐CALL, INC ETHERWAN INFOCUS ADDON STORE AZIO CORPORATION COMPUTER EXCHANGE LTD EVGA.COM INGRAM BOOKS ADESSO B & B ELECTRONICS COMPUTERLINKS EXABLAZE INGRAM MICRO ADTRAN B&H PHOTO‐VIDEO COMTROL EXACQ TECHNOLOGIES INC INNOVATIVE ELECTRONIC DESIGNS ADVANTECH AUTOMATION CORP. BASF CONNECTGEAR EXTREME NETWORKS INOGENI ADVANTECH CO LTD BELDEN CONNECTPRO EXTRON INSIGHT AEROHIVE NETWORKS BELKIN COMPONENTS COOLGEAR F5 NETWORKS INSIGNIA ALCATEL BEMATECH CP TECHNOLOGIES FIRESCOPE INTEL ALCATEL LUCENT BENFEI CRADLEPOINT, INC. FORCE10 NETWORKS, INC INTELIX -

Silicon Valley

Silicon Valley 1 What is Silicon Valley ? Silicon Valley is an economic cluster. A network of networks, rich in financial and social capital spanning every area of technology, all focused on developing and commercializing new technologies. SV is therefore the center of technical innovation of the US and of the world. 2 History matters History matters ! 3 Historical framework What is called today the Bay of San Francisco was accidentally discovered in 1769 by the Spanish soldier and explorer Gaspar de Portolà How many inhabitants were there in San Francisco in the year 1846 ? 200 100 Ohlone indians + 100 mexicans San Francisco grew from such small settlement to a boomtown of about 36,000 by 1852. Why ? What had happened ? 4 Historical framework The Berkeley campus of the University of California opened in 1883. Stanford University opened in 1891. 5 6 cornerstones The Silicon Valley system stands on six cornerstones 6 30 “Fortune-500” companies of Silicon Valley • Adobe • Hewlett-Packard • Netflix • AMD • Intel • Nvidia • Agilent • Intuit • Oracle • Apple • Juniper Networks • Salesforce • Applied Materials • KLA Tencor • SanDisk • Brocade • LSI Logic • Sanmina • Cisco • Marvell • Symantec • eBay • Maxim • Western Dig. • Facebook • National Semicond. • Xilinx • Google • NetApp • Yahoo! 7 100 Silicon Valley stars 3Com IBM Quantcast A10 Networks IDEO Quora Actel Informatica Rambus Actuate Corporation Intuitive Surgical Riverbed Technology Adaptec Kerio Technologies ROBLOX Aeria Games LinkedIn RSA Akamai Technologies Logitech Redback Networks Altera LynuxWorks Samsung Amazon Maxtor SAP Amdahl McAfee Siemens Ampex Memorex Silicon Graphics Antibody Solutions Micron Technology Silicon Image Aricent Microsoft Solectron Asus Mozilla Foundation Solstice Atari Move Inc Sony Atmel Nokia SRI International Broadcom Netscape SunPower BEA Systems NeXT Computer Synopsys Inc. -

Fujitsu Computer Products of America, Inc. XG700 and XG2000

TTOLLY H E GROUP No. 207227 July 2007 Fujitsu Computer Test Products of America, Inc. Summary XG700 and XG2000 Switches Functionality Certification and Cooperative Interoperability Evaluation Test Highlights Premise: Network managers who deploy a variety of Fast Ethernet, Giga- Earns five Switch Interoperability certifications for Layer 2 bit Ethernet and 10GbE switching advanced LAN functions devices in their networks need guaran- teed interoperability of these switches in Achieves broad Layer 2 interoperability with 15 switches order to maintain a functional network. from nine vendors Interoperates with other devices tested when supporting 10- ujitsu Computer Products of Gigabit Ethernet LAN PHY interface, 802.1p/Q VLAN tags, F America, Inc. commissioned Jumbo Frame Support, Link Aggregation, and Rapid The Tolly Group to evaluate its Spanning Tree Protocol Fujitsu XG700 and XG2000 LAN switches for interoperability with other brand switches. Fujitsu Switches Tested Partial List of Tolly Switch Tolly Group engineers subjected the Fujitsu XG700 and XG2000 switches to Interoperability Certifications Earned more than a dozen tests with devices from 3Com, Alcatel-Lucent, Cisco Certification Result Systems, Enterasys, Extreme Networks, Foundry Networks, IBM Nortel and Hewlett-Packard Co. 802.1p/Q VLAN Tag Propagation Engineers subjected the Fujitsu XG700 and XG2000 switches to advanced LAN services tests, including support for 10GbE LAN PHY support 802.1p/Q VLAN tag propagation, Rapid Spanning Tree Protocol (RSTP) and Jumbo Frames. The Fujitsu switches Rapid Spanning Tree Protocol (RSTP) achieved interoperability with other devices tested. Tests were conducted in March/April Link Aggregation Control Protocol (LACP) 2007 at Terremark Worldwide Inc.’s world-class NAP of the Americas facil- ity in Miami, a major Internet peering Jumbo Frame Support point for carriers and service providers. -

1-800-870-4340

MNJ Technologies Direct is a full-service technology reseller providing MNJ Technologies Direct, access to cutting edge technology that is cost effective and project-specific. headquartered in Buffalo Grove, Illinois, was founded in 2002. We offer an extensive range of products including desktop computers, We are a technology solutions laptops, printers, servers, storage devices, and software from a wide provider with a reputation for variety of manufacturers. In conjunction with our broad product offering reliable, knowledgeable sales is a strategy tailored to each client. representatives and outstanding logistical capabilities. Our Our sales representatives continue to be extensively trained by many sales representatives have the of the leading IT manufacturers. This in depth training enables experience , the training, the MNJ Technologies Direct to provide customized solutions and support knowledge and the dedication for all of our clients and ongoing technical training keeps our sales to help you with all of your representatives up to date on all of the latest technology offerings. IT–related products and services. MNJ Technologies Direct is focused on servicing the needs of small MNJ Technologies Direct is and medium sized businesses as well as governmental and educational certified by the Women’s institutions. Our dedication, experience and flexibility enables us to meet Business Enterprise National and exceed the demands of our clients in the ever changing field of Council as a Women’s Business information technology. Enterprise (WBE), and is one of the largest Women Owned and Operated Businesses in the State of Illinois. 1-800-870-4340 MNJ Technologies Direct Inc.• 1025 Busch Parkway• Buffalo Grove, IL 60089 www.mnjtech.com MNJ Technologies Direct, Inc. -

Silicon Valley 130

Silicon Valley 130 Board of Directors Compensation Practices October 2007 Compensia THOUGHTFUL PAY 1731 TECHNOLOGY DRIVE SUITE 810 SAN JOSE, CA 95110 408 876 4025 770 TAMALPAIS DRIVE SUITE 207 CORTE MADERA, CA 94925 415 462 2990 compensia.com Silicon Valley 130 Board of Directors Compensation Practices IN SUMMER AND FALL 2007, Compensia analyzed the Director compensation practices of the largest 133 technology companies headquartered in Silicon Valley. This report—which we call the SV130—documents the findings of the analyses. A list of companies examined in the analyses is provided at the end of the document. Methodology All data reported in the charts and graphs represent medians (or the 50th percentile). Analyses are provided on an All Company basis, as well as by company size and in limited cases, by industry. Company size is divided into three categories: 4 Small: Less than $250 million in revenue (n = 37) 4 Medium: Revenue of $250M to $1B (n = 48) 4 Large: Greater than $1B (n = 48) Data were collected in May/June, 2007 from public filings, and represent the most current Board pay prac- tices, based on the most recent fiscal year reported or changes reflected immediately after the fiscal year end in a Form 8-K. Annual utilization (“burn rate”) analyses are based on data as of the last fiscal year. (Burn rate is defined as the number of shares/options allocated to employees divided by common shares outstanding.) In this report, restricted stock/units refers to full value stock awards that vest based solely on continued employment. Equity grant values are based on the following methodology: i) stock options are valued using the Black-Scholes stock option pricing model and ii) restricted stock is valued based on the number of shares multiplied by the grant date stock price. -

HSA: Winning Over the Software Ecosystem

Broadcast of Innovative Spirit from the Industry to Universities in Silicon Valley Dr. Timour Paltashev, Sr. Manager, Graphics IP Engineering РАСПРОСТРАНЕНИЕ ИННОВАЦИОННОГО ДУХА ИЗ ИНДУСТРИИ В УНИВЕРСИТЕТЫ КРЕМНИЕВОЙ ДОЛИНЫ ГДЕ ЭТО И КАК ТУДА ПОПАСТЬ? ЗЕМЛЯ ОБЕТОВАННАЯ ВЫСОКИХ ТЕХНОЛОГИЙ ДО СИХ ПОР МНОГО ЖЕЛАЮЩИХ ??? International Academy of Business, Almaty | October 31 – November 1, 2013 | 2 КТО ТАМ УЖЕ ОБОСНОВАЛСЯ И ЕСТЬ ЛИ ЕЩЕ МЕСТО? . Ученые и инженеры со всего мира определяют лицо Кремниевой долины с населением 3.5-4 млн. человек . Многоуровневая сеть университетов и колледжей для подготовки специалистов всех уровней . Исследовательские лаборатории . Штаб-квартиры ведущих компаний ИТ, электронной и био-индустрии . Инженерные и исследовательские подразделения крупных корпораций . Малые компании-стартапы . Венчурные капиталисты всех мастей и «танцоры вокруг инноваций» . Есть ли там место нормальным людям? . Конечно есть, если эти люди талантливы в науке и технологиях . Привлечение талантов – главное условие выживания как сети университетов, так и всей индустрии «земли обетованной» International Academy of Business, Almaty | October 31 – November 1, 2013 | 3 MAJOR ENGINEERING UNIVERSITY LIST AND GRADING Top level: . University of California, Berkeley . Stanford University . University of California, Davis . University of California, Santa Cruz Second level: . San José State University . San Francisco State University . California State University, East Bay, Hayward . Santa Clara University . Northwestern Polytechnic University . Carnegie Mellon University (Silicon Valley campus) . University of San Francisco (South Bay Campus) International Academy of Business, Almaty | October 31 – November 1, 2013 | 4 THIRD LEVEL UNIVERSITIES AND COMMUNITY COLLEGES Third Level Universities: . University of Phoenix . National Hispanic University . Silicon Valley University Community Colleges: . Cogswell Polytechnical College . De Anza College . Evergreen Valley College . Foothill College . -

Of 79 UNITED STATES DISTRICT COURT EASTERN DISTRICT of TEXAS MARSHALL DIVISION Plaintiff, V. Defendant. Civil Action

Case 2:18-cv-00060 Document 1 Filed 03/08/18 Page 1 of 79 PageID #: 1 UNITED STATES DISTRICT COURT EASTERN DISTRICT OF TEXAS MARSHALL DIVISION DIFF SCALE OPERATION RESEARCH, LLC, Civil Action No._________ Plaintiff, v. JURY TRIAL DEMANDED CISCO SYSTEMS, INC. Defendant. COMPLAINT FOR PATENT INFRINGEMENT DIFF Scale Operation Research, LLC (“Plaintiff”), by its undersigned counsel, bring this action and make the following allegations of patent infringement relating to U.S. Patent Nos.: 7,881,413 (the, “‘413 patent”); 6,664,827 (the, “‘827 patent”); 7,106,758 (the, “‘758 patent”); 6,407,983 (the, “‘983 patent”); 6,847,609 (the, “‘609 patent”); 6,940,810 (the, “‘810 patent”); 6,990,110 (the, “‘110 patent”); 6,721,328 (the, “‘328 patent”); and 6,216,166 (the, “‘166 patent”); and 6,859,430 (the, “‘430 patent”) (collectively, the “patents-in-suit”). Defendant Cisco Systems, Inc. (“Cisco” or “Defendant”) infringes each of the patents-in-suit in violation of the patent laws of the United States of America, 35 U.S.C. § 1 et seq. INTRODUCTION This case arises from Cisco’s infringement of a portfolio of semiconductor and network infrastructure patents. This patent portfolio arose from the groundbreaking work of ADC Telecommunications, Inc. (“ADC Telecommunications”). Page 1 of 79 Case 2:18-cv-00060 Document 1 Filed 03/08/18 Page 2 of 79 PageID #: 2 In 1935, ADC Telecommunications, then known as the Audio Development Company1 was founded in Minneapolis, Minnesota by two Bell Laboratory engineers to create custom transformers and amplifiers for the broadcast radio industry. -

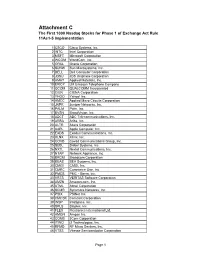

Attachment C the First 1000 Nasdaq Stocks for Phase 1 of Exchange Act Rule 11Ac1-5 Implementation

Attachment C The First 1000 Nasdaq Stocks for Phase 1 of Exchange Act Rule 11Ac1-5 Implementation 1 CSCO Cisco Systems, Inc. 2 INTC Intel Corporation 3 MSFT Microsoft Corporation 4 WCOM WorldCom, Inc. 5 ORCL Oracle Corporation 6 SUNW Sun Microsystems, Inc. 7 DELL Dell Computer Corporation 8 JDSU JDS Uniphase Corporation 9 AMAT Applied Materials, Inc. 10 ERICY LM Ericsson Telephone Company 11 QCOM QUALCOMM Incorporated 12 CIEN CIENA Corporation 13 YHOO Yahoo! Inc. 14 AMCC Applied Micro Circuits Corporation 15 JNPR Juniper Networks, Inc. 16 PALM Palm, Inc. 17 BVSN BroadVision, Inc. 18 ADCT ADC Telecommunications, Inc. 19 ARBA Ariba, Inc. 20 ALTR Altera Corporation 21 AAPL Apple Computer, Inc. 22 EXDS Exodus Communications, Inc. 23 XLNX Xilinx, Inc. 24 COVD Covad Communications Group, Inc. 25 SEBL Siebel Systems, Inc. 26 NXTL Nextel Communications, Inc. 27 NTAP Network Appliance, Inc. 28 BRCM Broadcom Corporation 29 BEAS BEA Systems, Inc. 30 CMGI CMGI, Inc. 31 CMRC Commerce One, Inc. 32 PMCS PMC - Sierra, Inc. 33 VRTS VERITAS Software Corporation 34 AMZN Amazon.com, Inc. 35 ATML Atmel Corporation 36 SCMR Sycamore Networks, Inc. 37 PSIX PSINet Inc. 38 CMCSK Comcast Corporation 39 INSP InfoSpace, Inc. 40 SPLS Staples, Inc. 41 FLEX Flextronics International Ltd. 42 AMGN Amgen Inc. 43 COMS 3Com Corporation 44 ITWO i2 Technologies, Inc. 45 RFMD RF Micro Devices, Inc. 46 VTSS Vitesse Semiconductor Corporation Page 1 47 INKT Inktomi Corporation 48 EXTR Extreme Networks, Inc. 49 SDLI SDL, Inc. 50 MFNX Metromedia Fiber Network, Inc. 51 VRSN VeriSign, Inc. 52 IMNX Immunex Corporation 53 COST Costco Wholesale Corporation 54 KLAC KLA-Tencor Corporation 55 TRLY Terra Networks, S.A.