NYSE Arca Options Fee Schedule

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NYSE National, Inc. Schedule of Fees and Rebates As of July 1, 2021

NYSE National, Inc. Schedule of Fees and Rebates As Of July 1, 2021 Fees and Credits Applicable to Market Participants • All fee disputes concerning fees billed by the Exchange must be submitted to the Exchange in writing and must be accompanied by supporting documentation. All fee disputes must be submitted no later than sixty (60) days after receipt of a billing invoice. I. Transaction Fees A. Definitions 1. “ADV” means average daily volume. 2. “Adding ADV” means an ETP Holder’s average daily volume of shares executed on the Exchange that provided liquidity. 3. “Adding Liquidity” means the execution of an ETP Holder’s order on the Exchange that provided liquidity. 4. “CADV” means consolidated average daily volume. 5. “Removing Liquidity” means the execution of an ETP Holder’s Aggressing Order, as defined under Rule 7.36(a)(5), or other orders that removed liquidity. 6. “Removing ADV” means an ETP Holder’s average daily volume of shares executed on the Exchange that removed liquidity. 7. “US CADV” means the United States consolidated average daily volume of transactions reported to a securities information processor (“SIP”). Transactions that are not reported to a SIP are not included in the US CADV. B. General • Rebates indicated by parentheses ( ). • For purposes of determining transaction fees and credits based on quoting levels, average daily volume (“ADV”), and consolidated ADV (“CADV”), the Exchange may exclude shares traded any day that (1) the Exchange is not open for the entire trading day, (2) is the date of the annual reconstitution of the Russell Investments Indexes, and/or (3) a disruption affects an Exchange system that lasts for more than 60 minutes during regular trading hours. -

NYSE American Options Customer Best Execution (“CUBE”) Mechanism Frequently Asked Questions

NYSE American Options Customer Best Execution (“CUBE”) Mechanism Frequently Asked Questions GENERAL INFORMATION 1. What is CUBE? CUBE is NYSE American Options’ (the “Exchange”) electronic crossing price improvement auction mechanism. CUBE is available for single-leg orders (“Single-Leg CUBE”) and complex orders (“Complex CUBE”) and offers exchange participants (“Participants”) the ability to seek price improvement for paired orders of any size. Additional information can be found in NYSE American Rules 971.1NY for Single-Leg CUBE and Rule 971.2NY for Complex CUBE. 2. What is a CUBE ‘Paired’ order? Paired orders are comprised of an ‘Initiating’ order -- i.e., the CUBE Order -- and a ‘Contra’ order. The orders may be made up of principal or solicited interest and are sent to the Exchange in a single CUBE order message; both the Initiating order and Contra order components are required to constitute a valid CUBE order, which is then evaluated for auction eligibility. Except for AON CUBE, where both Initiating and Contra orders may be canceled in certain circumstances where the AON order contingency is not met (see below), the Contra order guarantees execution of the Initiating order within an allowable execution range. 3. What is AON CUBE? AON CUBE provides All-or-None (“AON”) functionality for CUBE orders with a minimum of 500 contracts for Single-Leg AON CUBE, and with a minimum of 500 contracts on the smallest leg for a Complex AON CUBE. For additional information on AON CUBE, please see the ‘AON CUBE Supplemental Information’ section below. 4. How does the CUBE auction operate? On receipt of a valid CUBE/Contra order pairing, the Exchange broadcasts the auction via a Request for Quote (“RFQ”) message to subscribers of the Exchange’s market data (“XDP”) feeds. -

Membership Application for New York Stock Exchange LLC and NYSE

Membership Application for New York Stock Exchange LLC1 and NYSE American LLC 1 NYSE membership permits the Applicant Firm, upon approval of membership, to participate in the NYSE Bonds platform. TABLE OF CONTENTS Page Application Process and Fees 2-3 Information and Resources 3 Explanation of Terms 4-5 Section 1 – Organizational Profile 6 Section 2 – Applicant Firm Acknowledgement 7 Section 3 – Application Questions 8-9 Section 4 – Floor Based Business 10 Section 5 – Key Personnel 11 Section 6 – Additional Required Documentation and Information 12-14 Section 7 – Designation of Accountant 15 Section 8 – Required Organizational Documents and Language Samples / References 16 NYSE and NYSE American Equities Membership Application - October 2019 1 APPLICATION PROCESS Filing Requirements Prior to submitting the Application for New York Stock Exchange LLC (“NYSE”) and/or NYSE American LLC (“NYSE American”) membership, an Applicant Firm must file a Uniform Application for Broker-Dealer Registration (Form BD) with the Securities and Exchange Commission and register with the FINRA Central Registration Depository (“Web CRD®”). Application Submission Applicant Firm must complete and submit all applicable materials addressed within the application as well as the additional required documentation noted in Section 6 of the application. Application and supplemental materials should be sent electronically to [email protected]. Please ensure all attachments are clearly labeled. NYSE Applicant Firm pays one of the below application fees (one-time fee and non-refundable): Clearing Firm $20,000 (Self-Clearing firm or Clears for other firms) Introducing Firm $ 7,500 (All other firms fall within this category) Non-Public Firm $ 2,500 (On-Floor firms and Proprietary firms) Kindly make check payable to “NYSE Market (DE), Inc.” and submit the check with your initial application. -

Margin Requirements Across Equity-Related Instruments: How Level Is the Playing Field?

Fortune pgs 31-50 1/6/04 8:21 PM Page 31 Margin Requirements Across Equity-Related Instruments: How Level Is the Playing Field? hen interest rates rose sharply in 1994, a number of derivatives- related failures occurred, prominent among them the bankrupt- cy of Orange County, California, which had invested heavily in W 1 structured notes called “inverse floaters.” These events led to vigorous public discussion about the links between derivative securities and finan- cial stability, as well as about the potential role of new regulation. In an effort to clarify the issues, the Federal Reserve Bank of Boston sponsored an educational forum in which the risks and risk management of deriva- tive securities were discussed by a range of interested parties: academics; lawmakers and regulators; experts from nonfinancial corporations, investment and commercial banks, and pension funds; and issuers of securities. The Bank published a summary of the presentations in Minehan and Simons (1995). In the keynote address, Harvard Business School Professor Jay Light noted that there are at least 11 ways that investors can participate in the returns on the Standard and Poor’s 500 composite index (see Box 1). Professor Light pointed out that these alternatives exist because they dif- Peter Fortune fer in a variety of important respects: Some carry higher transaction costs; others might have higher margin requirements; still others might differ in tax treatment or in regulatory restraints. The author is Senior Economist and The purpose of the present study is to assess one dimension of those Advisor to the Director of Research at differences—margin requirements. -

Frequently Asked Questions About the 20% Rule and Non-Registered Securities Offerings

FREQUENTLY ASKED QUESTIONS ABOUT THE 20% RULE AND NON-REGISTERED SECURITIES OFFERINGS issuance, equals or exceeds 20% of the voting power understanding the 20% Rule outstanding before the issuance of such stock; or (2) the number of shares of common stock to be issued is, or will be upon issuance, equal to or in excess What is the 20% rule? of 20% of the number of shares of common stock The “20% rule,” as it is often referred to, is a corporate outstanding before the transaction. “Voting power governance requirement applicable to companies listed outstanding” refers to the aggregate number of on nasdaq, the nYSe or the nYSe American LLC votes that may be cast by holders of those securities (“nYSe American”) (collectively, the “exchanges”). outstanding that entitle the holders thereof to vote each exchange has specific requirements applicable generally on all matters submitted to the issuer’s to listed companies to receive shareholder approval securityholders for a vote. before they can issue 20% or more of their outstanding common stock or voting power in a “private offering.” However, under nYSe Rule 312.03(c), the situations The exchanges also require shareholder approval in in which shareholder approval will not be required connection with certain other transactions. Generally: include: (1) any public offering for cash, or (2) any issuance involving a “bona fide private financing,1” if • Nasdaq Rule 5635(d) requires shareholder approval such private financing involves a sale of: (a) common for transactions, other than “public offerings,” -

In the Matter of New York Stock Exchange LLC, and NYSE Euronext

UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION SECURITIES EXCHANGE ACT OF 1934 Release No. 67857 / September 14, 2012 ADMINISTRATIVE PROCEEDING File No. 3-15023 In the Matter of ORDER INSTITUTING ADMINISTRATIVE AND CEASE-AND-DESIST PROCEEDINGS New York Stock Exchange LLC, and PURSUANT TO SECTIONS 19(h)(1) AND 21C NYSE Euronext, OF THE SECURITIES EXCHANGE ACT OF 1934, MAKING FINDINGS AND IMPOSING Respondents. SANCTIONS AND A CEASE-AND-DESIST ORDER I. The Securities and Exchange Commission (“Commission”) deems it appropriate and in the public interest that public administrative and cease-and-desist proceedings be, and hereby are, instituted pursuant to Sections 19(h)(1) and 21C of the Securities Exchange Act of 1934 (“Exchange Act”) against the New York Stock Exchange LLC (“NYSE”) and NYSE Euronext (collectively, “Respondents”). II. In anticipation of the institution of these proceedings, Respondents have submitted Offers of Settlement (the “Offers”) that the Commission has determined to accept. Solely for the purpose of these proceedings and any other proceedings brought by or on behalf of the Commission, or to which the Commission is a party, and without admitting or denying the findings herein, except as to the Commission’s jurisdiction over them and the subject matter of these proceedings, which are admitted, Respondents consent to the entry of this Order Instituting Administrative and Cease-and-Desist Proceedings Pursuant to Sections 19(h)(1) and 21C of the Securities Exchange Act of 1934, Making Findings and -

Two Market Models Powered by One Cutting Edge Technology

Two Market Models Powered by One Cutting Edge Technology NYSE Amex Options NYSE Arca Options CONTENTS 3 US Options Market 3 US Options Market Structure 4 Traded Volume and Open Interest 4 Most Actively Traded Issues 4 Market Participation 5 Attractive US Options Dual Market Structure 5 NYSE Arca & NYSE Amex Options Private Routing 6-7 NYSE Arca Options - Market Structure - Trading - Market Making - Risk Mitigation - Trading Permits (OTPs) - Fee Schedule 8-10 NYSE Amex Options - Market Structure - Trading - Market Making - Risk Mitigation - Trading Permits (ATPs) - Fee Schedule - Marketing Charge 10 Membership Forms US Options Market The twelve options exchanges: NYSE Arca Options offers a price-time priority trading model and The US Options market is one of the largest, most liquid and operates a hybrid trading platform that combines a state-of-the- fastest growing derivatives markets in the world. It includes art electronic trading system, together with a highly effective options on individual stocks, indices and structured products open-outcry trading floor in San Francisco, CA such as Exchange Traded Funds (ETFs). The US Options market therefore presents a tremendous opportunity for derivatives NYSE Amex Options offers a customer priority trading model traders. and operates a hybrid trading platform that combines an Key features include : electronic trading system, supported by NYSE Universal Trading Twelve US Options exchanges Platform technology, along with a robust open-outcry trading floor at 11 Wall Street in New York, NY Over 4.0 billion contracts traded on the exchanges in 2012 BATS Options offers a price-time priority trading model and Over 15 million contracts traded on average operates a fully electronic trading platform per day (ADV) in 2012 The Boston Options Exchange (BOX) operates a fully electronic Over 3,900 listed equity and index based options market The Penny Pilot Program was approved by the SEC in January The Chicago Board of Options Exchange (CBOE), launched in 2007. -

Американський Долар» План Лекції 1. Introduction 2. Doll

Лекція №1 Тема лекції: «Американський долар» План лекції 1. Introduction 2. Dollars in Circulation 3. Faces and Symbols on Dollar Bills 4. Dollar Coins 5. The history of American currency Література: 1. Орел Ю., Артюхова І.Починаємо вивчати бізнес: Навчально-методичний посібник. – Дніпропетровськ: Видавництво ДАУБП, 2001. 2. https://www.factmonster.com/math/money/us-money-history 3. https://www.xe.com/currency/usd-us-dollar 4. https://www.uscurrency.gov/history 5. https://www.scholastic.com/teachers/articles/teaching-content/history-american- currency/ 6. http://time.com/5383055/dollar-bill-design-history/ Зміст лекції 1. Introduction The dollar is the basic unit of U.S. currency. It has been so since 1792. That year the United States began its own coinage system. Before then, the most accepted coin was the Spanish peso. Americans called it the Spanish dollar. The value of a Spanish peso was eight reales (pronounced ray-AHL-ays). To make change for an eight-reales coin, merchants would cut the coin into smaller pieces. The change might be one-half (four reales), one-quarter (two reales), or one-eighth (one real, also called one bit). This is the origin of "pieces of eight," a familiar phrase in pirate tales. Americans were used to seeing prices stated in Spanish dollars. The United States thus selected the dollar as its basic unit. Thomas Jefferson thought that dividing money by eight was impractical. As a result, Congress adopted the decimal system. In this system each dollar is divided into 100 cents. 2. Dollars in Circulation The United States Treasury Department produces U.S. -

Chicago Mercantile Exchange Holdings Inc

PROSPECTUS 4,751,070 Shares CLASS A COMMON STOCK Chicago Mercantile Exchange Holdings Inc. is offering 3,000,000 shares of Class A common stock and the selling shareholders are offering 1,751,070 shares of Class A common stock. This is our initial public offering, and there has been no organized public market for our Class A common stock. Chicago Mercantile Exchange Holdings Inc. will not receive any proceeds from the sale of shares by the selling shareholders. Our Class A common stock has been approved for listing on The New York Stock Exchange under the symbol ``CME.'' Investing in our common stock involves risks. See ``Risk Factors'' beginning on page 7. PRICE $35 A SHARE Underwriting Proceeds to Chicago Discounts and Mercantile Exchange Proceeds to Selling Price to Public Commissions Holdings Shareholders Per Share .......... $35.00 $2.45 $32.55 $32.55 Total ............. $166,287,450.00 $11,640,121.50 $97,650,000.00 $56,997,328.50 Chicago Mercantile Exchange Holdings Inc. has granted the underwriters the right to purchase up to an additional 712,660 shares to cover over-allotments. The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense. Morgan Stanley & Co. Incorporated expects to deliver the shares to purchasers on December 11, 2002. MORGAN STANLEY UBS WARBURG SALOMON SMITH BARNEY JPMORGAN WILLIAM BLAIR & COMPANY December 5, 2002 Chicago Mercantile Exchange futures and options on futures are traded on CME's open outcry trading floors in Chicago, electronically on CME's GLOBEX® platform and through privately negotiated transactions. -

Nyse® Factset U.S. Infrastructure Index

TICKER: NYFSINF NYSE® FACTSET U.S. INFRASTRUCTURE INDEX U.S. INFRASTRUCTURE: AN EMERGING OPPORTUNITY The NYSE FactSet U.S. Infrastructure Index (NYFSINF) The index is modified equal-weighted and is reconstituted is an equity benchmark designed to track the performance annually after the close of the third Friday in March of companies involved in the U.S. infrastructure value each year. Index constituent weights are rebalanced chain, from asset owners and operators to their upstream quarterly after the close of the third Friday in March, June, enablers. Within the asset owner and operator category, September, and December each year. the index covers three asset types: energy transportation NYSE FACTSET INDEX SOLUTION and storage, railroad transportation, and utilities. Within The NYSE® FactSet U.S. Infrastructure Index is calculated the enabler category, the index covers three upstream and maintained by ICE Data Indices, LLC based on a verticals: construction and engineering services, methodology developed by FactSet. The methodology machineries, and materials. leverages FactSet RBICS (Revere Business Industry This holistic approach to defining infrastructure not only Classification System) industry classifications to determine retains the attractive attributes of traditional equity Infrastructure Enablers and Infrastructure Asset Owners infrastructure investing – stable cash flows, high barriers to and Operators. entry and acting as an inflation hedge – but also improves potential capital appreciation by including the more direct beneficiaries -

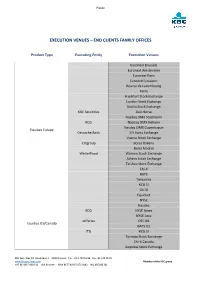

Execution Venues – End Clients Family Offices

Public EXECUTION VENUES – END CLIENTS FAMILY OFFICES Product Type Executing Entity Execution Venues Euronext Brussels Euronext Amsterdam Euronext Paris Euronext Lissabon Bourse de Luxembourg Xetra Frankfurt Stock Exchange London Stock Exchange Dublin Stock Exchange KBC Securities Oslo Borse Nasdaq OMX Stockholm KCG Nasdaq OMX Helsinki Nasdaq OMX Copenhague Equities Europe Deutsche Bank SIX Swiss Exchange Vienna Stock Exchange Citigroup Borsa Italiana Bolsa Madrid Winterflood Warsaw Stock Exchange Athens Stock Exchange Tel Aviv Stock Exchange Chi-X BATS Turquoise KCG SI Citi SI Equiduct NYSE Nasdaq KCG NYSE Amex NYSE Arca Jefferies OTC BB Equities US/Canada BATS US ITG KCG SI Toronto Stock Exchange Chi-X Canada Aequitas Stock Exchange KBC Securities NV Havenlaan 2 – 1080 Brussels Tel. +32 2 429 16 86 Fax +32 429 98 39 www.kbcsecurities.com Member of the KBC group VAT BE 0437.060.521 RLP Brussels IBAN BE77 4096 5474 0142 BIC KREDBE BB Public Product Type Executing Entity Execution Venues Tokyo Stock Exchange Instinet Hong Kong Stock Exchange Singapore Stock Exchange Equities Asia/Afrika Jefferies Sydney Stock Exchange Chi-X Johannesburg Stock Exchange Euronext Brussels KBC Securities Euronext Amsterdam Structured products Deutsche Bank Euronext Paris Banca IMI Frankfurt Stock Exchange Borsa Italiana Euronext Brussels KBC Securities Euronext Amsterdam Euronext Paris Listed Bonds Frankfurt Stock Exchange Banca IMI Bourse de Luxembourg Borsa Italiana Bloomberg MTF OTC Bonds KBC Bank Banca IMI Listed NAV-funds KBC Securities Euronext Amsterdam OTC NAV-funds Transfer Agents Euronext Brussels Euronext Amsterdam Euronext Paris KBC Securities Eurex Intercontinental Exchange Societe Generale AMEX Listed derivatives BATS AFS Boston Stock Exchange CBOE Merrill Lynch ISE Nasdaq NYSE Arca Philadelphia Stock Exchange KBC Securities NV Havenlaan 2 – 1080 Brussels Tel. -

Price Discovery in the U.S. Stock Options Market

Price Discovery in the U.S. Stock Options Market YUSIF E. SIMAAN AND LIUREN WU YUSIF E. SIMAAN In the U.S., several exchanges with different market the Securities and Exchange Commission is an associate professor of microstructure designs compete to provide quotes and (SEC) approved a plan to electronically link finance in the Graduate attract order flow on a common set of stock options. the various market centers (the “Linkage School of Business at Fordham University in In this article, we analyze how the different Plan”). The SEC has also adopted more strin- New York, NY. microstructure designs affect the price discovery of gent quoting and disclosure rules on the options [email protected] options quotes and how they alter the flow of options market. The “firm quote” rule was applied to trading activities over time. We find that the fully the options markets on April 1, 2001. LIUREN WU electronic exchange system at the International Secu- At the time of our study, five options is an associate professor of rities Exchange (ISE), where several market makers exchanges compete to provide quotes and economics and finance in the Zicklin School of provide quotes independently and anonymously to attract order flows on a common set of stock Business, Baruch College at compete for order flow within the exchange, generates options: the American Stock Exchange the City University of New options quotes that are the most informative and the (AMEX), the Chicago Board of Options York in New York, NY. most executable, with the narrowest bid–ask spreads. Exchange (CBOE), the International Securi- [email protected] Over time, the ISE’s leading quote quality has ties Exchange (ISE), the Pacific Stock attracted order flow to the exchange, and has com- Exchange (PCX), and the Philadelphia Stock pelled other exchanges to pursue technology Exchange (PHLX).